How Much Life Insurance Do I Need? Find Your Number

The Short Version

Start with 10 to 12 times your income, then sharpen it with the DIME method: add your debt, income replacement, mortgage, and education costs, and subtract what you already have. The number that remains is the coverage you are actually shopping for. Most families land somewhere between the rule of thumb and a full needs calculation.

If you have ever asked yourself "how much life insurance do I need," you are already ahead of most people. It is the right question, and it deserves a real answer instead of a sales pitch. The goal is simple. You want enough coverage that the people who depend on you could keep their lives intact if your income suddenly stopped, without buying so much that the premium becomes a burden today. The trick is landing on a life insurance amount that is built from your actual life, not a number someone guessed for you.

Below is the same walkthrough I use on the phone with families. No jargon, no pressure. We will start with the quick rules of thumb, move to the DIME method and income replacement, work a full example with real numbers, adjust for stay-at-home parents and different life stages, and finish with the mistakes that cost people the most. By the end you will have a number you can actually defend, and you will understand why it is your number.

What this guide covers

- Why the amount matters most

- The quick rules of thumb

- Income replacement, explained

- The DIME method, step by step

- A full sample calculation

- Build your own coverage calculator

- Subtract what you already have

- How much for a stay-at-home parent

- How the number changes by life stage

- Does the amount change the policy type?

- Common mistakes to avoid

- How to turn your number into a policy

- Frequently asked questions

How much life insurance do I need, and why the amount matters most

Most people shop for life insurance by price first. That is backwards. A policy that is cheap but far too small can leave your family short of what they actually need, and that is the exact problem you were trying to solve in the first place. The amount comes first. Price comes second. Once you know the right number, you can shop the price honestly, because you are comparing the cost of the same job rather than the cost of two different jobs.

Here is the way to think about it. Life insurance is income replacement. When you pass, the paycheck stops, but the bills do not. The mortgage, the groceries, the car payment, the kids' activities, the utilities, all of it keeps coming. The right coverage amount is the one that lets your family keep paying for the life you built together, for as long as they need to find their footing. That might be three years while a spouse retrains, or it might be eighteen years until a toddler is grown. The honest answer to how much life insurance you need is always tied to the answer of how long, and for whom.

There is a real cost to getting this wrong in either direction. Buy too little, and you have spent money on a promise that still leaves your family scrambling. Buy far too much, and you are paying premiums today that you cannot comfortably keep, which raises the risk you cancel the policy in a few years when money gets tight. A canceled policy protects no one. The aim is the right amount, the amount you can fund and keep, sized to the people who would feel the gap.

No medical exam for a ballpark. Free, and no pressure.

The quick rules of thumb, and where they break

If you want a fast answer in under a minute, the rules of thumb get you in the neighborhood. They are not precise, but they are a useful sanity check before and after you do the detailed math.

The 10 to 12 times income rule

The most common starting point is to multiply your annual income by 10 to 12. If you earn 70,000 dollars a year, that points you toward roughly 700,000 to 840,000 dollars of coverage. According to industry research from LIMRA, a large share of households say they would feel financial strain within months if a primary earner passed away, which is exactly the gap a properly sized policy is meant to close. The 10 to 12 times rule is popular because it is simple and it usually lands in a sensible range for a working parent with a mortgage and kids.

The age-banded multiplier

A more refined rule of thumb adjusts the multiplier for your age, because a younger earner has more future paychecks to replace than an older one. A widely used version looks like this: about 30 times income in your late teens to age 40, about 20 times from 41 to 50, about 15 times from 51 to 60, and about 10 times from 61 to 65. The logic is that a thirty-year-old is insuring decades of earning power, while a sixty-year-old is insuring a much shorter runway. It is a blunt tool, but it captures something the flat multiplier misses.

Where the rules of thumb break

A multiplier is useful, but it is only a starting line. It does not know whether you have a 400,000 dollar mortgage or a paid-off house. It does not know whether you have one child or four, whether your spouse earns nothing or earns more than you, or whether you already carry a policy through work. Two families with identical incomes can have wildly different real needs. That is why the rule of thumb is a first draft, not the final number. To get a figure built from your real life, you move to income replacement and the DIME method.

