IUL Tax-Free Retirement Income: How It Actually Works

The Short Version

An indexed universal life policy is permanent life insurance with a cash value that earns interest tied to a market index, with a 0% floor in down years. Fund it right and you can pull IUL tax-free retirement income out later through withdrawals up to your basis and then policy loans. It costs more than a Roth, it has to be built and managed correctly, and the upside is capped, so it fits some people and not others.

Most folks I talk to want the same thing in retirement. They want income they can count on, and they do not want a surprise tax bill chewing into it. That is where the idea of IUL tax-free retirement income comes up, and it is the main reason people ask me about an indexed universal life policy, usually just called an IUL.

This is the long version of that conversation. I will walk you through how an IUL actually works, how the money comes out tax-free, what it costs, how it compares to a Roth and a 401k, who it fits, and where it goes wrong. You get the upside and the downside in equal measure, because this product is genuinely right for some people and flat wrong for others. None of it is a sales pitch and none of it is tax advice. It is the explanation I wish more people got before they signed anything.

What this guide covers

- What "tax-free retirement income" means

- What an IUL actually is

- How index crediting and the 0% floor work

- How the tax-free income comes out

- A worked example, honest assumptions

- IUL vs Roth vs 401k vs brokerage

- What an IUL actually costs

- Who it fits, and who should skip it

- How a good income policy is built

- The effect on Social Security and Medicare

- Mistakes and red flags to watch

- How it compares to other strategies

- How to decide if it fits you

- Frequently asked questions

What "tax-free retirement income" actually means

Before we touch the product, let us be clear about the goal, because the phrase "tax-free retirement income" gets thrown around loosely.

When you save in a traditional 401k or IRA, you get a tax break going in, but every dollar you pull out in retirement is taxed as ordinary income at whatever rates exist decades from now. You are a partner with the IRS, and you do not get to pick its share later. That is taxable retirement income. Tax-free income flips it: you pay tax on the money first, then it grows and comes out without further income tax. A Roth IRA works this way, and so does the cash value of a properly structured life insurance policy, including an IUL.

The appeal is not just the tax savings in a vacuum. It is control. If a chunk of your retirement income does not show up on your tax return, it does not push you into a higher bracket, it does not inflate the formula that decides how much of your Social Security gets taxed, and it does not raise your Medicare premiums through the income surcharge known as IRMAA. People often care about that ripple effect more than the headline tax rate. So when we talk about IUL tax-free retirement income, we mean a stream of money in retirement that, under current tax law and a correctly managed policy, does not land on your 1040 as taxable income. That is the promise. The rest of this guide is about whether the cost and the rules are worth it for you.

Tax-advantaged growth with a floor against losses. Quick and free.

What an IUL actually is

An IUL is permanent life insurance first. It pays a death benefit to your family when you pass, the same as any life policy. The difference is what happens inside it while you are alive. Two things go on at once: you are insured, and you are building a cash value account.

Where your premium goes

When you pay your premium, it does not all land in one place. Part covers the cost of insuring your life, called the cost of insurance. Part covers policy fees and a premium load. The rest goes into a cash value account that grows over time, with growth tied to a stock market index, usually the S&P 500.

Here is the piece that confuses people, so read it slowly. You are not invested in the market directly. You do not own the stocks and you do not collect the dividends. The insurer credits interest to your cash value based on how the index moves over a set period, inside limits we will get to next, while your money actually sits in the insurer's general account. That is the whole reason an IUL can offer a floor: because you are not in the market, the insurer can promise your credited interest will not go negative.

Max funded, not maximum death benefit

An IUL built for retirement income is usually "max funded." You put in close to the most the IRS rules allow for that death benefit, year after year, while keeping the death benefit as low as the rules permit. That sounds backwards if you think of life insurance as buying the biggest payout possible. For income it is the opposite: the point is to grow cash value, and a smaller death benefit means a smaller cost of insurance, which leaves more premium to compound. Underfund it and the costs can eat you alive, because the insurance charges keep coming whether or not you feed the cash value. It is why an IUL bought casually, with minimum premiums and a big death benefit, almost never delivers the income people were sold on. The design is the job.

How an IUL differs from its cousins

- Whole life credits a fixed, guaranteed rate plus possible dividends. Predictable and slow. No index, no caps, less upside, more certainty.

- Universal life is flexible-premium permanent insurance that credits a declared rate set by the insurer.

- Indexed universal life ties the interest to an index with a floor and a cap, trading some certainty for more potential growth.

- Variable universal life puts your cash value straight into market subaccounts, with real market risk and no floor. More upside, but you can lose money.

If you want the simpler decision underneath all of this, our breakdown of term versus whole life insurance lays out the basic fork in the road before you ever get to indexing.

