Cash Value Life Insurance: How It Works and How to Use It

The Short Version

Cash value life insurance is permanent coverage with a built-in savings account that grows tax-deferred. Part of your premium funds the death benefit, and part builds a pool of money you can borrow against or withdraw while you are alive. It is slower to grow and costs more than term life, so it fits people who want lifelong protection plus a flexible, tax-advantaged place for money, not someone who just needs the most coverage for the least cost.

Most people meet the phrase "cash value life insurance" in a sales pitch, which is a shame, because it is one of the more useful and most misunderstood tools in personal finance. The promise sounds almost too good: a life insurance policy that also builds money you can use while you are still here. The reality is more grounded than the hype and more interesting than the skeptics admit. This guide walks through how cash value life insurance actually works, which policies build it, what the money costs you to access, how the taxes really land, and the honest trade-offs that a good agent should put on the table before you sign anything.

I write this as a licensed agent, not a pitchman. By the end you should be able to tell whether this kind of policy fits your life or whether a simpler, cheaper option does the same job better. Both answers happen often, and both are fine.

What this guide covers

- What cash value life insurance actually is

- How cash value works inside the policy

- Which policies build cash value

- A worked example over 30 years

- Guaranteed vs non-guaranteed value

- How to access your cash value

- How cash value is taxed

- What happens to the cash value when you die

- The honest costs and trade-offs

- Who it fits and who it does not

- How to use cash value well

- Frequently asked questions

What cash value life insurance actually is

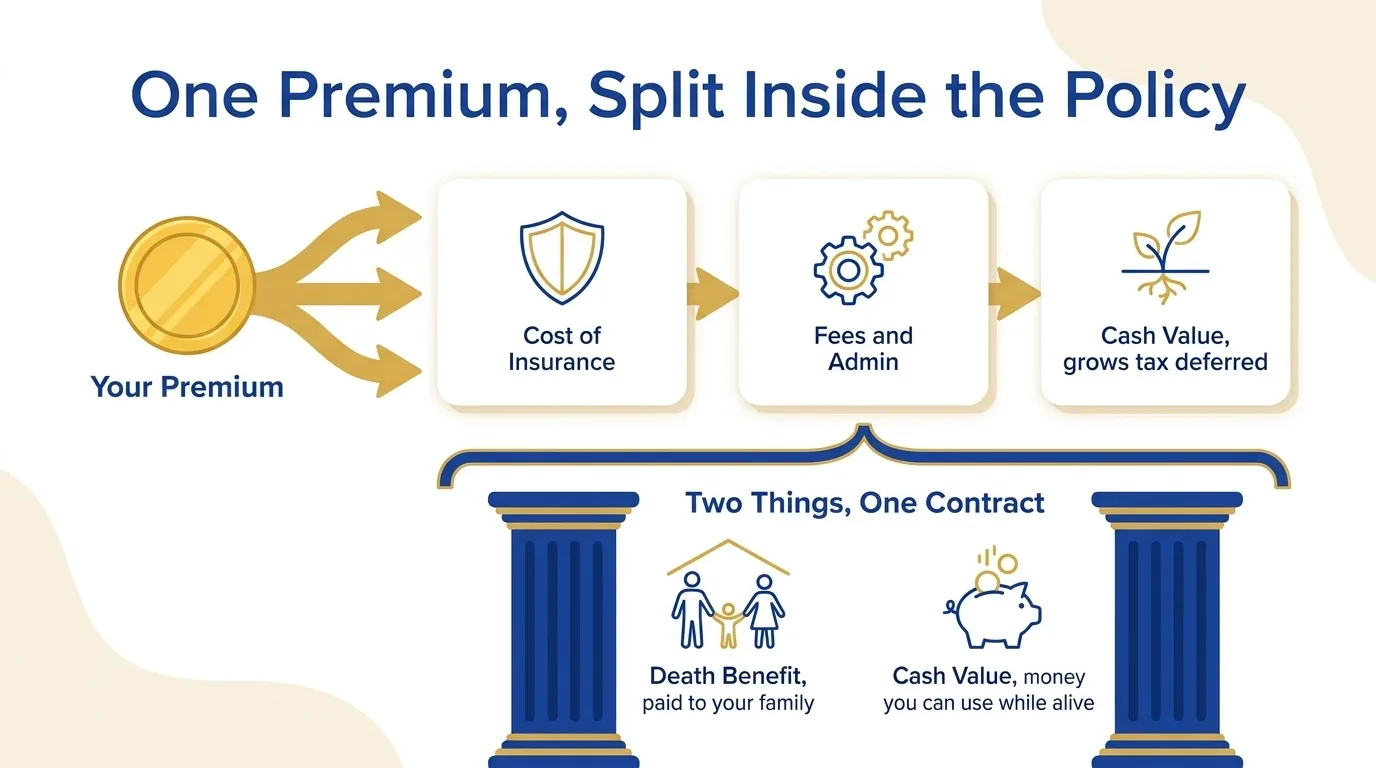

Cash value life insurance is any permanent life insurance policy that builds a pool of money over time on top of paying a death benefit. "Permanent" means it is designed to last your whole life, not a set number of years, as long as you keep funding it. The death benefit is the part everyone understands: when you pass away, your beneficiary gets a tax-free check. The cash value is the part that confuses people, so let us name it plainly.

The cash value is a savings-like account that lives inside the policy. Each time you pay a premium, the insurer splits the money. Some goes toward the actual cost of insuring your life, some covers fees and the cost of running the policy, and the rest is credited to your cash value, where it grows over the years. Because that growth happens inside a life insurance contract, it is generally allowed to compound without you owing tax on it each year, which is one of the features that makes these policies appealing for long-term planning.

