Mortgage Protection Guide: How It Works and What It Costs

The Short Version

Mortgage protection pays off or pays down your home loan if you pass away, so your family keeps the house instead of forcing a sale. It is not PMI, and it is never required to get a loan. For many healthy buyers, a level term life policy does the same job with more flexibility for a similar price, which is why it is worth comparing both before you sign anything.

Here is the question almost nobody wants to sit with: if you did not come home tomorrow, could the people you love keep paying the mortgage? For most families the honest answer is "not for long." The income stops, but the bank's bill does not. This mortgage protection guide exists for exactly that gap, and it is written to give you straight answers without the pressure. We will walk through what mortgage protection actually is, how the claim really works, what it costs and why, how it stacks up against PMI and ordinary term life, the riders worth understanding, the junk mail to ignore, and the honest cases where you do not need it at all.

I write this as a licensed agent, not a marketer chasing a sale. Some of what follows will talk you out of buying the most expensive option in the room. That is the point. Good coverage is the goal, not a big commission.

What this guide covers

- What mortgage protection actually is

- How mortgage protection insurance works

- What it costs and what drives the price

- Mortgage protection vs PMI

- Mortgage protection vs term life insurance

- The riders people actually ask about

- Those official-looking letters in the mail

- When you probably need it

- When you probably do not

- How much coverage and how long a term

- How to shop for it without overpaying

- Is mortgage protection worth it?

- Frequently asked questions

What mortgage protection actually is

Mortgage protection is a life insurance policy designed around your home loan. If you pass away while it is in force, it pays a benefit that your family can use to wipe out or pay down the mortgage. The goal is simple and human: keep your family in their home instead of forcing a sale during the worst month of their lives. You will also hear it called mortgage protection insurance, mortgage life insurance, or MPI. For the purposes of this mortgage protection guide, treat those names as the same idea.

There are two main flavors, and the difference matters more than most people realize.

