Be Your Own Bank: How Infinite Banking Works

The Short Version

To be your own bank, you overfund a dividend-paying whole life policy, build cash value, then borrow against it for big purchases while that cash value keeps growing. It is real and it works. It is also slow, takes discipline, and is not for everyone. No magic, no guaranteed riches.

You have probably seen the videos. Somebody in a nice car promising you can "be your own bank" and fire your lender forever. The phrase sounds too good to be true, so let's slow down and talk about what is real and what is hype. The infinite banking concept is a legitimate strategy, but it is buried under more marketing nonsense than almost anything else in personal finance.

Watch: Is infinite banking a scam? The honest truth from a licensed agent.

The idea is real. The over-promising around it is not. In this guide I will walk you through how to be your own bank step by step, the honest math, what it actually costs, the part most of those videos skip, who this is not for, and how to tell a good policy design from a bad one. By the end you will be able to spot the hype and judge the real thing on its merits.

What this guide covers

- What "be your own bank" really means

- How the infinite banking concept works

- How the policy is engineered for banking

- The borrowing mechanics, plainly

- How to start, step by step

- The honest pros

- The honest cons

- Your policy vs a traditional bank

- What it costs to run your own bank

- Who it actually fits

- Common myths and the scam question

- Frequently asked questions

What "be your own bank" really means

The infinite banking concept came from a man named R. Nelson Nash, a forester and finance thinker who wrote a book called Becoming Your Own Banker back in 2000. The core idea is simple. Banks make money by holding your cash and lending it out, capturing the spread between what they pay you and what they charge you. Nash asked a sharp question: what if you ran a small version of that same system for your own household, so that you, not a bank, captured the financing in your life?

You do it with a specially structured, dividend-paying whole life insurance policy. You put money in. It builds cash value you can use. When you need cash for a truck, a roof, a tax bill, or a business expense, you borrow against the policy instead of going to a bank. You pay yourself back on your own terms. Over a lifetime, the average family finances an enormous amount of money, through car loans, mortgages, and credit. Nash's argument was that recapturing even part of that financing inside a system you control is worth real money over decades. That is the whole concept in one breath. Business owners use the same kind of policy to fund key person insurance and a buy-sell agreement, so the company controls the capital instead of a lender.

It is important to be clear about one thing up front: "be your own bank" is a marketing phrase, not a literal description. You are not chartering a bank, and you cannot do everything a bank does. What you are really doing is building a private, liquid pool of money inside a life insurance policy and using policy loans as your personal line of credit. The product underneath is old, boring, and time-tested. Whole life insurance has been around well over a hundred years, and as the Insurance Information Institute describes, it is the type of permanent coverage that builds cash value you can borrow against. There is nothing new or secret about it. The only thing that is new is the deliberate way it is funded and used.

Tax-advantaged growth with a floor against losses. Quick and free.

