No-Exam vs Traditional Life Insurance: Which to Choose

The Short Version

No-exam life insurance skips the physical and pays out just as reliably, but the insurer prices in the missing health data, so a healthy person often pays a bit more and can buy a little less. Traditional, fully underwritten coverage takes weeks and involves an exam, and in return it unlocks the highest coverage amounts and the lowest rates for healthy applicants. Choose no-exam for speed, simplicity, or a health history that makes an exam risky. Choose traditional when you are healthy, want a large benefit, and can wait a few weeks for the best price.

If you have been putting off life insurance because you dread the needle and the paperwork, here is the good news: the choice today is no longer buy or skip it. The real choice is no exam vs traditional life insurance, and both are legitimate ways to leave your family protected. One trades a little money for speed and convenience. The other asks for a few weeks and a short exam and rewards you with the sharpest price and the highest coverage. Neither is a trick, and neither is automatically the right answer for you.

I write this as a licensed agent who places both kinds of policies every week, not as a marketer with one product to push. My job in this guide is simple: show you exactly how these two paths differ on cost, speed, coverage, and approval, walk you through a real worked example, and help you land on the option that fits your life instead of the one that pays the biggest commission. Let us make this decision clear.

What this guide covers

- What each type actually means

- No exam vs traditional life insurance at a glance

- The four ways a policy gets underwritten

- What each one costs and why

- How fast you can actually get covered

- How much coverage you can buy

- When to choose no-exam life insurance

- When to choose traditional life insurance

- A real worked example: two neighbors, two paths

- Myths that push people to the wrong choice

- How to decide without overpaying

- Frequently asked questions

What each type actually means

No-exam life insurance is a policy issued without a paramedical exam, meaning no nurse visit, no blood draw, and no urine sample. Traditional, or fully underwritten, life insurance is the classic version that includes that brief exam plus a detailed health review. Both are real coverage from licensed carriers. The difference is how the insurer gathers information about your health and how it prices the risk.

That distinction sounds small, but it drives everything else in this comparison: the price you pay, how much coverage the carrier will issue, how long approval takes, and how likely a health condition is to trip you up. Before we compare them head to head, it helps to define both plainly, because the labels get thrown around loosely and the marketing muddies them on purpose.

No-exam life insurance, in plain English

No-exam simply means the carrier decides whether to insure you without sending you for a physical. Instead of lab work, it leans on data it can pull quickly: your answers to health questions, your prescription history, motor vehicle records, and databases the insurance industry shares. Some no-exam policies still ask a lot of health questions. A few ask almost none. The label tells you what is missing, the exam, but it does not tell you how much health screening still happens behind the scenes. That is why two no-exam policies can look identical on the surface and price very differently.

Traditional life insurance, in plain English

Traditional life insurance is fully underwritten. You complete a detailed application, then a paramedical professional measures your height, weight, and blood pressure and collects blood and urine. The carrier reviews those results along with your medical records, prescription history, and sometimes an interview. With that full picture, it can sort you into precise health classes, from preferred plus down to substandard, and price you accordingly. More information for the insurer usually means a better deal for a healthy applicant, because there is less unknown risk to charge for.

No exam vs traditional life insurance at a glance

The core trade-off in no exam vs traditional life insurance is convenience against cost and coverage. No-exam wins on speed and simplicity and is often the only realistic path for certain health histories. Traditional wins on price for healthy applicants and on the size of the benefit you can buy. Everything below is a variation on that theme.

Here is the head-to-head, so you can see the whole picture before we dig into each row.

| Factor | No-exam life insurance | Traditional (fully underwritten) |

|---|---|---|

| Medical exam | None | Yes, blood and urine |

| Health questions | Few to many, varies by type | Detailed application and records |

| Approval speed | Minutes to a few days | Roughly 3 to 8 weeks |

| Price for a healthy person | Often somewhat higher | Usually the lowest available |

| Maximum coverage | Commonly capped lower | Very high, into the millions |

| Best health classes | Limited | Preferred plus and preferred available |

| Good fit for | Speed, convenience, some health histories | Healthy buyers wanting max coverage and price |

Notice that no single column wins every row. That is the honest heart of this decision. If one option were better in every way, this article would be one sentence long. Instead, the right answer swings on what you value most and on the specifics of your health and budget. Let us take the drivers one at a time.