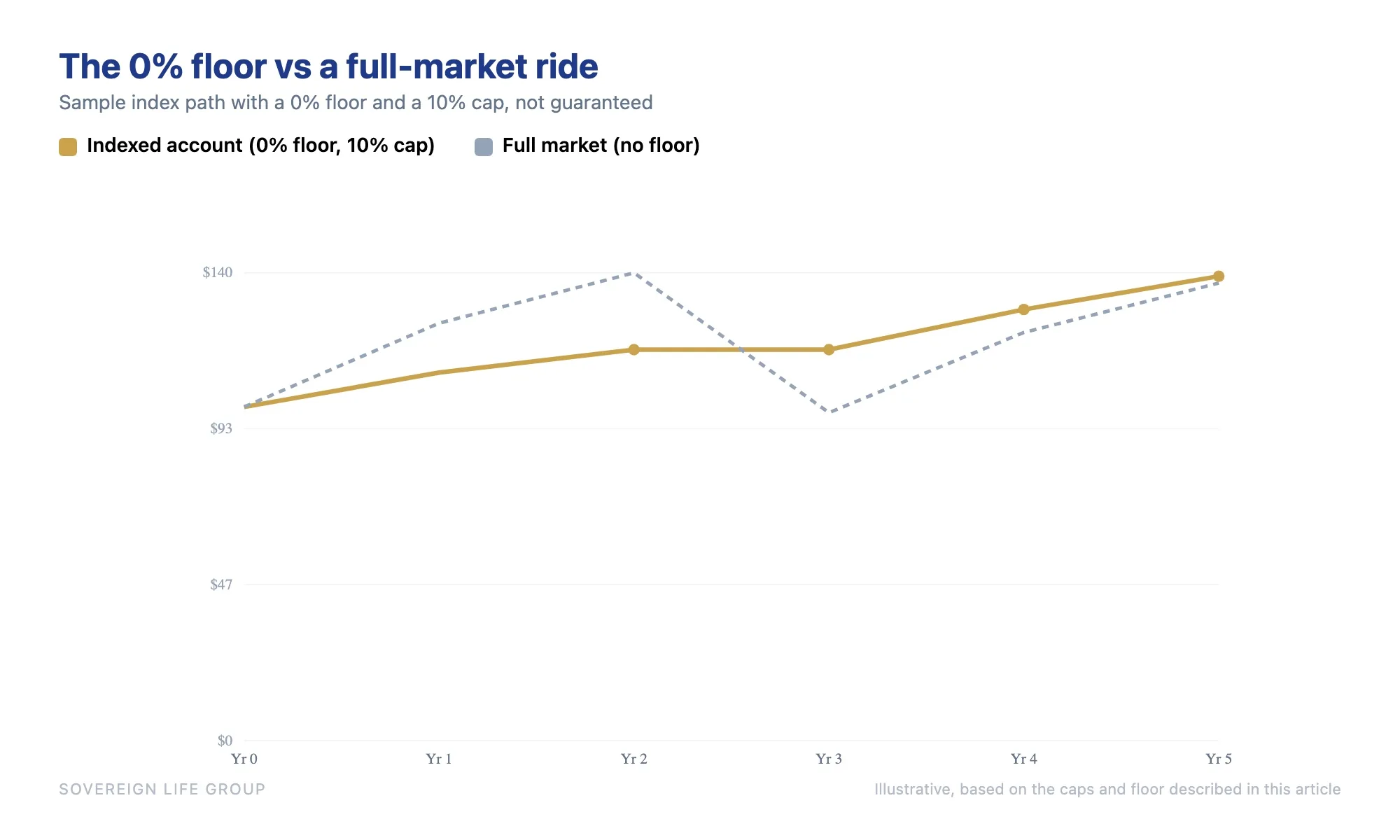

How index crediting and the 0% floor work

Your cash value earns interest based on the index, but the insurer puts brackets around it. Those brackets are the heart of the trade an IUL makes.

- The floor. In a year the market drops, your credited interest cannot go below 0%. If the S&P falls 30%, your indexed account gets credited 0%, not a loss. You still pay policy costs, so the cash value can dip slightly from charges, but your indexed gains are not wiped out. That floor is the whole selling point for a lot of people.

- The cap. In exchange for the floor, the insurer caps your upside. Caps move by carrier and over time, often landing in the high single digits to low teens in recent years. If the index returns 25% and your cap is 10%, you get 10%. You give up the biggest years to skip the worst ones.

- Participation rate. Some strategies skip the hard cap and credit a percentage of the index gain instead. A 60% participation rate on a 20% index year credits you 12%.

- The spread or margin. A percentage the insurer subtracts before crediting. If the index gains 12% and the spread is 4%, you are credited 8%. Spreads usually show up on uncapped, high-participation strategies.

