Best Age to Buy Life Insurance: Why Waiting Costs You

The Short Version

The best age to buy life insurance is usually your 20s or 30s, when rates are lowest and approval is easiest. But the honest answer is simpler: the right time to buy is the day someone starts depending on your income. If that day already passed, the best age is the one you are today.

Almost everyone who calls me about life insurance says some version of the same thing: "I probably should have done this years ago." They are usually right, and they usually feel worse about it than they need to. So let's deal with the real question head on. The best age to buy life insurance is younger than most people think, and every year of waiting tends to add cost. But "you waited too long" is rarely true, and where you stand today still matters more than where you stood five years ago.

This guide walks through life insurance by age, decade by decade, with a real worked example of what waiting actually costs, the life events that matter more than your birthday, and an honest look at whether it is ever too late. No pressure, no hype, just the math and the trade-offs laid out plainly so you can decide.

What this guide covers

- The short answer on the best age

- Why waiting costs you: the two clocks

- Life insurance by age, decade by decade

- The cost of waiting: a comparison

- A real worked example

- When to buy: events over birthdays

- Is it too late for life insurance?

- Does the best age change by policy type?

- When buying earlier is not the right move

- How to lock in the right rate

- Frequently asked questions

The short answer on the best age to buy life insurance

If you want one number, here it is: for most people the best age to buy life insurance is your 20s or early 30s. That is when premiums are at their lowest and your odds of easy, fast approval are at their highest. A healthy person who locks in a long level term policy in their late 20s often pays a fraction of what the same coverage costs at 45.

But a number alone misses the point. Life insurance is not a thing you buy because of your age. It is a thing you buy because someone would feel a financial hole if your income disappeared. So the deeper answer is this: the best time to buy life insurance is the moment another person starts depending on what you earn or what you do at home. A new spouse, a baby, a mortgage, a business partner, an aging parent you help support. If one of those is already true for you, your best age to buy is not 25 and it is not 35. It is right now, because today you are younger and likely healthier than you will be next year.

No medical exam for a ballpark. Free, and no pressure.

