Living Benefits Life Insurance: Use Your Policy While Alive

The Short Version

Most people think life insurance only pays out after you die. Living benefits are the part you can use while you are still alive. If you are diagnosed with a terminal, chronic, or critical illness, accelerated death benefit riders let you pull money from your own policy to cover treatment, income, or daily life. The catch worth knowing up front: whatever you take early lowers what your family receives later, often by a little more than the dollars you draw.

Here is the part of the conversation that surprises almost everyone I sit down with: a good life insurance policy can pay you while you are still here. People picture life insurance as a check that arrives after a funeral. That is the death benefit, and it matters. But living benefits life insurance flips the timeline. If a serious illness hits, the right policy can put a meaningful chunk of money in your hands during the hardest stretch of your life, when the medical bills are real and the paycheck has stopped.

This guide walks through exactly how that works in plain language: what living benefits are, the three illness triggers that unlock them, how the payout is actually calculated (including the discount almost nobody explains), what it costs, how taxes treat it, a real worked example, and the honest cases where you do not need to pay extra for any of it. I write this as a licensed agent, not a marketer chasing a sale, so you will also read where the fine print bites.

What this guide covers

- What living benefits life insurance actually is

- The three illness triggers

- How the payout is really calculated

- Living benefits on term vs permanent

- Cash value as a living benefit

- A real worked example

- How to file a living benefits claim

- What living benefits cost

- Taxes and the fine print

- Living benefits vs standalone coverage

- Who needs them and who can skip

- Common mistakes to avoid

- Frequently asked questions

What living benefits life insurance actually is

Living benefits are features of a life insurance policy that you can use while you are still alive, rather than benefits that pay out only after you pass away. The phrase covers a family of options, but the heart of living benefits life insurance is a simple idea: under certain serious circumstances, you can reach into your own death benefit early and use the money now.

The main engine behind this is something called an accelerated death benefit. An accelerated death benefit rider lets you receive part of your policy's death benefit ahead of schedule if you are diagnosed with a qualifying illness. The word "accelerated" is doing the work there. You are not getting bonus money on top of the policy. You are getting some of the death benefit early, which is why it gets subtracted from what your beneficiaries collect later. We will return to that trade-off because it is the single most misunderstood part of the whole subject.

Underneath the accelerated death benefit umbrella sit the specific riders you will hear named:

- Terminal illness rider. Pays early when a physician certifies you have a limited life expectancy, commonly twelve to twenty four months depending on the carrier.

- Chronic illness rider. Pays early when you can no longer perform a set number of basic daily activities, or have a serious cognitive impairment such as advanced dementia.

- Critical illness rider. Pays early on specific severe diagnoses such as a heart attack, stroke, invasive cancer, or a major organ transplant.

Beyond the accelerated death benefit family, two other things often get filed under living benefits. The first is the cash value inside a permanent policy, which you can borrow against or withdraw while alive. The second is a small group of extras like a return of premium feature on some term policies, or a long-term care rider that functions much like a chronic illness rider but is built specifically around care costs. We will sort all of these out so the labels stop blurring together.

Tax-advantaged growth with a floor against losses. Quick and free.