Think of it as two things sharing one contract: protection for the people who depend on you, and a slow-building reserve of money you can reach during your lifetime. Term life, by contrast, is only the first thing. It rents you a death benefit for ten, twenty, or thirty years and builds nothing on the side. That is exactly why term costs less and why cash value life insurance costs more.

Tax-advantaged growth with a floor against losses. Quick and free.

How cash value works inside the policy

To understand how cash value works, follow a single premium dollar as it enters the policy. In the early years, a large share of what you pay goes toward the cost of insurance, administrative charges, and the commission that funds the agent and carrier work behind the policy. Only what is left over lands in the cash value. That is why these policies start slow. People who cancel in year two and feel cheated were usually never told that the first couple of years are front-loaded with costs.

As the years pass, the math flips. The amount of pure insurance the policy has to buy each year shrinks, because your growing cash value is quietly doing some of the heavy lifting behind the death benefit. More of every premium dollar can then go to growth, and the balance you have already built keeps earning on itself. This is compounding, and it is the reason cash value policies are a long game. The fifteenth year usually looks far healthier than the third.

Where the growth comes from

How your cash value grows depends entirely on the type of policy, which we break down in the next section. In broad strokes, the money grows in one of three ways: a fixed interest rate set by the insurer, an interest rate linked to the movement of a market index with a floor that limits downside, or the performance of investment subaccounts you choose. The first is the most predictable, the last is the most exposed to market risk, and the middle sits in between. None of them are a checking account, and none should be treated like an emergency fund you can drain on a whim.

Funding matters as much as the product

Here is a point most articles skip. Two people can own the exact same policy and end up with wildly different cash value, simply because of how they funded it. Paying the minimum premium keeps the policy alive but starves the cash value. Paying more, up to the limits the tax code allows before the policy becomes a "modified endowment contract," pours more into the growth engine sooner. How a policy is designed and funded is often the difference between a sluggish account and a useful one, which is exactly what R. Nelson Nash argued in Becoming Your Own Banker and why design is a real conversation, not a brochure.

Which policies build cash value

Not every life insurance policy builds cash value. Term life does not, full stop. If you outlive a term policy, the coverage simply ends with no payout, the same way your car insurance does not refund you for the years you did not crash. Cash value only lives inside permanent policies, and there are three main families. If you want the structural comparison between renting coverage and owning it, our breakdown of term versus whole life insurance is a good companion to this section.