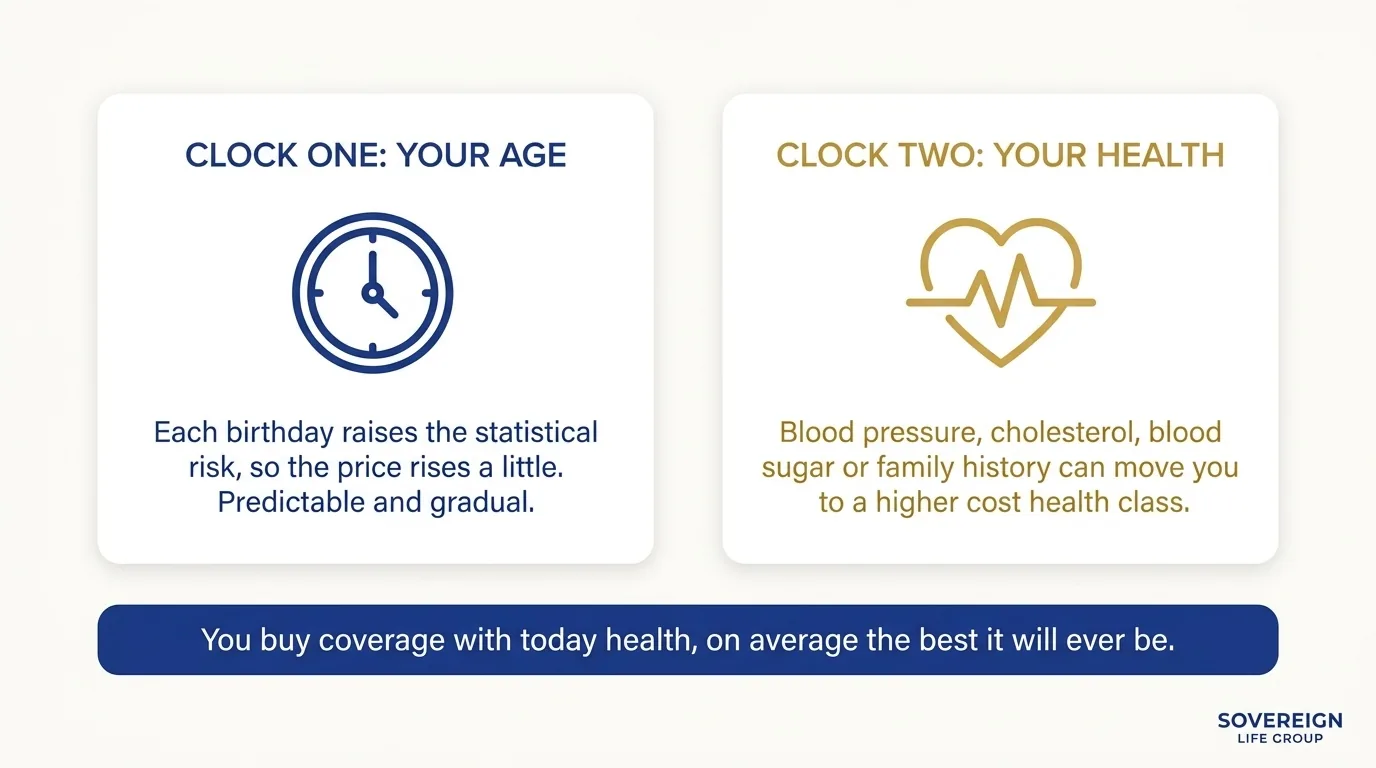

Why waiting costs you: the two clocks running against you

Clock one: your age

Insurers price a policy on the statistical risk that they will pay a claim during the term. Each year you age, that risk rises a little, so the price rises a little. This part is predictable and gradual. A year here or there is not dramatic. A decade is.

Clock two: your health

This is the clock most people forget. Your rate is built on your health at the moment you apply, and a level term policy locks that rate in for the whole term. The problem is that health rarely improves quietly in the background while you wait. Blood pressure creeps up. A routine physical turns up high cholesterol, elevated blood sugar, or a thyroid issue. A parent gets diagnosed with something and now there is family history on your application. None of that means you cannot get covered. It means you may pay more, or move from the best health class to a standard one, or in some cases need a different type of policy.

Here is the uncomfortable truth that makes the best age to buy so much earlier than people expect: you are buying coverage with today's health, and today's health is, on average, the best it will ever be again. Waiting is a bet that nothing changes. Sometimes you win that bet. When you lose it, you do not just pay an older-age rate, you pay a worse-health rate on top of it. If you want the deeper comparison of how policy structure affects this, our breakdown of term versus whole life insurance walks through how the rate lock works in each.

Life insurance by age: a decade-by-decade breakdown

In your 20s: cheapest rates, biggest insurability advantage

This is the cheapest and easiest decade to get covered, full stop. A healthy person in their 20s is exactly who insurers want, so rates are low and approval is fast. The catch is motivation: many twenty-somethings have no kids, no mortgage, and no obvious reason to think about death benefits.

So why consider it now? Three reasons. First, if you carry co-signed debt, such as private student loans a parent guaranteed, your death could leave that bill with them. Second, buying young lets you lock a low rate and protect your future insurability before any health surprise arrives. Third, the dollars are genuinely small at this age. If you are also thinking about the bigger financial picture in these years, the habits in our guide to money moves that build wealth in your 30s and 40s start paying off when you begin them in your 20s.

The honest counterpoint: if you are single, debt-free, and no one relies on you, it is reasonable to keep coverage small or wait. You do not need a large death benefit to protect an income nobody depends on yet.

In your 30s: the decade most families actually need it

This is when life insurance stops being optional for most people. The 30s tend to bring the trifecta: marriage, children, and a mortgage, often within a few years of each other. Now there is a household built partly on your income and a family that would feel its loss immediately.

This is the sweet spot for a substantial level term policy, often 20 or 30 years, sized to replace your income, pay off the mortgage, and cover the cost of raising children to adulthood. Rates are still very reasonable in your 30s, but they are higher than your 20s, and they climb faster from here. If you became a parent recently, the specific planning steps in our overview of life insurance for new parents will help you size the coverage to the actual job.

