Annuities Explained: Fixed vs Indexed vs Variable Annuity

The Short Version

A fixed annuity pays a guaranteed rate. An indexed annuity links growth to a market index with a floor that protects your principal and a cap that limits the upside. A variable annuity invests directly in the market, so it can grow more but can also lose value. The right one depends on how much risk you can stomach and when you need the money.

Annuities get sold a lot, and explained well almost never. People walk out of meetings having signed something they could not repeat back to you a week later. That is a problem, because the difference between a fixed vs indexed vs variable annuity is the difference between guaranteed, protected, and exposed. Three very different deals wearing one word.

So here are annuities explained the plain way. What each type is, how the returns are actually credited, what it really costs, where the catch lives, how the taxes work, and who each one fits. No hype, no fear-selling, and an honest look at the cases where the answer is "none of these."

What this guide covers

- What an annuity actually is

- Fixed annuities: the simple one

- Indexed annuities: the in-between one

- Variable annuities: the exposed one

- Fixed vs indexed vs variable, side by side

- How indexed returns are really credited

- The fees, line by line

- Surrender periods and liquidity

- Income riders and other add-ons

- How annuities are taxed

- How to choose the right type

- Common mistakes people make

- How to vet the carrier

- Frequently asked questions

First, what an annuity even is

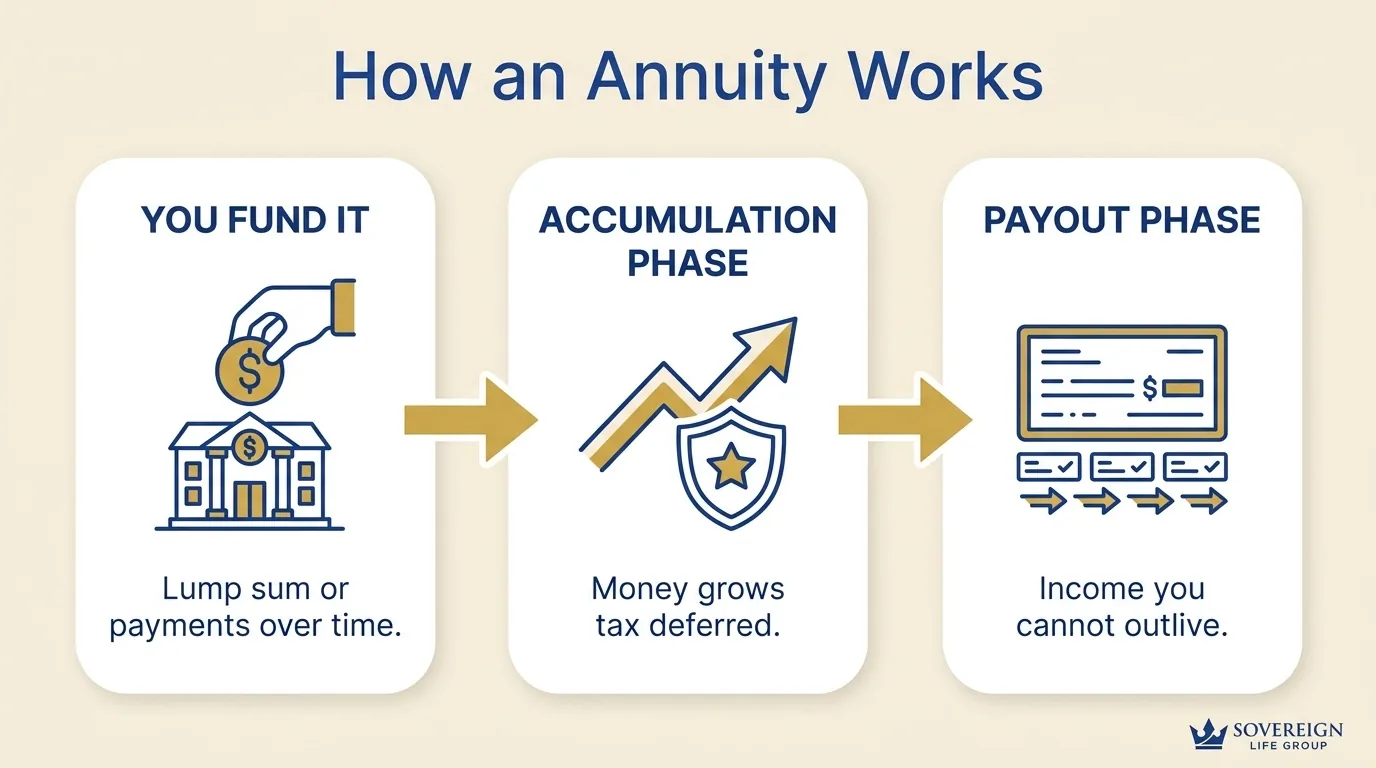

An annuity is a contract with an insurance company. You hand them money, either a lump sum or payments over time, and in return they grow it and pay it back to you, often as income you cannot outlive. According to the SEC at Investor.gov, that promise of future payments is what legally defines an annuity. That last part is the whole point for a lot of retirees. It is a way to turn a pile of savings into a paycheck.

Before we get to the three types, there are two structural choices baked into every annuity. Understanding them keeps the rest of this from getting confusing.

Immediate vs deferred

This is about timing, when the income turns on.