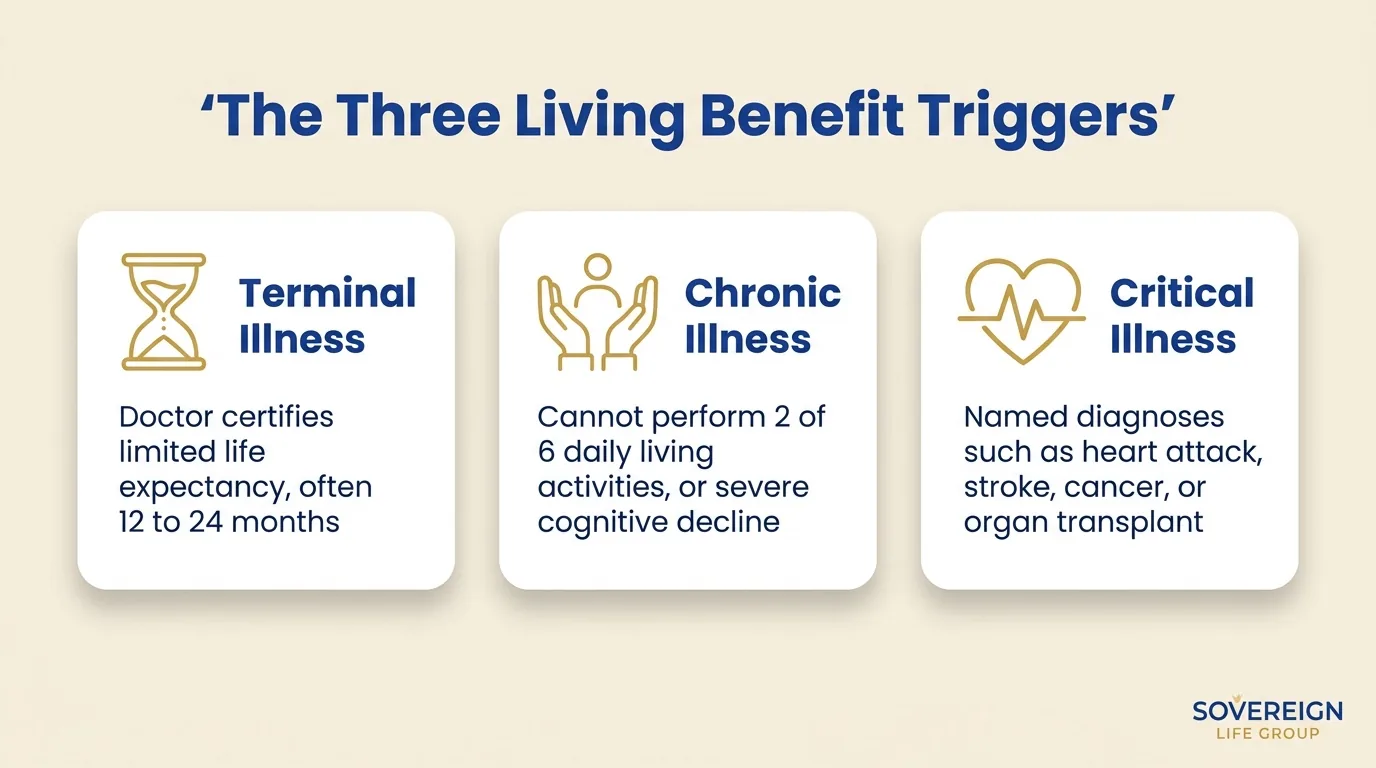

The three illness triggers that unlock living benefits

Almost every accelerated death benefit rider is built around one of three triggers. They sound similar, but each one has a different definition, a different bar to clear, and a different feel in real life. Knowing which triggers your policy actually carries is more important than the marketing label on the brochure.

Terminal illness

This is the original living benefit and the most widely included. A terminal illness rider activates when a doctor certifies that your life expectancy is below a stated threshold, usually twelve months at some carriers and up to twenty four months at others. Because the insurer is going to pay the death benefit soon regardless, advancing part of it early is relatively straightforward. Many companies include a terminal illness rider at no separate premium. It exists so that someone facing the end has the option to settle affairs, travel, pay for care, or simply remove money worry from their final months.

Chronic illness

A chronic illness rider is about function, not life expectancy. It typically activates when a licensed health professional certifies that you cannot perform a certain number of Activities of Daily Living, usually two of the six. Those six are bathing, dressing, eating, toileting, transferring (getting in and out of a bed or chair), and continence. The rider also commonly triggers on a severe cognitive impairment such as Alzheimer's, even if the body can still do those tasks. This is the rider that overlaps most with long-term care, because the situations that set it off are exactly the situations that drive care costs.