In your 40s: catch-up coverage during peak earnings

The 40s are often peak earning years, which means peak responsibility. Kids may be heading toward college, the mortgage balance is still meaningful, and your income is doing heavy lifting for the whole household. If you never bought coverage, this is the catch-up decade, and it is still very buyable, just not as cheap as it was.

Two things change in your 40s. Underwriting pays closer attention, because more people this age have a health condition to consider. And the cost of waiting becomes visible: the rate you skipped in your 30s is now noticeably higher. The move here is usually a level term policy matched to how many more years your family truly depends on your income, sometimes layered with a smaller permanent policy if there is a lasting need.

In your 50s: shorter horizons, sharper choices

By your 50s the planning question shifts from "replace decades of income" to "cover what is left." Maybe a remaining mortgage, a few years until the kids are fully launched, a spouse's retirement security, or final expenses so no one inherits a bill. Term is often still available and sensible, though the term lengths get shorter and the price reflects your age and health.

This is also the decade where permanent coverage gets a closer look, because some needs, such as leaving a legacy or covering final costs, do not expire. The trade-off is real: permanent insurance costs more per dollar of death benefit than term. Match the tool to the job rather than buying the most expensive option by default.

In your 60s and beyond: legacy, final expenses, and peace of mind

Plenty of people buy their first policy in their 60s, and it is not a mistake. The goals are usually different now: cover a funeral and final expenses so children are not handed the bill, leave something behind, or settle a specific debt. This is also the age when many adult children step in to arrange life insurance for elderly parents on their behalf. Term may still be available depending on health, but this is the natural home of final expense coverage and, for those with health conditions, guaranteed-issue policies that ask few or no medical questions in exchange for a smaller benefit and a waiting period. Coverage costs more here, but "more" is relative to a small, purpose-built benefit, and it can still be very affordable for what it does.

The cost of waiting: how price climbs by age

Exact premiums depend on your health, the coverage amount, the term length, your state, and the carrier, so no honest agent can promise you a specific number from an article. If you want a fuller picture, our breakdown of the average cost of life insurance by age and policy type shows the typical monthly numbers behind these factors. What does hold true is the shape of the curve. The table below shows the general pattern for a healthy non-smoker buying the same level term coverage, using illustrative figures to show direction, not a quote.

| Age at purchase | Relative monthly cost | What usually changes |

|---|---|---|

| Late 20s | Lowest | Best rates, fastest approval, top health classes within easy reach |

| Mid 30s | Noticeably higher | Still affordable, but the gap from your 20s is real |

| Mid 40s | Roughly double the late-20s level | Underwriting looks closer, more health factors appear |

| Mid 50s | Several times the late-20s level | Shorter terms, health class matters a lot |

| 60s and up | Highest, and options narrow | Final expense and guaranteed-issue become the common fit |

The pattern is clear and well documented across the industry. The point of the table is not the precise multiples, it is the direction: the line goes one way, and it does not come back down. According to research published by LIMRA, a large share of Americans say they own less life insurance than they know they need, and a common reason is the belief that it costs more than it does, a belief that, ironically, gets more accurate the longer they wait.