- Immediate annuity. You give a lump sum and income starts almost right away, usually within a year. Good for someone already retired who wants a paycheck now.

- Deferred annuity. Your money grows tax deferred for years first, then you turn on income later. Most fixed, indexed, and variable annuities you will see are deferred.

Accumulation vs payout phase

A deferred annuity has two stages. In the accumulation phase, your money grows inside the contract. In the payout phase (also called annuitization, or triggered by an income rider), the contract converts to income. You do not have to annuitize most modern contracts to get income, which is a change from the old days, but the two-phase structure is still the mental model to hold.

The three types we are about to cover, fixed, indexed, and variable, describe how your money grows during that accumulation phase. That is the real fork in the road, so let us walk each one.

Protected, tax-deferred growth for retirement. Quick and free.

Fixed annuities: the simple one

A fixed annuity pays a set interest rate that the insurance company guarantees for a stated period. Think of it like a certificate of deposit from a bank, but issued by an insurer and usually tax deferred. The market can crash and your rate does not move. You know exactly what you will have.

The most common flavor people buy today is a multi-year guaranteed annuity, or MYGA. It locks a single rate for a set term, say three, five, or seven years, much like a CD locks a rate. When the term ends you can renew, move to a new contract, or take the money. A traditional fixed annuity, by contrast, may guarantee a rate for one year and then reset to a renewal rate the carrier sets, with a minimum floor written into the contract.

The trade is obvious. Safety costs upside. If the market rips 20% in a year, you still get your fixed rate and nothing more. For people who just want their money to sit still and grow steadily without drama, that is a fair deal, and in higher rate environments a fixed annuity can be genuinely competitive with other safe-money options.

Fixed annuities also carry the lowest fees of the three. Often there is no explicit annual fee at all, because the carrier simply keeps the spread between what they earn on their investments and what they credit to you. What looks like "no fee" is really a built-in margin, which is fine as long as the rate you are quoted is competitive.