Whole life insurance

Whole life is the oldest and most predictable form, with roots that run back through the whole history of life insurance. The premium is fixed, the death benefit is fixed, and the whole life cash value grows at a guaranteed minimum rate set in the contract. Many whole life policies are issued by mutual companies that may also pay dividends, which are not guaranteed but, when paid, can be used to buy more coverage or add to the cash value, the same mechanism that powers overfunded whole life insurance. Whole life is the slow, steady tortoise: less upside, fewer surprises, and a contract you can largely set and forget.

Universal life insurance

Universal life adds flexibility. Within limits, you can adjust your premium and even your death benefit as life changes. The cash value typically earns a declared interest rate that the insurer can move over time, above a guaranteed floor. That flexibility is a double-edged sword: pay too little for too long and a universal life policy can run thin on cash value and risk lapsing in later years, which is the classic complaint from owners who never revisited their policy. If you are torn between the steady route and the flexible one, our breakdown of whole life vs universal life compares the two head to head.

Indexed universal life insurance

Indexed universal life, or IUL, ties the cash value growth to a market index such as the S&P 500, but you are not actually invested in the market. In a good year your credited interest is capped at a ceiling the carrier sets, and in a down year a floor, often zero, protects you from market losses to the cash value. You trade some of the market's upside for protection against its worst days. IUL is the policy most often discussed in the context of tax-advantaged retirement income; our deeper look at using an IUL for tax-free retirement income walks through how that strategy is built and where the risks hide.

Variable universal life insurance

Variable universal life, or VUL, lets you invest the cash value directly in subaccounts that work like mutual funds. The upside is real market growth potential. The downside is also real: there is usually no floor, so a bad market can shrink your cash value and, if you are not careful, threaten the policy. VUL is a securities product and suits people comfortable with investment risk inside their insurance.

| Policy type | How cash value grows | Premium | Downside risk to cash value | Best suited to |

|---|---|---|---|---|

| Whole life | Guaranteed rate, plus possible dividends | Fixed | Lowest, growth is contractually backed | People who want predictability and simplicity |

| Universal life | Declared interest rate above a floor | Flexible | Low to moderate, depends on funding | People who want premium flexibility |

| Indexed universal life | Index-linked with a cap and a floor | Flexible | Moderate, growth can be zero in flat years | People who want upside potential with downside protection |

| Variable universal life | Investment subaccounts you choose | Flexible | Highest, market losses can hit the value | Investors comfortable with market risk |

