Average Cost of Life Insurance in 2026: A Plain Breakdown

The Short Version

The average cost of life insurance often gets quoted at around twenty-five to thirty dollars a month, but that figure describes a healthy forty-year-old buying a twenty-year term policy, not you. Your real price is built around your age, your health, the policy type, the coverage amount, and the carrier. Term life costs far less than whole life. The cheapest thing you can do is buy while you are young and healthy, because a level premium locks in at the rate you start with.

Most people overestimate what coverage costs, and then put off buying it for years over a number that was never real. So let us deal with the actual question head on. The average cost of life insurance in 2026 lands near twenty-five to thirty dollars a month for a common policy, but an average is a blurry photograph of millions of very different people. What matters is what it costs for someone like you, and that is a question with an honest, specific answer. This guide walks through what life insurance really costs by age, by policy type, and by coverage amount, what moves the price up or down, a full worked example, and the practical ways to pay less without gutting the protection your family depends on.

I write this as a licensed agent, not a marketer chasing a sale. You will find numbers here, but you will also find the part most pricing articles leave out: why the average can mislead you, and where the real savings actually live. No hype, no pressure, just the math laid out plainly.

What this guide covers

- What the average cost of life insurance really means

- Average cost of life insurance by age

- How much life insurance costs by policy type

- What different coverage amounts cost

- What actually drives your monthly premium

- A real worked example: the Brooks family

- Why the average can mislead you

- The hidden cost of waiting

- How to lower the cost honestly

- What you are actually paying for

- Frequently asked questions

What the average cost of life insurance really means

When you see a headline like "the average cost of life insurance is about twenty-six dollars a month," it is describing one very specific buyer: a healthy, nonsmoking forty-year-old purchasing a twenty-year term policy with five hundred thousand dollars of coverage. That profile gets used because it is roughly the most common term policy sold in the United States, so it makes a tidy reference point. It is not a price tag for the rest of us.

Think of it the way you would think about the average price of a car. The "average" blends a compact sedan and a loaded pickup, a teenager's first car and a retiree's luxury coupe. Nobody actually pays the average, because nobody buys the average car. Life insurance works the same way. So when people ask how much does life insurance cost, the most useful answer is a range tied to real variables, not a single number.

Here are the four things that move your premium the most, and we will take each one in turn:

- Your age. Younger almost always means cheaper, and the gap widens fast after about age fifty.

- Your health. Health class and tobacco use can swing the price more than almost anything else.

- The policy type. Term life is the affordable workhorse. Whole life and other permanent policies cost much more because they do much more.

- The coverage amount and term length. A bigger death benefit over more years costs more, in a fairly predictable way.

Get those four straight and you can estimate your own ballpark within minutes, which beats memorizing somebody else's average. If you are still deciding how big a policy you actually need before you price it, our walkthrough on how much life insurance you need is the right place to start, because the coverage amount drives the cost as much as anything on this page.

No medical exam for a ballpark. Free, and no pressure.