Income replacement, explained in plain English

The single biggest job most life insurance does is income replacement. So it helps to slow down and define it, because it is the heart of the whole calculation. Income replacement means giving your family enough money to stand in for the paychecks you would have brought home, for the number of years they would actually need them.

There are two honest ways to think about it. The simple version multiplies your annual income by the number of years your family would need support. If you earn 70,000 dollars and your youngest child is two, your family might need that income for the roughly sixteen years until that child is independent, which points toward a large number on the income piece alone. The more careful version accounts for the fact that a lump sum of life insurance can be invested conservatively and earn something while it is spent down, so a smaller amount can sometimes fund the same number of years. Both approaches are reasonable. For most families, multiplying income by the years of need gives a safe, slightly generous figure, and that margin of safety is a feature, not a bug, because grief is not the time to discover the math was tight.

The key decision inside income replacement is the number of years. Be honest with yourself here. Common anchors families use include the years until the youngest child finishes school, the years until a surviving spouse could reasonably become self-sufficient, or the years until a planned retirement when other savings would take over. Pick the anchor that fits your family, multiply, and you have the income piece. The rest of the calculation, the DIME method, simply makes sure you do not forget the big one-time costs that income replacement alone leaves out.

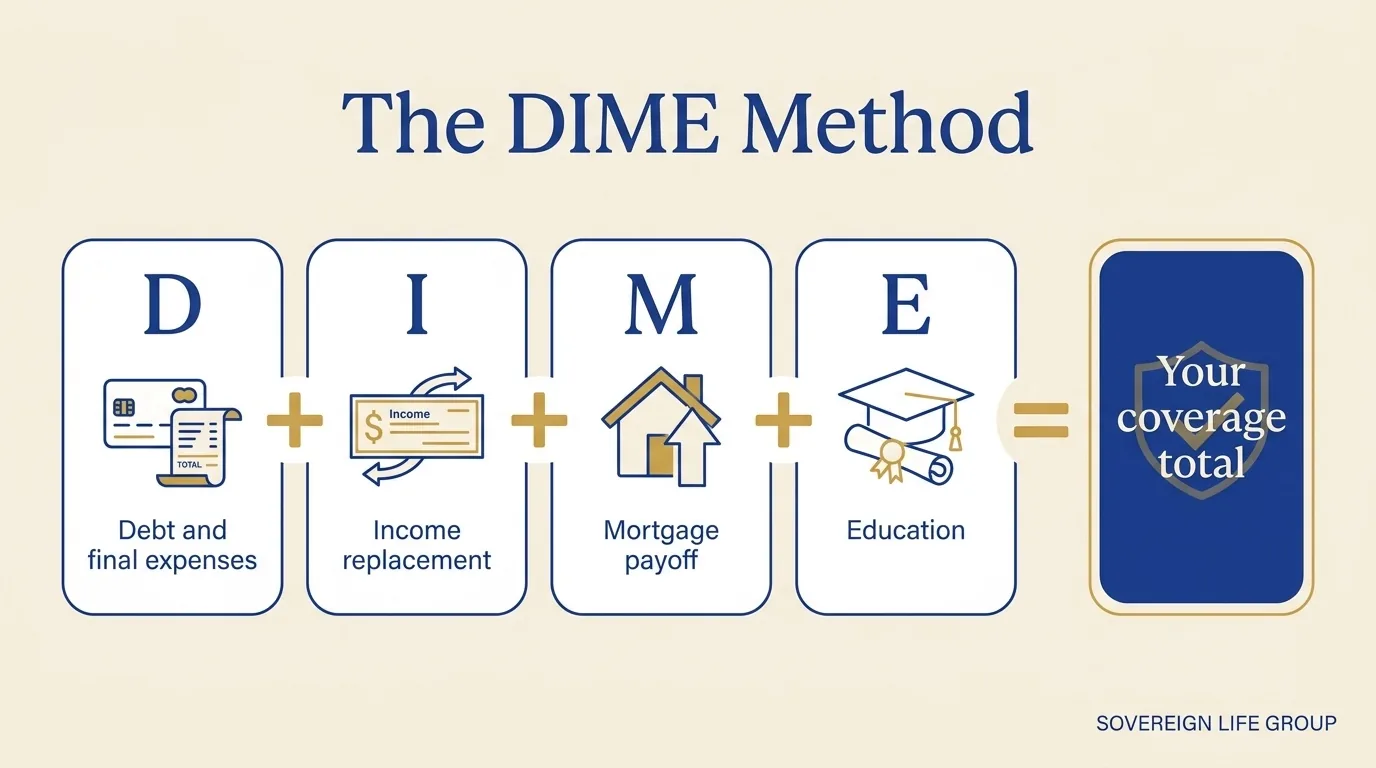