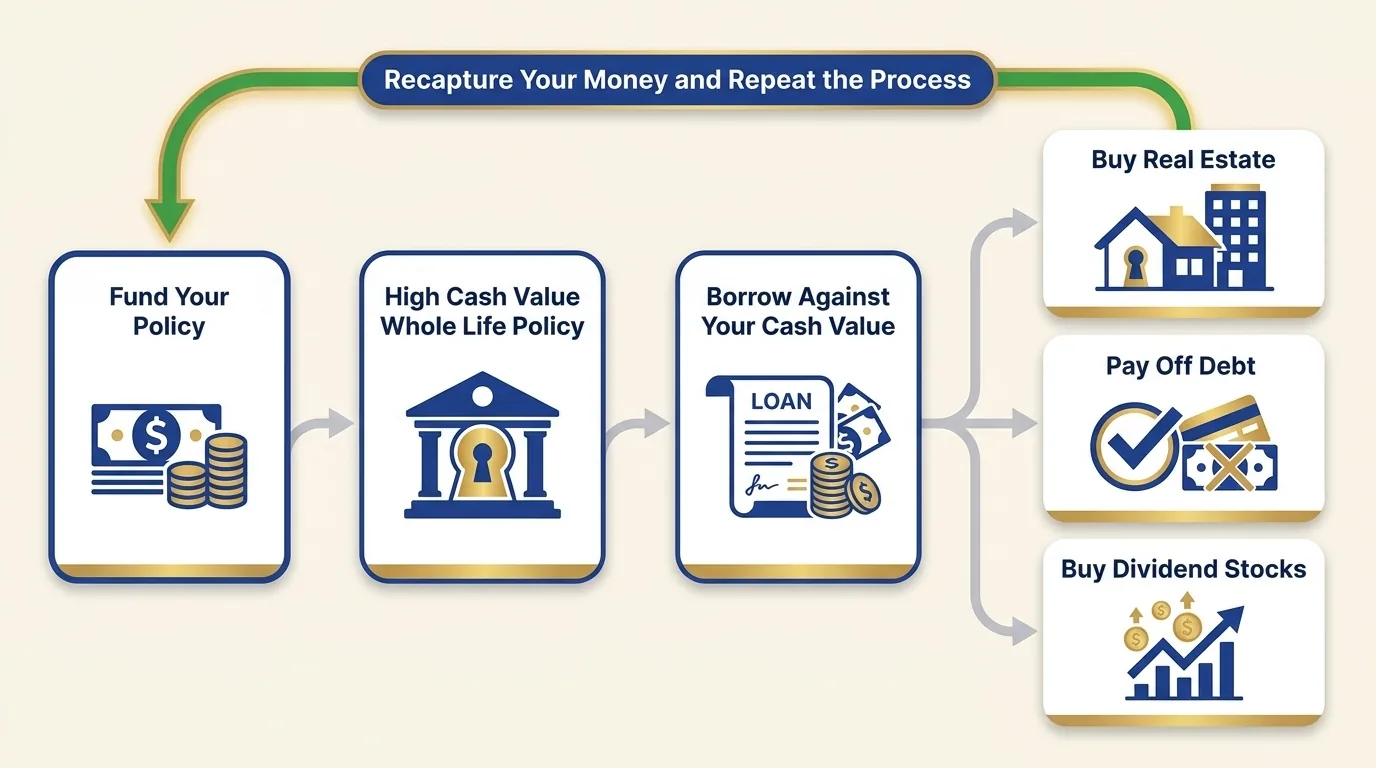

How the infinite banking concept works

Strip away the jargon and the strategy runs on a simple, repeatable loop. Once you understand the loop, every other detail falls into place.

- Step one, fund the policy. You pay premiums into a whole life policy that has been structured to build cash value quickly rather than to maximize the death benefit. A large slice of each premium goes straight to work as accessible cash value.

- Step two, let it grow. Your cash value grows on a guaranteed schedule, and the company may pay dividends on top of that. The longer it compounds, the more there is to borrow against.

- Step three, borrow against it. When you need money, you request a policy loan. The insurer hands you cash and uses your cash value as collateral. Crucially, your cash value stays in the policy and keeps growing as if you never touched it.

- Step four, put the money to work. You use the loan for whatever you would have financed anyway, a vehicle, a home repair, inventory for a business, an investment property down payment.

- Step five, pay yourself back. You repay the loan on a schedule you set, with interest going to the insurer. As you repay, your available borrowing capacity is restored, and the cycle starts again.

That is the engine. You become the financing department for your own life. Instead of sending interest to a bank and never seeing it again, you keep the money flowing through a system you own. The discipline of paying yourself back is what makes it work, and the lack of that discipline is what makes it fail. Notice that nothing in this loop promises a high investment return. The growth on the cash value is steady and modest by design. The power, if there is power here, is in the cash flow and the control, not in beating the stock market.