Crediting does not happen continuously. Your money is allocated into "segments" that run for a set period, most often one year, and at the end the insurer applies your floor, cap, and participation rate to the index move and credits the result before the next segment starts fresh. This "annual reset" is quietly powerful, because each year stands on its own: if the index drops you get 0% rather than a loss, and the next year you earn from where you are, not from a hole you have to climb out of first. The flip side is real too. A one-year point-to-point method can credit 0% in a year that fell most of the way and only recovered at the very end, even though a buy-and-hold investor would have ended flat. The measurement window cuts both ways.

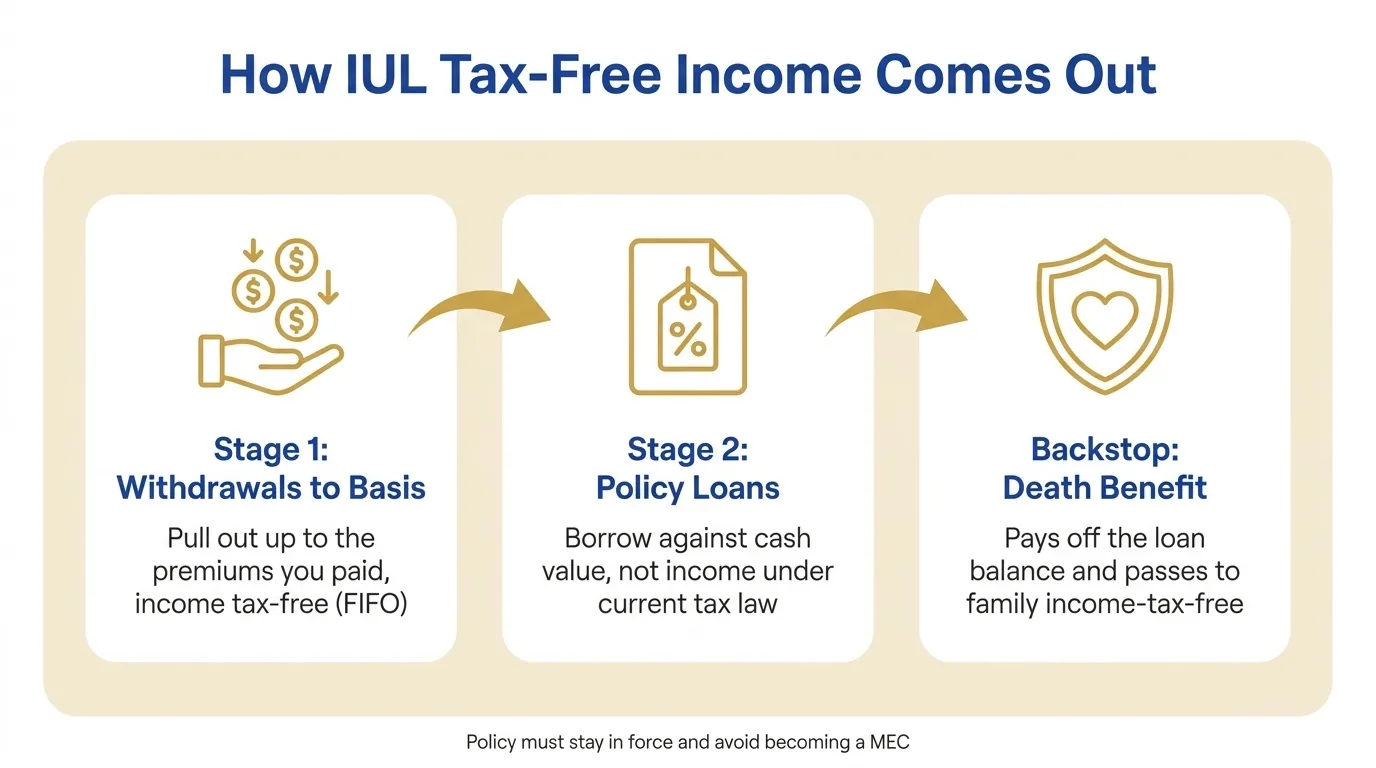

How IUL tax-free retirement income actually comes out

This is the question that brought you here. Money coming out of a properly structured life insurance policy can be income tax-free, and it happens in two stages plus a backstop. Underneath all of it sits tax-deferred growth: there is no annual 1099 on the interest credited inside the policy, the same reason a Roth or a 401k can outgrow a taxable account over decades.

Stage one: withdrawals up to your basis

Your "basis" is the total of premiums you have paid in. Life insurance generally uses first-in, first-out treatment, often called FIFO, so the money you withdraw first is treated as your own premiums coming back to you, not as gains. That portion comes out income tax-free, which lines up with guidance from the federal tax agency on how life insurance proceeds are treated. Once you have pulled out everything you put in, further withdrawals dip into gains, which can become taxable, so most income plans do not stop here.