The DIME method, step by step

DIME is a simple checklist that turns "I have no idea" into a grounded estimate. It is the most widely taught needs-based approach for a reason: it is easy to remember and it catches the four things that actually drain a surviving family's resources. DIME stands for four numbers you add together.

- D is for Debt and final expenses. Total your non-mortgage debt: credit cards, car loans, student loans, and any personal loans. Then add an estimate for final expenses, since a funeral and related costs commonly run into the thousands. You do not want your family inheriting those payments on top of everything else.

- I is for Income replacement. Decide how many years your family would need your income replaced, then multiply your annual income by that number. This is almost always the largest piece of the total, and it is the one that does the heavy lifting of keeping the lights on month to month.

- M is for Mortgage. Add your remaining mortgage balance. A paid-off home is one less thing your family has to worry about losing, and removing that single largest monthly payment buys them enormous breathing room.

- E is for Education. Estimate what you want to set aside for your children's schooling. A frequently used planning range is 100,000 to 150,000 dollars per child for college, though even a partial amount can take real pressure off later. Adjust it to your goals and your kids.

Add those four together and you have a needs-based number. Think of it as a personal life insurance coverage calculator you can run on a napkin. It is rough, but it is yours, and a number built from your obligations beats a generic multiplier every time. The beauty of DIME is that it forces you to look at the one-time costs, like the mortgage payoff and education, that a simple income multiple quietly ignores.