The four ways a policy gets underwritten

Underwriting is just how a carrier decides whether to insure you and at what price. There are four main levels, and understanding them clears up most of the confusion in the no exam vs traditional debate. Fully underwritten sits at one end with an exam and the best pricing. Then come accelerated, simplified issue, and guaranteed issue, each asking for less information and, in return, offering less coverage or a higher price.

Most people picture only two options, exam or no exam. In reality it is a spectrum, and knowing where a policy sits on that spectrum tells you almost everything about its price and its limits. This is also where the phrase simplified issue vs fully underwritten life insurance comes from, and it is worth getting straight.

Fully underwritten (traditional)

This is the deepest review. You answer a long application, take the exam, and the carrier pulls your records. Because it knows the most about your health, it can offer the sharpest rates to healthy people and the largest benefits, often into the millions. The cost is time. Approval commonly runs a few weeks and occasionally longer if medical records are slow to arrive. If you are healthy and patient, this path usually delivers the most coverage per dollar.

Accelerated underwriting (no-exam, but thorough)

Accelerated underwriting is the modern middle ground and the reason no-exam has gone mainstream. You answer a detailed application, and instead of ordering an exam, the carrier runs your data through algorithms that check prescription history, motor vehicle records, and shared industry databases. Healthy applicants who fit the model can be approved in minutes to days with coverage that reaches into the hundreds of thousands or more. If the model flags something, the carrier may still ask for an exam. This is the sweet spot for a healthy person who wants speed without giving up much price. To go deeper on how this path works end to end, read our full no-exam life insurance guide.

Simplified issue

Simplified issue skips the exam and relies on a short health questionnaire, often 10 to 30 yes or no questions about your medical history. Approval is fast, frequently within a day or a few days. The trade-offs are real: coverage amounts are usually lower, commonly in the tens of thousands up to a few hundred thousand depending on the carrier, and prices run higher because the insurer is accepting more unknown risk. Simplified issue is a strong fit when a full exam would likely produce a decline or a steep rating, or when you simply want coverage in force quickly.

Guaranteed issue

Guaranteed issue asks no health questions and cannot turn you down for health, which is its whole appeal. In exchange, benefit amounts are small, usually a few thousand up to around 25,000 or 50,000 dollars, premiums are the highest per dollar of coverage, and there is almost always a graded or waiting period, meaning the full benefit does not apply for the first two or three years unless death is accidental. This is a last-resort tool for people who cannot qualify elsewhere, and it is most often used for final expense coverage to handle burial and end-of-life costs. It is not a substitute for real income protection.