How the policy is engineered for banking

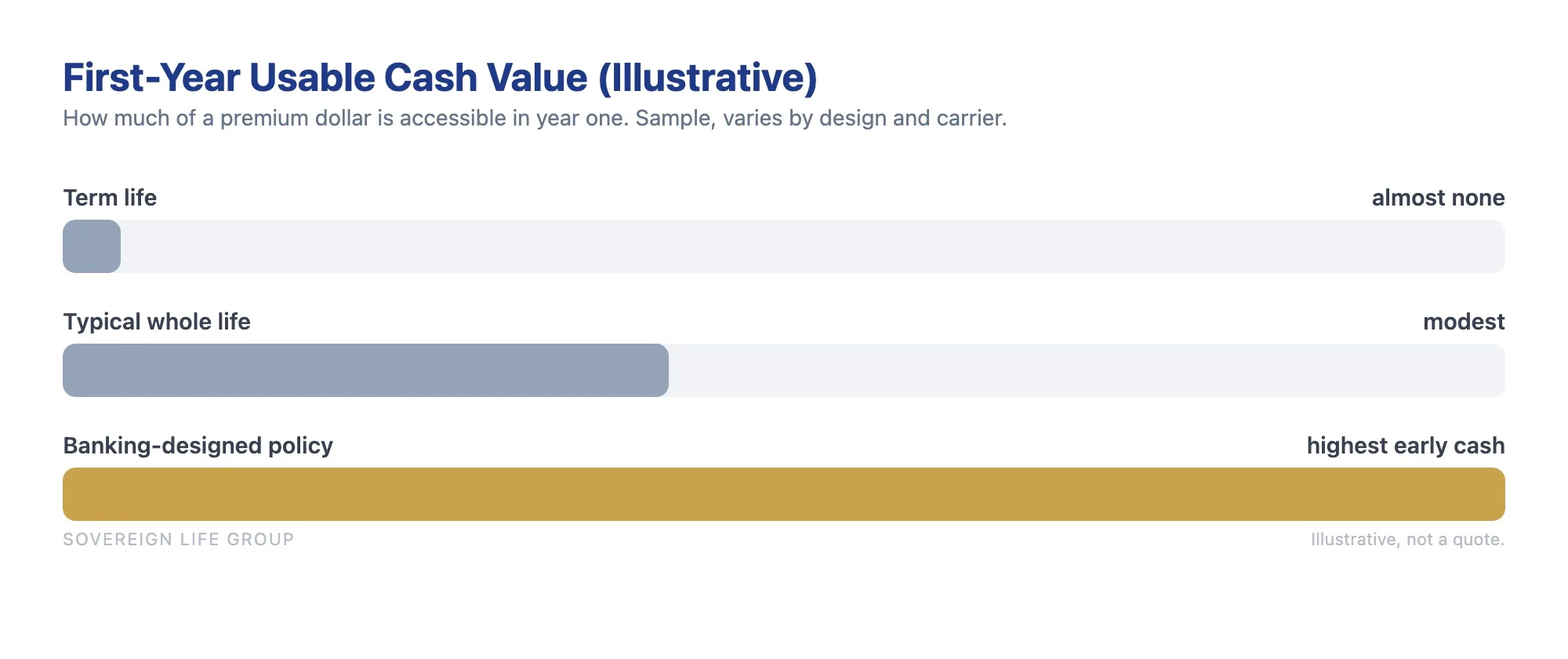

This is the part that separates a good banking policy from an expensive mistake, and it is where most of the online hype goes quiet. A normal, off-the-shelf whole life policy is not ideal for this job. It is built to maximize the death benefit, so the cash value grows slowly in the early years and the agent earns a larger commission. For banking, you want close to the opposite emphasis: more cash value sooner, even though that means a smaller commission for whoever sells it.

The base policy plus paid-up additions

An agent who knows what they are doing structures the policy around two parts working together:

- A base whole life policy. This is the foundation. It guarantees lifelong coverage and a steady, guaranteed climb in cash value. It also carries the bulk of the policy's costs in the early years.

- A paid-up additions rider, often called PUA. This is the engine that makes banking work. A paid-up addition is a small chunk of extra, fully paid-up insurance you buy with additional dollars, and almost all of that money shows up as cash value right away. Loading a policy with PUA is what gets your cash value working early instead of years down the road.

The art is in the premium split. A policy designed for banking leans heavy on paid-up additions and lighter on the base, often something in the range of a small base with a large additions allowance. Get that mix right and your cash value grows far faster than a standard policy in the first decade. Get it wrong, with too much base and little or no PUA, and you are simply paying for expensive insurance with a slow-building side account. This is why the design matters more than the brand name on the policy.

The MEC limit you cannot cross

There is a ceiling on how much you can stuff into a policy, and it is set by tax law, not by the insurer's generosity. If you overfund a policy past a federal threshold, the IRS reclassifies it as a Modified Endowment Contract, or MEC. Once a policy becomes a MEC, the tax-friendly treatment of loans and withdrawals changes, and you can lose much of the reason you built it in the first place. The IRS lays out how this classification works in its guidance on taxable and nontaxable income. A properly designed overfunded whole life insurance policy is funded right up to the line that keeps it tax-advantaged, but not over it. This is a technical job, and it is one of the clearest reasons to work with someone who does this regularly rather than building it yourself from a video.

If the difference between whole life and the other permanent options is still fuzzy, our breakdown of term versus whole life insurance lays out where each one fits before you ever get to banking.

The borrowing mechanics, plainly

Here is where people get confused, so let me be careful. When you take a policy loan, you are not actually withdrawing your own cash. You are borrowing from the insurance company, and your cash value sits there as collateral for that loan, which only works because of how cash value life insurance builds and can be borrowed against.