Indexed annuities: the in-between one

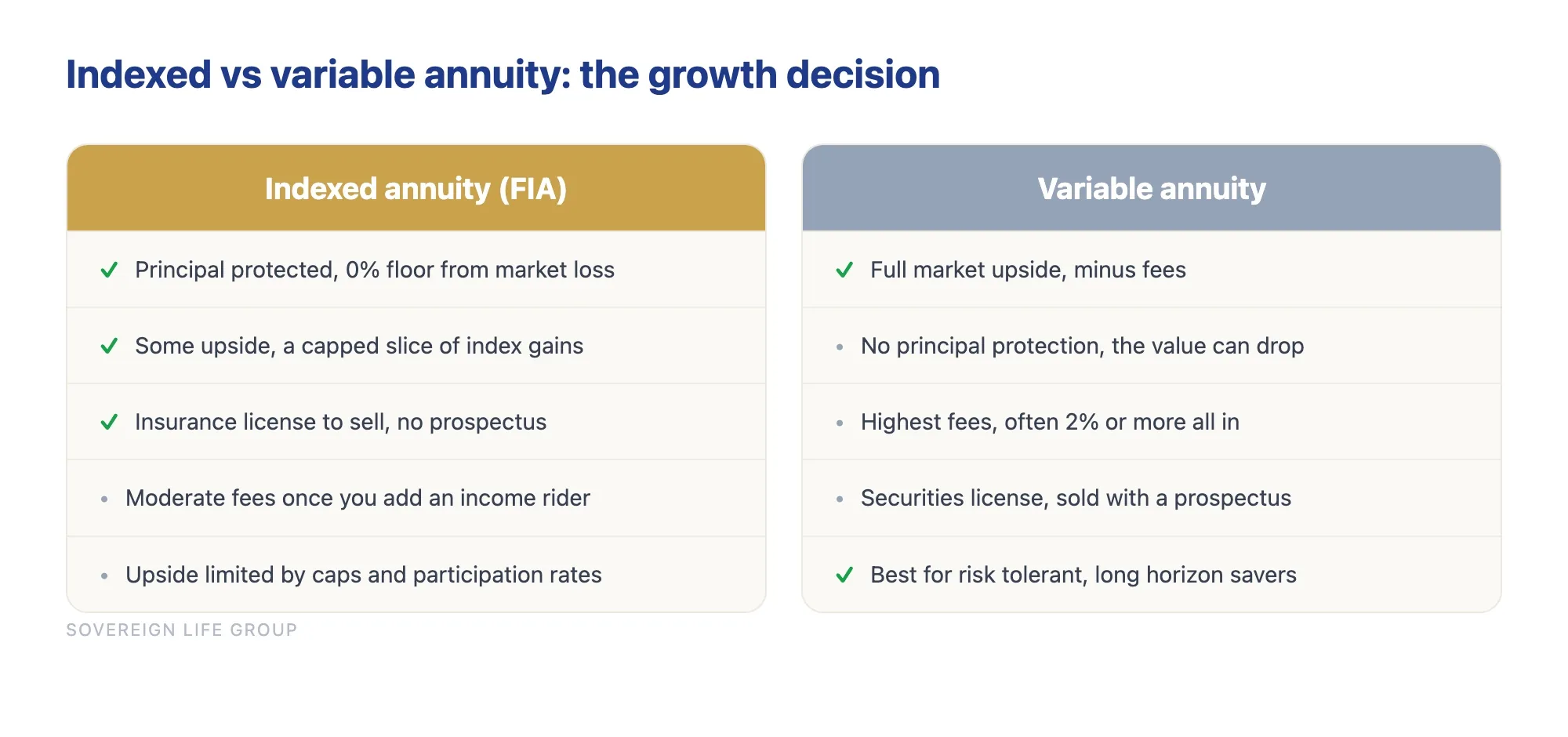

A fixed indexed annuity (you will see it called an FIA) ties your interest to a market index like the S&P 500. When the index goes up, you get credited based on a formula. When the index goes down, you get credited zero for that period and you do not lose principal to the market. That floor, usually 0%, is the selling point.

But the upside is not free, and this is where people get fooled. The carrier limits how much of the index gain you keep through a few levers:

- Cap. A ceiling on what you can earn in a period. If your cap is 9% and the index returns 18%, you get 9%.

- Participation rate. The share of the gain you keep. At an 80% participation rate, a 10% index gain credits you 8%.