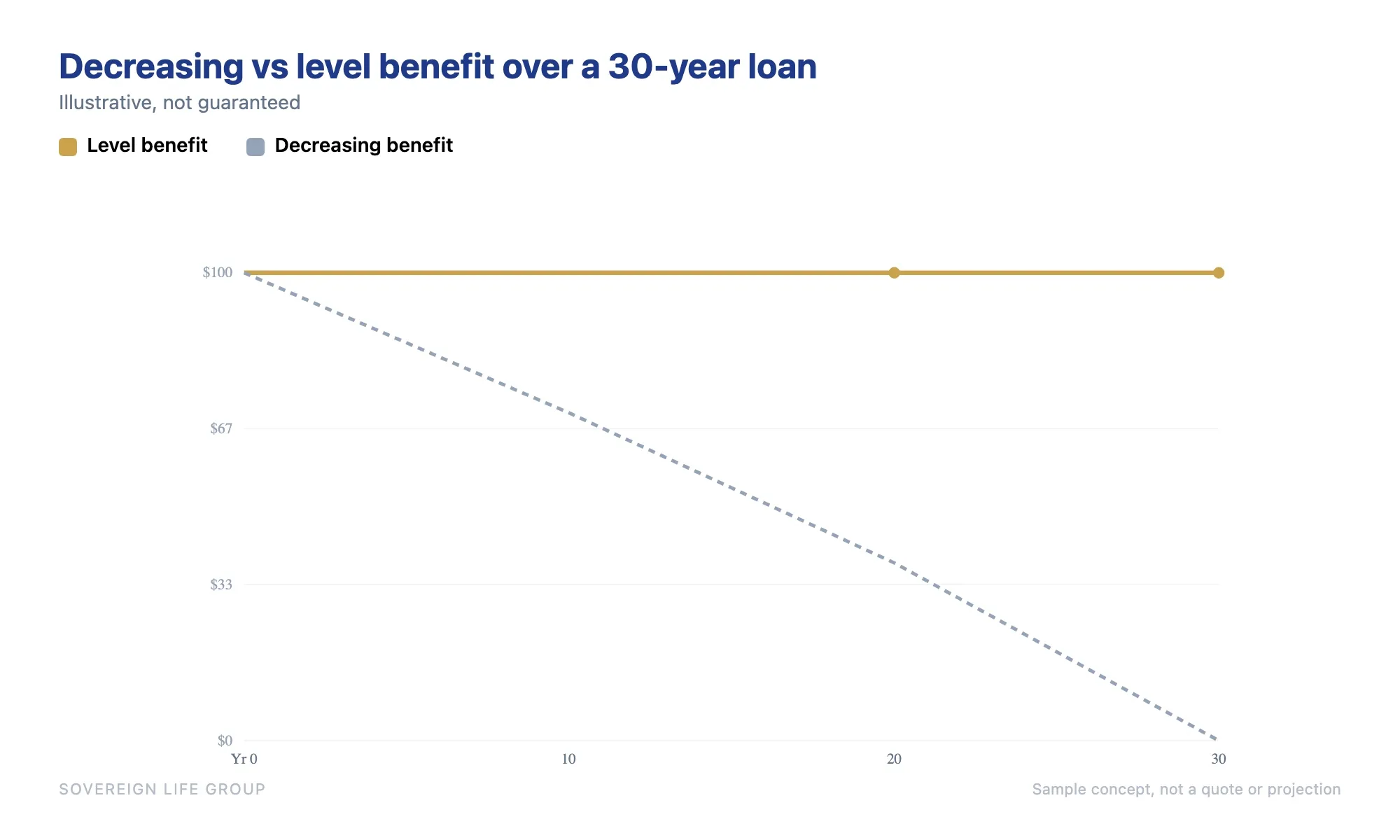

- Decreasing term. The benefit shrinks over time, roughly tracking your loan balance as you pay it down. Because the payout the insurer might owe gets smaller each year, this version is often cheaper. The trade-off is that the benefit is tied to the mortgage and tends to leave nothing extra behind.

- Level term. The benefit stays the same for the whole term, even as your mortgage balance falls. If you passed away in year fifteen of a thirty-year loan, your family could pay off the house and still have money left over for income, childcare, or college. It usually costs a bit more than decreasing coverage, and it does more.

One important note on who controls the money. With a true mortgage protection life policy that you own, your chosen beneficiary, usually your spouse or family, receives the benefit and decides what to do with it. With some lender-offered products, the payout goes straight to the lender to retire the loan. That distinction shapes how much flexibility your family has, and it is one of the first things worth confirming before you sign.

Cover the loan so your family keeps the house. About 2 minutes.