Stage two: policy loans against the cash value

After your basis, you switch to loans. Instead of withdrawing, you borrow against your cash value. A loan is not income, so under current tax law it is not taxed. There is no application and no credit check, because you are borrowing against your own policy with the cash value as collateral, and depending on the loan type your full cash value can keep earning credited interest while the loan is outstanding. This is how people pull a stream of income out year after year without it showing up as taxable income. It is the mechanical heart of IUL tax-free retirement income.

Loan types matter more than people realize. A fixed or standard loan charges a set rate and often credits your collateral at a similar rate, so the net cost can be low or near zero. A participating or variable loan lets your borrowed amount keep earning the index-credited rate while you pay a loan rate, so in good years you can earn more than the loan costs and in flat years you pay interest while earning only the 0% floor. More upside, more risk. A cautious plan often leans on fixed loans late in life so a string of flat market years cannot quietly drain the policy.

The two rules that make it work

First, the policy has to stay in force until you die, because the tax-free nature of loans depends on the death benefit eventually paying off the loan balance. If you let it lapse or surrender it while a loan is outstanding, the loan is treated as a distribution and any gain above your basis becomes taxable income that year. Picture borrowing for years, then the policy collapses in your 80s, and suddenly you owe income tax on decades of gains you already spent. That is the worst case, avoidable with conservative borrowing and monitoring, but real.

Second, the policy has to avoid becoming a Modified Endowment Contract, or MEC, which happens when you pay premiums faster than the IRS allows under the 7-pay test. A MEC is still life insurance, but it loses the friendly tax treatment: loans and withdrawals are taxed gains-first, like an annuity, and can carry a 10% penalty before age 59 and a half. The irony people miss is that putting in too much money too fast is what creates a MEC, so an income-focused policy is deliberately funded right up to, but not over, the line. These limits come from real tax law, mainly Section 7702, which defines what counts as life insurance, and the TAMRA rules of 1988, which created the MEC test to stop people from using insurance as a pure tax shelter.

The backstop is the death benefit: whatever is left when you pass goes to your beneficiaries generally free of federal income tax, so the money is doing two jobs at once.

People sometimes call this the "triple tax advantage": tax-deferred growth, tax-free access through basis and loans, and a tax-free death benefit. It is a fair description as long as nobody pretends it is free. All three are bought, not given, paid for through the cost of insurance and policy fees and a capped upside. A Roth IRA offers tax-free growth and access without those insurance costs, so the advantage is real but it is a feature you are paying for, not a magic trick that beats every other account.

A worked example, with honest assumptions

Here is a composite example drawn from the kind of conversations I have every week. The names are invented and the figures are illustrative to show the shape of it. They are not a quote, not a projection of any specific policy, and not a promise of any result.

Dana is 40, healthy, a non-smoker, and a high earner who already gets her full 401k match and maxes a Roth. She has extra money she wants to grow tax-free and likes the idea of a floor and a death benefit riding along, so she funds an income-designed IUL for 20 years with the death benefit kept as low as the rules allow. Over those years her cash value grows through tax-deferred crediting, up to her cap in strong years and at the 0% floor in down years. By her 60s she has a substantial cash value built on money she already paid tax on. At retirement she takes income in two stages: first withdrawals up to her basis, income tax-free, then policy loans against the remaining cash value, which are not taxable income under current law. The result, in this scenario, is a stream of income for many years that never appears on her tax return.