- Spread (or margin). A percentage the carrier subtracts off the top before crediting you. With a 3% spread, a 10% index gain credits you 7%.

A given contract might use one of these levers or stack two of them together. Here is the part nobody mentions at the kitchen table: the carrier can usually reset those caps, rates, and spreads each renewal period based on interest rates, bond yields, and the cost of the options they buy to hedge. So the generous cap you bought in year one can shrink in year three. Indexed annuities are not the same as owning the index, and they are not the same as the market's full return. They are a protected, capped slice of it.

One more honest note: index crediting almost always excludes dividends. The S&P 500's price index leaves out the dividend yield that long-term stock investors actually earn, so even before caps, you are tracking a slimmer version of "the market" than the headline number suggests.

Variable annuities: the market-exposed one

A variable annuity puts your money into investment subaccounts that work like mutual funds. Your value rises and falls with those investments. More upside potential than fixed or indexed, and real downside risk too. You can lose principal here, and in a bad market you can lose a meaningful amount of it.

Variable annuities also tend to carry the highest fees of the three. You are often looking at mortality and expense charges, administrative fees, the underlying subaccount management fees, and the cost of any optional riders. Stacked together, those can run a couple of percent a year or more, which is a real drag on returns over time. Some buyers add a guaranteed living benefit rider to put a floor under their income despite the market exposure, and that rider has its own cost.

Because they involve securities, variable annuities are sold with a prospectus and require a securities license, not just an insurance license. That alone tells you they are a different animal. If your representative cannot hand you a prospectus, you are not looking at a true variable annuity. As a life insurance agency, Sovereign Life Group focuses on the fixed and indexed side of the aisle and on protection-first life insurance strategy for families, so treat the variable section here as education, not a pitch.

Fixed vs indexed vs variable annuity, side by side

Here is the comparison most people actually want, in one place.

| Fixed | Indexed (FIA) | Variable | |

|---|---|---|---|

| How returns work | Set guaranteed rate | Index-linked with a cap, participation rate, or spread | Market subaccounts |

| Risk level | Lowest | Low to moderate | Highest |

| Principal protection | Yes, from market loss | Yes, 0% floor from market loss | No, value can drop |

| Upside potential | Limited to the fixed rate | Capped slice of index gains | Full market upside, minus fees |

| Typical fees | Lowest, often none stated | Moderate, rider fees common | Highest, often 2%+ all in |

| Liquidity / surrender | 3 to 10 yr period, often about 10% free yearly | Often 7 to 10 yr, sometimes longer | Varies, surrender charges apply |

| License to sell | Insurance license | Insurance license | Securities license, sold with a prospectus |

| Best suited for | Safety-first savers near retirement | Protected growth with some upside | Risk-tolerant, long horizon |

One thing applies to all three: the surrender period, which we cover in depth below. If you might need the lump sum soon, an annuity of any kind is the wrong tool.

How indexed returns are really credited

The fixed and variable types are easy to picture. Indexed annuities are where most of the confusion lives, because "your interest is linked to the S&P 500" can mean several very different things depending on the crediting method written into your contract. Here are the common ones in plain English.

Annual point-to-point

The carrier looks at the index value on your contract anniversary and compares it to one year earlier. If it is up, you get credited that gain subject to your cap, participation rate, or spread. If it is down, you get zero. This is the most common and the easiest to understand.

Monthly sum (monthly point-to-point)

The carrier tracks the index change each month, usually capping each positive month but letting negative months count in full, then adds the twelve numbers at year end. This method can look attractive in a calm, steadily rising year and can disappoint badly in a choppy year, because one sharp down month drags the whole sum lower. Read this one carefully.

Multi-year point-to-point

The comparison spans two or more years instead of one. Longer terms sometimes come with higher caps or full participation, but your money is committed to that window before you see a credit.