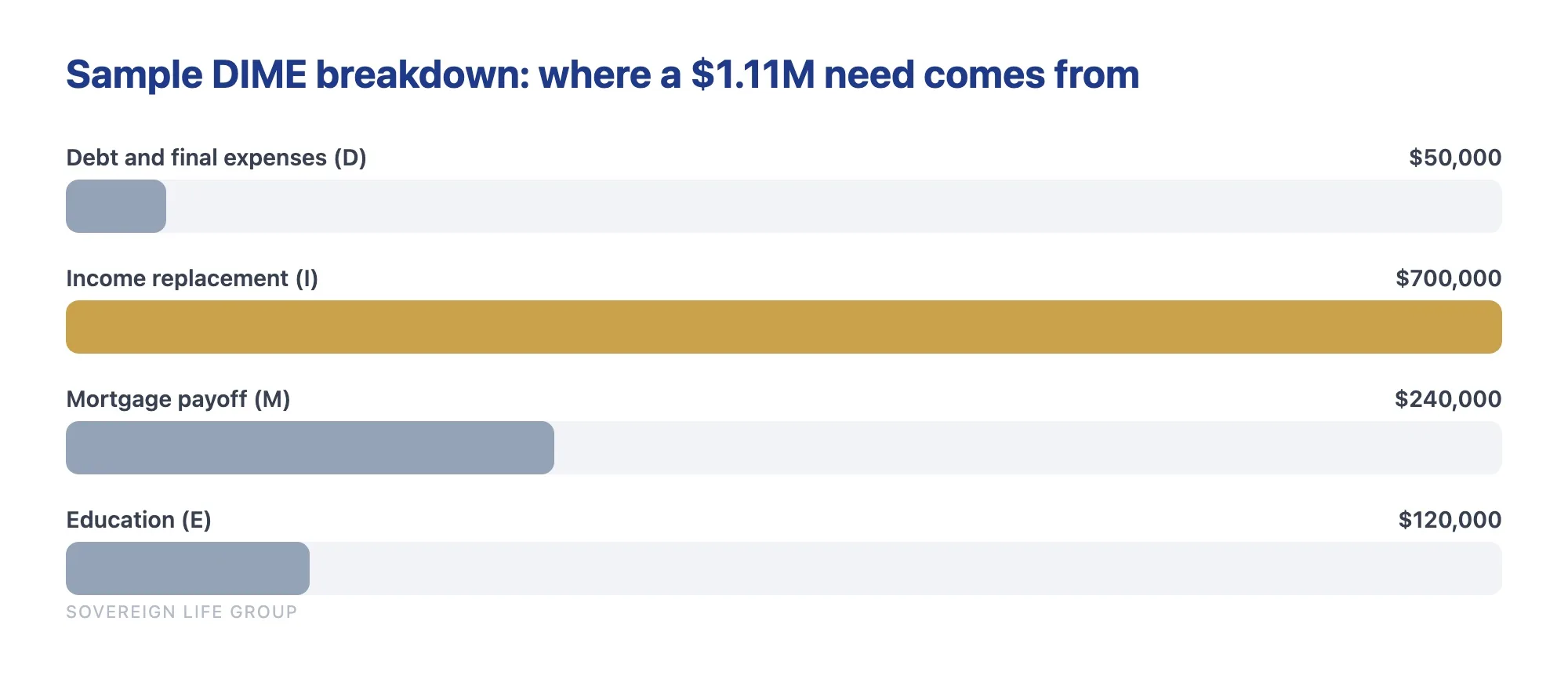

A full sample DIME calculation

Numbers make this concrete. Imagine a 35-year-old parent earning 70,000 dollars a year, with a mortgage, a car loan, some credit card debt, and two young children. Here is how the DIME method might shake out. These figures are illustrative only, meant to show the math rather than to quote any real policy or premium.

| DIME factor | What it covers | Sample amount |

|---|---|---|

| Debt and final expenses | Car loan, credit cards, and an estimate for a funeral and final bills | 50,000 |

| Income replacement | 70,000 per year for 10 years of support | 700,000 |

| Mortgage | Remaining home loan balance | 240,000 |

| Education | College support for two children | 120,000 |

| Total need | Sum of the four factors | 1,110,000 |

That total looks large, and it should. It reflects what it would genuinely cost to keep this family whole if the earner were gone tomorrow. The good news is that for a healthy person at this age, term coverage in this range is often far more affordable than people expect, because term life is priced to do one job well. Locking it in early matters too, since the best age to buy life insurance is usually younger than people assume, and both age and health help set the rate you can get.

Build your own coverage calculator in five lines

You do not need a fancy online coverage calculator to get a solid answer. You need five lines on a piece of paper or a notes app. Here is the whole thing, and it takes about ten minutes once you have your numbers in front of you.

- Line 1, income replacement: annual income times the years your family would need it.

- Line 2, debts and final expenses: all non-mortgage debt plus a funeral estimate.

- Line 3, mortgage payoff: the balance left on your home loan.

- Line 4, future goals: education, and anything else you want funded, like a paid-off car or a cushion for the surviving spouse.

- Line 5, subtract your assets: savings, existing policies, and accessible funds your family could use.

Add lines 1 through 4, subtract line 5, and the result is your coverage target. That is the entire calculation an agent runs for you, just done on your own terms first so you walk in informed. If you would rather not do it alone, we are glad to walk through your numbers together on a short call, but the math itself is genuinely this simple. The point of doing it yourself first is that you arrive knowing the answer, which means no one can talk you into far more, or far less, than you actually need.

Get a fast, free estimate tailored to your age and health.

Subtract what you already have

The DIME total is your need, not your purchase. Before you shop, subtract the resources your family could realistically draw on. This is the step most rule-of-thumb estimates skip, and skipping it is how people end up over-insured and overpaying.