Critical illness

A critical illness rider keys off specific, named diagnoses rather than function or life expectancy. The exact list varies by carrier, but it usually centers on events like a heart attack, stroke, invasive cancer, kidney failure, major organ transplant, or paralysis. The point is to deliver a lump sum at the moment of a major medical event, when out-of-pocket costs spike and work often stops, even if you are expected to recover fully. Of the three, critical illness is the one most likely to pay on something you survive and move past.

| Trigger | What sets it off | Typical use |

|---|---|---|

| Terminal illness | Physician certifies limited life expectancy, often 12 to 24 months | End-of-life care, settling affairs, removing money stress |

| Chronic illness | Cannot perform 2 of 6 daily living activities, or severe cognitive decline | Home care, caregiving help, daily living costs |

| Critical illness | Specific diagnoses such as heart attack, stroke, cancer, organ transplant | Treatment costs and lost income during and after a major event |

One policy can carry more than one of these triggers, and the strongest living benefits packages include all three. When you compare options, do not just ask "does it have living benefits." Ask which of the three triggers are included, how each is defined, and how much of the death benefit each one lets you accelerate. Two policies can both advertise living benefits and still be miles apart on the details that matter.

How the payout is really calculated

This is the section most articles skip, and it is the one that prevents an unpleasant surprise later. When you accelerate a death benefit, you usually do not receive the full face amount you request. Carriers use one of two broad approaches, and the difference can be tens of thousands of dollars.

The discounted, or lien, method

Many chronic and critical illness riders pay on a discounted basis. The insurer looks at your age, your health, and how much benefit you want to accelerate, then applies a discount because it is handing you money years before it expected to. In practice that means a request to accelerate one hundred thousand dollars of death benefit might put somewhere less than that in your pocket, and the full one hundred thousand still gets deducted from the future payout. The size of the discount depends heavily on the severity of the condition and your life expectancy at claim time. The more your situation looks like a near-term claim, the smaller the discount tends to be.

The dollar-for-dollar method

Other riders, more often terminal illness riders, pay closer to dollar for dollar, sometimes minus a modest administrative fee and an interest adjustment. Here, accelerating one hundred thousand dollars puts close to one hundred thousand dollars in hand, and one hundred thousand comes off the death benefit. This is cleaner and easier to plan around, which is part of why terminal riders are so commonly included.

Either way, the core rule holds: living benefits reduce the death benefit. You are spending your own future payout early. That is not a flaw. It is the entire design. But it means the decision to accelerate is a real trade-off between your needs today and your family's needs tomorrow, and a good agent will walk you through both sides rather than only the upbeat one.

