No-Exam Life Insurance: How It Works and Who Qualifies

The Short Version

No-exam life insurance approves you without a blood draw or physical, using health questions and data instead. It is fast and convenient, and more people qualify than expect to. Very healthy buyers can sometimes earn a lower rate by taking the exam, so it is worth comparing both before you decide.

A lot of people put off life insurance for one stubborn reason: they do not want to deal with a nurse, a needle, and a cup. That is exactly where this no-exam life insurance guide comes in. No medical exam life insurance lets you apply, get a decision, and get covered without any of that. For busy parents especially, and for people who live behind the wheel like long-haul truck drivers shopping for life insurance, removing that one obstacle is often what finally gets the job done after months or years of meaning to.

This is the long version, written to answer the questions people actually ask me on the phone. We will walk through how no-exam underwriting really works, the three very different products hiding under the "no exam" label, who qualifies, how much it costs, how fast you can be covered, the trade-offs against a traditional exam, and the mistakes that quietly cost families money. No hype. Just the honest picture so you can pick the right path for your household.

What this guide covers

- What no-exam life insurance actually is

- How the underwriting works behind the scenes

- The three types and how they differ

- Who qualifies for no-exam coverage

- How much it costs versus an exam

- How fast you can be covered

- Coverage limits, ages, and term lengths

- Health conditions and no-exam coverage

- Graded benefits and waiting periods

- No exam versus a medical exam: the trade-offs

- A real worked example

- Does it build cash value?

- Common mistakes to avoid

- Who it is best for

- How to apply: a simple checklist

- Frequently asked questions

What no-exam life insurance actually is

No-exam life insurance is real life insurance, the same term and permanent products the Insurance Information Institute describes. The only thing that disappears is the paramedical exam, the part where someone draws blood, takes a urine sample, and checks your blood pressure at your kitchen table. Everything else about the policy works the way a traditional one does. There is a death benefit, you name a beneficiary, you pay a premium, and if you pass away while the coverage is in force, the carrier pays your family.

It helps to clear up the most common misunderstanding right away. "No exam" does not mean "no underwriting" and, for most products, it does not mean "no questions." It means the insurer is sizing up your risk a different way, leaning on data and your answers instead of a fresh blood and urine sample. That distinction matters, because it explains why two people can both buy "no exam" coverage and end up with wildly different prices, benefit limits, and waiting rules. The label is an umbrella. What sits under it is what counts.

It also helps to know why this exists at all. For decades the exam was the gatekeeper, and it added four to six weeks and a fair amount of friction to buying a policy. A lot of families simply never made it to the finish line. Carriers noticed that the exam was scaring off healthy applicants who would have been profitable to insure, so they built faster paths. The result is a market where, for a large share of people, the exam is now optional rather than mandatory.

No medical exam for a ballpark. Free, and no pressure.