- Existing life insurance, including any policy you bought before and any coverage through your employer.

- Savings and emergency funds your family could access without hardship.

- Other liquid assets they could use without selling the home or disrupting long-term retirement plans.

So if our sample family already had 110,000 dollars in combined savings and group coverage, their gap would be about 1,000,000 dollars. That gap, not the gross need, is the coverage they are actually shopping for. One caution worth repeating: workplace coverage usually ends when the job does, and it is often only one or two times salary, which rarely covers a real family need. Leaning on group coverage alone can be risky. Building your own plan that travels with you is part of the broader set of money moves that build wealth in your 30s and 40s, and it is one of the few that protects everything else you are trying to build.

How much life insurance do I need for a stay-at-home parent

This is the piece families miss most often. A stay-at-home parent may not bring home a paycheck, but the work they do has real economic value. Childcare, transportation, cooking, cleaning, scheduling, and household management would all cost money to replace. If that parent passed, the surviving spouse might need to pay for full-time childcare and help, or cut back at work to provide it themselves, and either choice has a price tag.

You can run a lighter version of the DIME method here, focused on the cost of replacing care and keeping the household running for several years. A practical approach is to estimate the annual cost of the childcare, housekeeping, and other help the family would need to hire, then multiply by the number of years until the youngest child is more independent. For many families that math points to a meaningful policy, often a few hundred thousand dollars, which surprises people who assumed a non-earning parent needed little or no coverage. The goal is not to put a price on a person. It is to make sure grief is never compounded by a financial crisis, and that the surviving parent has the room to grieve without immediately going back to work or into debt.