That detail is the whole point. Because the money never leaves the policy, your full cash value keeps earning growth and any dividends the company pays. You get to use the cash and keep it compounding at the same time. People call this "uninterrupted compounding," and it is the closest thing to a free lunch in this strategy. Even so, it has a catch worth understanding.

The catch is interest. The insurance company charges you interest on the loan. The rate is set by the policy and is usually reasonable, and there is no credit check, no application drama, and no approval process, because you are borrowing against your own collateral. The loan does not show up on your credit report, and you decide the repayment schedule. But interest is real, and it compounds against you if you let a loan run for years without paying it down. Some policies are "non-direct recognition," meaning your cash value earns the same dividend whether or not you have a loan out, and some are "direct recognition," which adjusts the dividend on the borrowed portion. Neither is automatically better, but it is a question worth asking before you sign.

There is also a real, if uncommon, risk to respect: if you borrow aggressively, never repay, and let loans plus interest grow larger than your cash value, the policy can lapse. A lapse can trigger a tax bill on gains you never actually pocketed. That is the worst-case outcome, and it comes from misuse, not from the tool itself. Treat the loan like a real obligation, and understanding how to borrow against your life insurance policy the right way keeps it a useful one.

How to start, step by step

If you have decided to look at this seriously, here is the practical path from interest to a working policy. None of it requires you to become an insurance expert, but all of it rewards patience.

- Handle the foundation first. Before a banking policy makes sense, you want an emergency fund in place, high-interest debt cleared, and steady income. This strategy sits on top of a solid base. It is not the base itself.

- Get clear on what the money is for. Are you financing vehicles, funding a business, smoothing irregular income, or simply building a private reserve? The job shapes how much you fund and how fast you want cash value to build.

- Set a premium you can sustain for a decade or more. This is the single most important number. Pick an amount that is comfortable in a bad year, not just a good one. The strategy punishes people who overcommit and bail early.

- Work with someone who designs for cash value. Ask directly how the policy splits base premium and paid-up additions, and how close it runs to the MEC limit. A good design answer is specific. A vague one is a warning sign.

- Fund it consistently, then leave it alone to grow. The early years are the slow years. Keep paying, let the cash value build, and resist the urge to borrow before there is enough there to matter.

- Borrow with a repayment plan, every time. When you do take a policy loan, decide up front how and when you will pay it back. The system only compounds in your favor if you actually close the loop.

To see roughly how a given premium could build cash value and borrowing power over the years, try our free infinite banking calculator. It is illustrative rather than a quote, but it makes the shape of the strategy concrete before you ever talk to anyone.

If a workplace retirement plan is part of your foundation and you are weighing where extra dollars should go, our IUL vs 401k breakdown shows how a cash-value policy and a retirement account play different roles rather than competing for the same job.

The honest pros

When the strategy fits the person, the benefits are genuine. Here is what you are actually buying.

- Real liquidity. A policy loan can be in your account in days, with no application and no underwriting. Try pulling equity out of your house that fast.

- Your money keeps working. Because you borrow against the cash value instead of pulling it out, the full balance keeps growing while you use the loan. That uninterrupted compounding is the heart of the appeal.

- Control and flexibility. You set the repayment pace. Skip a month in a tight season, double up in a strong one. The discipline is on you, which is both a pro and a con.

- Tax advantages. Cash value grows tax-deferred, and properly handled policy loans are generally not treated as taxable income. The rules are specific, so talk to a tax professional about your own situation.

- It is not tied to the stock market. The guaranteed portion does not drop when the market has a bad year. Some people value that steadiness alongside their other accounts, especially as a place to park cash they want safe but reachable.

- Privacy and simplicity. Policy loans do not appear on your credit report and do not require you to justify the purchase to a lender. For business owners and the self-employed, that quiet access can be genuinely useful.

- A death benefit underneath it all. Whatever else it does, the policy is still life insurance. Your family is protected the entire time you are building and using the cash value.

See the strategy applied to your age and goals. No pressure.

The honest cons

This is the section the hype videos leave out. Read it twice, because the trade-offs here are real and they are where people get hurt.