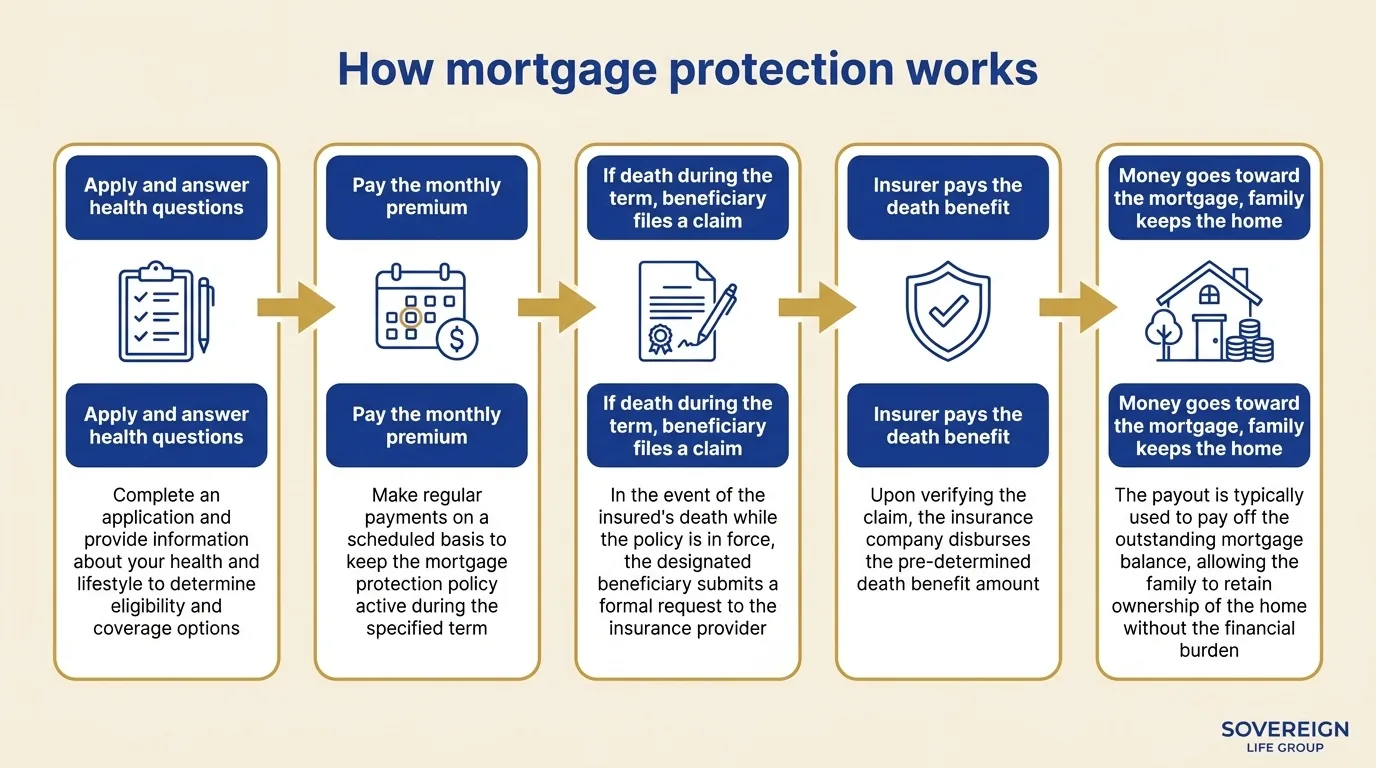

How mortgage protection insurance works

The mechanics are not complicated once you strip away the jargon. You apply, you answer health questions or take a brief exam, the insurer sets a monthly premium, and the policy is in force as long as you pay it. If you pass away during the term, your beneficiary files a claim, the insurer pays the death benefit, and that money goes toward the mortgage. If you outlive the term, the coverage ends and, with most policies, there is no payout, the same way your auto insurance does not refund you for the years you did not crash.

What the policy is built around

A mortgage protection policy is usually sized to two numbers: your loan balance and your remaining term. A family with a 30-year mortgage often buys a 30-year policy so the coverage lasts as long as the debt. Some people match a shorter term to a refinanced loan or to the years until the house is paid off. The closer the policy lines up with the actual obligation, the less you tend to pay for coverage you do not need.

Who gets the money, and when

This is where ownership matters. If you own the policy and name your spouse as beneficiary, the claim pays your spouse, who can then pay the mortgage, or not, depending on what the family needs most that year. That flexibility is valuable. A family might decide to keep a low mortgage rate and use part of the benefit for living expenses instead. With lender-tied coverage where the payout retires the loan automatically, the house gets paid off, but the family loses the option to use those dollars another way.

What it usually does not cover

Standard mortgage protection covers death. It generally does not pay simply because you lost your job, and it does not cover a missed payment because money is tight. Some policies add living benefits through riders, which we cover below, but the base policy is built for the death benefit. Read the contract for exclusions such as a contestability period in the first two years, during which the insurer can review a claim for misstatements on the application.