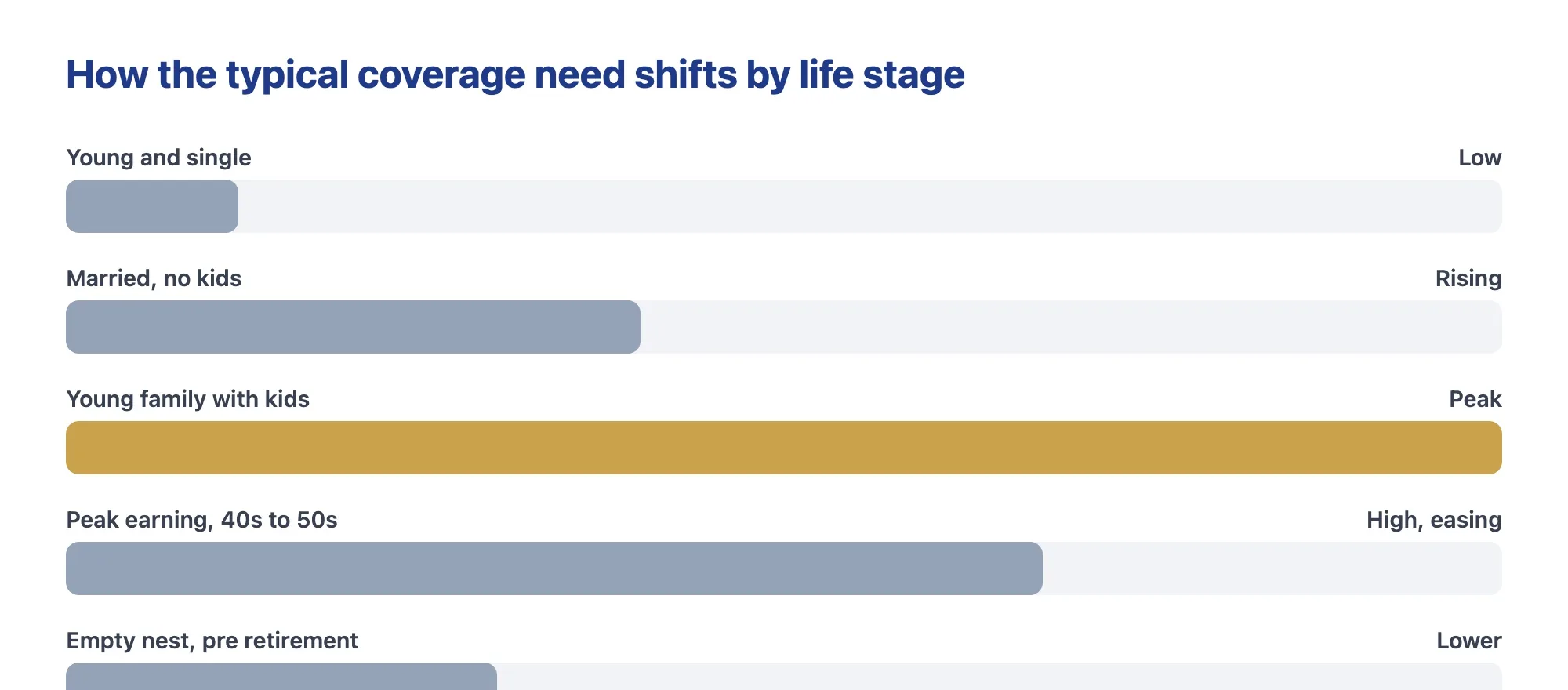

How the right number changes by life stage

Your life insurance amount is not a fixed target you hit once. It rises and falls as your responsibilities change. Understanding the shape of that curve helps you size coverage for where you are now, and anticipate when you will want to revisit it. Here is the general pattern.

| Life stage | What is driving the need | Typical direction |

|---|---|---|

| Young and single, no dependents | Co-signed debt, future insurability, locking a low rate | Low, if any |

| Married, no kids | Shared debt, a mortgage, replacing income for a spouse | Moderate and rising |

| Young family with children | Income replacement, mortgage, childcare, education | Highest, peak need |

| Peak earning years, 40s and 50s | Remaining mortgage, college, a few more income years | High but starting to ease |

| Empty nest and pre-retirement | Final expenses, legacy, a spouse's retirement security | Lower, more focused |

| Retirement and beyond | Final expenses, leaving something behind, a specific debt | Smallest, purpose-built |

The takeaway is that the biggest number usually lands in the young-family years, when income replacement, a fresh mortgage, and small children all stack up at once. That is also when budgets feel tightest, which is the tension at the center of this whole question. The answer is almost always term insurance sized to the peak need and matched to the years it lasts, because it delivers the most coverage for the least money during exactly the decade you need the most. As the kids launch and the mortgage shrinks, your need naturally falls, and you can let a term policy expire or carry a smaller permanent policy for lasting goals.

Does the amount change the policy type you choose?