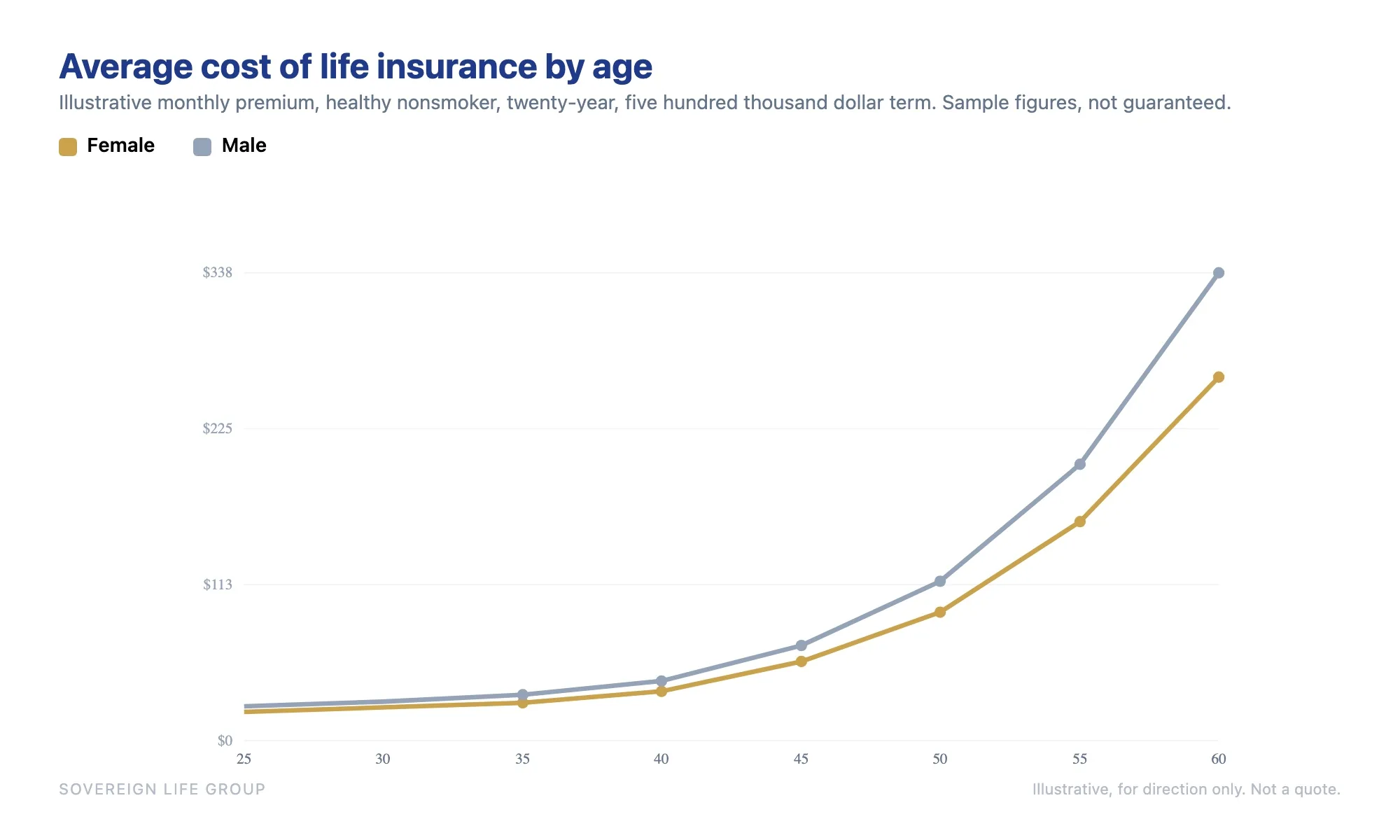

Average cost of life insurance by age

Age is the cleanest predictor of price, because life insurance is fundamentally a bet on longevity. Each year you age, the statistical chance of a claim ticks up, and the premium follows. The pattern is gentle through your twenties and thirties, then it steepens. This is why looking at life insurance rates by age is the single most useful exercise before you shop.

The table below shows illustrative monthly premiums for a healthy nonsmoker buying a twenty-year, five hundred thousand dollar level term policy. Treat these as direction and rough scale, not a quote. Actual pricing varies by carrier, health class, and state, and any policy is subject to underwriting approval.

| Age at purchase | Female (approx. monthly) | Male (approx. monthly) |

|---|---|---|

| 25 | $18 to $24 | $22 to $28 |

| 30 | $20 to $27 | $24 to $32 |

| 35 | $23 to $31 | $28 to $38 |

| 40 | $30 to $42 | $36 to $50 |

| 45 | $48 to $66 | $58 to $80 |

| 50 | $78 to $108 | $95 to $135 |

| 55 | $130 to $185 | $165 to $235 |

| 60 | $215 to $310 | $275 to $400 |

Two things jump out of that table. First, the jump between your thirties and your forties is meaningful, and the jump from your forties into your fifties is steep. A policy that felt like a rounding error at thirty-five can cost several times more at fifty-five. Second, men generally pay more than women at the same age, because women on average live longer, so the insurer expects to collect premiums for more years before any claim.

Why the climb accelerates with age

The reason the curve bends upward is not arbitrary. Mortality risk does not rise in a straight line. It rises slowly for decades and then more quickly, and the pricing mirrors that curve. The practical takeaway is simple: the cheapest version of your policy almost always exists today, not next year. A level term policy fixes your monthly premium for the whole term, so the age you lock it in at is the age you keep paying for, even as you grow older.

What about seniors?

Coverage does not disappear later in life, but the math changes. After about age sixty, large term policies get expensive, and many older buyers shift toward smaller, purpose-built coverage such as final expense or a modest whole life policy meant to cover a funeral and clear small debts rather than replace decades of income. If you are shopping later in life, the question moves from "replace my paycheck" to "do not leave a bill behind," and the pricing is sized to that smaller, focused job.