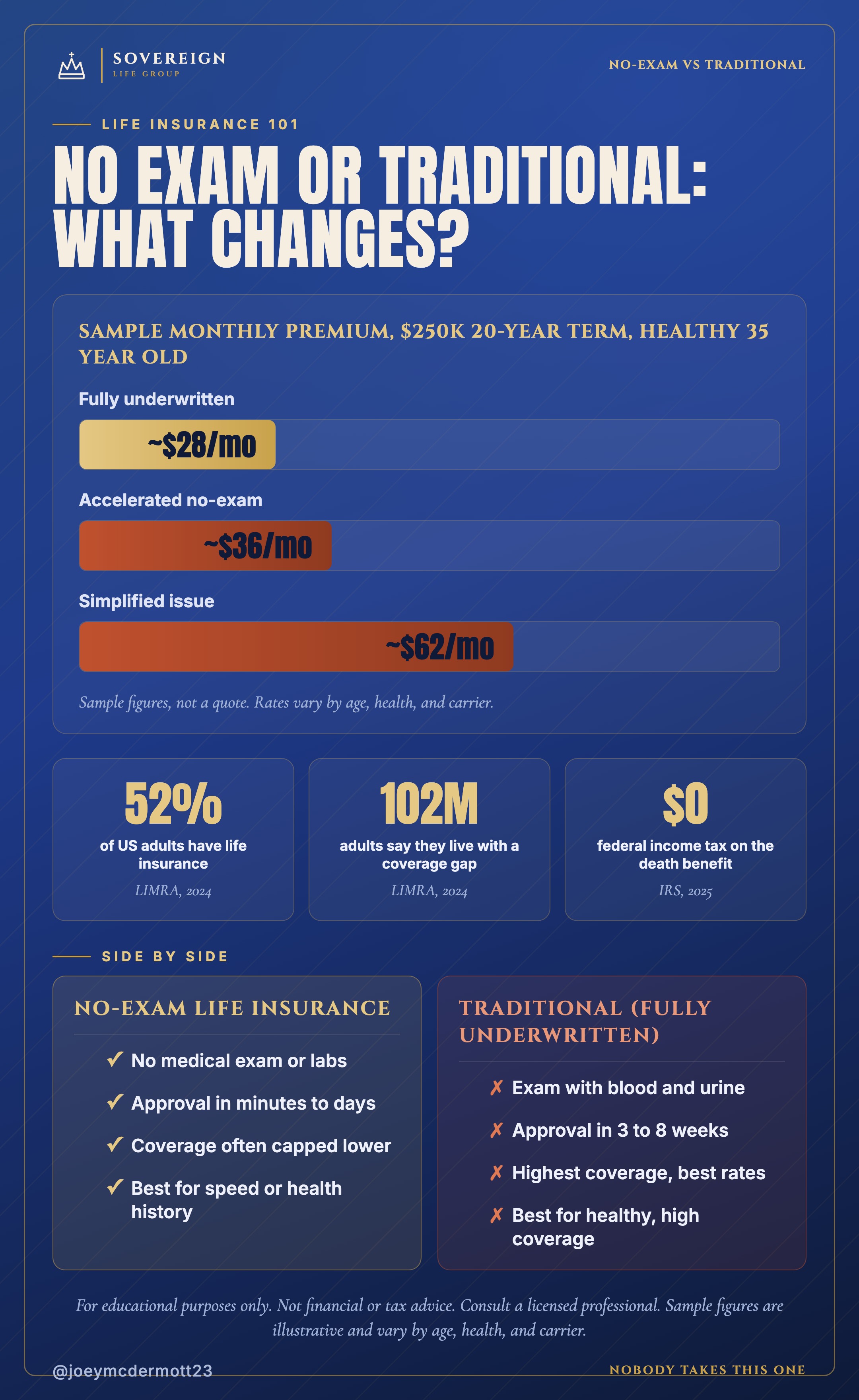

What each one costs and why

Traditional life insurance is usually cheaper for a healthy person, and no-exam usually costs somewhat more for the same profile. The reason is information. When a carrier cannot see your lab work, it prices in the risk of what it cannot see, so it charges a cushion. Industry pricing for simplified issue can run meaningfully higher than a comparable fully underwritten policy for the same person.

That said, the gap is not always dramatic, and for a young, healthy applicant buying a modest amount it can be small. The honest answer to what it costs is that it depends on your age, health, the amount of coverage, and which carrier's model you fit best. No responsible agent can quote you a flat rate from an article, and you should be wary of anyone who does before they know your details.

Why no-exam carries a premium

Think of it from the insurer's side. With a fully underwritten applicant, the carrier has blood work, a blood pressure reading, and a full records review. It can confidently place a healthy 35 year old in a top health class and price them low. With a no-exam applicant, it is working with less certainty, so it assumes a somewhat worse-than-average risk to protect itself. You are essentially paying a small convenience premium for skipping the exam and getting covered faster. For some people that convenience is easily worth it. For others, especially the very healthy buying a large policy, the exam pays for itself.

Where no-exam can actually save you

There is a flip side worth naming. If a full exam would surface a condition that lands you a steep rating or a decline, a well-chosen simplified issue policy can end up cheaper than the substandard offer full underwriting would have produced, or it can be the difference between coverage and none. This is exactly where an independent agent earns their keep, by knowing which carriers forgive which conditions. Our overview of life insurance with health conditions walks through how carriers view common diagnoses and which underwriting path tends to treat them kindly.

One more cost factor that catches people off guard is time itself. Your rate is set by the version of you who applies today, and life insurance almost never gets cheaper as you age or as new conditions appear. Waiting for the perfect policy you never actually buy is the most expensive choice of all. If speed is what gets you covered this month, a slightly higher no-exam premium can be the bargain.