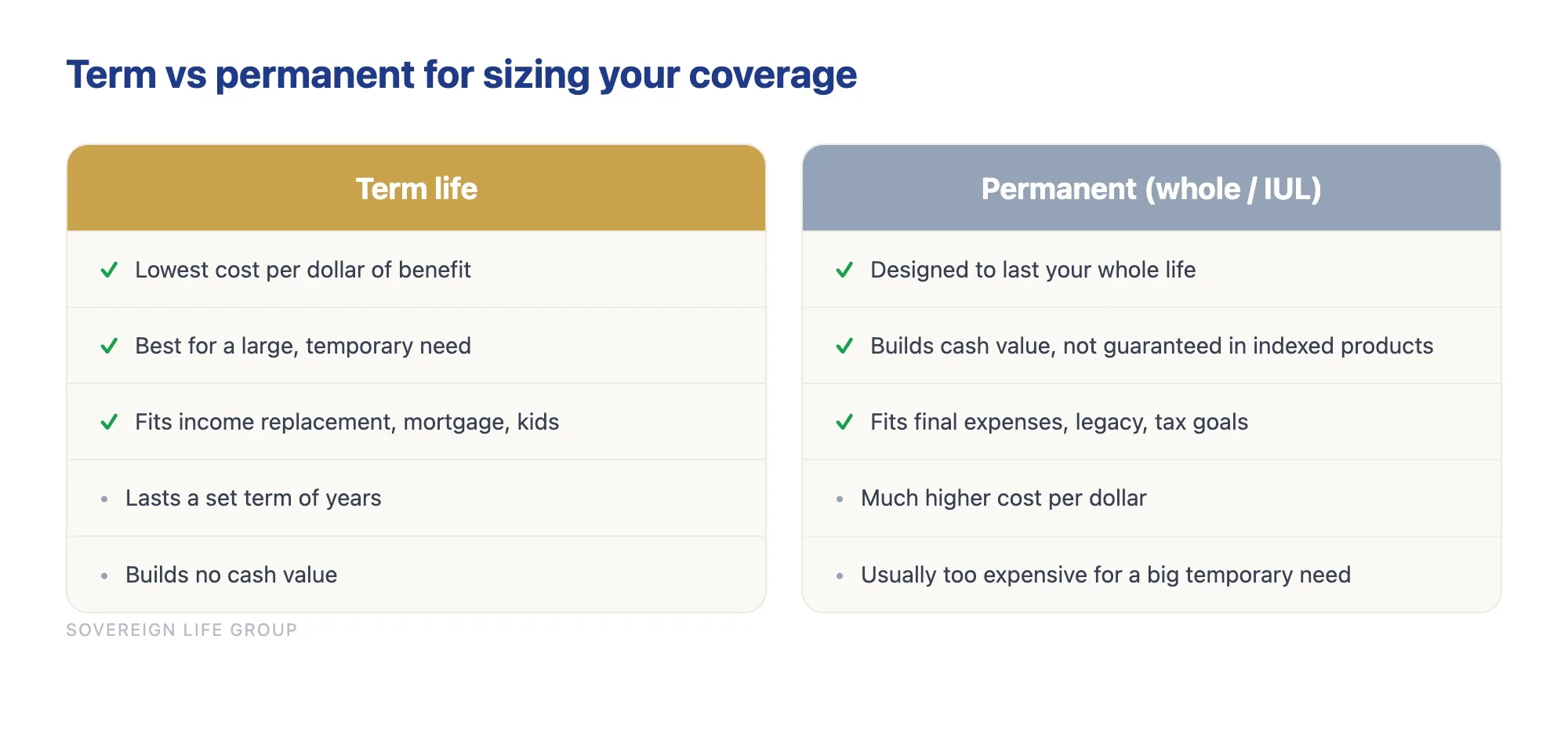

It can, and it is worth understanding because the right product depends partly on the size and the duration of your need. The two broad families are term and permanent, and they answer different questions.

Term life insurance covers you for a set number of years and pays a death benefit if you pass during the term. It is the most affordable way to get a large benefit, which makes it the natural fit for a big, temporary need like replacing income while the kids are home and the mortgage is large. When your DIME number is high and the need has a clear end date, term usually wins on cost.

Permanent insurance, such as whole life or an indexed universal life policy, is designed to last your whole life and can build cash value over time. It costs significantly more per dollar of death benefit than term, so it is not the tool for chasing the biggest number cheaply. It fits lasting needs that do not expire, like final expenses, leaving a legacy, or certain estate goals. The honest trade-off is real: permanent coverage costs more, and cash value growth is not guaranteed in indexed products, so it should be matched to a specific job rather than bought by default.

| Factor | Term life | Permanent (whole / IUL) |

|---|---|---|

| Cost per dollar of benefit | Lowest | Much higher |

| Best for a large, temporary need | Yes, this is its strength | Usually too expensive at scale |

| How long it lasts | A set term of years | Designed to last your whole life |

| Builds cash value | No | Yes, though not guaranteed in indexed products |

| Best fit | Income replacement, mortgage, raising kids | Final expenses, legacy, certain tax goals |

For most people asking how much life insurance they need, the answer is a term policy sized to the DIME number, sometimes paired with a smaller permanent policy for a lasting need. Many families even layer two term policies of different lengths so coverage steps down as obligations shrink, which keeps the premium efficient over time. Once you have a target number, it helps to see the average cost of life insurance by age and coverage amount so the monthly price is no surprise.