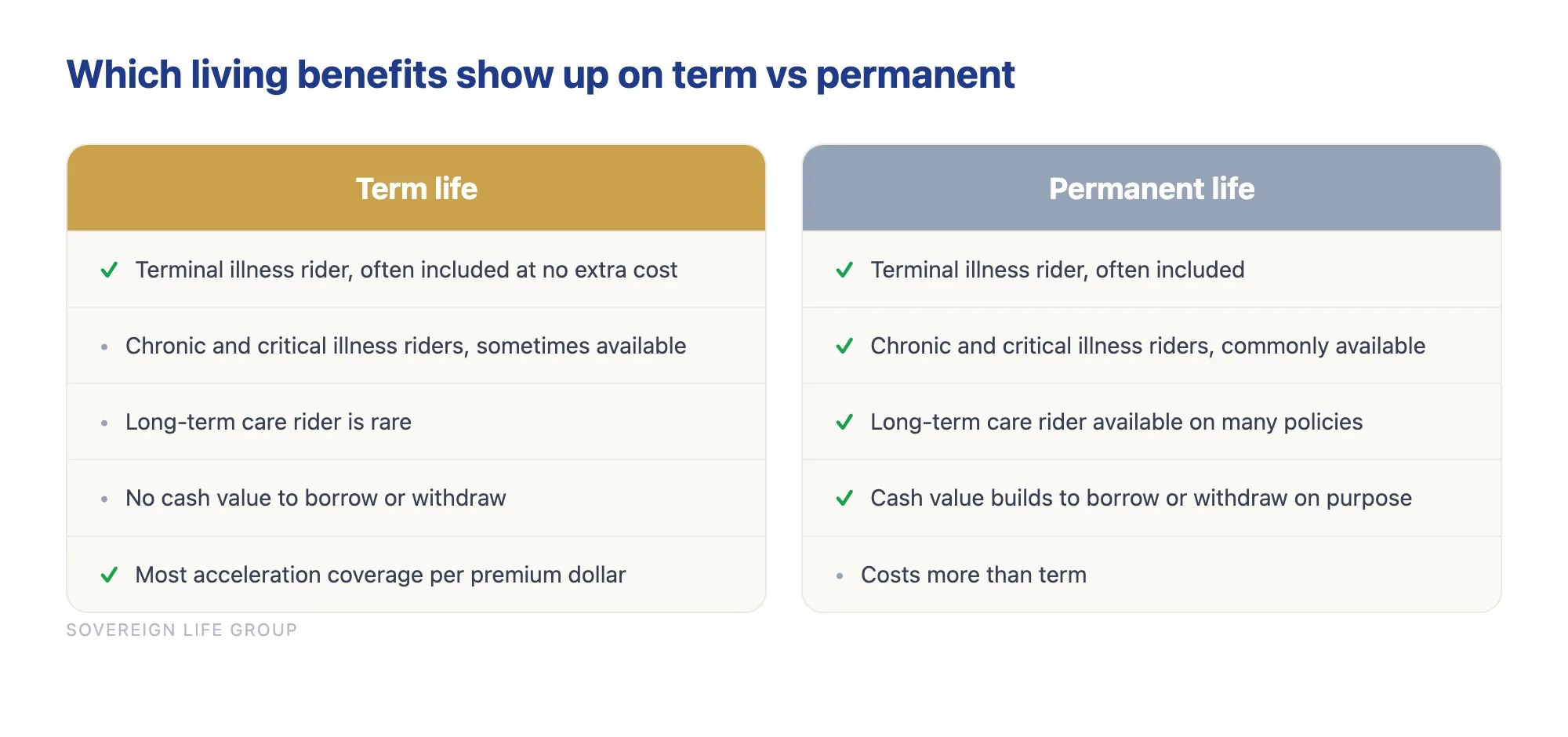

Living benefits on term vs permanent policies

People often assume living benefits only come with expensive permanent policies. That is not true. Accelerated death benefit riders show up on plenty of term policies too, frequently at no extra premium for the terminal illness piece. What changes between term and permanent is the menu, not whether the door exists at all.

Term life is pure death benefit for a set number of years. Many term policies include or allow accelerated death benefit riders for terminal illness, and a growing number add chronic and critical illness options. What term cannot give you is cash value, so the borrowing style of living benefit is off the table. If your goal is the most acceleration coverage per dollar of premium, a strong term policy with robust living benefit riders is often the efficient choice. Our breakdown of term versus whole life insurance digs into that structural choice in more depth.

Permanent life, including whole life and indexed universal life, can carry the same illness riders and adds the cash value dimension. That cash value grows over time and becomes a pool you can borrow against or withdraw from for any reason, not just illness. For people who want a living benefit they can use on purpose rather than only in a medical crisis, that is the appeal. It also costs more, and the trade-offs deserve honest scrutiny, which is exactly what we cover in our guide to using an indexed universal life policy for tax-advantaged retirement income.

| Living benefit | Term life | Permanent life |

|---|---|---|

| Terminal illness rider | Often included | Often included |

| Chronic illness rider | Sometimes available | Commonly available |

| Critical illness rider | Sometimes available | Commonly available |

| Long-term care rider | Rare | Available on many policies |

| Cash value to borrow or withdraw | No | Yes, builds over time |

| Return of premium feature | On some policies | Not applicable in the same way |

Cash value: the living benefit you build on purpose

The illness riders are living benefits you hope never to use. Cash value is the living benefit you can plan to use. Inside a permanent policy, part of what you pay builds an accumulating value that belongs to the policy and grows on a tax-advantaged basis. You can borrow against it or withdraw from it during your lifetime, for a down payment, a business need, a college bill, or income in retirement.