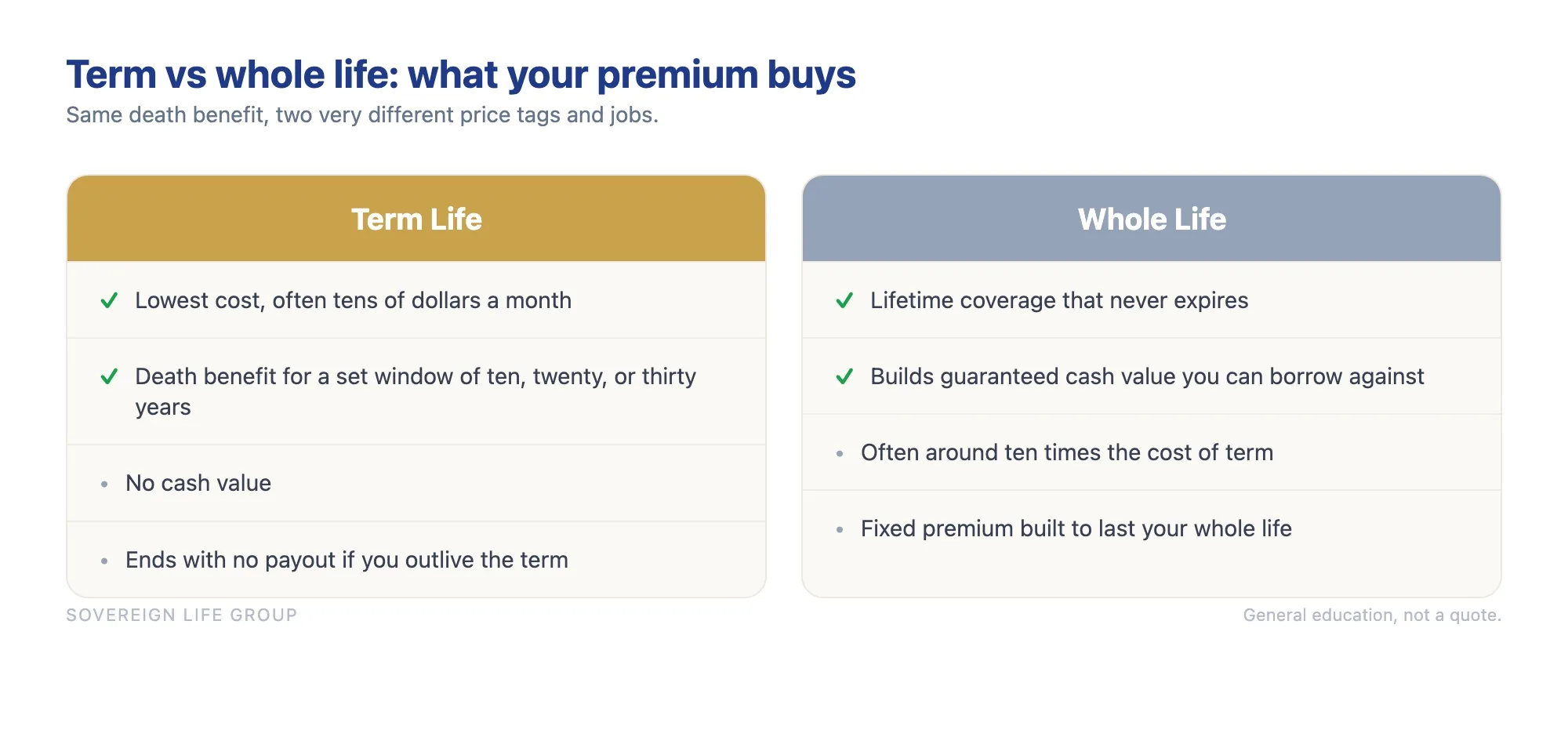

How much life insurance costs by policy type

This is where the biggest price differences hide, and where a lot of confusion starts. Two policies with the same death benefit can cost wildly different amounts because they are built to do different things. Comparing the price of term to the price of whole life without understanding why is like comparing the cost of renting an apartment to buying a house and concluding that renting is simply better. The numbers are not measuring the same thing.

Term life insurance

Term life is pure protection for a set number of years, usually ten, twenty, or thirty. If you pass away during the term, it pays the death benefit. If you outlive the term, it ends with no payout, the same way your auto insurance does not refund you for the years you did not crash. Because the insurer is only on the hook for a defined window and there is no savings component, term is dramatically cheaper. For most working families protecting income and a mortgage, term is the workhorse, and it is what makes the famous low averages possible.

Whole life insurance

Whole life is permanent. It is designed to last your entire life, the premium is generally fixed, and it builds cash value you can borrow against over time. All of that costs money, so whole life typically runs many times the price of term for the same death benefit. That does not make it a bad deal. It makes it a different tool, suited to lifelong needs such as final expenses, estate planning, or leaving a guaranteed legacy. If you are weighing the two, our deeper comparison of term versus whole life insurance breaks down which job each one is actually built for.