The takeaway is not to memorize formulas. It is to understand that two indexed annuities both "linked to the S&P 500" can credit wildly different amounts in the same year because their crediting methods and caps differ. Always ask the representative to show you, in writing, how the contract would have credited over several past years, including a down year. A protected slice of the market is a reasonable thing to want. Just know which slice you are buying.

The fees, line by line

Fees are where annuities earn their mixed reputation, so let us pull them apart by type instead of lumping them together.

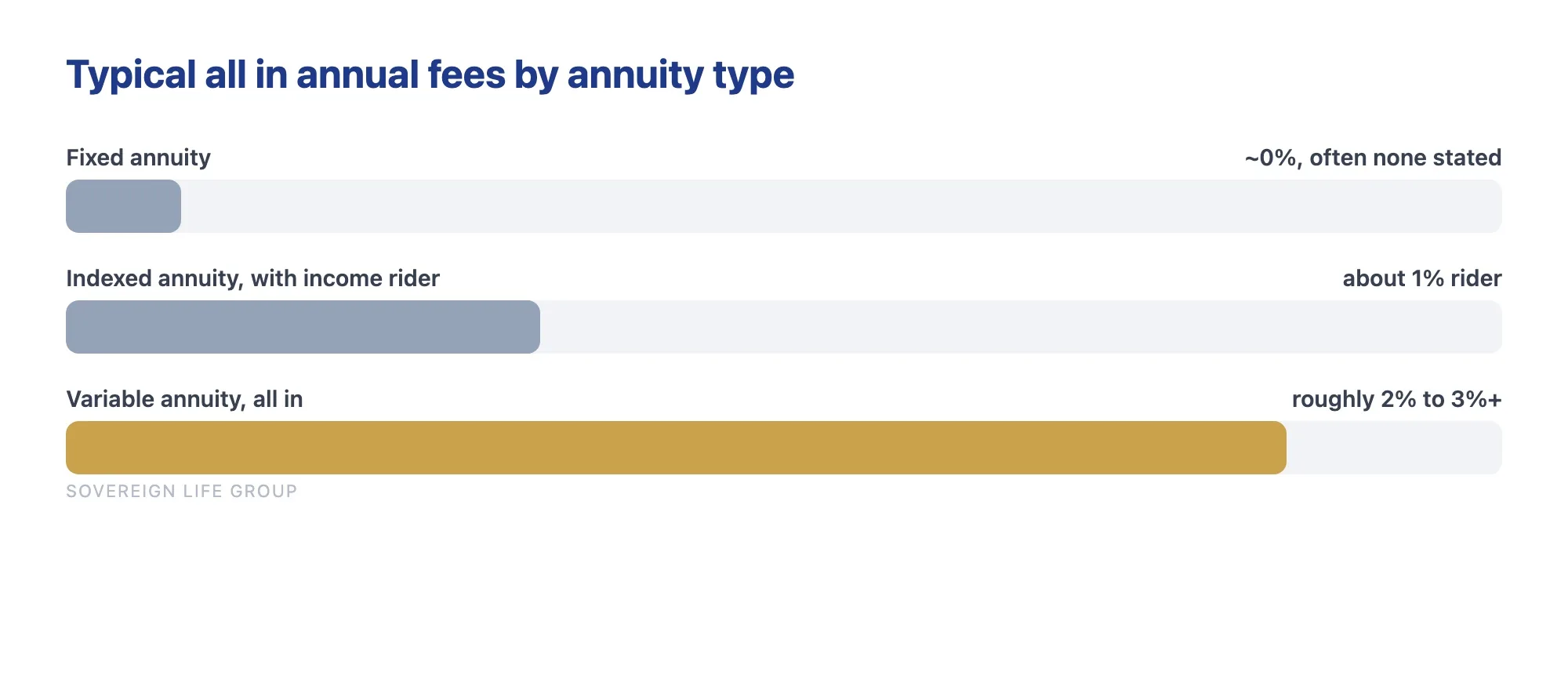

- Fixed annuities. Usually no stated annual fee. The carrier keeps the spread. Your main "cost" is the upside you give up for safety.