What it costs and what drives the price

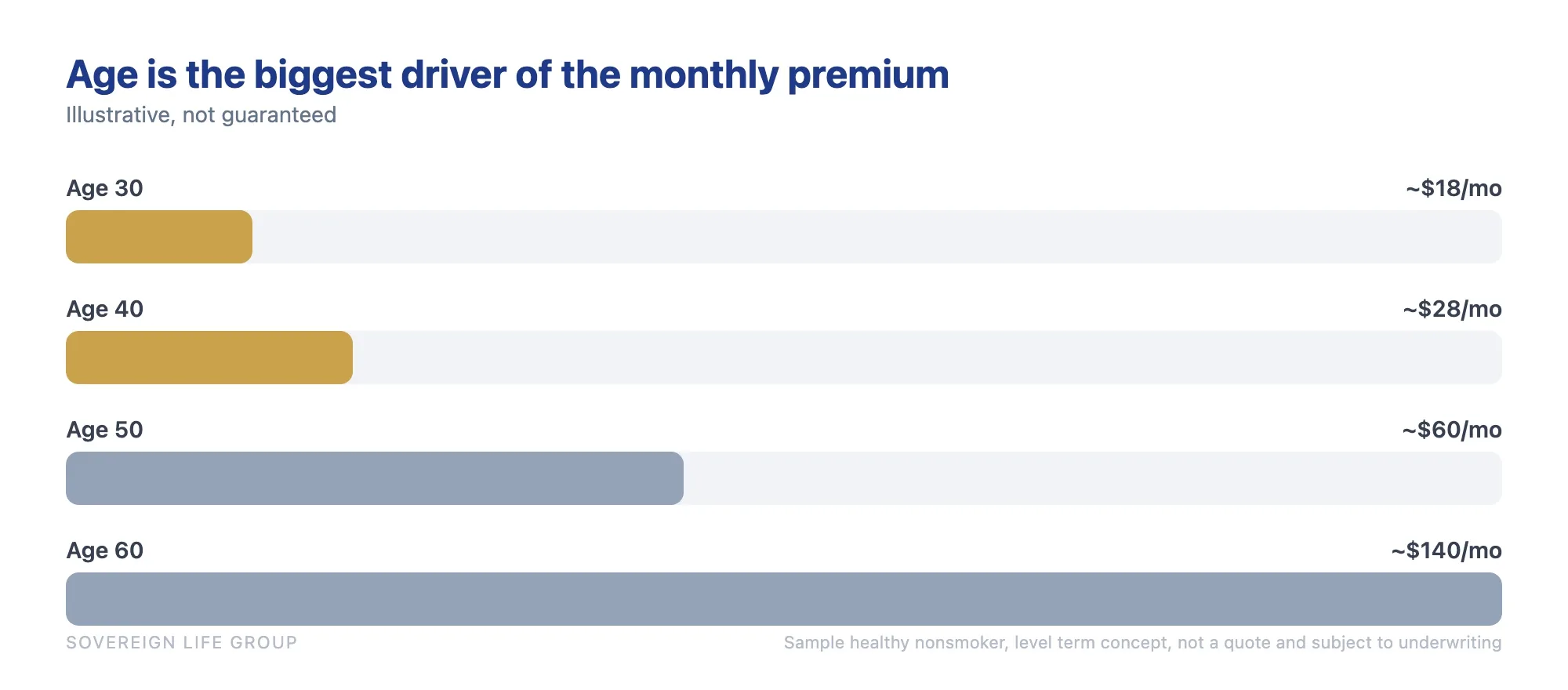

Mortgage protection often costs less than people guess. For a healthy person in their 30s or 40s, meaningful coverage can run in the range of a streaming subscription or two each month. But "often" is doing real work in that sentence, because the price swings widely based on a handful of factors. No honest agent can promise you a specific number from an article, and you should be skeptical of anyone who quotes a flat rate before they know your details.

Here is what actually moves the premium, and which direction.

| Factor | Effect on price | Why |

|---|---|---|

| Your age | Older costs more | Statistical risk of a claim rises each year, so the premium rises with it |

| Your health | Better health, lower price | The rate is built on your health at application, and a level policy locks it in |

| Tobacco use | Smokers pay significantly more | Underwriting treats nicotine as a major risk factor |

| Coverage amount | More benefit, more premium | A larger loan needs a larger benefit to cover it |

| Term length | Longer term, higher price | The insurer is on the hook for more years |

| Level vs decreasing | Level usually costs more | A benefit that stays flat is worth more than one that shrinks |

| Underwriting type | No-exam often costs more | Skipping the exam shifts risk to the insurer, who prices for it |

Two of those factors deserve a closer look because they catch people off guard. The first is the gap between fully underwritten coverage and no-exam coverage. Skipping the needle is convenient, and for some people with a health history it is the difference between getting covered and not. But that convenience is rarely free. If you are healthy and willing to do a brief exam, you will often qualify for a lower price on a fully underwritten policy. If exams are the thing that has stopped you for years, a no-exam option that gets you covered today beats a perfect policy you never buy.

The second is your health timeline. Your rate is set by the version of you that applies, and a level term policy locks that rate in for the whole term. Health rarely improves quietly while you wait. Blood pressure creeps up, a routine physical flags cholesterol, a diagnosis enters the family history. None of that means you cannot get covered later, but it can mean a higher price or a different policy type. That is why the cheapest day to buy is usually the soonest one you reasonably can. Our companion piece on the best age to buy life insurance walks through that math in detail.