There are three honest things to keep in mind here. First, cash value takes years to build into anything meaningful, so this is a long-game benefit, not a quick one. Second, an unpaid policy loan reduces the death benefit your family receives, the same trade-off as accelerating, just through a different door. Third, the growth and the costs depend on the product and, in the case of indexed policies, on how the underlying index performs within the policy's limits. Nobody can promise you a specific return, and you should be skeptical of anyone who does.

Used carefully, cash value is a genuine living benefit that can quietly do a lot of work over a lifetime. Used carelessly, or oversold on rosy projections, it can disappoint. The right approach is to look at conservative numbers, understand the fees, and decide whether the structure fits your goals. If retirement income is the driver, the indexed universal life coverage page lays out how that design works and where the limits are.

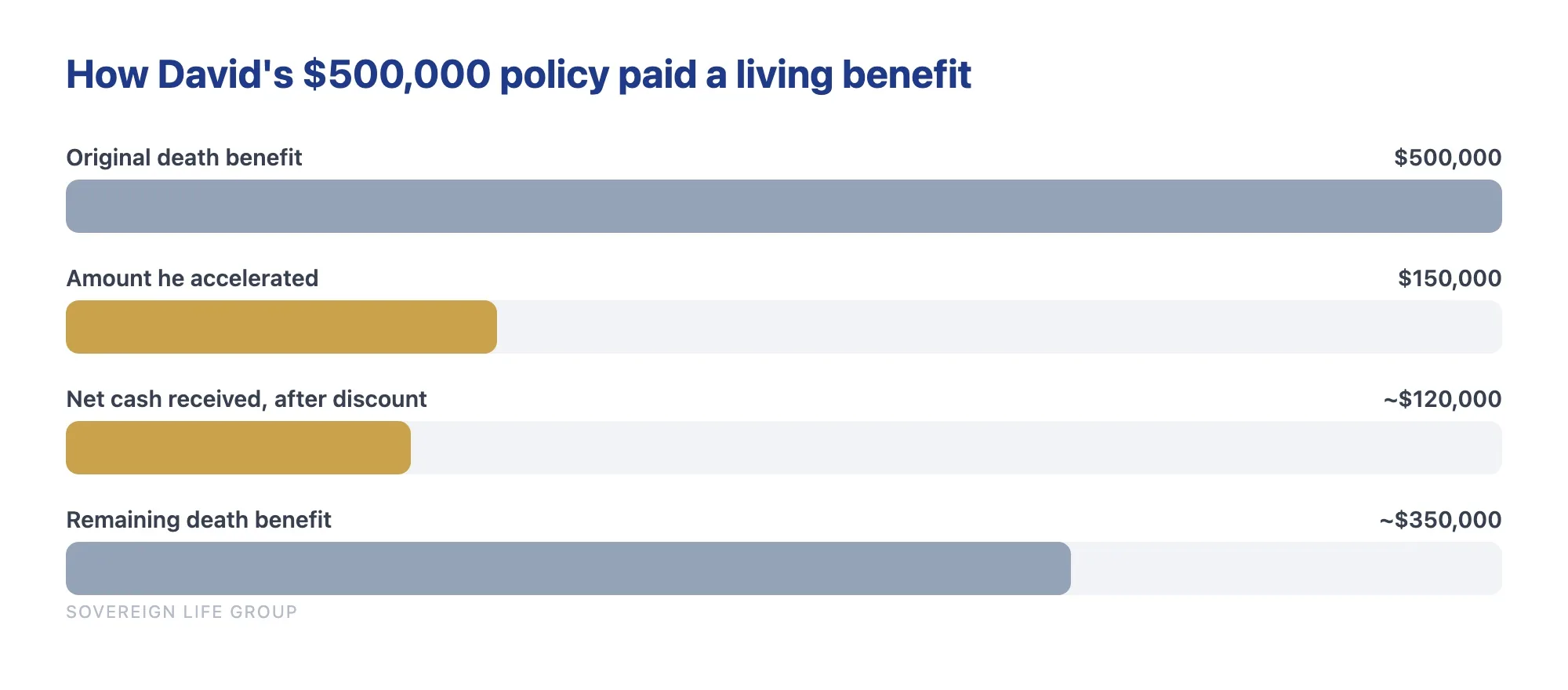

A real worked example

Numbers make this concrete. Let me walk through a realistic scenario. The figures below are illustrative, chosen to show the mechanics, not a quote or a promise of how any specific policy would pay.