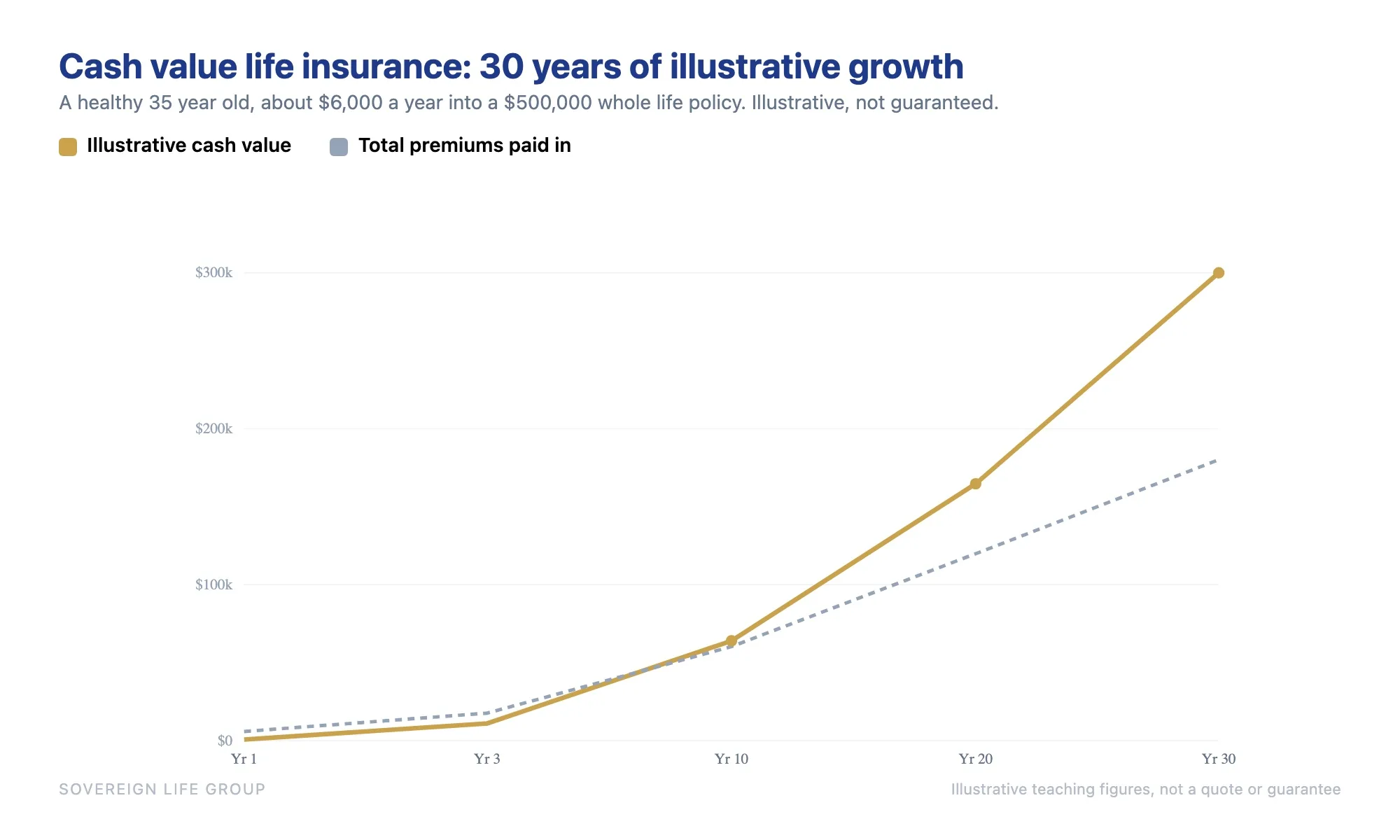

A worked example over 30 years

Numbers make this real, so here is a simplified, illustrative example. Treat it as a teaching tool, not a quote. The actual figures for any real policy depend on your age, health, the carrier, the policy design, and how it is funded, and no growth shown here is guaranteed.

Imagine a healthy 35-year-old who buys a whole life policy with a starting death benefit of about $500,000 and pays roughly $6,000 a year, or $500 a month. We are going to watch the cash value, not the death benefit. Here is the shape such a policy might take, using conservative, illustrative growth.

| Policy year | Approx. total paid in | Illustrative cash value | What is happening |

|---|---|---|---|

| Year 1 | $6,000 | $0 to $1,500 | Early costs and commission absorb most of the premium |

| Year 3 | $18,000 | Around $9,000 to $13,000 | Still building, often below what you have paid in |

| Year 10 | $60,000 | Around $58,000 to $70,000 | Roughly breaking even, growth accelerating |

| Year 20 | $120,000 | Around $150,000 to $180,000 | Compounding now clearly ahead of premiums paid |

| Year 30 | $180,000 | Around $270,000 to $330,000 | A substantial reserve you can borrow against |

Two lessons jump out of that table. First, the early years are humbling. For roughly the first decade, the cash value often trails the total you have paid in, which feels like a bad deal if you judge it by month or by year. Second, time changes everything. Once compounding takes over, the same policy that looked sleepy in year three can hold more than you put in by a wide margin in year thirty, while still carrying a death benefit the whole way.

This is the heart of why cash value life insurance rewards patience and punishes impatience. It is built for someone with a multi-decade horizon who will leave the money alone to grow and then put it to work later in life. It is a poor fit for someone who might need that cash back in three years, because surrendering early can mean walking away with less than you paid.

Guaranteed vs non-guaranteed value

This distinction is where a lot of disappointment is born, and where you most need a clear head when an illustration is in front of you. Every cash value illustration tends to show two columns: a guaranteed side and a non-guaranteed side.