Universal and indexed universal life

Universal life and indexed universal life are also permanent, but with more flexibility in how premiums and cash value work. They generally cost less per month than traditional whole life and more than term, and they carry more moving parts, including fees and crediting features that deserve careful reading. They are powerful in the right situation and oversold in the wrong one, so the trade-offs matter more here than with a simple term policy.

| Policy type | Roughly what it costs | What you get for it |

|---|---|---|

| 20-year term | Lowest, often tens of dollars a month | A death benefit for a set window, no cash value |

| 30-year term | Modestly higher than 20-year | Same idea, longer protection window |

| Universal / indexed universal | Several times the cost of term | Lifetime coverage plus flexible cash value, more complexity and fees |

| Whole life | Highest, often around ten times term or more | Lifetime coverage, fixed premium, guaranteed cash value growth |

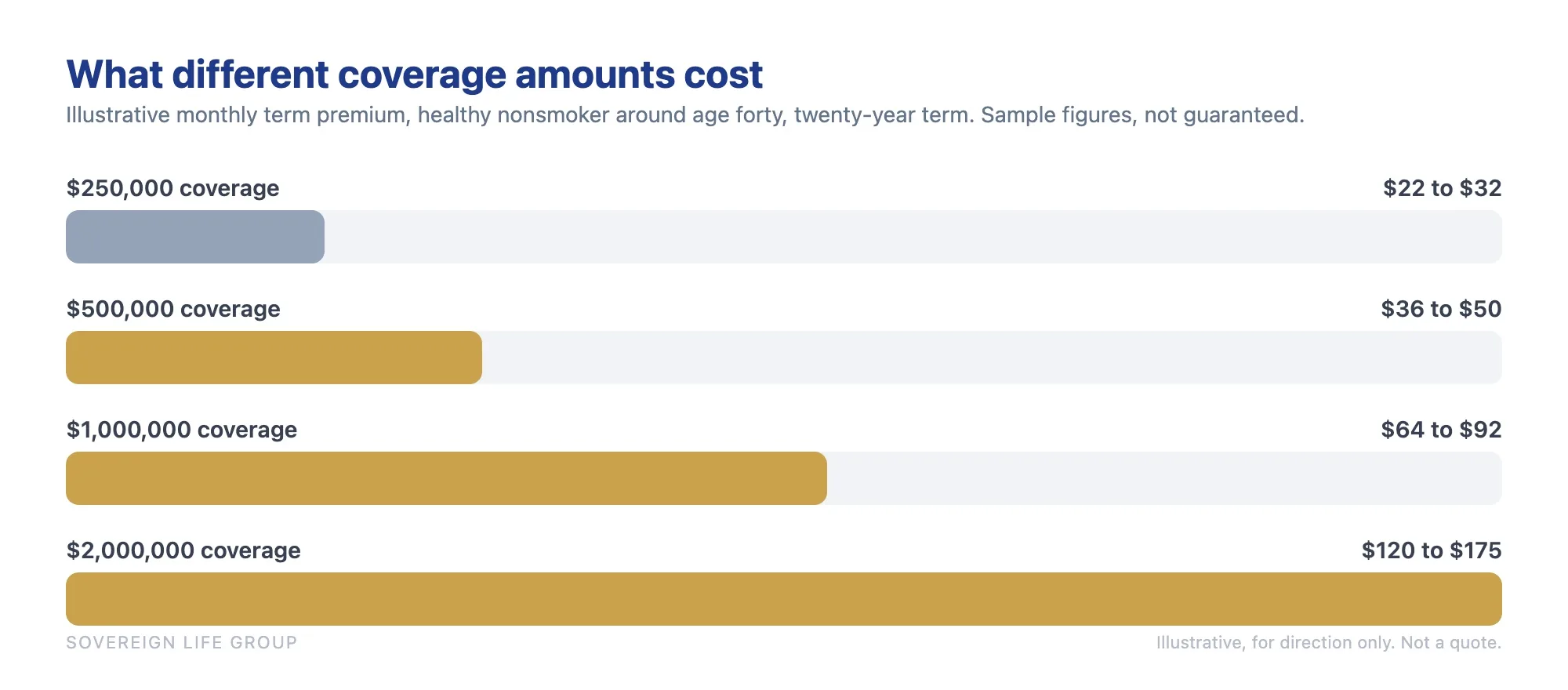

What different coverage amounts cost

The death benefit, meaning how much your family receives, is the other big lever. More coverage costs more, though not always in a perfectly straight line, because carriers sometimes price larger policies a little more efficiently per dollar. The table below shows illustrative term pricing for a healthy person in their late thirties to early forties across common coverage amounts, so you can see how the monthly premium scales with the size of the benefit.

| Coverage amount | Approx. monthly (female) | Approx. monthly (male) |

|---|---|---|

| $250,000 | $18 to $26 | $22 to $32 |

| $500,000 | $30 to $42 | $36 to $50 |

| $1,000,000 | $52 to $74 | $64 to $92 |

| $2,000,000 | $98 to $140 | $120 to $175 |

Notice that doubling the coverage rarely doubles the price. Going from five hundred thousand to one million does not usually cost twice as much, which is why right-sizing the benefit to your real need is smarter than reflexively buying the smallest policy. A common rule of thumb is ten to fifteen times your annual income, plus your mortgage and any other debts, minus what you have saved. That is a starting point, not gospel, and the right figure depends on your household. The point here is that a larger, more useful policy often costs less per dollar of protection than people assume. That per-dollar math is the same when a company buys coverage on a key employee, which is why our look at how much key man insurance costs lands on similar ranges.