Picture David, age 48, a married father of two with a $500,000 term life policy that includes accelerated death benefit riders for terminal, chronic, and critical illness. David is the household's main earner. One spring he has a serious heart attack and, during recovery, is diagnosed with a condition that limits his ability to work for the foreseeable future.

Here is how living benefits could play out for his family:

- The critical illness trigger fires. A heart attack is a named critical illness on his policy. David files a claim and elects to accelerate $150,000 of his $500,000 death benefit.

- The carrier applies its calculation. Because this rider pays on a discounted basis, the net advance David receives is less than the full $150,000 he accelerated. For the sake of the example, say he nets roughly $120,000 after the discount. That cash is his to use however he chooses.

- The money goes to work immediately. David covers out-of-pocket medical costs, keeps the mortgage current while he is out of work, and buys his family breathing room instead of panic.

- The death benefit adjusts. The $150,000 he accelerated is subtracted from the policy. His remaining death benefit is now about $350,000, still in force for his wife and children should the worst happen later.

Notice the two truths sitting side by side. David got real money at the worst possible moment, which is the whole point of living benefits life insurance. And the family's future payout dropped by more than the cash he received, which is the cost of getting it early. Neither truth cancels the other. The benefit was almost certainly worth it for David. It is just not free, and anyone who pretends otherwise is selling, not advising.

See the strategy applied to your age and goals. No pressure.

How to file a living benefits claim

If you ever need to use these riders, the process is more human than the paperwork makes it look. Here is the general path, recognizing that each carrier has its own forms and timelines.

- Confirm the rider and the trigger. Pull your policy or call your agent and verify which living benefit riders you actually carry and which trigger your diagnosis falls under. This is where having an agent who knows your file pays off.

- Gather medical certification. The carrier will require documentation from your physician, a terminal prognosis, proof you cannot perform the required daily living activities, or confirmation of a qualifying critical diagnosis, depending on the trigger.

- Request a benefit illustration. Ask the insurer to show you, in writing, the net advance you would receive for a given acceleration amount and the resulting reduction to your death benefit. Decide how much to accelerate based on those real numbers, not a guess.

- Submit the claim and elect your amount. You usually do not have to accelerate the maximum. Take what you need and leave the rest as death benefit for your family if that fits your situation better.

- Receive the funds. Payouts commonly arrive as a lump sum, though some chronic illness and care-focused benefits can be structured as monthly payments. The money is generally yours to use for anything, not just medical bills.

A practical tip: do not wait until a crisis to learn what your policy contains. Read your riders now, while nothing is wrong, so that if a hard day comes, your family is not deciphering a contract under stress. If you are not sure what you have, that is a normal reason to book a quick policy review and get a clear summary in plain English.

What living benefits cost

The honest answer is "it depends," and the variation is wide enough that flat statements should make you cautious. Living benefits riders are priced in a few different ways, and it is worth knowing which one applies before you sign.

- Built in at no separate charge. Many terminal illness riders, and some chronic and critical riders, are simply included. The cost is baked into the base premium rather than billed as a line item.

- Free to add, paid when used. Some riders cost nothing extra to attach but charge you at claim time through the discount applied to your acceleration. You pay only if you ever use it.

- An additional premium. Richer riders, especially robust chronic illness or long-term care features, may add to your monthly premium for the life of the policy.