The guaranteed column is what the insurer is contractually obligated to deliver, assuming you keep paying. It uses the minimum interest rate and accounts for the maximum charges the contract allows. It is the floor under the policy, the worst realistic case if everything goes the carrier's way.

The non-guaranteed column assumes things go better than the minimum: dividends get paid, interest is credited above the floor, an index performs well. It is a projection, not a promise. The single most common way people get burned is treating the non-guaranteed column as if it were the plan. A responsible agent shows you both columns and helps you make a decision that survives even if only the guaranteed side comes true.

- Guaranteed values are the contractual floor. Build your decision on these.

- Non-guaranteed values are projections based on assumptions that may not hold. Treat them as upside, not as the baseline.

- Dividends, caps, and crediting rates can and do change. Ask what the policy still does for you if they move against you.

How to access your cash value

The whole point of building cash value is that you can use it while you are alive. There are three main doors, and they behave very differently. Knowing the difference is the line between a tool that serves you and a mistake that quietly damages your policy.

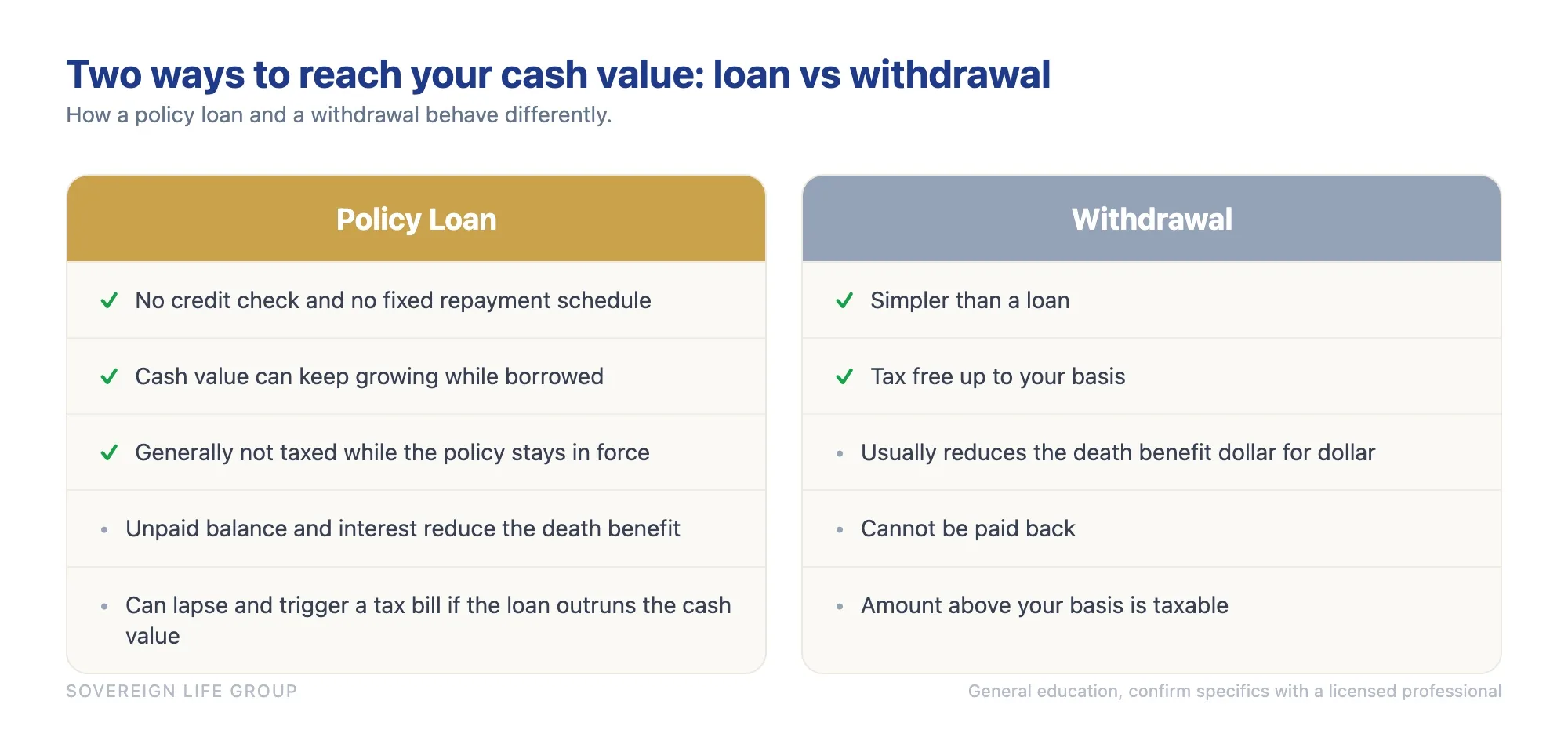

Policy loans: borrow against life insurance

The most talked-about option is a policy loan. When you borrow against life insurance, you are not actually withdrawing your own money. The insurer lends you cash and uses your policy as collateral, which is why there is no credit check, no application to deny, and no fixed repayment schedule. In many policies your full cash value keeps earning as if the loan were not there, because the borrowed money technically comes from the insurer's general account, not your account.

That is the appeal, and it is genuine. The catch is discipline. The loan accrues interest, and any unpaid balance plus interest is subtracted from the death benefit if you pass away with the loan outstanding. Worse, if a loan grows large enough to consume the cash value, the policy can lapse, and a lapsed loan can trigger a surprise tax bill. Loans are a feature, not free money. Used well they are powerful; used carelessly they can hollow out the very policy that created them.

Withdrawals

You can also withdraw cash value directly. Up to the amount you have paid in, your cost basis, a withdrawal is generally tax-free. Withdrawals are simpler than loans, but they usually reduce your death benefit dollar for dollar, and in some policy types they can have a larger effect on the policy than the amount you take out. Once you withdraw past your basis, the excess is typically taxable. Withdrawals are best thought of as permanent, while loans can be paid back.

Surrender