Mortgage protection vs PMI: a common and costly mix-up

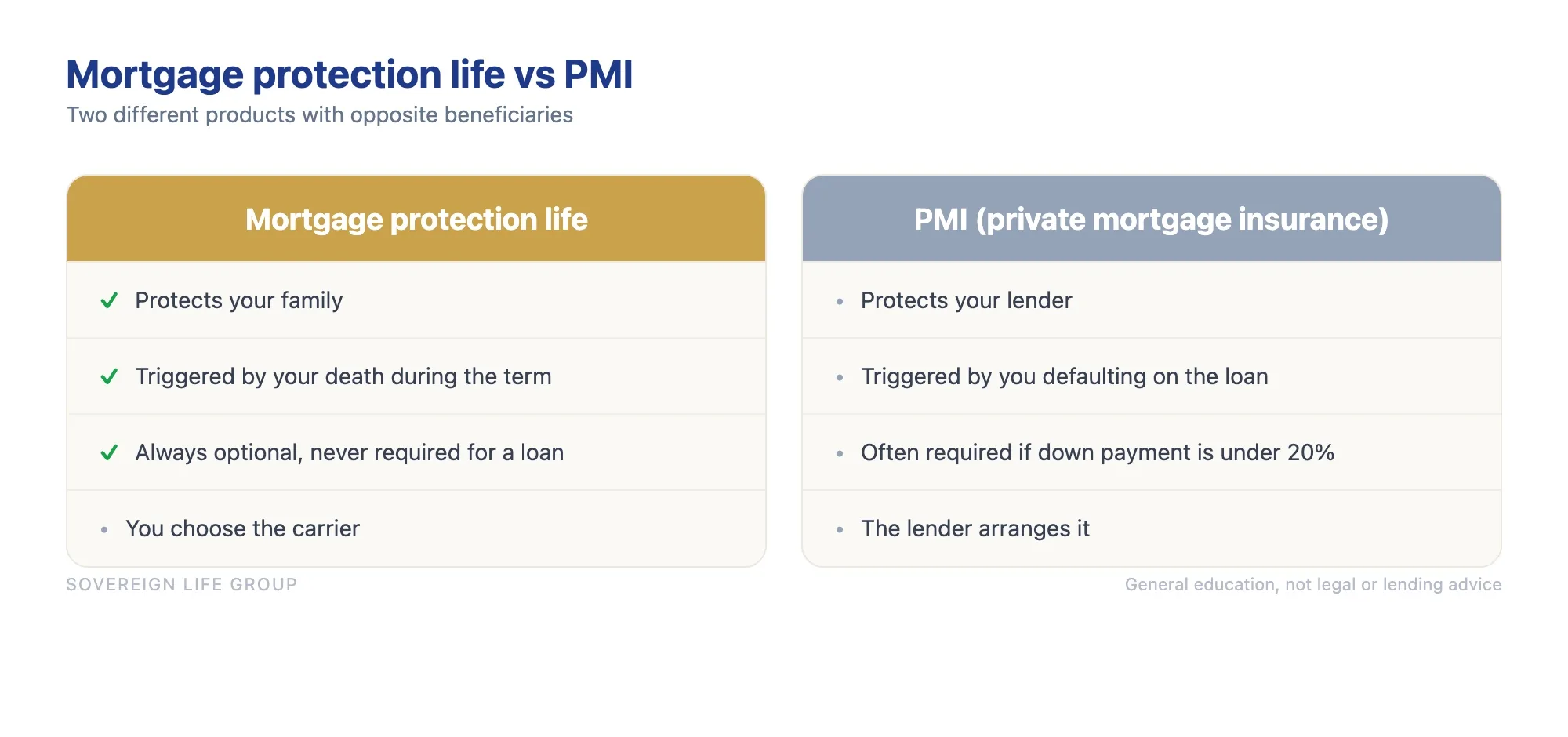

This is the single most frequent confusion I hear, and it costs people clarity right when they need it. Mortgage protection is not the same as PMI, which stands for private mortgage insurance. They sound alike and they are completely different products.

PMI protects your lender. When you put down less than twenty percent on a home, the lender often requires PMI so that if you stop paying and the loan goes into default, the insurer covers part of the lender's loss. You pay for it, but you are not the one being protected, and it does nothing for your family if you die. PMI usually falls away once you build enough equity, and the lender, not you, is the one made whole.

Mortgage protection life insurance protects your family. It is optional, it is never required to close a loan, and the benefit exists so your household can keep the home if your income disappears. Same neighborhood of words, opposite beneficiaries.

| Question | Mortgage protection life | PMI (private mortgage insurance) |

|---|---|---|

| Who is protected? | Your family | Your lender |

| What triggers it? | Your death during the term | You defaulting on the loan |

| Is it required? | No, always optional | Often required if down payment is under twenty percent |

| Can it go away? | Ends when the term ends | Usually drops off once you reach enough equity |