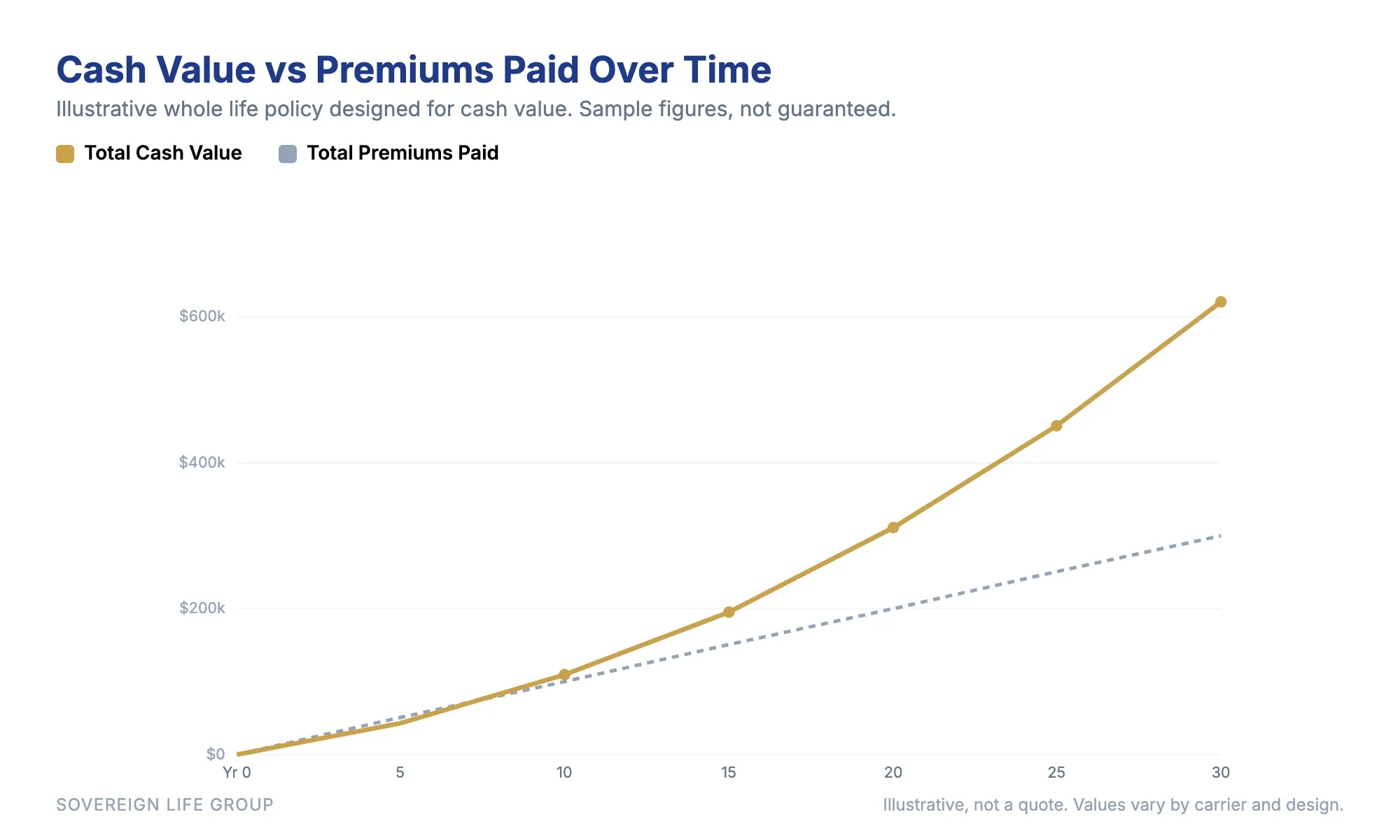

- It takes years to get going. On a well-built policy, your cash value usually does not pass the total premiums you have paid until somewhere around year seven to ten. Early on, you have put in more than you can borrow, and that gap tests people's patience.

- The costs are front-loaded. Insurance costs and commissions hit hardest in the first few years. If you cancel early, you can walk away with less than you put in. An early exit is the most common way people lose money with this strategy.

- It demands discipline. Nobody forces you to repay a policy loan. If you keep borrowing and never pay yourself back, the system stops compounding in your favor and the policy can eventually unravel or lapse.

- The growth is steady, not spectacular. The guaranteed and dividend growth is modest. This is a cash-flow and stability tool, not a high-return investment. Anyone promising you market-beating returns from a whole life policy is selling, not advising.

- It costs more than term. A properly funded banking policy is a serious monthly commitment, far more than a term policy with the same death benefit. That money is unavailable for other uses while it is funding the policy.

- Opportunity cost is real. Dollars going into premiums are dollars not going into a market account that might earn more over the long run. For someone with a long horizon and no need for liquidity, that trade may not be worth it.

- It is easy to design badly. A policy sold by someone chasing commission rather than cash value can quietly underperform for years. Bad design is common, and it is hard for a beginner to spot.