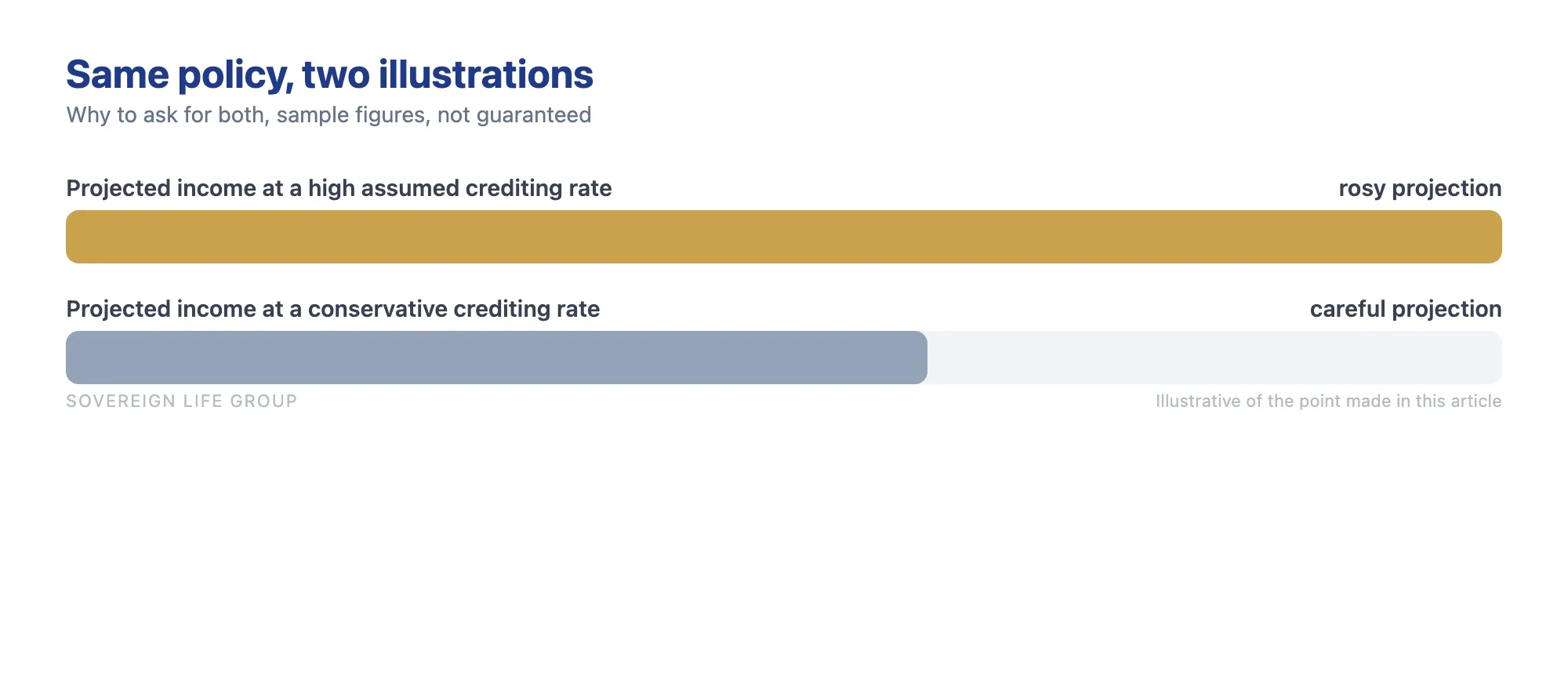

Now the honest part. Whether Dana gets that outcome depends on things nobody can promise: how the index performs over decades, whether the insurer keeps caps near current levels, whether she funds the policy without skipping years, and whether she borrows conservatively enough that the policy survives to pay its own loan at the end. Run the same illustration at a lower assumed crediting rate, the way a careful agent should, and the income figure comes down, sometimes a lot. That gap between the rosy illustration and the conservative one is where most disappointment lives, so always ask to see both. Change the facts and the answer flips: a 58-year-old with seven years to fund, a tight budget, and an unfilled Roth is usually better served filling the Roth, capturing the match, and using a brokerage account for the rest. The product does not change. The timeline and the budget decide it.

IUL vs Roth vs 401k vs brokerage: the fair comparison

I am not going to tell you an IUL beats everything. It does not. Each tool does a different job, and for most people the smart move is to use them in order. If your employer matches your 401k, capture that first, because it is free money you will not get anywhere else. A Roth IRA or Roth 401k is simple, low-cost, and tax-free in retirement, which is why for most people who can use one it should come before an IUL, a tradeoff we break down in our honest IUL vs Roth IRA comparison. A taxable brokerage account has no contribution limits and full liquidity, with taxes on dividends and gains as the cost. An IUL adds no IRS contribution cap, a 0% floor, tax-free access, and a death benefit, in exchange for insurance costs, capped upside, and the need for disciplined funding over decades. It earns its place as a later tier, not a first move.

| Feature | 401k (traditional) | Roth IRA | Taxable brokerage | IUL |

|---|---|---|---|---|

| Tax on the way in | Pre-tax | After-tax | After-tax | After-tax |

| Tax on growth | Deferred | None if qualified | Taxed yearly and at sale | Deferred |

| Tax on the way out | Ordinary income | Tax-free if qualified | Capital gains | Tax-free via basis and loans, if managed right |

| Contribution cap | Yes | Yes, with income phase-outs | No | No IRS cap, but a MEC limit per death benefit |

| Downside protection | None | None | None | 0% floor on index crediting |

| Upside | Full market | Full market | Full market | Capped or participation-limited |

| Costs | Fund fees | Low fund fees | Low fund fees | Insurance, policy, and rider charges |

| Death benefit | Account balance | Account balance | Account balance | Income-tax-free death benefit |

| Employer match | Often | No | No | No |

For most people the order is simple: get the 401k match, fund the Roth if you can, then, if you still have money to grow tax-free and room in your budget for the long haul, an IUL can be the next bucket. Our honest IUL vs 401k comparison puts those two side by side in more detail. It is almost always an "and," not an "instead of," and anyone who tells you to drop your 401k to fund an IUL deserves a hard second look.