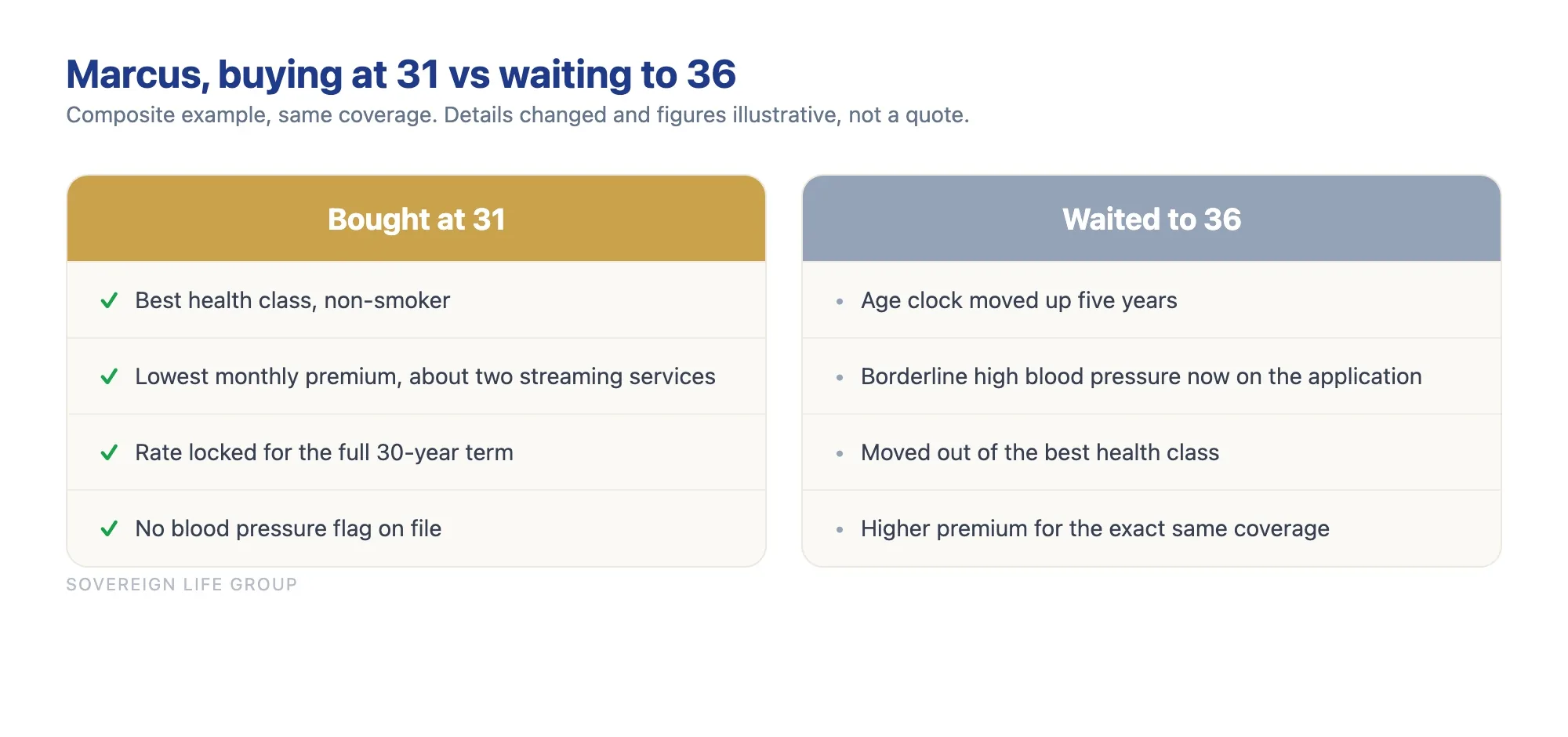

A real worked example: what waiting five years did to one family

Marcus and Renee came to me at 36, with two young kids and a fresh mortgage. Marcus had meant to "get around to" life insurance since they got married at 31. Back then, healthy and a non-smoker, a long level term policy large enough to cover the mortgage and replace years of his income would have cost them a modest amount each month, about the price of a couple of streaming services.

In the five years he waited, two things happened. He turned 36, so the age clock moved. And at a routine checkup he was flagged for borderline high blood pressure, now managed with a low-dose medication. Nothing dramatic, and he is in good shape. But on the application it moved him out of the very best health class. The result was a monthly premium meaningfully higher than the quote he would have qualified for at 31, for the exact same coverage. Over a 30-year term, that difference adds up to real money, the cost of a family vacation every year, give or take.