- Indexed annuities. The base contract often has no explicit annual fee either, because the cap and participation rate are how the carrier makes its margin. The fees show up if you add optional riders, most commonly an income rider, which typically costs an annual percentage of your value.

- Variable annuities. This is where fees stack. Mortality and expense (M&E) charges, administrative fees, the expense ratios of the underlying subaccounts, and any rider fees can add up to roughly 2% to 3% or more per year all in. Over a long retirement, that compounding drag is significant.

None of this makes annuities bad. It makes them products you have to price honestly. A 2% annual drag is fine if the contract is doing a job nothing cheaper can do, such as guaranteeing income you cannot outlive. It is a poor deal if you are paying variable-annuity fees for growth you could have gotten more cheaply in a simple investment account. The product should earn its cost. If you are weighing protected growth against other strategies, our breakdown of a cash-value life insurance and infinite banking approach walks through a different way families build tax-advantaged money, with its own trade-offs.

Compare your options with no pressure. Takes about 2 minutes.

Surrender periods and liquidity

Every annuity ties up your money for a stretch, and this is the single most common source of regret when an annuity is sold to the wrong person. The surrender period is the window, often three to ten years and sometimes longer, during which pulling out more than the allowed amount triggers a surrender charge.

How it usually works:

- Most contracts let you withdraw up to about 10% of the value each year without penalty (the "free withdrawal").

- Take out more than that during the surrender window and you pay a surrender charge on the excess.

- The charge starts higher and steps down each year, often something like 9%, 8%, 7% and so on, until it reaches zero when the period ends.

- Some contracts add a market value adjustment, which can move the charge up or down based on interest rates when you withdraw.

A longer surrender period is not automatically bad. Carriers often pay a higher rate or a higher cap in exchange for your willingness to commit longer. But it is a real constraint. If there is any chance you will need this money for an emergency, a home repair, a medical bill, or simply peace of mind, do not put it all into a long-surrender contract. Keep a separate, liquid emergency fund outside the annuity. The classic painful mistake is locking up money you turn out to need in year two.

Income riders and other add-ons

Modern annuities are often sold with optional riders, and the most important one to understand is the income rider, sometimes called a guaranteed lifetime withdrawal benefit (GLWB). This is frequently the real reason someone buys an indexed annuity, so it deserves a clear explanation.

An income rider promises a stream of income you cannot outlive, even if your actual account value gets drawn down to zero over a long retirement. It usually works off a separate "benefit base," a number used only to calculate your guaranteed income, which is not the same as the cash you could walk away with. The rider grows that benefit base by a stated amount, and when you turn income on, you receive a set percentage of it for life.

Two honest cautions. First, the benefit base is not your money. You generally cannot cash it out. It is an accounting figure for income, so do not confuse a "7% roll-up" on the benefit base with a 7% return on your savings. Second, the rider costs an annual fee, often around 1% of value, every year. For someone who genuinely wants guaranteed lifetime income and will use it, that can be money well spent. For someone who just wants growth and may never turn on income, it can be a fee paid for a feature never used.

Other riders you may see include enhanced death benefits, which pass more to heirs for a cost, and long-term-care or confinement riders, which boost income if you cannot perform certain daily activities. Each adds value for the right person and cost for the wrong one. The rule is the same throughout this guide: match the feature to the job, and do not pay for guarantees you will not use.

How annuities are taxed

Taxes are part of the annuity story people skip, then get surprised by. Here is the plain version, with the standard disclaimer that this is general education, not tax advice, and you should confirm your specifics with a tax professional.

- Tax-deferred growth. Inside a deferred annuity, your money grows without an annual tax bill. You owe nothing until you take money out. That deferral is one of the genuine advantages of the structure.