| Who chooses the carrier? | You do | The lender arranges it |

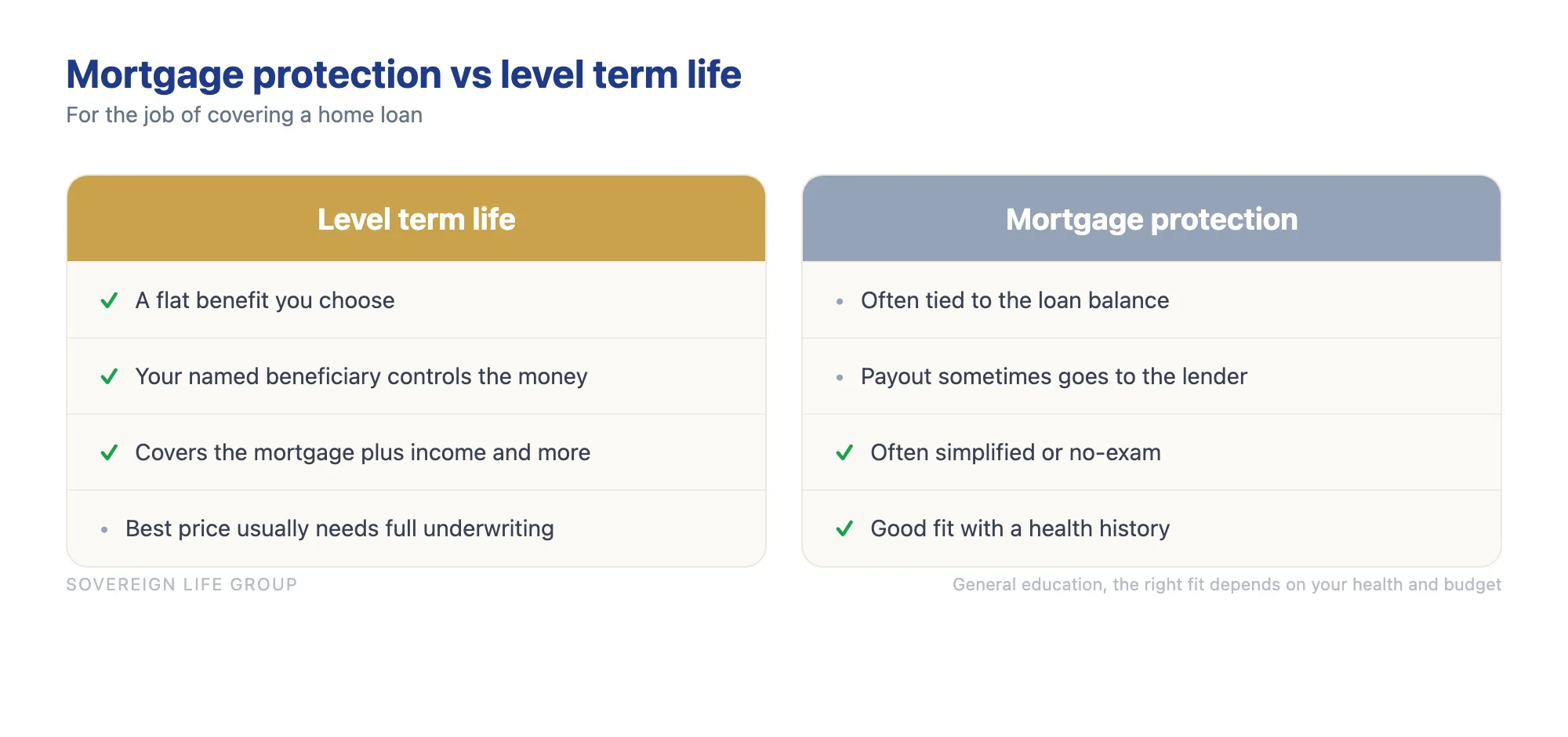

Mortgage protection vs term life insurance

Here is the comparison a lot of sales pitches skip, because it does not always favor the dedicated product. A mortgage protection policy and a plain level term life policy can both pay off your house. The difference is what else they do, and how flexible the money is, which our side by side breakdown of mortgage protection vs term life and which protects the house better walks through in detail.

Term life insurance is just a death benefit for a set number of years, paid to whoever you name. You can buy it large enough to cover the mortgage and replace years of income, and your family decides how to use it. A dedicated mortgage protection policy is often narrower by design, sometimes paying the lender directly, sometimes using a decreasing benefit that only ever tracks the loan. For a healthy buyer, level term frequently delivers more coverage and more flexibility for a similar price.

So why does mortgage protection still exist and still make sense for plenty of people? Because it is often easier to qualify for, faster to put in place, and available with simplified underwriting when health history would complicate a fully underwritten term policy. If you have a condition that makes traditional underwriting difficult, the simplified path can be the realistic one. To understand how carriers actually view common diagnoses, our overview of life insurance with health conditions is a useful next read.

| Factor | Mortgage protection | Level term life |

|---|---|---|

| What it pays | Often tied to the loan balance | A flat benefit you choose |

| Who controls the money | Sometimes the lender, sometimes your family | Always your named beneficiary |

| Flexibility of payout | Lower, aimed at the mortgage | Higher, covers mortgage plus income and more |

| Ease of approval | Often simplified or no-exam | Best price usually needs full underwriting |

| Typical best fit | Health history, want speed and simplicity | Healthy buyer who wants the most coverage per dollar |

The riders people actually ask about

A rider is an optional add-on that expands what a policy does, usually for an extra cost. Riders are where mortgage protection can start to feel genuinely useful beyond the death benefit, but they are also where a simple policy can get expensive fast. Add only what fits your situation. Here are the ones that come up most.