The last door is the exit. Surrendering the policy cancels it entirely and pays you the cash surrender value, which is the cash value minus any surrender charges the carrier applies in the early years. Surrender ends your coverage, so it is a last resort, not a strategy. Any amount you receive above your total premiums paid is taxed as ordinary income. If you no longer need the policy, there may be smarter moves than a plain surrender, including a tax-advantaged exchange into another policy or an annuity, which is a conversation worth having before you cancel anything.

| Method | Coverage stays? | Repayable? | Effect on death benefit | Typical tax treatment |

|---|---|---|---|---|

| Policy loan | Yes, if managed | Yes | Reduced by any unpaid loan balance | Generally not taxed unless the policy lapses |

| Withdrawal | Yes, but reduced | No | Usually reduced dollar for dollar | Tax-free up to basis, then taxable |

| Surrender | No, it ends | No | Gone, the policy is cancelled | Gains above basis taxed as ordinary income |

See the strategy applied to your age and goals. No pressure.

How cash value is taxed

The tax treatment is a big part of why these policies exist in financial plans, so it is worth getting right rather than relying on slogans. Three rules cover most situations.

First, growth is tax-deferred. As long as the money stays inside the policy, the gains in your cash value are not taxed each year the way a bank account or a taxable brokerage account would be. That uninterrupted compounding is a real advantage over decades.

Second, loans are generally not a taxable event while the policy stays in force. This is the mechanism behind the "tax-advantaged income" language you hear, because borrowing against cash value can let you access money without triggering income tax, provided the policy is structured and maintained properly. The phrase doing the heavy lifting there is "properly." A policy that lapses with a large loan can turn what looked like tax-free access into a taxable surprise.

Third, the death benefit is income-tax-free to your beneficiaries in the vast majority of cases. That is true of life insurance generally, not just cash value policies. For a neutral, plain overview of how policies and their values are taxed, the Insurance Information Institute is a good place to read up, and the IRS publishes the official rules on life insurance proceeds. None of this is tax advice for your situation, and the details can change, so a quick check with a tax professional before you act is always the safe move.

What happens to the cash value when you die

Here is the question almost every brochure dodges, and it is the one that surprises families most. With most traditional cash value policies, when you pass away your beneficiary receives the death benefit, and the insurer keeps the remaining cash value. It can feel like the cash disappears, but here is what is really happening: the cash value was funding the death benefit from the inside the whole time. The two were never fully separate pools you could collect twice.