What an IUL actually costs

A guide that skips the fees is a brochure, not a guide. Here is where your money goes besides the cash value.

- Cost of insurance. The charge for the actual life insurance, which rises as you age. The main reason a smaller death benefit helps an income policy.

- Premium load. A percentage skimmed off each premium, often covering the insurer's expenses and state premium taxes.

- Policy and per-thousand charges. Flat monthly administrative fees plus a charge based on each thousand dollars of death benefit, usually heaviest in the early years.

- Rider charges. Optional add-ons like a chronic illness or long-term-care living benefits rider cost extra. Useful for some, unnecessary for others.

- Surrender charges. Cancel in the early years, often the first 10 to 15, and the insurer takes a charge that can claw back a meaningful chunk of your cash value.

These costs are front-loaded, hitting hardest in the early years when your cash value is smallest, which is why bailing out after a few years is usually a bad outcome and why an IUL is a long-term commitment, not a place to park money you might need soon. Give the same money to a low-cost index fund and you skip these charges entirely, so the IUL has to deliver enough value from the floor, the tax treatment, and the death benefit to justify what it costs. For the right person it can. For the wrong person, the fees just quietly win.

See the strategy applied to your age and goals. No pressure.

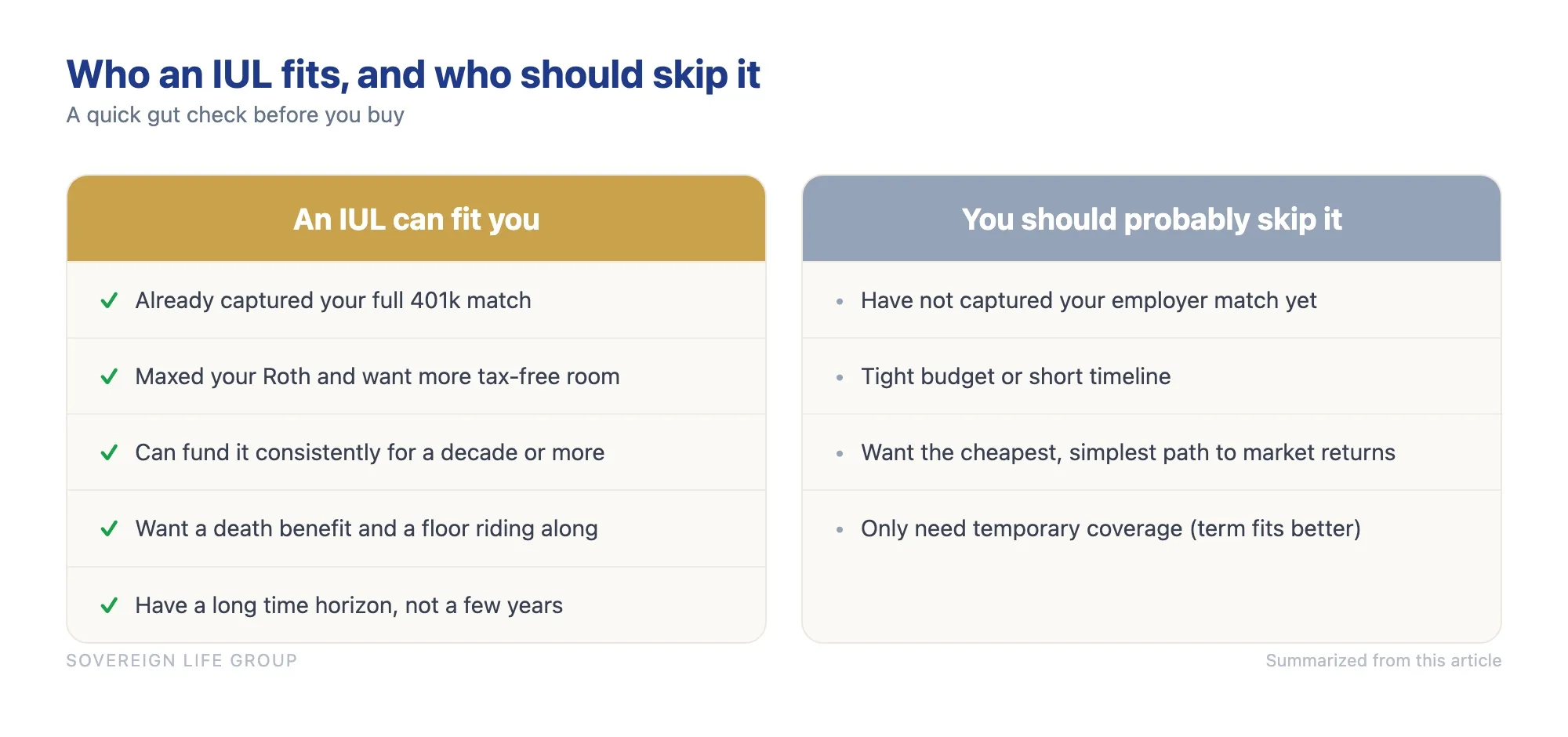

Who an IUL fits, and who should skip it

An IUL tends to fit people who have already captured their full employer match and maxed the easy tax-advantaged accounts and want more tax-free room, or who earn too much for a Roth IRA and want a tax-free bucket anyway. It fits those who can fund it consistently for a decade or more, who want a death benefit and a floor riding along with the growth, and who have a long time horizon rather than a few years before retirement.