Because the structures differ so much, the only number that matters is your number, for your age, your health, the carrier, and the riders you choose. Be wary of any quote presented before someone knows those details, and be just as wary of an article, including this one, that pretends to know your price. What I can tell you is that adding strong living benefits often costs less than people expect, and for many families it is one of the higher-value dollars in the whole policy. According to the Insurance Information Institute, riders like accelerated death benefits are now common features rather than exotic add-ons, which has helped bring their cost down over time.

Taxes and the fine print most people miss

Living benefits can carry favorable tax treatment, but the rules are specific and this is squarely an area to confirm with a professional rather than trust a blog. Here is the lay of the land, in general terms.

Under federal tax law, accelerated death benefits paid because of a terminal illness are generally received income tax free, much like a regular death benefit. Benefits paid for a chronic illness can also be received tax free when the policy and the claim meet the requirements, though there can be daily or annual limits tied to long-term care rules. Critical illness payouts and cash value transactions can be treated differently, and a policy loan handled poorly can create a taxable event you never saw coming. The Internal Revenue Service addresses the treatment of accelerated death benefits in its guidance, and you can read the federal framework directly from the IRS publication on taxable and nontaxable income.

Two pieces of fine print deserve a flashlight. First, the reduction to your death benefit is permanent for the amount you accelerate, so a family that was counting on the full face amount should plan around the lower number. Second, accelerating a benefit can, in some situations, affect eligibility for need-based government programs, because cash in hand counts where a future death benefit does not. None of this should scare you off living benefits. It should simply send you into the decision with eyes open and a tax professional on the phone.

Living benefits vs standalone disability and long-term care insurance

A natural question once you understand living benefits is whether they replace standalone disability insurance or a dedicated long-term care policy. The honest answer is that they overlap but do not fully substitute. Each tool is shaped for a slightly different job, and the smartest plans often layer them rather than pick one.

Standalone disability insurance replaces a portion of your income, month after month, when you cannot work, and it keeps doing so without draining a death benefit. A critical or chronic illness rider, by contrast, hands you a lump sum once and reduces your policy. For a primary earner, disability coverage is built to protect the paycheck specifically; living benefits are built to protect against a major event. They solve related but distinct problems.

Standalone long-term care insurance is designed around extended care costs, with benefit pools and daily limits tuned for years of care. A chronic illness or long-term care rider on a life policy can cover similar ground, with the advantage that if you never need care, the death benefit still goes to your family rather than evaporating. The trade-off is that the care money and the death benefit draw from the same well, so heavy use of one shrinks the other.

| Feature | Living benefits riders | Standalone disability / LTC |

|---|---|---|

| What it pays | Lump sum from your death benefit | Ongoing income or dedicated care benefit |

| Effect on death benefit | Reduces it by the amount used | Leaves any life policy untouched |

| If you never claim | Death benefit passes to family in full | Premiums generally not recovered |

| Best at | One-time crisis cash, broad flexibility | Sustained income or long care episodes |

| Typical cost feel | Often modest add-on to a life policy | A separate, sometimes larger, premium |

This is the content gap most quick explainers leave out: living benefits are not a magic replacement for every other protection. They are a powerful, flexible layer that pairs well with the rest. A balanced plan for a young family, for instance, often starts with enough life insurance carrying solid living benefit riders, and adds disability or care coverage where the gaps are widest. Our overview of how protection fits a household appears on the families coverage guide.

Who needs living benefits and who can skip them

An article that only says "add every rider" is a pitch, not advice. So here is the honest split.

Living benefits are usually worth it if

- You are the primary or sole earner and a serious illness would stop your income cold.

- Your emergency savings would not carry the household through a long treatment or recovery.

- You have a family history that makes a major diagnosis a real, not abstract, risk.

- The rider is included or low cost, in which case the value usually outweighs the small price.

- You want flexible cash in a crisis rather than money locked behind narrow conditions.

You can reasonably skip or minimize them if

- You already carry strong standalone disability and long-term care coverage that does the same job without touching the death benefit.

- Your assets are large enough to self-fund a medical crisis without selling anything you care about.