An example makes it concrete. Say you have a $500,000 death benefit and $120,000 of cash value when you pass away. On a standard policy, your family receives the $500,000, and the $120,000 was part of what made that benefit possible. They do not receive $620,000. This is normal and is not a trick, but it is essential to understand, because it changes how you should think about using the cash value during your lifetime.

There is a flip side. Some policies and riders are built to pay some or all of the cash value on top of the death benefit, sometimes called an increasing death benefit option. It costs more, and it changes the math, but it exists for people who specifically want both. The lesson is the same one that runs through this whole guide: the structure of the policy decides the outcome, so the structure deserves real attention before you buy.

The practical implication is freeing once you see it. If the insurer keeps the cash value at death anyway on a standard policy, then leaving a large cash value untouched "to be safe" can mean dying with money you could have used. Many strategies are built precisely to put that cash value to work during life, through loans or income, rather than letting it sit. That is the bridge to the strategy that gets the most attention, the idea of using a policy as your own private financing system, which our guide to the be your own bank infinite banking concept unpacks in full.

The honest costs and trade-offs

An article that only lists benefits is an advertisement. Cash value life insurance carries real costs and real trade-offs, and you deserve to see them laid out before anyone talks you into a policy.

- It costs more than term, often a lot more. For the same death benefit, a permanent policy can cost several times what term costs. You are paying for lifelong coverage and the cash value engine, not just protection.

- The early years are slow. As the worked example showed, your cash value can sit below what you have paid in for years. If there is any real chance you will cancel early, this is the wrong tool.

- Surrender charges bite. Cancel in the early years and the carrier may keep a chunk of the cash value through surrender charges that fade over time.

- Fees and the cost of insurance are ongoing. Internal charges come out along the way, and on flexible policies they can rise with age, which is why underfunded universal life policies sometimes struggle later.

- Loans need management. Borrowing against the policy is powerful, but an ignored loan can compound until it threatens the policy and creates a tax bill.

- Opportunity cost is real. Money parked in a slow-growing early policy is money not in a retirement account match or a low-cost index fund. For many people, filling tax-advantaged accounts first is the smarter first move, which is exactly the choice our IUL versus Roth IRA comparison weighs out.

None of this makes cash value life insurance bad. It makes it specific. The product is genuinely valuable for the right person with the right time horizon and the right funding, and genuinely a poor fit for someone who needs cheap protection or quick access to cash. The job of an honest agent is to tell you which one you are, even when the cheaper answer pays them less.

Who it fits and who it does not

Coverage decisions come down to your goals, your budget, and your time horizon, not to whatever product earns the biggest commission. With that framing, here is who tends to benefit and who usually should look elsewhere.

It often fits people who

- Already contribute enough to capture any retirement plan match and have used other tax-advantaged accounts.

- Want coverage that lasts their whole life, not just a term, often for estate, legacy, or a dependent who will always need support.

- Value tax-deferred growth and flexible access to money, and will leave the policy alone long enough to let it work.

- Are business owners or higher earners looking for another tax-advantaged bucket and a source of flexible capital.

- Want to self-finance large purchases over time and like the idea of borrowing against their own policy.

It usually does not fit people who

- Mainly need the largest possible death benefit for the lowest cost, where term life clearly wins.

- Have a tight budget and might struggle to fund the policy for the long haul, risking an early lapse.

- Have not yet built an emergency fund or captured an available retirement match.

- Want their money fully liquid in the next few years, since the early surrender math is unforgiving.

If you are not sure which list you belong on, that uncertainty is itself the answer to one question: do not buy yet. Get the comparison first. A clear-eyed look at term against permanent, with your real numbers, settles it faster than any brochure.

How to use cash value well

Say you own a policy, or you are about to. How do you actually use the cash value so it helps rather than hurts? A few principles separate the people who get real value from the people who end up disappointed.