Here is the part that matters most, and it is not the dollars. Because his blood pressure is controlled and he is otherwise healthy, he still got covered at a fair rate, and his family is now protected. The waiting cost him money, not coverage. That is the usual outcome. But it is a coin flip he did not need to take. Had the checkup turned up something more serious, the story could have ended with a much higher rate, a different type of policy, or a benefit cap. The lesson Marcus repeats to his friends now: the rate you can get today is the best rate you will be offered, because tomorrow you are only older and your health is only less certain.

Get a fast, free estimate tailored to your age and health.

When to buy life insurance: the events that matter more than your birthday

Age sets the price, but life events set the need. For most people, the question of when to buy life insurance is answered by a life change rather than a number on a cake. These are the triggers that almost always mean it is time to get covered, or to add more:

- You get married or move in together. Now two financial lives are intertwined, and one income often helps carry shared costs.

- You have a baby or adopt. A child depends on your income for roughly two decades. This is the single most common reason families finally buy.

- You buy a home. A mortgage is a long obligation that does not pause if your income stops. This is the heart of mortgage protection coverage, keeping your family in the home rather than forcing a sale.

- You take on co-signed or business debt. Debt with a co-signer can land on someone you love. Business debt can land on a partner.

- You become the financial support for a parent or family member. If someone relies on the money you send, that reliance does not end if you do.

- You start a business with a partner. Key person and buy-sell needs arrive the day the business does.

- One spouse leaves the workforce. A stay-at-home parent provides care that would cost a fortune to replace, and that work deserves coverage too.

Notice that none of these are about being a particular age. They are about responsibility. When one of them happens, the best age to buy is whatever age you are when it happens, because the alternative is leaving the gap open.

Is it too late for life insurance? An honest answer for older buyers

This is the question I hear most from people in their 50s, 60s, and beyond, and it deserves a straight answer, because the fear of "too late" stops a lot of good coverage from ever being bought. So here it is: it is rarely too late. The word "best" in best age to buy life insurance does not mean "only." It means cheapest and easiest. Older does not mean uninsurable.

What actually changes as you get older is not whether you can get covered, but which doors are widest open:

- Term life is often still available well into the 60s for people in reasonable health, though term lengths shorten.

- Final expense whole life is purpose-built for older ages and modest benefit amounts, designed to cover a funeral and final bills, with simpler underwriting.

- Guaranteed-issue policies ask few or no health questions and cannot turn you down for health, in exchange for a smaller benefit and a waiting period before the full benefit applies. For those managing a diagnosis, our page on life insurance with health conditions explains how carriers actually look at common conditions.

So if you are older and have been putting this off because you assumed the answer was no, please hear this clearly: the answer is usually yes, and the cost only rises the longer you wait to ask. The honest trade-off is that you will pay more than a 30-year-old, and some options carry waiting periods. But protecting your family from a funeral bill, or leaving something behind, is very much still on the table. If you want to talk it through for your specific situation, you can always reach out and ask a real person rather than guess.