If protecting the family budget on a single income is the worry that keeps you up, the family coverage page lays out how a sensibly sized policy fits a real household without straining the monthly numbers.

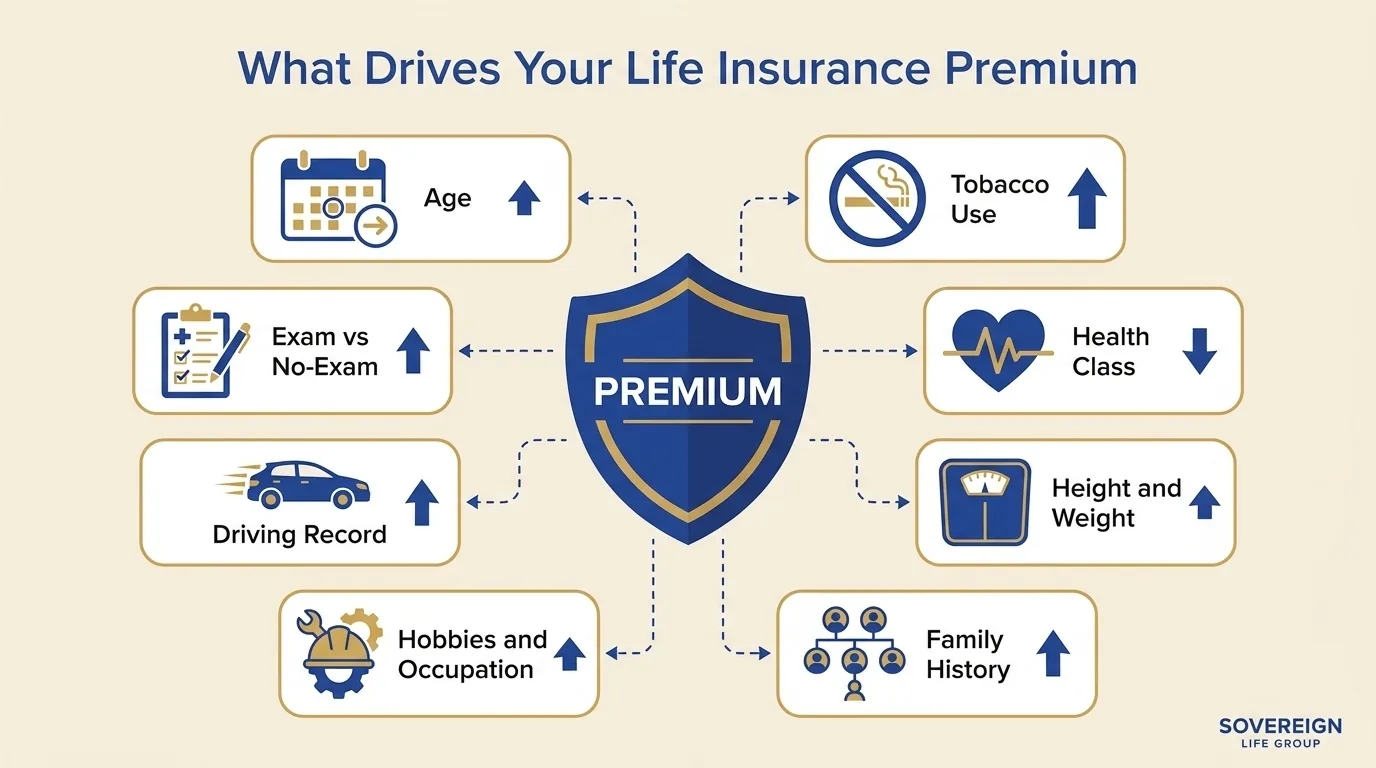

What actually drives your monthly premium

Beyond age, type, and amount, a handful of personal factors decide where your quote lands. None of these are mysterious, and knowing them helps you see why two neighbors the same age can pay very different prices. Here is what underwriters actually weigh, and which direction each one pushes the cost.

| Factor | Effect on price | Why it matters |

|---|---|---|

| Age | Older costs more | Mortality risk rises each year, and the premium follows |

| Tobacco or nicotine use | Often two to three times more | Underwriting treats nicotine as a major health risk |

| Health class | Better health, lower price | The gap between top and standard classes can be large |

| Height and weight | Can raise the price | Build affects the risk profile carriers price for |

| Family medical history | Can raise the price | Certain hereditary conditions factor into the rate |

| Hobbies and occupation | High-risk ones cost more | Skydiving, aviation, and hazardous jobs add risk |

| Driving record | Recent issues can raise it | A serious record signals elevated risk |

| Exam vs no-exam | No-exam often costs more | Skipping the exam shifts risk to the insurer, who prices for it |

Health class, in plain English

Carriers sort applicants into health classes after underwriting, with names like preferred plus, preferred, standard plus, and standard, plus separate smoker categories. The difference between the top and the middle is not small. The same forty-year-old on the same policy can pay close to double depending on which class the underwriting assigns. Blood pressure, cholesterol, build, and history all feed into it. This is also why an honest application matters, because the contestability period in the first two years lets an insurer review a claim for misstatements.