- Disability or disability income rider. Helps cover payments if a covered disability keeps you from working. Useful because disability, not death, is the more common reason a household suddenly cannot make the mortgage.

- Critical or chronic illness rider. Lets you access part of the benefit early as a living benefit if you are diagnosed with a qualifying serious illness. The money can help with bills during treatment rather than only after death.

- Return of premium rider. Refunds some or all of your premiums if you outlive the term. It sounds appealing, but it raises your cost meaningfully, so weigh whether you would rather pay less now and invest the difference.

- Unemployment or layoff rider. May cover a few months of payments if you lose your job involuntarily. Coverage is usually narrow and time-limited, so read the conditions closely.

- Children's term rider. Adds a small amount of coverage on your children. Inexpensive, and for some families a meaningful peace-of-mind item, though it is not the core reason to buy.

The honest trade-off with riders is the same every time: each one adds cost, and the value depends entirely on your odds of using it. A disability rider can be worth real money to a sole earner in a physical job and close to pointless for someone with strong long-term disability coverage through work. Match the rider to the risk you actually carry, not to the longest list the brochure offers.

See what it costs to keep your family in the home. No pressure.

Those official-looking letters in the mail

Buy a home and you will soon receive envelopes that look like they came from your lender or a government office. They often print your lender's name, your loan amount, and a stamped "urgent response required" warning, and they urge you to call about your "mortgage protection." These are marketing pieces, not notices from your lender, and the urgency is manufactured.

None of this means mortgage protection is a scam. It means the mail is designed to pressure you, and pressure is the enemy of a good decision. A few guardrails:

- Your lender did not send it. Loan details are pulled from public records, which is why the letter can quote your balance.

- Mortgage protection is never required to keep your loan. Any letter implying otherwise is being misleading.

- You do not have to buy through whoever mailed you. You can compare options on your own timeline with a licensed agent you choose.

- Slow down. A legitimate policy will still be available next week. Real urgency in insurance comes from your health and age, not a deadline printed on a flyer.

If a letter ever leaves you unsure, the safest move is to set it aside and talk to a real person who is not the one who mailed it. You can always reach out and ask a licensed human rather than respond to a stamp that says urgent.

When you probably need mortgage protection

Coverage is about responsibility, not age. If one of these describes you, having protection for the home loan in place usually makes sense, whether through a dedicated policy or term life.

- You have a mortgage and a family that depends on your income.

- Your partner could not comfortably cover the loan alone if your paycheck stopped.

- You want the house to stay the family's, not the bank's, no matter what.

- You have a health history that makes simplified or no-exam coverage the realistic path to getting protected.

- You are the sole earner, or the larger earner, and the household budget leans on you.

Buying a home is itself one of the classic moments to put coverage in place, right alongside getting married or having a child. A mortgage is a long obligation that does not pause if your income stops, which is the heart of mortgage protection coverage: keeping your family in the home rather than forcing a sale during a hard season.

When you probably do not need it

An article that only says "buy now, buy more" is a sales pitch, not advice. So here are the honest cases where you can skip a dedicated mortgage protection policy or buy less.

- The home is paid off, or nearly so. There is little balance left to protect.

- You already carry enough term life insurance to cover the mortgage and then some. Layering a second mortgage-specific policy on top can be redundant.

- Your household could absorb the payment on one income without strain.

- You have substantial savings or investments your family could use to cover or retire the loan.

- You are being steered toward a pricier or narrower product when plain level term clearly fits the job better.

The goal is the right coverage for your actual situation, not the biggest policy or the most expensive product. More is not automatically better. Sometimes the smartest move is one well-sized term policy that does several jobs at once.

How much coverage and how long a term

If you decide coverage makes sense, two questions follow: how big and for how long. Neither requires you to become an insurance expert.

For the amount, start with the obligation you are protecting. At a minimum that is your current mortgage balance. Many families size the benefit a little higher so there is room for property taxes, insurance, and a cushion of living expenses, or they fold the mortgage into a larger term policy that also replaces income. If your aim is purely "pay off the house," your loan balance is your floor. If your aim is "keep my family stable," the number is usually bigger than the loan alone.