Common mistakes to avoid

After a lot of these conversations, the same handful of errors come up again and again. None of them are about being bad at math. They are about skipping a step or trusting a shortcut too far.

- Buying on price alone. A policy that is too small to do the job is not a bargain. Decide the amount first, then shop the price for that amount.

- Forgetting the mortgage and education. A simple income multiple can quietly leave out the two biggest one-time costs. DIME exists to catch them.

- Counting on group coverage forever. Workplace life insurance often disappears when you change jobs, and it is usually too small to begin with.

- Ignoring the stay-at-home parent. The cost of replacing childcare and household work is real, and it deserves coverage too.

- Forgetting to update the amount. A new baby, a new mortgage, a divorce, or a big raise can all change your number. Coverage you bought five years ago may no longer fit.

- Skipping coverage because the exam feels like a hurdle. Many people qualify for a no-exam life insurance option with health questions instead of needles, depending on age, health, and the carrier.

How to turn your number into a policy

Once you have a coverage target, the path to an actual policy is short and not nearly as intimidating as people fear. Here is the practical sequence.

- Confirm the amount. Run the DIME math, subtract your assets, and write down the gap. That gap is your target.

- Match the term to the need. If your youngest is a toddler, a longer term covers them to independence. If the need ends when the mortgage does, match the term to the loan.

- Apply while your health is on your side. The application captures today's health, and today is, on average, your best health going forward. Age and health both help set your rate.

- Compare honestly, then act. Look at more than one carrier, understand the trade-offs, and then actually pull the trigger. The most expensive policy is the one you keep meaning to buy. If you want a clear, no-pressure look at your numbers, you can find a real human and not a robot at Sovereign Life Group, your life insurance strategist.

Want help running your number?

Fifteen minutes. We will work through the DIME method together, account for income replacement, and find the simplest way to cover the gap. No pressure, no jargon, just a straight answer for your situation.

Get a Quote Book a 15-Min Call Prefer to start small? Save my card or get a quick term life quote.Frequently asked questions

How much life insurance do I need?

A common starting point is 10 to 12 times your annual income, then sharpened with the DIME method, which adds your debt, income replacement, mortgage, and education costs and subtracts what you already have. The right life insurance amount depends on your family's bills, debts, and how many years they would need support, not on a single rule of thumb.

Is 10 times my income enough life insurance?

For many families it is a reasonable baseline, but it is only a rule of thumb. A household with a large mortgage, several young children, or a single income may need more, while someone with few dependents and significant savings may need less. Running the DIME method or an income replacement calculation gives you a number built from your actual obligations.

What is the DIME method for life insurance?

DIME stands for Debt, Income, Mortgage, and Education. You add up your non-mortgage debt and final expenses, several years of income replacement, your remaining mortgage balance, and expected education costs. The total is a grounded estimate of how much coverage your family would actually need before you subtract existing assets.

How much life insurance do I need for a stay-at-home parent?

Often more than people expect. A stay-at-home parent provides childcare, transportation, cooking, and household management that would cost real money to replace. A common approach is to insure several years of the cost of paying for that care and help, so the surviving spouse can keep the household running without going into debt or cutting back at work.

Should I subtract my savings and existing coverage from the amount?

Yes. After you total your needs, subtract the resources your family could realistically use, such as savings, emergency funds, existing life insurance, and any workplace group coverage. The gap that remains is the coverage you are actually shopping for, which keeps you from over-buying and overpaying.

How often should I update my life insurance amount?

A good rule is to review it every few years and after any major life change, such as a new baby, a new mortgage, a marriage, a divorce, or a big raise. Your coverage should track your responsibilities as they grow and shrink, so the life insurance amount you bought five years ago may no longer be the right number today.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. The figures shown are illustrative examples to demonstrate the math, not quotes or promises of coverage. Product availability, features, rates, and approval depend on your age, health, state, and the issuing carrier, and any coverage is subject to underwriting approval. Please talk with a licensed professional about your specific situation before making any decision.