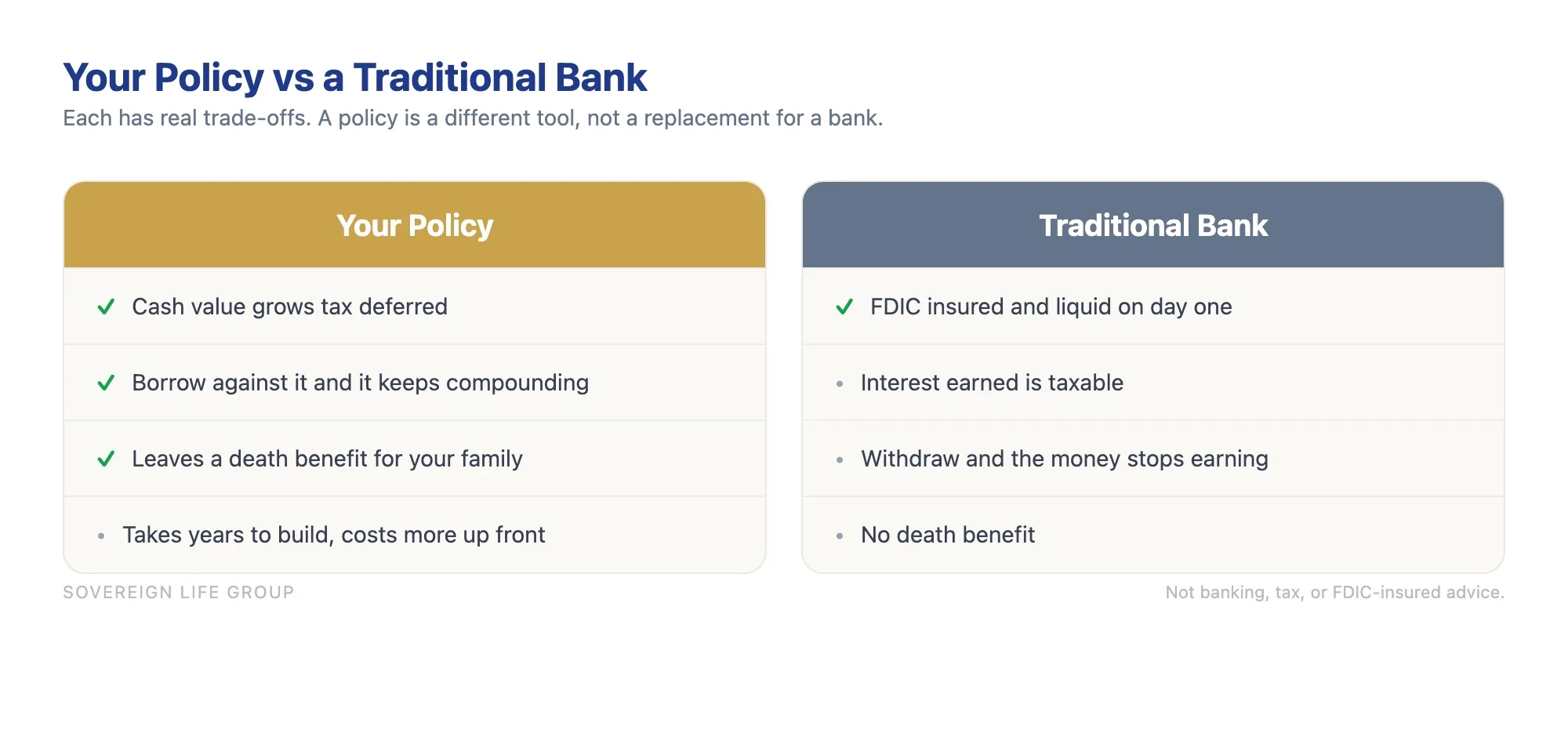

Your policy vs a traditional bank

The clearest way to see what you gain and give up is to put a policy loan next to a normal bank loan, side by side. Neither column is "better" in the abstract. They fit different situations.

| Feature | Policy loan (your own bank) | Traditional bank loan |

|---|---|---|

| Approval | No credit check; collateral is your cash value | Credit check and underwriting required |

| Speed | Often a few days, no application drama | Days to weeks, depending on the loan |

| Repayment schedule | You set the pace and timing | Fixed schedule set by the lender |

| Does collateral keep growing? | Yes, cash value keeps compounding while borrowed | No equivalent; your deposit is spent or pledged |

| Shows on credit report? | No | Usually yes |

| What if you never repay? | Loan plus interest reduces your death benefit; policy can lapse if it grows too large | Default, collections, and credit damage |

| Time to build the system | Years of funding before meaningful capacity | None; the bank's capital is already there |

Read that table honestly and the picture is balanced. The policy wins on speed, privacy, flexibility, and the fact that your collateral keeps growing. The bank wins on one big thing: it is ready today, with no years of funding required. That is the real trade. You are spending time and discipline now to build a financing tool you control later.