Fund it the way it was designed

The fastest way to ruin a cash value policy is to underfund it. Pay what the design calls for, and where the strategy allows, fund toward the higher end of the allowable range to push more into growth early without crossing into MEC territory. A policy that is fed properly in the first decade behaves very differently from one fed the bare minimum.

Let it grow before you lean on it

Because the early years are slow, the cash value rewards patience. Resist the urge to borrow in year two. The longer you let compounding run before you start drawing on it, the more the policy can do for you when you actually need it, whether that is funding a business, smoothing income in retirement, or covering a large expense without selling investments at a bad time. Business owners often put the same cash value to work funding key person insurance or a buy-sell agreement.

Use loans with a plan

When you do borrow against the policy, treat it like the financing tool it is. Know your interest rate, have a rough plan to repay or at least to keep the loan from outrunning the cash value, and review the policy regularly. Some people use policy loans as a flexible reserve for opportunities and emergencies; others build a deliberate income stream in retirement. Either way, the difference between success and a lapse is attention.

Coordinate it with the rest of your plan

Cash value life insurance works best as one piece of a plan, not the whole thing. It pairs naturally with retirement accounts, an emergency fund, and other coverage rather than replacing them. The tax-deferred growth and flexible access can complement accounts that have contribution limits or early-withdrawal penalties, which is exactly why some families add a policy after the basics are handled, not before. If you want a sounder grounding in the products and how they fit a household, start from Sovereign Life Group, your life insurance strategist, and read up before any sales conversation.

If retirement income is your main interest, the indexed approach deserves a close look, because its floor-and-cap structure is designed for drawing income later. You can see how carriers structure that on our indexed universal life coverage page, and weigh it honestly against the trade-offs covered above.

Want to see if cash value fits your plan?

Fifteen minutes, no pressure. We will look at your goals, your budget, and whether a cash value policy, plain term, or something else does the job best for your family. You will leave with options laid out clearly, not a pitch.

Get a Quote Book a 15-Min Call Prefer to start now? Save my card or get a quick quote and we will follow up on your schedule.Frequently asked questions

What is cash value life insurance and how does it work?

Cash value life insurance is permanent coverage that pairs a death benefit with a savings-like account that grows over time. Part of each premium covers the cost of insurance and fees, and part goes into the cash value, which builds on a tax-deferred basis. Once enough has accumulated, you can borrow against it or withdraw from it while you are alive, and the death benefit still pays your family when you pass away.

Can I withdraw or borrow against the cash value in my life insurance?

Yes, once the policy has built enough value. A withdrawal pulls money out directly and can reduce the death benefit. A policy loan lets you borrow against the cash value while it keeps growing, and there is no credit check or fixed repayment schedule. Unpaid loan balances and interest are subtracted from the death benefit, so loans need to be managed so the policy does not lapse.

What happens to the cash value when I die?

With most traditional policies, your beneficiary receives the death benefit and the insurer keeps the remaining cash value, because the cash value was funding that benefit from the inside. Some policies and riders are designed to pay some or all of the cash value on top of the death benefit, which costs more. This is why how the policy is structured matters as much as the headline numbers.

How long does it take to build cash value?

Cash value usually grows slowly in the first few years because early premiums go toward the cost of insurance, fees, and commissions, and surrender charges can apply if you cancel early. Many policies start to show meaningful value somewhere around years three to ten, and the growth compounds from there. The exact pace depends on the policy type, the carrier, how the policy is funded, and the design.

Is cash value life insurance a good investment?

It is better understood as protection with a savings feature than as a pure investment. It can make sense for people who have already used other tax-advantaged accounts, want lifelong coverage, and value tax-deferred growth plus flexible access to money. For someone who mainly needs the largest death benefit for the lowest cost, term life is usually the better fit. The right answer depends on your goals, budget, and time horizon.

Does term life insurance have cash value?

No. Term life insurance is pure protection for a set number of years and builds no cash value. If you outlive the term, the coverage ends with no payout, which is part of why term costs less. Only permanent policies such as whole life, universal life, and indexed universal life build cash value.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Cash value growth, dividends, and interest crediting are not guaranteed and depend on the policy and the claims-paying ability of the issuing insurance company.