How fast you can actually get covered

Speed is where no-exam clearly wins. Accelerated and simplified issue policies can approve you in minutes to a few days because there is no exam to schedule and no lab results to wait on. Fully underwritten coverage typically takes about three to eight weeks from application to an in-force policy, and longer if your doctor is slow to send records. If you need protection in place now, no-exam is built for that.

Why does the timeline matter beyond impatience? Because you are not covered until the policy is actually issued and paid. During a multi-week underwriting window, you are exposed. For most people that risk is small, but life does not check your underwriting status before something happens. Several situations make speed genuinely important:

- A new mortgage or loan. You just took on a large obligation and want protection in force before the ink dries. See how this plays out in our guide to mortgage protection coverage.

- A new baby or marriage. A dependent now relies on your income, and you do not want to wait weeks to be covered.

- A business or divorce requirement. A contract, loan, or court order may require coverage by a specific date.

- Plain honesty about follow-through. If a weeks-long process is the thing that has stalled you for years, the policy you can finish today beats the ideal one you keep postponing.

The counterpoint is simple. If none of these apply and you are healthy, a few weeks of patience can buy you a lower rate and a bigger benefit for the entire life of the policy. Speed is valuable, but it is not free, and it is not always necessary.

How much coverage you can buy

Traditional life insurance lets you buy the most. Fully underwritten policies routinely issue benefits into the millions, because the carrier has enough information to take on that much risk. No-exam coverage is usually capped lower, with accelerated underwriting reaching into the hundreds of thousands, simplified issue often topping out lower still, and guaranteed issue limited to small final expense amounts.

This matters because the amount of coverage is the whole point. A policy that pays out reliably but is far too small still leaves your family short. Before you decide between no-exam and traditional, you need a real number for how much protection your household actually requires. If your honest number is large, say enough to replace a decade or two of income plus a mortgage and college, traditional underwriting may be the only path that can issue it in one policy. If your number is more modest, no-exam can cover it comfortably.

Do not guess at this. A common starting framework adds up income replacement, mortgage and other debts, and future costs like education, then subtracts existing savings and coverage. Our walkthrough on how much life insurance you actually need gives you a clean way to land on a defensible figure before you shop, so the coverage cap of any one option does not surprise you later.

When to choose no-exam life insurance

No-exam life insurance is the better choice when speed, convenience, or your health history matters more than squeezing out the last dollar of price. It is a genuinely good fit for reasonably healthy people who want coverage without friction, for anyone who needs protection in force quickly, and for people whose medical history would make a full exam risky or likely to produce a steep rating.

Reach for no-exam if one or more of these describes you:

- You want it done this week. A new baby, a new home, or years of procrastination make getting covered now worth a small premium.

- Needles or scheduling are your blocker. If the exam is the reason you have gone uninsured, removing it is the whole win.

- You have a manageable health condition. Certain histories are placed more smoothly through simplified issue than through a full exam that could trigger a decline.

- Your coverage need is moderate. If the amount you need fits inside no-exam limits, you may not need the extra ceiling traditional underwriting offers.

- You value simplicity. Fewer steps, less waiting, and a faster yes have real worth, even if the price is a little higher.

None of this means no-exam is a compromise you should feel bad about. It is often the smart, practical choice, and the coverage pays claims exactly like any other policy. The only trap is assuming no-exam always means almost no questions. Accelerated and simplified policies still screen your health through data and questionnaires, so answer everything truthfully. An untruthful application is the fastest way to have a claim contested during the first two years.

When to choose traditional life insurance

Traditional, fully underwritten life insurance is the better choice when you are healthy, want the largest possible benefit, and can wait a few weeks for the sharpest price. Because the exam lets you prove low risk, healthy applicants earn the best health classes and the lowest rates, and the coverage ceiling climbs into the millions. If maximizing coverage per dollar is your goal, traditional usually wins.

Lean toward traditional underwriting if these fit you:

- You are in good health. The exam is your chance to prove it and be rewarded with a preferred rate a no-exam model may not offer.