It is usually the wrong tool if you have not captured your employer match yet, if your budget is tight or your timeline is short, or if you want the cheapest, simplest path to market returns, which is a Roth or a brokerage account in index funds. If you only need temporary coverage for a season, you want term life, not a cash-value policy. And if you are being sold the income story without the fees and risks, the problem is the pitch. If you are not sure which group you are in, that is the conversation to have before you buy. You can book a no-pressure review to walk through your own numbers, or see how we work with families planning for the long term.

How a good income policy is built and illustrated

Two policies with the same premium can produce very different income depending on how they are built. For income, you want the smallest death benefit the rules allow for your premium, funded close to the MEC line without crossing it, which minimizes the cost of insurance and maximizes cash value. Most policies also let you choose how the death benefit behaves, level or increasing, and a common income design uses the increasing option during the funding years, then switches to level to reduce costs as the income phase approaches.

The document that sells most policies is the illustration, and it is the one people understand least. Read it like a skeptic. Find the guaranteed column, which assumes worst-case charges and the minimum rate and shows the floor of the contract. Check the assumed crediting rate and ask to see it run a couple of points lower, because if the plan only works at a high rate it is fragile. Read the charges page, and watch the loan years to confirm the policy stays comfortably in force rather than limping near zero. According to the national association of state insurance regulators, illustration rules exist precisely because projected, non-guaranteed values can mislead buyers who treat them as promises. Treat the guaranteed column as the contract and the rest as a hopeful sketch.

The effect on Social Security and Medicare

This benefit gets underrated, and for many retirees it matters more than the headline tax savings. Several painful retirement formulas run on reported income, so income that stays off your tax return helps twice. How much of your Social Security benefit gets taxed depends on a measure called provisional income, which traditional 401k and IRA withdrawals raise but properly managed life insurance loans do not count toward the same way. Medicare Part B and Part D premiums rise at higher income through the IRMAA surcharge, and taxable withdrawals can push you over a threshold while tax-free income does not. None of this is a reason to buy an IUL on its own, since a Roth offers similar flexibility without insurance costs, but for a high earner who has already filled the Roth and the 401k, the planning value is real. The specifics belong with a qualified tax professional, not an article.

Common mistakes and red flags to watch

After enough of these conversations, the same handful of errors show up again and again, and most disappointment with IULs traces back to one of them, not to the product itself.

- Underfunding it. Pay the minimum and the front-loaded costs can hollow out the cash value, and the tax-free income never materializes.

- Buying too much death benefit. A bigger death benefit means a higher cost of insurance and less for cash value. For income you size the death benefit down and the funding up, within the rules.

- Treating the illustration as a promise. Those projections lean on non-guaranteed caps and rates held flat for decades. Ask to see them run at lower assumed rates.

- Over-borrowing late in life. Loan interest compounds, and participating loans can cost more than they earn in flat years. Pull too much and an aging policy can lapse, turning a tax-free plan into a taxable mess in a single year.

- Not monitoring the policy. An IUL is not "set it and forget it." It needs an annual review to confirm funding is on track, charges are behaving, and the income plan still holds.

Because commissions on permanent life insurance are larger than on term, some sellers have a real incentive to push a policy that fits their paycheck better than your plan. A few warning signs are worth taking seriously: they lead with the income number and skip the costs, they tell you to drop your 401k or skip the match, they show only the rosy illustration, they imply guaranteed returns when caps and credited rates are not guaranteed, they rush a multi-decade decision, or they will not clearly explain the MEC line and the loan mechanics. The fix is simple. Ask questions, ask for the unflattering numbers, and work with someone who treats the downsides as part of the job.

How an IUL compares to other tax-free strategies

An IUL is not the only way to chase tax-advantaged retirement income. Whole life is the more conservative cash-value cousin, with guaranteed growth and potential dividends instead of index crediting, and some people use it as the engine for the be your own bank, or infinite banking, idea. The trade-off is more certainty and usually slower growth. An annuity is built to turn a lump sum into guaranteed lifetime income, a different job, and nonqualified annuity income is taxed gains-first rather than tax-free, so if income certainty is your priority our overview of how annuities work across fixed, indexed, and variable types is worth reading next. And for pure tax-free income at the lowest cost, a Roth is hard to beat, which is why it usually comes first. The IUL's edge over a Roth is the lack of a contribution cap, the floor, and the death benefit, not a tax advantage the Roth lacks. If a Roth gives you everything you need, you may not need an IUL at all, and an honest advisor will say so.