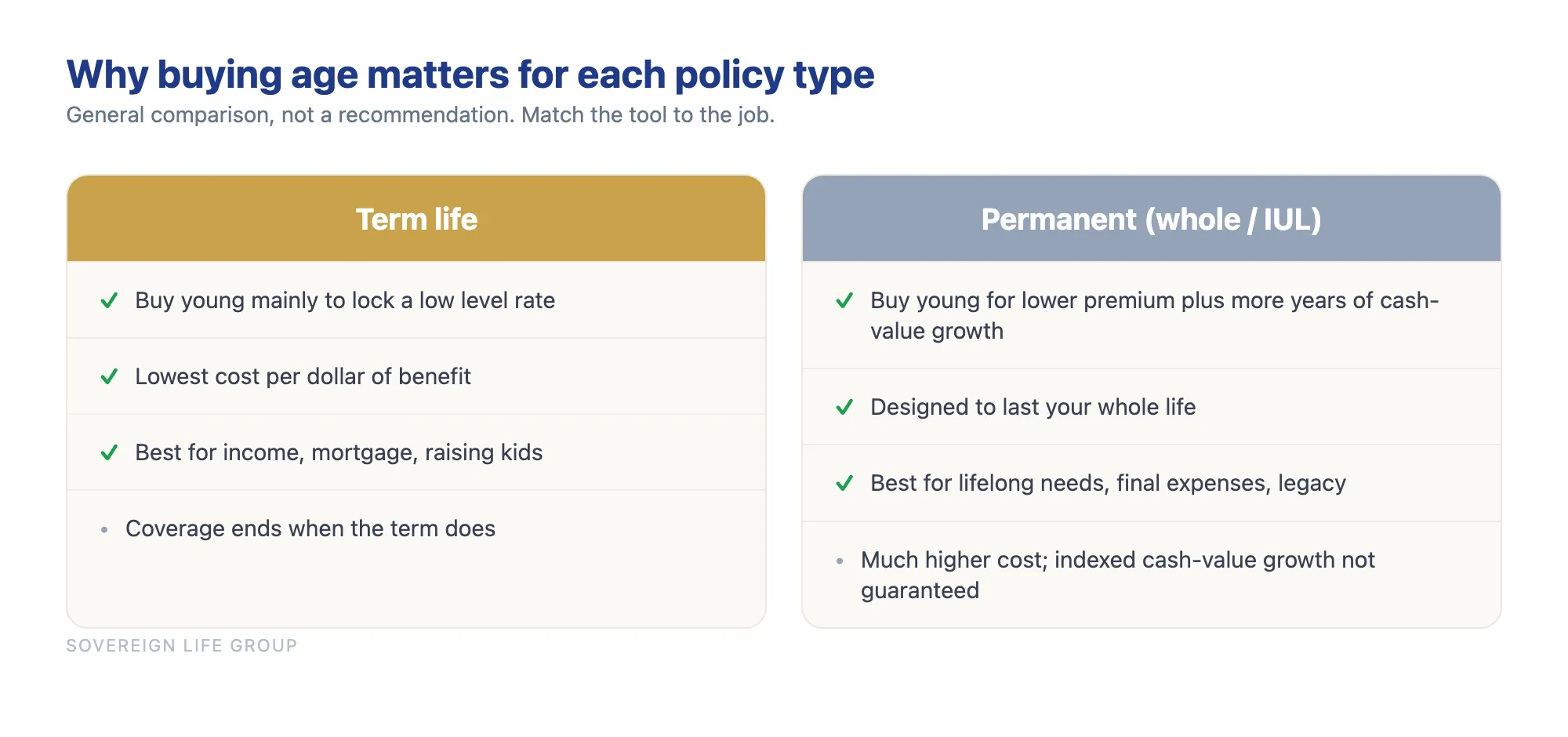

Does the best age change by policy type?

Term life insurance covers you for a set number of years, pays a death benefit if you pass during the term, and is the most affordable way to get a large benefit. For term, age and health at purchase set your locked rate, so buying earlier mostly saves you premium dollars.

Permanent insurance, such as whole life or an indexed universal life policy, is designed to last your whole life and can build cash value over time. For permanent coverage, buying earlier helps in two ways: the premium is lower at younger ages, and the cash value has more years to grow. That is why people exploring cash-value strategies often look at an indexed universal life policy earlier rather than later. The honest trade-off, and it is a real one, is that permanent insurance costs significantly more per dollar of death benefit than term, the returns on cash value are not guaranteed in indexed products, and fees and structure matter a great deal. Permanent coverage is not automatically better. It is better for specific jobs, like lifelong needs or estate goals, and worse as a way to get the most death benefit for the least money.

| Factor | Term life | Permanent (whole / IUL) |

|---|---|---|

| Main reason to buy young | Lock a low level rate | Lower premium plus more years for cash value to grow |

| Cost per dollar of benefit | Lowest | Much higher |

| How long it lasts | A set term of years | Designed to last your whole life |

| Best fit | Income replacement, mortgage, raising kids | Lifelong needs, final expenses, legacy, certain tax goals |

| Key trade-off | Coverage ends when the term does | Higher cost; cash value growth not guaranteed in indexed products |

When buying earlier is not the right move

An article that only says "buy now, buy young, buy more" is a sales pitch, not advice. So here are the honest cases where waiting, or buying less, is reasonable:

- No one depends on your income and you have no shared debt. If you are single, childless, debt-free, and no one would face a bill if you were gone, a large policy may be premature. A small policy to lock insurability can still make sense, but you do not need to over-insure.