- Gains taxed as ordinary income. When you withdraw earnings, they are taxed as ordinary income, not at the lower long-term capital gains rates that a stock or fund might enjoy. For some people in retirement that is fine; for others it matters a lot.

- Last-in, first-out for nonqualified annuities. If you funded the annuity with after-tax money, withdrawals are generally treated as gains first (taxable) and your original principal last (not taxable).

- The age 59 and a half rule. Withdraw gains before that age and you may owe an additional 10% federal penalty on top of ordinary income tax, similar to a retirement account.

- Qualified vs nonqualified. If the annuity sits inside an IRA or other pretax account, the account's own rules drive the tax treatment, and the annuity's deferral is redundant with the account's. That is a common critique of putting an annuity inside an IRA, and a fair question to ask any representative.

The buyer's guide published by the NAIC is a neutral, regulator-written resource worth reading before you sign anything, and it covers the tax basics in similar plain language.

How to choose the right type

Skip the product names for a second and answer these honestly. Your answers point to the type far better than any sales script.

- When do you need the money? If it is within a few years, the surrender period alone may rule annuities out entirely.

- Can you handle a down year? If a 20% drop would wreck your sleep or your plan, the variable lane is probably not yours.

- What is the job? Steady safe growth points to fixed. Protected growth with some market upside points to indexed. Maximum growth with real risk and a long runway points to variable. Guaranteed lifetime income points to an income rider on a fixed or indexed contract.

- How does it fit the rest of your plan? An annuity is one tool. For some families a properly structured cash-value strategy, or simply more term life insurance plus index investing, does the job better. The product should serve the plan, not the other way around.

A quick way to translate goals into types:

| If your main goal is | The type that usually fits | The honest trade-off |

|---|---|---|

| Safe, predictable growth like a CD | Fixed / MYGA | You give up market upside |

| Some market upside with no market losses | Indexed (FIA) | Caps and renewals limit your return |

| Guaranteed income you cannot outlive | Fixed or indexed with an income rider | Rider fees and a benefit base that is not your cash |

| Maximum growth, can accept losses | Variable | Highest fees and real downside risk |

| Liquidity and short time horizon | Probably not an annuity | Surrender charges punish early access |

Common mistakes people make

- Buying for the bonus. Some annuities dangle a premium bonus up front. That money usually comes with longer surrender periods and lower caps. Bonuses are rarely free.

- Believing "market gains, no risk." Indexed annuities protect principal, but the cap, participation rate, spread, and renewal resets all limit your return, and dividends are excluded. It is protection, not a free lunch.

- Locking up money you will need. Putting your emergency fund or near-term cash into a long surrender contract is a classic, painful error.

- Confusing the benefit base with cash value. A roll-up on the income rider's benefit base is not a return on your savings. Know which number is real.

- Ignoring the fees on variable. Two to three percent a year compounds against you. Over a long retirement that is a lot of money quietly leaving.

- Putting an annuity inside an IRA without a reason. The tax deferral is redundant there, so make sure the annuity is doing something else worthwhile, like guaranteed income.

- Not checking the carrier. Every guarantee here rests on the insurance company's ability to pay. The strength of the issuer matters as much as the product.

How to vet the carrier

This point gets its own section because it is the one people skip and the one that matters most for the guarantees. An annuity is only as solid as the company standing behind it. Unlike a bank account, an annuity is not FDIC insured. Fixed and indexed guarantees rest on the carrier's claims-paying ability, with a state guaranty association providing a backstop up to certain limits that vary by state.

Before you commit, ask:

- What are the carrier's financial strength ratings? Independent agencies such as A.M. Best, Standard & Poor's, and Moody's rate insurers. Higher, more stable ratings suggest a stronger ability to pay long-dated promises.

- How long has the company issued annuities? A long, steady track record in this specific product line is reassuring.