- You need a large benefit. Big income replacement, a sizable mortgage, or business needs often exceed no-exam caps.

- You are optimizing for price over years. On a long term policy, a lower rate compounds into real savings across the full term.

- A few weeks is fine. You have no urgent deadline and would rather wait for the better deal.

- You want the widest carrier choice. The full market, including the most competitive term products, opens up with full underwriting.

The trade-off is patience and a short, mildly inconvenient exam. For a healthy person buying a substantial term policy, that is usually a fair price for a lower rate locked in for decades. If you want to understand how the term itself is structured before you apply, our breakdown of term versus whole life insurance is a useful companion, since most no-exam and traditional shopping happens inside the term market.

A real worked example: two neighbors, two paths

To make this concrete, here is a side-by-side story of two people facing the same decision from different starting points. The names and numbers are illustrative, chosen to show how the choice actually plays out, not to quote a rate. Notice that they reach opposite conclusions and both are right for their own situation.

Maria, 34, healthy, wants a big benefit

Maria is a healthy nonsmoker with two young kids and a new 30 year mortgage. When she adds it up, she needs a large benefit to replace her income, clear the house, and fund college if the worst happens. She has no urgent deadline. For Maria, traditional underwriting is the clear pick. The exam is a minor inconvenience, and because she is genuinely healthy, it lets her lock in a top health class and a low rate on a benefit large enough to cover the whole plan. Skipping the exam would likely cost her more each month and might cap her below the amount she actually needs. She schedules the exam, waits about a month, and ends up with the most coverage per dollar for her family.

David, 47, well managed condition, wants it done now

David is 47, takes medication for high blood pressure and cholesterol, both well controlled, and wants coverage in place before his daughter's wedding season swallows his calendar. His coverage need is moderate, enough to clear debts and give his wife breathing room. For David, a no-exam path fits better. A full exam might flag his readings on a bad day and push him into a higher rating, and the multi-week wait is time he does not want to spend exposed. An accelerated or simplified issue policy through a carrier that treats controlled hypertension kindly gets him approved in days at a fair price. He pays a little more per dollar than a perfectly healthy applicant would, and in exchange he is protected now, with no lab surprises.

The lesson is not that one path is superior. It is that the right choice depends on your health, your coverage number, and your timeline. Maria valued maximum coverage and the best rate and had time to earn it. David valued speed and a smooth approval around a manageable condition. An honest agent runs both scenarios for you instead of assuming your answer, because the same question genuinely has two correct answers depending on who is asking.

Myths that push people to the wrong choice

A few stubborn myths steer people into the wrong policy, and clearing them up is often what unlocks a good decision. No-exam coverage is not fake, it is not always no-questions, and traditional coverage is not automatically cheaper for everyone. Getting these straight keeps you from overpaying or from skipping coverage entirely out of a misunderstanding.

Here are the ones I hear most, and the reality behind each.

- "No-exam policies do not really pay out." They pay valid claims just like any other policy. They come from the same licensed, financially rated carriers. What changes is how they collect health information, not whether the death benefit is real. The one thing that can void a claim is dishonesty on the application, which is true of every policy type.

- "No-exam means no health questions." Only guaranteed issue skips questions entirely. Accelerated and simplified issue still ask about your health and check databases like your prescription history and the MIB. Assuming otherwise leads people to answer carelessly and risk a contested claim.

- "Traditional is always cheaper." It is usually cheaper for a healthy person, not for everyone. If full underwriting would surface a condition that earns a steep rating, a smart simplified issue policy can cost the same or less, and it can be the only path to a yes.

- "Guaranteed issue is a great deal because anyone qualifies." Anyone qualifies precisely because the carrier prices for the highest risk. Tiny caps, high cost per dollar, and a waiting period make it a last resort, not a default.

- "If I pick no-exam now, I am stuck." Not true. Many people buy no-exam to get protected fast, then later apply for a fully underwritten policy for a better rate or larger benefit, and only drop the first policy once the new one is approved and in force.

That last point is the content gap most articles miss, so it deserves its own line: these are not mutually exclusive forever. Buying coverage is not a single locked-in event. A no-exam policy today can be a bridge, real protection while life settles, that you later upgrade to a fully underwritten policy when you have time to do the exam. The cardinal rule is never to cancel existing coverage until the replacement is fully issued and in force. Layering, then replacing, is a legitimate and often smart strategy.