For the term, match it to how long the need lasts. A 30-year mortgage often pairs with a 30-year policy. If you refinanced and have 22 years left, a shorter term can fit and cost less. The principle is simple: do not pay for years of coverage past the point your family would still need the house protected, and do not cut the term so short that it ends while the debt and the dependents are still there.

How to shop for it without overpaying

Here is the practical path, in the order I would walk a friend through it.

- Decide what the money is really for. Just the mortgage, or the mortgage plus income and final expenses? The job determines whether a dedicated mortgage policy or broader term life is the better tool.

- Compare mortgage protection against level term. Get both on the table. For many healthy buyers, term wins on flexibility and price. For others, simplified mortgage protection wins on ease of approval. There is no universal answer, only the right answer for you.

- Confirm who owns the policy and who gets paid. Owning the policy and naming your family as beneficiary keeps the flexibility in your hands. Coverage that pays the lender directly is more rigid.

- Apply while your health is on your side. The application captures today's health, and today is, on average, the best it will be going forward.

- Read the riders before adding them. Add what matches a real risk you carry. Skip the rest. A leaner policy you keep beats a loaded one you cancel.

- Use a licensed agent who shows you options. If someone only ever presents one product, that is a flag. You want choices and trade-offs, not a single pitch.

As a point of reference on why this matters, according to research published by LIMRA, a large share of Americans say they own less life insurance than they know they need, and a common reason is the belief that it costs far more than it actually does. The Insurance Information Institute is another neutral place to read up on how term policies are structured before you talk to anyone trying to sell you one. When you are ready for a real conversation, you can find a clear, no-pressure look at your numbers with Sovereign Life Group, your life insurance strategist.

Is mortgage protection worth it? An honest verdict

Strip everything down and the verdict is two-sided, which is exactly why it gets oversimplified in sales material. Having protection for the mortgage in place is worth it for most families with a home loan and dependents, because the alternative is leaving your household one bad day away from selling the house. That part is not really debatable.

Whether a dedicated mortgage protection policy is the best vehicle is the more nuanced question. If you are healthy and can qualify for fully underwritten term life, a level term policy usually gives you more coverage, more flexibility, and a comparable price, while also protecting your income, not just the house. If your health history makes traditional underwriting hard, or you value speed and simplicity, a simplified mortgage protection policy can be the right and realistic call. Both are legitimate. The wrong move is buying the first thing a high-pressure letter or call puts in front of you without comparing.

So the worth-it answer is this: protect the home, yes. Choose the tool on purpose, after you have seen the options side by side and understood the trade-offs. That is the entire reason this mortgage protection guide exists.

Want a straight answer for your situation?

Fifteen minutes. We will look at your mortgage, your budget, your health, and the simplest way to protect both the home and your family. No pressure, no jargon, just options laid out plainly.

Get a Quote Book a 15-Min Review Prefer to start small? Visit the families coverage page to see how protection fits a household budget.Frequently asked questions

Is mortgage protection insurance the same as PMI?

No. PMI, or private mortgage insurance, protects your lender if you stop paying and is usually required when your down payment is under twenty percent. Mortgage protection life insurance protects your family by paying a benefit if you pass away, so they can keep the home. Different product, different beneficiary, different purpose.

Is mortgage protection insurance worth it?

If your family would struggle to cover the mortgage without your income, having coverage in place is usually worth it. Whether a dedicated mortgage protection policy is the best tool is a separate question. For many healthy buyers, a level term life policy does the same job with more flexibility for a similar price, so it is worth comparing both before you decide.

Does mortgage protection insurance require a medical exam?

Not always. Many mortgage protection and simplified-issue policies use a short set of health questions instead of a full exam. Coverage amounts may be capped and the price can be higher than a fully underwritten policy, but approval is often faster, which helps people who want coverage in place quickly or who have a health history.

What happens to my mortgage if I die without coverage?

The loan does not disappear. Whoever inherits the home inherits the payments. If the household cannot cover those payments from savings, other insurance, or a surviving income, the family often has to sell the home, sometimes during the hardest months of their lives.

Can I get mortgage protection insurance if I have health conditions?

Often yes. Simplified-issue and guaranteed-issue options are built for people who may not qualify for fully underwritten coverage. They typically cost more per dollar of benefit and may include a waiting period, but they make it possible to protect the home even with a diagnosis. The right fit depends on the condition, your age, and the carrier.

Is mortgage protection insurance required to get a loan?

No. Mortgage protection life insurance is optional and is never a condition of getting a mortgage. PMI can be required by the lender when your down payment is small, but that is a different product that protects the lender, not your family. Be cautious of any letter or call that implies mortgage protection life insurance is mandatory.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.