Industry data shows why this conversation matters. According to research published by LIMRA, a large share of Americans worry about outliving their money in retirement, and tax treatment is one of the few levers a thoughtful plan can actually control. The point is not that an IUL is the answer. It is that the right mix of these tools, in the right order, usually is.

How to decide if an IUL fits you

If you have read this far, you are taking the decision seriously. Here is a practical path that does not require you to become an insurance expert.

- Cover the basics first. Build an emergency fund, capture your full employer match, and use your Roth if you can. An IUL belongs on top of these, not instead of them.

- Be honest about your time horizon and budget. Can you fund this consistently for a decade or more without strain? If the honest answer is no, an IUL is probably not your tool.

- Clarify the job. Tax-free income, a death benefit, downside protection, or all three? The job shapes the design, including the death benefit size and the funding level.

- Get an illustration and read it like a skeptic. Look at the guaranteed column, ask for a lower assumed rate, study the charges, and check the loan years.

- Compare it honestly to the alternatives. Put the IUL next to simply investing the same money in a Roth or a brokerage account. Either answer is useful.

- Work with someone who shows the downsides. The fees, the risks, and the conservative numbers should all be on the table. You can always start with a real human and not a robot at Sovereign Life Group, your life insurance strategist.

The goal is not to buy an IUL. It is a clear-eyed decision about whether one belongs in your plan. For some people it is a genuinely powerful piece of a tax-free retirement. For others, a Roth and a brokerage account do the same job for less. You deserve to see the full math before you choose.

Frequently asked questions

Is the income from an IUL really tax-free?

It can be, when the policy is set up and managed correctly. You can withdraw up to the premiums you paid in tax-free, and you can take policy loans against the cash value without triggering income tax under current rules. The policy has to stay in force and avoid becoming a Modified Endowment Contract. This is not tax advice, so talk to a qualified tax professional about your own situation.

How does an IUL create tax-free retirement income?

You fund the policy over years so the cash value grows tax-deferred, with a 0% floor that protects against index losses. In retirement you pull income out in two stages: first withdrawals up to your basis, which is the premiums you paid, then policy loans against the cash value. Loans are not income under current tax law, so the stream can come out income tax-free as long as the policy stays in force and is not a MEC.

Is an IUL better than a Roth IRA or a 401k?

Not better, just different. A Roth is simpler and cheaper and has no insurance costs. A 401k often comes with a match you should not pass up. An IUL adds a 0% floor, a death benefit, and no IRS contribution cap. Most people who use an IUL fund it after they have captured the match and used their Roth, not instead of those.

What are the downsides and fees of an IUL?

It carries cost of insurance, policy and rider charges, and premium-load fees that a low-cost index fund does not. Surrender charges apply in the early years. Caps and participation rates limit your upside, and the insurer can change them within contract limits. It has to be funded and structured properly, and the illustration is a projection, not a promise. If you stop funding it or borrow too much, the policy can lapse, which can trigger a tax bill.

How much do I need to fund an IUL for retirement income?

There is no single number, but an IUL built for income usually means funding it consistently for many years, near the maximum the IRS rules allow for that death benefit. Underfund it and the costs can eat the cash value. If your budget is tight or your timeline is short, an IUL is probably not the right tool, and a Roth or taxable account may fit better.

What is a MEC and why does it matter for tax-free income?

A Modified Endowment Contract, or MEC, is what a life insurance policy becomes if you pay premiums faster than the IRS 7-pay limit allows. A MEC loses the favorable tax treatment on loans and withdrawals, so distributions are taxed gains-first and may carry a penalty before age 59 and a half. A policy built for tax-free income is designed to stay just under the MEC line on purpose.

Want to see if an IUL fits you?

Fifteen minutes. We will look at your income goals, your budget, and whether an IUL even makes sense for you. If a Roth or a simple brokerage account does the job better, I will tell you that plainly.

Get a Quote Book a 15-Min Retirement-Income Review Prefer to read more first? Start with our IUL vs 401k breakdown.Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a qualified tax professional and a licensed professional about your specific situation before acting. Indexed universal life is permanent life insurance with costs of insurance, fees, and surrender charges. IUL cash values and index-credited returns are not guaranteed and assume non-guaranteed elements such as caps, participation rates, spreads, and credited interest that the insurer can change within contract limits. Policy loans and withdrawals reduce the death benefit and cash value and may have tax consequences, including taxable income if the policy lapses or is surrendered with a loan outstanding. Any illustration is a projection, not a promise of future results. Product availability, features, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company. Reach out with questions about your situation.