How to decide without overpaying

The cleanest way to choose between no exam vs traditional life insurance is to answer three questions in order: how much coverage you need, how fast you need it, and how your health looks on paper. Those three answers point almost everyone to the right path. From there, comparing real offers across several carriers, rather than accepting the first pitch, is what protects you from overpaying.

Here is the practical path, in the order I would walk a friend through it.

- Nail down the number first. Decide how large a benefit your family actually needs before you look at underwriting. The amount often decides the path on its own.

- Be honest about urgency. If you truly need coverage in force this week, no-exam is built for that. If not, patience can buy a better rate.

- Take an honest look at your health. Very healthy points toward traditional for the best price. A health history often points toward a no-exam carrier that forgives your condition.

- Compare both, across carriers. Underwriting models differ wildly between insurers. The same person can be preferred at one carrier and rated at another. This is the single biggest lever on price.

- Answer every question truthfully. On any policy type, honesty on the application is what keeps a claim from being contested in the first two years.

- Use an independent agent who shows you options. If someone only ever presents one product, treat that as a flag. You want trade-offs laid out, not a single script.

For context on why comparing matters, according to research published by LIMRA, a large share of Americans go without the coverage they know they need, and a leading reason is the belief that it costs far more or is far harder to get than it actually is. The Insurance Information Institute is another neutral place to read up on how term policies are structured before you talk to anyone selling one. And on the reassuring side, under current federal tax rules a life insurance death benefit paid to your beneficiaries is generally received free of federal income tax, which you can confirm in the IRS guidance on taxable and nontaxable income. When you are ready for a real conversation, you can get a clear, no-pressure look at both paths with Sovereign Life Group, your life insurance strategist.

Not sure which path fits you?

Fifteen minutes. We will look at your coverage number, your timeline, and your health, then compare no-exam and fully underwritten options across multiple carriers so you see the real trade-offs. No pressure, no jargon, just your best fit laid out plainly.

Book a 15-Min Review Prefer to move fast? You can save my card or get a quick quote and we will follow up.

Frequently asked questions

Is no-exam life insurance more expensive than traditional life insurance?

Usually a little, yes. Because the insurer has less health data, it prices in more unknown risk, so a healthy person often pays somewhat more for no-exam coverage than for a fully underwritten policy. The gap is frequently small for younger, healthy applicants and can widen with age or a coverage amount in the hundreds of thousands. The right way to know is to compare real offers side by side.

Is no-exam life insurance legitimate and does it really pay out?

Yes. No-exam policies are issued by the same licensed, rated carriers that sell fully underwritten coverage, and they pay valid claims the same way. The main differences are how they gather health information and how much coverage they will issue, not whether the death benefit is real. Answer the health questions truthfully so a claim is not contested later.

What is the difference between simplified issue and fully underwritten life insurance?

Simplified issue uses a short health questionnaire and no medical exam, so approval is fast but coverage amounts are lower and prices run higher. Fully underwritten life insurance uses a detailed application plus an exam with blood and urine, which takes longer but unlocks the highest coverage limits and the best rates for healthy applicants.

Can I switch from a no-exam policy to a traditional policy later?

Often yes. Many people buy no-exam coverage to get protected quickly, then later apply for a fully underwritten policy for a lower rate or a higher benefit, and drop the first policy only once the new one is approved and in force. Never cancel existing coverage until the replacement is fully issued.

Does no-exam life insurance require any health questions at all?

Most does. Accelerated and simplified issue policies skip the physical exam but still ask health questions and check databases like your prescription history and the MIB. Only guaranteed issue policies skip health questions entirely, and those carry small benefit caps, higher costs, and usually a waiting period before the full benefit applies.

Which is better for someone with a health condition?

It depends on the condition. Some conditions are handled well by fully underwritten carriers who can review the full picture and offer a fair rate. Others are easier to place through simplified issue, where a short questionnaire avoids a decline. A good independent agent compares both paths across several carriers so a diagnosis does not push you into the most expensive option by default.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.