The exam question

Skipping the medical exam is convenient, and for some people with a complicated health history it is the difference between getting covered and not. But convenience is rarely free. If you are healthy and willing to do a brief exam, a fully underwritten policy often comes in lower than a no-exam alternative, and our breakdown of no-exam versus traditional life insurance weighs that cost trade-off in detail. If the needle is the thing that has stopped you for years, a no-exam policy you actually buy beats a perfect policy you keep putting off. People managing a specific diagnosis can still find good options, and our overview of life insurance with health conditions covers how carriers tend to view common ones.

Get a fast, free estimate tailored to your age and health.

A real worked example: the Brooks family

Averages are abstract, so let us make this concrete with a realistic household. Meet the Brooks family. Marcus is thirty-eight, a nonsmoker in good health, earning about eighty thousand dollars a year. His wife Dana is thirty-six and works part time. They have two kids, a fifteen-year mortgage balance of around two hundred forty thousand dollars, and roughly thirty thousand dollars in savings. They want to make sure that if something happened to Marcus, Dana could pay off the house, keep the kids steady, and not face a fire sale on top of a funeral.

Step one: size the need

They start with the obligation. The mortgage is two hundred forty thousand. Replacing roughly ten years of Marcus's income adds another eight hundred thousand. A cushion for childcare, college help, and final expenses adds another hundred thousand. That totals about one million one hundred forty thousand. They subtract their thirty thousand in savings and round to a clean one million dollar target. That is the death benefit they will price.

Step two: choose the structure

Because the need is temporary, it lasts until the mortgage is gone and the kids are grown, term life fits better than permanent coverage. They look at a twenty-year term, which carries them until the youngest is well into adulthood and the house is paid off. A thirty-year term would cost more for years of protection they would not really need, so twenty is the smarter match.

Step three: price it

For a healthy thirty-eight-year-old nonsmoker, a one million dollar, twenty-year term policy plausibly lands somewhere in the range of fifty to seventy dollars a month, depending on the carrier and the final health class. That is real money, but it is also roughly the cost of a phone plan to protect a million dollars of his family's future. Marcus could trim it by dropping to seven hundred fifty thousand of coverage, or stretch it by adding a rider, but the core policy does the main job affordably.

If you want to run your own version of this math before talking to anyone, our guide on calculating how much coverage your family needs walks through the same steps the Brooks family used, so you arrive at a number you can actually price.

Why the average can mislead you

Here is the section most pricing articles skip, because it complicates the neat headline. The "average cost of life insurance" is a genuinely useful sanity check and a genuinely misleading shopping target, at the same time. Understanding why protects you from two opposite mistakes: overpaying because you assumed it would be expensive, and underbuying because you anchored to a low average that does not apply to you.

An average flattens enormous variety into one figure. It blends the twenty-five-year-old marathon runner with the fifty-eight-year-old smoker, the small final expense policy with the two million dollar term plan, the simple term product with the cash value permanent one. The result is a number that describes almost nobody. A few specific traps to watch for:

- Averages skew young and healthy. Many published averages quote the best health class, which only some applicants qualify for. If your underwriting lands at standard, your real price can be meaningfully higher than the cheerful headline.

- Averages usually mean term. The low numbers you see almost always describe term life. If you are looking at whole life or universal life, multiply your expectations several times over.

- Averages ignore your coverage gap. A low monthly cost on a small policy is not a bargain if it leaves your family short. Cheap and insufficient is still insufficient.

- Averages hide the smoker penalty. Nicotine use can two or three times the premium, so a blended average wildly understates the cost for a smoker and slightly overstates it for a nonsmoker.

According to research published by LIMRA, a large share of Americans overestimate the price of coverage, sometimes by a factor of three, and that misperception is one of the most common reasons people delay buying. The fix is not a better average. It is a real quote built around real you. The neutral consumer resources at the Insurance Information Institute are a good, sales-free place to read more before you talk to anyone.