- A rider adds meaningful premium for a trigger that does not fit your situation, and you would rather buy more base coverage instead.

- You are being steered toward an expensive, loaded policy when a simpler one with the riders you actually need would serve you better.

The goal is the right coverage for your life, not the longest list of features. More riders are not automatically better. Sometimes the smartest move is a clean policy with two well-chosen living benefits and the savings put toward a larger death benefit.

Common mistakes to avoid

After enough honest conversations, the same avoidable errors keep showing up. Here are the ones worth guarding against.

- Assuming the brochure amount is the cash you get. With discounted riders, the net advance is smaller than the accelerated amount. Always ask for the real net figure.

- Forgetting the death benefit shrinks. Money taken early is gone from the future payout. Plan your family's number around what is left, not the original face amount.

- Buying "living benefits" without checking which triggers are included. A policy can advertise the feature and still leave out the trigger you most need. Read the definitions.

- Treating riders as a substitute for disability or care coverage. They overlap but do not fully replace those tools, as the comparison above shows.

- Waiting until a diagnosis to learn the policy. Underwriting captures today's health. The cheapest and easiest day to lock in strong living benefits is usually the soonest one you reasonably can.

- Trusting rosy projections on cash value. Look at conservative numbers and understand the fees before you count on growth. No one can guarantee a return.

Avoid those six and you are ahead of most buyers. The thread running through all of them is the same: living benefits are genuinely valuable, and they reward people who understand exactly what they are buying. When you are ready for a clear, no-pressure look at your own numbers, you can start with Sovereign Life Group, your life insurance strategist.

Want to know what your policy can actually do?

Fifteen minutes. We will look at your current coverage, the living benefits you may already have or be missing, and the simplest way to protect both today and tomorrow. No pressure, no jargon, just options laid out plainly.

Get a Quote Book a 15-Min Call Prefer to start fast? You can save my card or get a quick quote here.Frequently asked questions

What are living benefits on a life insurance policy?

Living benefits are features of a life insurance policy that you can use while you are still alive, instead of only paying out after death. The most common are accelerated death benefit riders that let you draw part of your own death benefit early if you are diagnosed with a terminal, chronic, or critical illness. Permanent policies can also build cash value you can borrow against. The money is yours to use for treatment, bills, or anything else.

Does accessing living benefits reduce the death benefit?

Yes. Money you take through an accelerated death benefit rider is subtracted from the amount your beneficiaries receive later, and many carriers also apply a discount or a small fee because they are paying early. So a one hundred thousand dollar advance may reduce the death benefit by more than one hundred thousand dollars. Cash value loans work differently but also lower the payout if they are not repaid.

Is there an extra cost for living benefits riders?

It depends on the carrier and the rider. Many terminal illness riders are included at no separate premium and are priced into the policy. Chronic and critical illness riders may be free to add but charged when you actually use them, through a discount on the advance, or they may carry an additional premium. Always confirm whether you pay at purchase, at claim, or both.

Are living benefits payments taxable?

Accelerated death benefits paid for a terminal or chronic illness are often received income tax free under federal rules when the policy and the claim meet the requirements, similar to a regular death benefit. Critical illness payouts and cash value transactions can be treated differently. Tax rules depend on your situation, so confirm the treatment with a licensed tax professional before you rely on it.

What is the difference between chronic, critical, and terminal illness riders?

A terminal illness rider applies when a doctor certifies a limited life expectancy, often twelve to twenty four months. A chronic illness rider applies when you cannot perform a set number of daily living activities such as bathing or dressing, or have a severe cognitive impairment. A critical illness rider applies to specific serious diagnoses such as a heart attack, stroke, cancer, or major organ transplant. One policy can carry more than one of these.

Can I add living benefits to a term life policy?

Often yes. Many term policies include or allow accelerated death benefit riders for terminal, and sometimes chronic and critical, illness. What term policies do not build is cash value, so the borrowing style of living benefit applies only to permanent coverage. Availability of each rider varies by carrier, state, age, and health, and any coverage is subject to underwriting approval.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.