- What does my state guaranty association cover? Coverage limits differ by state and are not a marketing tool, so do not let anyone sell on the backstop. Treat it as a floor, not a feature.

A good agent will walk you through this without being asked, and will be candid when a flashier product from a weaker carrier is not worth the trade. If the answers get vague, that is your signal.

Frequently asked questions

What is the difference between a fixed, indexed, and variable annuity?

A fixed annuity pays a set interest rate the carrier guarantees. An indexed annuity ties your interest to a market index with a floor that protects principal, in exchange for a cap on the upside. A variable annuity puts your money directly in market subaccounts, so you can gain or lose value based on how those investments perform.

What is the difference between a fixed and a variable annuity?

A fixed annuity pays a set interest rate the carrier guarantees, so your principal does not drop when the market falls. A variable annuity invests your money directly in market subaccounts, so it can grow more but can also lose value. Fixed trades upside for safety. Variable takes on market risk for a shot at higher returns.

How does an indexed annuity differ from a fixed annuity?

A fixed annuity pays a flat guaranteed rate set by the carrier. An indexed annuity ties your interest to a market index like the S&P 500, with a floor that protects your principal and a cap that limits the upside. Both protect against loss, but an indexed annuity gives you a chance at more growth in strong market years in exchange for a variable, capped return.

What is the difference between an indexed annuity and a variable annuity?

An indexed annuity protects your principal with a floor and ties gains to a market index up to a cap, so a market drop cannot take your money. A variable annuity invests directly in the market with no floor, so it can gain more but can also lose value. Indexed limits both the risk and the upside. Variable leaves both wide open.

Are annuities safe?

Fixed and indexed annuities protect your principal from market losses, backed by the claims-paying ability of the issuing carrier. Variable annuities can lose value because your money is invested directly in the market. No annuity is FDIC insured, so the financial strength of the company matters, with a state guaranty association providing a backstop up to limits that vary by state.

What is a surrender period on an annuity?

It is the window, often three to ten years, when pulling out more than the allowed amount triggers a charge. Most contracts let you withdraw up to about 10% a year penalty free. The surrender charge usually starts higher and shrinks each year until it disappears.

How are annuities taxed?

Money inside a deferred annuity grows tax deferred, so you owe no tax until you take it out. Withdrawals of gains are taxed as ordinary income, not at capital gains rates, and gains pulled before age 59 and a half may face an extra 10% federal penalty. How the contract was funded also changes the picture, so talk with a tax professional about your situation.

What is an income rider on an annuity?

An income rider, often called a guaranteed lifetime withdrawal benefit, is an optional add-on that promises income you cannot outlive, even if the account value runs down. It usually charges an annual fee and uses a separate benefit base to calculate income. It can be valuable if you will actually use the income, but read how the fee and the benefit base work first.

Who should buy an annuity?

They tend to fit people near or in retirement who want protected growth or guaranteed income they cannot outlive, and who can leave the money alone through the surrender period. They are a poor fit if you may need the cash soon or you are still decades out with cheaper options on the table.

Want a straight read on whether an annuity fits you?

Fifteen minutes. We will look at your retirement timeline, your risk comfort, and whether fixed, indexed, variable, or none of them makes sense for your money. No pressure, no jargon.

Get a Quote Book a 15-Min Retirement Income Review Prefer to start with the bigger plan? See how we help families protect income and build wealth.Annuities can be a genuinely useful tool, or an expensive mistake, depending on the product and the person. The only way to know which is to match the contract to your actual plan, read the crediting and surrender language, and vet the carrier behind the guarantee. If you want help doing that, book a review or read more in our retirement and insurance library.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, caps, and rates vary by state, age, and carrier, and any contract is subject to underwriting and suitability review. Annuity values and indexed returns are not guaranteed, and surrender charges may apply. All guarantees are subject to the claims-paying ability of the issuing insurance company. Annuities are not FDIC insured.