- Your budget is genuinely stretched right now. Buying the right amount of term you can keep is better than buying an expensive permanent policy you cancel in two years. A canceled policy protects no one. Start with what you can sustain.

- You are being steered toward permanent coverage when term fits the job. If the need is "replace my income for the 20 years my kids are home," term usually does that for far less. Be cautious of anyone who only shows you the most expensive option.

- You already have enough coverage. If your existing policy plus savings already covers the mortgage, the income years, and final expenses, you may not need more. More is not always better.

The goal is the right coverage for your actual situation, not the biggest policy or the most expensive product. Sometimes the best move this year is a modest term policy and a plan to revisit it after the next life change.

How to lock in the right rate at the right age: a simple checklist

If you have decided it is time, here is the practical path. None of this requires you to become an insurance expert.

- Decide what the money is for. Replace income, pay off the mortgage, cover final expenses, fund the kids to adulthood, or some mix. The job determines the amount and the type.

- Size the benefit honestly. A common starting point is several years of income plus outstanding debts and future costs like education, minus what you already have saved or covered.

- Match the term to the need. If your kids are toddlers, a longer term covers them to independence. If your need ends when the mortgage does, match the term to the loan.

- Apply while your health is on your side. The application captures today's health, and today is, on average, your best health going forward. There are also no-exam options if a medical exam is what has been stopping you.

- Compare honestly, then act. Look at more than one carrier, understand the trade-offs, and then actually pull the trigger. The most expensive policy is the one you keep meaning to buy. If you want a clear, no-pressure look at your numbers, you can find a real human and not a robot at Sovereign Life Group, your life insurance strategist.

Not sure what your best age and best fit are?

Fifteen minutes. We will look at who depends on you, what you can comfortably afford, and the simplest way to lock in coverage before another year goes by. No pressure, no jargon, just a straight answer for your situation.

Get a Quote Book a 15-Min Call Prefer to start small? Save my card or get a quick term life quote.Frequently asked questions

What is the best age to buy life insurance?

For most people the best age to buy life insurance is your 20s or 30s, because premiums are lowest and approval is easiest while you are young and healthy. The truer answer is the day someone starts depending on your income. If that day already passed, the best age is the one you are today, because waiting only adds age and health risk to the price.

Is it too late to buy life insurance in my 50s or 60s?

It is rarely too late. Coverage costs more at older ages and some options narrow, but term life is often still available into the 60s for people in reasonable health, and final expense or guaranteed-issue policies are built specifically for older ages and common health conditions. The cost only rises the longer you wait to ask, so it is worth checking now.

Does life insurance get more expensive every year I wait?

Generally yes. Age and health are the two biggest factors in your rate, and both tend to move against you over time. Each birthday nudges the price up a little, and a new health condition can move you to a higher-cost health class. Locking a level term rate while you are younger and healthier usually costs less over the life of the policy.

Should I buy life insurance if I am single with no kids?

It can still make sense. If you carry co-signed debt, help support a parent, want to protect your future insurability, or want to lock a low rate before any health change, a small policy in your 20s is often inexpensive. If no one relies on you financially and you have no shared debt, it may be reasonable to keep coverage small or wait until your situation changes.

What is the best age to buy whole life or permanent insurance?

Earlier generally helps permanent policies more than term, because the premium is lower at younger ages and cash value has more years to grow. The honest trade-off is that permanent coverage costs much more than term for the same death benefit, and cash value growth is not guaranteed in indexed products. Match the policy type to the job you need it to do rather than buying the most expensive option by default.

How much does waiting five years actually cost?

It varies by person, but the pattern is consistent. A level term rate locked in your late 20s is often meaningfully lower than the same coverage bought in your mid 30s, and the gap widens each decade. A health change during those years can raise the cost further or limit which policies you qualify for. You do not avoid the premium by waiting, you defer it to an older, less certain version of yourself.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.