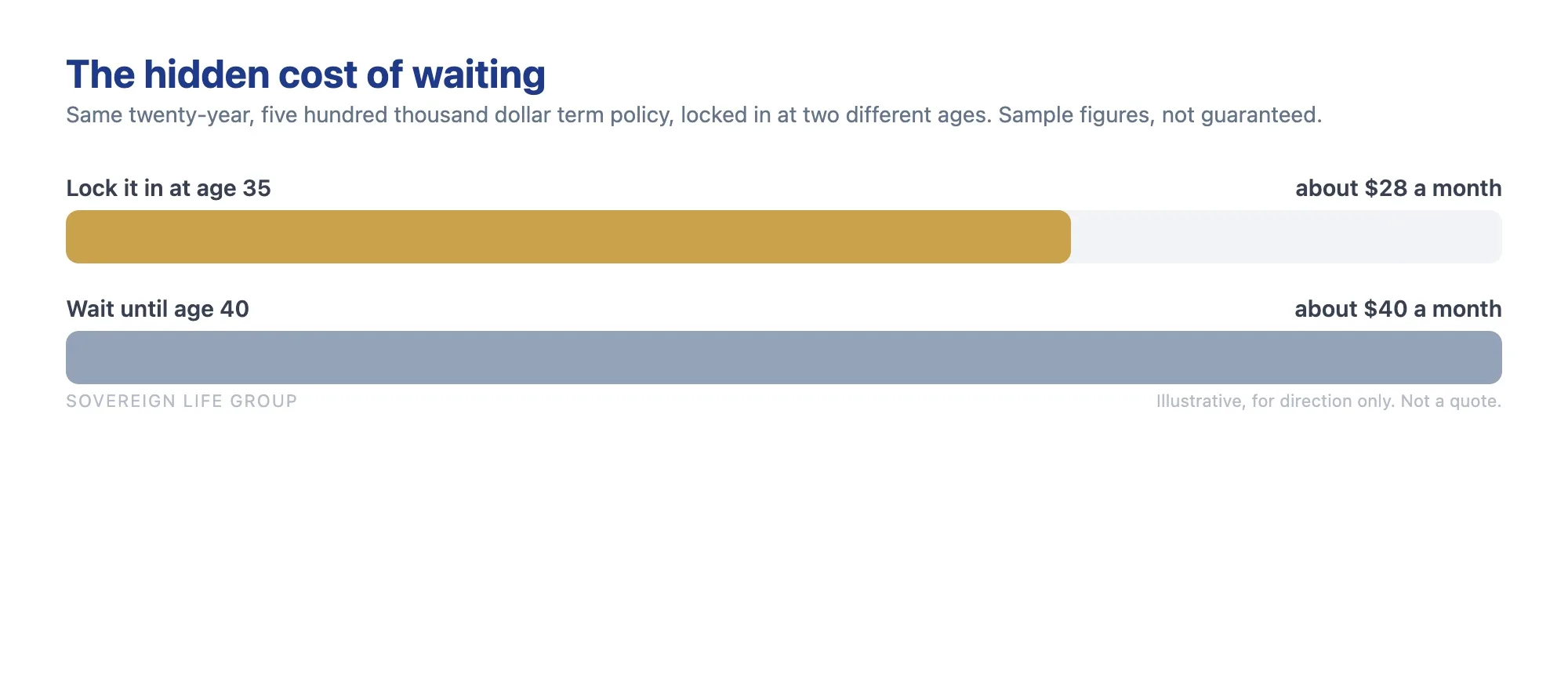

The hidden cost of waiting

If there is one number that should change your behavior, it is not the average premium. It is the cost of waiting. Because a level term premium locks in at the age and health you buy at, every year you delay is a year of compounding price increases you will pay for the entire life of the policy. This is the part of the math that quietly costs families the most.

Walk through a simple version. Suppose a healthy person could lock in a twenty-year, five hundred thousand dollar term policy for about twenty-eight dollars a month at thirty-five. Wait until forty and a comparable policy might cost about forty dollars a month. That is twelve dollars more, every month, for twenty years, which is roughly two thousand eight hundred dollars in extra premium over the life of the policy, for the exact same coverage. Wait until forty-five and the gap widens sharply, because that is where the age curve steepens.

And that assumes your health stays exactly the same, which is the optimistic case. Health rarely improves quietly while you wait. Blood pressure drifts up, a routine physical flags cholesterol, a diagnosis enters the picture, and any of those can move you into a higher-priced class or change which policies are available at all. So the true cost of waiting is two costs stacked together: the age increase you can predict, and the health risk you cannot.

This is also why young, healthy people sometimes get talked out of acting, on the logic that "I have time." You do have time. You also have the lowest price you will ever see, and it does not come back.

How to lower the cost honestly

Lowering your premium does not have to mean buying less protection. Most of the real savings come from buying smart, not buying skimpy. Here is the practical path, in the order I would walk a friend through it.

- Buy sooner. We just covered why. The single biggest lever for most people is simply their age at purchase, and that lever only gets heavier with time.

- Match the term to the actual need. If your need lasts twenty years, do not pay for thirty. Aligning the term length to when your family stops depending on the coverage trims cost with no downside.

- Choose term unless you truly need permanent. If the job is replacing income and covering a mortgage for a defined period, term does it for a fraction of the price. Save permanent coverage for genuinely lifelong needs.