What it costs to run your own bank

There is no single price tag, because a banking policy is sized to you, not sold off a shelf. That said, you should walk in with realistic expectations rather than a video's fantasy.

A policy built to do real banking generally needs a meaningful, sustainable annual premium, often several thousand dollars a year and sometimes much more, funded steadily for at least a decade. The exact figure depends on your age, your health, the death benefit, how the base and paid-up additions are split, and how close the design runs to the MEC limit. What matters is not hitting a specific dollar amount. What matters is choosing a premium you can comfortably maintain through a bad year, because the strategy only works if the policy stays in force long enough to mature.

Be wary of two failure patterns. The first is underfunding, where someone buys a small policy hoping to "be their own bank" on a premium too low to ever build useful cash value. The second is overfunding relative to your real budget, where someone stretches for an impressive illustration and then cancels in year two when money gets tight, losing a chunk of what they paid in. The right number lives between those two mistakes, and finding it is most of the job.

It is also worth remembering that the policy is doing two jobs at once: building cash value and providing a death benefit. Some of what you pay is the genuine cost of insurance, not a fee being skimmed. When people compare a whole life policy to a pure savings account and call the difference "lost money," they are ignoring the coverage they are getting the entire time.

Who it actually fits

This strategy rewards a very specific person. It fits you well if you are a high-discipline saver with steady, reliable income and a long time horizon. It tends to fit business owners and real estate investors who finance things often and would rather pay interest back into their own system than to a bank. It fits people who already have the basics handled: an emergency fund in place, high-interest debt gone, and retirement contributions flowing. This is a tool you add on top of a solid foundation, not the foundation itself.

Who should skip it, at least for now

- You carry credit card debt or other high-interest balances. Pay those off first. That return is guaranteed and immediate.

- You do not have an emergency fund yet. Build that before locking money into a policy.

- Your income is unpredictable and a large monthly premium would strain you. The premium needs to survive your worst months, not just your best.

- There is any real chance you would cancel in the first few years. The early exit is exactly where people get burned by front-loaded costs.

- You are looking for the highest possible investment return. This is not that, and anyone framing it that way is not being straight with you.

If that describes you, term life and a simple savings or investing plan will serve you better right now, and there is no shame in that. Most families should start there. When you are ready to think about long-term, tax-advantaged growth, a properly built policy or an annuity can enter the conversation. A straight-shooting agent will sometimes tell you that you are not ready for this yet, and that is the agent worth keeping.

Is infinite banking a scam, or is it legit? The myths, cleared up

Because this topic is so heavily marketed, it collects myths the way a magnet collects filings. Let's clear up the big ones.

"It is a scam"

No. The underlying product, dividend-paying whole life insurance, is over a century old and regulated in every state. What deserves skepticism is the marketing, not the math. When you hear guaranteed double-digit returns, "the banks do not want you to know this," or pressure to buy immediately, you are hearing a sales pitch, not a strategy. The tool is real. Some of the people selling it are not being honest about the trade-offs.

"You are getting free money by borrowing your own cash"

Not quite. You borrow from the insurer against your cash value, and you pay interest to do it. The genuine benefit is that your cash value keeps compounding while borrowed, not that the loan is free. Treat anyone who calls it free money with caution.

"It replaces your bank and your investments"

It does not, and it should not try to. Most people who use this well keep a checking account, keep an emergency fund, keep investing in the market, and add a policy as one more tool for liquidity and stability. It is an addition to a financial plan, not a replacement for one.

"Any whole life policy will do"

False, and this myth costs people the most. A standard policy not designed for cash value can take far longer to become useful for banking. The paid-up additions design and careful funding are what make the strategy work, which is why the design conversation matters more than the carrier's name. If you want to see how the carriers stack up, our guide to the best whole life insurance for infinite banking walks through what actually separates a strong banking policy from a weak one.

See the pattern? Every myth either oversells the upside or hides the work involved. The honest version of infinite banking is less exciting and far more trustworthy: a patient, private cash-flow system for people who already live below their means.

What about Dave Ramsey's take on infinite banking?

Dave Ramsey is famously against whole life insurance, and by extension the infinite banking concept. His core argument is fair and worth hearing: whole life costs far more than term, the returns are modest, and most families would build more wealth buying term and investing the difference. For the average household carrying debt and just starting to save, that advice is sound, and I would tell many of the same people the same thing.

Where the picture gets more nuanced is the specific person this strategy is built for. Ramsey speaks to the masses who need a simple, disciplined path out of debt and into investing. Infinite banking is not for that person. It is a tool for someone who already has the foundation handled, an emergency fund in place, high-interest debt gone, retirement funded, and who wants a private, liquid pool of capital they control. Both things can be true: term and investing is the right call for most people, and a well-designed banking policy can still serve a disciplined saver who has moved past that stage. The honest answer is not "Ramsey is wrong," it is "Ramsey is right for most people, and this is a tool for the exception."

Wondering if you're a fit?

Fifteen minutes, no pressure. We will look at your income, your goals, and whether this strategy actually makes sense for you, or whether something simpler does first.

Get a Quote Book a 15-Min Strategy Review Prefer to read more first? Browse the families coverage overview.Frequently asked questions

Is the infinite banking concept a scam?

No. It is a real strategy built on dividend-paying whole life insurance, which has existed for over a century. The problem is how it gets sold online. The product is legitimate, but the hype around guaranteed riches is not. Done right it is a slow, disciplined cash-flow tool, not a get-rich scheme.

Is infinite banking legit?

Yes. The strategy is built on dividend-paying whole life insurance, a regulated product that has existed for over a century. What is not legitimate is some of the marketing around it, such as promises of guaranteed double-digit returns or pressure to buy immediately. The tool is real. Judge the person selling it by whether they are honest about the trade-offs.

What does Dave Ramsey say about infinite banking?

Dave Ramsey is against whole life insurance and infinite banking. His argument is that whole life costs far more than term with modest returns, and most families build more wealth buying term and investing the difference. That is sound advice for most people. Infinite banking is a tool for a narrower group who already have an emergency fund, no high-interest debt, and funded retirement, and who want private, controllable liquidity on top of that foundation.

How much money do you need to be your own bank?

There is no single number, but a policy built for banking usually needs a meaningful, sustainable annual premium, often several thousand dollars a year, that you can keep funding for at least a decade. The key is not the dollar amount, it is whether the premium is comfortable for the long haul. Overcommitting and canceling early is the most common way people lose money with this strategy.

How do you become your own bank?

You become your own bank by overfunding a whole life policy built for high early cash value, then borrowing against that cash value when you need money instead of going to a lender. You repay the loan on your own terms while the full cash value keeps growing. The steps are simple: fund the policy properly, let the cash value build, borrow against it, and repay so the system keeps working.

Can you really be your own bank?

Yes, within limits. You are not printing money, you are using a properly designed whole life policy as a private financing system. You can borrow against your cash value for a car, real estate, a business, or an emergency without a credit check, and the money keeps compounding while the loan is out. It only works if the policy is structured correctly and you actually repay your loans, so it is a discipline, not a loophole.

How long does it take to be your own bank?

On a well-built policy it usually takes several years before your cash value passes the total premiums you have paid in. Many policies reach that break-even point somewhere around year seven to ten. This is a long game, not a quick one.

Do I really borrow my own money with a policy loan?

Not exactly. You borrow from the insurance company and use your cash value as collateral. Your full cash value keeps earning while the loan is out, but you still pay interest on the loan. If you never repay it, the unpaid balance plus interest reduces your death benefit.

Is infinite banking better than investing in the stock market?

They do different jobs, so it is not a fair head-to-head. The market is built for long-term growth and carries more risk and volatility. A banking policy is built for steady, predictable cash value you can borrow against. Most people who use this strategy keep their market investments and add a policy for liquidity and stability, rather than choosing one over the other.

Who is infinite banking not a good fit for?

It is a poor fit if you have high-interest debt, no emergency fund, an unstable income, or you might cancel the policy in the first few years. The fees are front-loaded, so an early exit can leave you with less than you paid in. Term life and a basic savings plan serve most families better first.

The infinite banking concept is not a shortcut to wealth, and anyone who frames it that way is doing you a disservice. Used right, it is a patient, private cash-flow system for people who already live below their means. That is the whole truth of it, no shinier than that. If you want a clear, no-pressure look at whether it fits your situation, you can find a real human and a straight answer at Sovereign Life Group, your life insurance strategist.

Want to talk it through first? You can always reach out with a question, or keep reading over on our news page.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Policy loans reduce the death benefit and available cash value. Cash values and dividends are not guaranteed. Guarantees are subject to the claims-paying ability of the issuing insurance company.