- Right-size the benefit. Bigger is not automatically better, and neither is smallest. Buy the amount your family would actually need, since a larger policy often costs less per dollar than people expect.

- Quit tobacco well before you apply. Carriers generally want you nicotine-free for a stretch, often a year or more, before non-smoker rates apply. Quitting early can move you out of the most expensive category entirely.

- Pay annually if you can. Many carriers add a small surcharge for monthly billing. Paying once a year can shave a few percent off the total.

- Improve what you can before underwriting. If a physical is coming, simple things like managing blood pressure or weight in the months before can influence your health class.

- Compare more than one carrier. This is the quiet one. Carriers underwrite the same person differently, so the same profile can be priced as preferred at one company and standard at another. Shopping multiple carriers is often where the real savings hide, and it is exactly what an independent agent does for you, which is a big part of why buying life insurance online versus using an agent changes what you ultimately pay.

That last point is the difference between a captive agent who sells one company's products and an independent strategist who shops the field on your behalf. The goal is to find the carrier that views your specific profile most favorably, which is not something you can do from a single quote box. When you want that done for you, a clear look at your numbers with Sovereign Life Group, your life insurance strategist costs nothing and carries no pressure.

What you are actually paying for

It is worth stepping back from the numbers for a moment, because life insurance is the rare purchase where the cost and the value live in completely different worlds. The cost is a small, predictable monthly premium. The value is a large, unpredictable safety net that exists for the worst day your family might face. Judging the price without the value is how people talked themselves out of coverage they later wished they had.

Consider what the premium buys for the Brooks family from our example. For something in the neighborhood of a streaming bundle each month, Dana would not have to sell the house, pull the kids out of their schools, or return to full-time work during the hardest season of her life. The mortgage would be gone. There would be breathing room instead of a financial emergency stacked on top of a personal one. That is what the monthly premium is really for, and it is why "is it worth it" is almost always the wrong question. The better question is whether the amount and structure fit your family.

So when you compare the average cost of life insurance against your own situation, hold both numbers in view. The premium is what you pay. The death benefit is what you are buying. For most families with people depending on their income, the trade is not close. The honest work is not deciding whether to protect your family. It is choosing the right tool, sized correctly, at the best price your health and timing allow.

Want your real number, not an average?

Fifteen minutes. We will look at your age, your health, your budget, and the coverage your family actually needs, then shop multiple carriers to find the right fit. No pressure, no jargon, just your options laid out plainly.

Get a Quote Book a 15-Min Call Prefer to move quickly? You can save my card and get a quick term life quote in a couple of minutes.Frequently asked questions

What is the average cost of life insurance per month?

Industry data often points to roughly twenty-five to thirty dollars a month, based on a healthy forty-year-old buying a twenty-year term policy with five hundred thousand dollars of coverage. That number is only a reference point. A young, healthy nonsmoker can pay far less, while an older applicant, a smoker, or someone choosing whole life can pay several times more. Your monthly premium is built around your own age, health, and the policy you choose.

How much does life insurance cost by age?

Term life premiums rise slowly from your twenties into your forties, then climb more steeply after that, because the statistical risk of a claim grows with each year. A healthy person in their thirties often pays a fraction of what the same coverage costs in their fifties. The exact figure depends on the carrier, your health class, the coverage amount, and the term length, and any policy is subject to underwriting approval.

Why is whole life insurance so much more expensive than term?

Whole life is built to last your entire lifetime and includes a cash value component, so the premium covers far more than a temporary death benefit. Term life only has to cover a set number of years and has no cash value, which is why it usually costs much less for the same death benefit. Neither is automatically better. The right choice depends on what job you need the policy to do and for how long.

Does my health really change the price that much?

Yes. Health is one of the largest single drivers of cost. The gap between a top health class and a standard class on the same policy can be substantial, and tobacco use alone often two to three times the premium. This is also why locking in coverage while you are healthy tends to mean a lower rate for the life of the policy, since a level term premium is set at application and does not rise as you age.

Can I lower the cost of life insurance without losing coverage?

Often yes. Buying sooner while you are younger and healthier, choosing term over permanent coverage if lifetime coverage is not the goal, matching the term length to the actual need, quitting tobacco well before you apply, and comparing more than one carrier can all lower the premium without cutting the death benefit. A licensed agent who shops multiple carriers can show you where the savings actually are for your situation.

Is the average cost a good guide for what I will pay?

Use it as a sanity check, not a quote. An average blends young and old, healthy and unhealthy, smokers and nonsmokers, term and permanent, so almost nobody pays exactly the average. The honest way to know your number is to get quotes built around your real age, health, coverage amount, and policy type. Any figure quoted before an application is an estimate, and final pricing is subject to underwriting approval.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. The figures in this article are general illustrations for direction only, not quotes, and actual rates vary by state, age, health, and carrier, with any coverage subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.