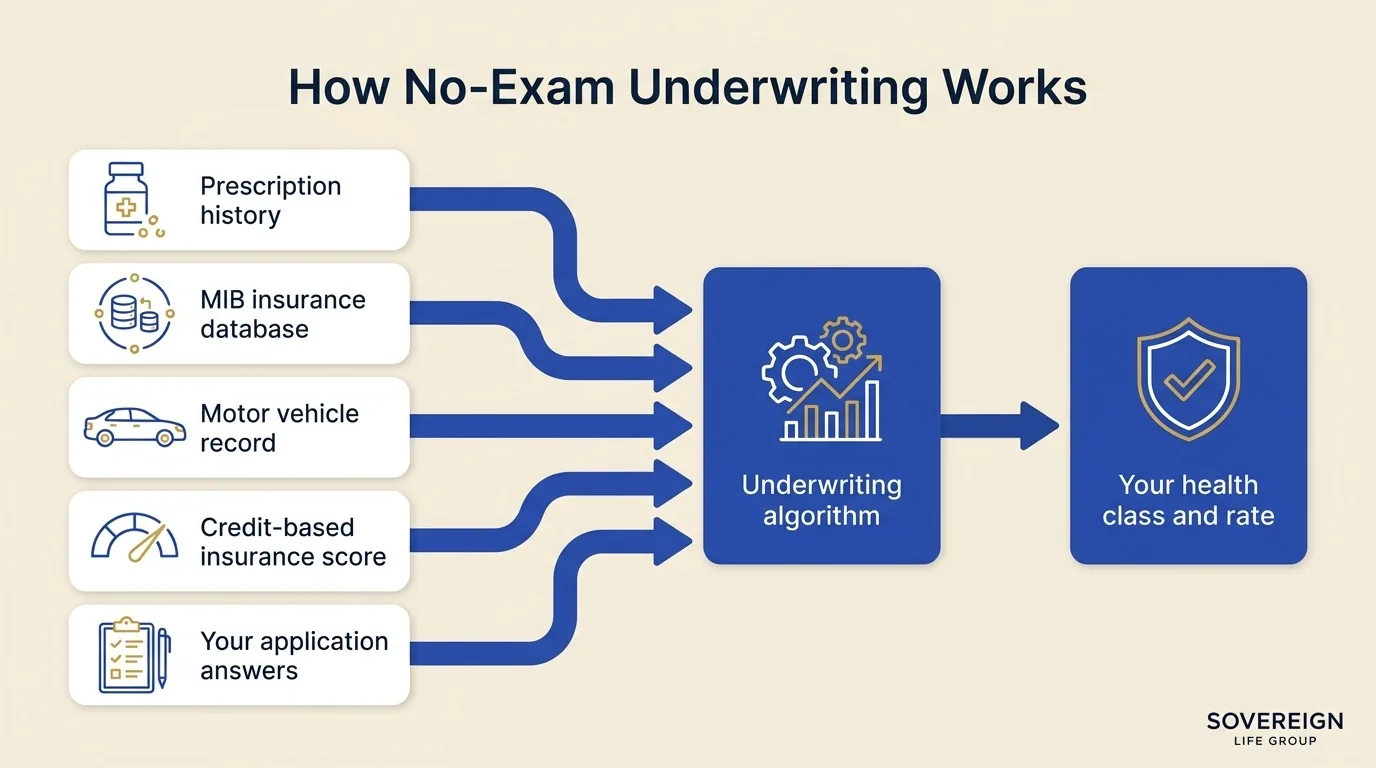

How no-exam underwriting works behind the scenes

If the carrier is not drawing your blood, how does it decide what to charge you, or whether to cover you at all? The short answer is data. Modern underwriting reads a set of databases in seconds and compares what it finds against the answers you gave on the application. When the picture is clean and consistent, you get a fast yes. When something does not line up, the file gets a closer look, and occasionally an exam is requested after all.

Here are the main sources a no-exam carrier typically pulls, in plain English:

- Prescription history. A database of the medications you have filled. This is one of the most revealing data points, because medications hint at the conditions behind them.

- The MIB (a shared insurance database). A record of past insurance applications across companies, used to catch inconsistencies between what you say now and what you said before.

- Your motor vehicle record. A history of tickets, suspensions, and serious driving violations, which correlate with risk more than people expect.

- Public and credit-based records. Some carriers use a credit-based insurance score, not your full credit report, as one more signal of overall stability.

- Your application answers. The health and lifestyle questions you answer honestly are still the backbone of the decision.

An algorithm weighs all of that and sorts you into a health class, the same kind of rating an exam-based policy uses. The cleaner and more consistent your profile, the better the class and the lower the rate. This is why honesty on the application is not just an ethical nicety. The carrier can and does verify your answers against the data, and a fib that surfaces later can give the company grounds to contest or deny a claim. Answer the questions straight. It is what keeps the coverage solid for the people you bought it for.

The three types of no-exam life insurance

This is the most important section in the guide, because almost every confusing thing about no-exam coverage traces back to people comparing two different products as if they were the same. "No exam" covers three distinct paths. The price, the amount of coverage, the speed, and who qualifies all change a lot from one to the next.

1. Accelerated underwriting

This is the one most healthy people actually want, and it is the closest thing to a traditional policy without the needle. It works like a normal fully underwritten policy, just with data standing in for the exam. The carrier reads your records, runs the algorithm, and makes a quick call. Clean applications can be approved in minutes to a few business days. Coverage can run from roughly $500,000 up to several million for healthy applicants, often under about age 60. Best of all, the rates can land close to what you would have paid with an exam, because the carrier is confident in the data it pulled.

The catch is that accelerated underwriting is the pickiest of the three. If your data raises a flag, or your answers do not match your records, the carrier may decline, offer a higher rate, or ask for an exam after all. It is built for people whose health story is clean and easy to verify.

2. Simplified issue

Simplified issue sits in the middle. You answer a short list of health questions, usually somewhere between five and fifteen, with no exam and no fluids. There is more forgiveness here for well managed conditions that might trip up accelerated underwriting. Coverage commonly tops out around $500,000, though some carriers go higher, and approval usually takes a few days. It is a solid landing spot when accelerated underwriting is not a fit but you still want a real underwriting answer and a meaningful benefit.

The trade-off is price. Because the carrier has less data confidence than it does in a fully verified accelerated file, simplified issue often costs somewhat more per dollar of coverage. You are paying a little extra for forgiveness and speed.

3. Guaranteed issue

Guaranteed issue asks no health questions at all, and you cannot be turned down for your health. That sounds like the easy button, and for the right person it is a genuine lifeline. But there are real strings, and an honest guide has to name them. The coverage is small, usually $5,000 to $50,000. The price per dollar of benefit is the highest of the three. And almost all of these policies carry a waiting period, commonly two to three years, before the full benefit pays out for death from natural causes. If you pass away from natural causes inside that window, the policy typically refunds the premiums paid plus some interest rather than the full face amount. Accidental death is usually covered from day one.

Guaranteed issue exists for people who cannot qualify elsewhere, often to cover final expenses like a funeral so the bill does not land on the family. It should be your fallback, not your first stop.

| Feature | Accelerated underwriting | Simplified issue | Guaranteed issue |

|---|---|---|---|

| Health questions | Yes, plus full data pull | Yes, a short list | None |

| Can you be declined? | Yes | Yes | No, not for health |

| Typical coverage | about $500k to several million | Up to about $500k | about $5k to $50k |

| Relative cost per dollar | Lowest of the three | Higher | Highest |

| Speed to decision | Minutes to a few days | A few days | Fast, but benefit waiting period applies |

| Best fit | Healthy buyers wanting larger coverage | Minor or managed conditions | Declined elsewhere or serious conditions |

Who qualifies for no-exam life insurance

More people than you would think. Underwriting has grown a lot more inclusive over the last several years, and the "no exam" door is wider than its reputation suggests. As a rough map of who tends to land where:

- Healthy applicants roughly 18 to 60 often qualify for the best accelerated-underwriting options and competitive rates.

- People with well managed conditions, such as controlled blood pressure, treated cholesterol, a stable thyroid issue, or well managed type 2 diabetes, frequently still qualify, sometimes through accelerated underwriting and sometimes through simplified issue.

- Busy parents and professionals who simply do not have time for an exam, and who want the decision handled this week rather than next month.

- Anyone who has stalled out for months because of needles, scheduling, or plain procrastination.

- Older buyers and those who have been declined before, who may use simplified issue or guaranteed issue rather than the top tier.

Age matters more than most people realize. Many no-exam products are aimed at applicants up to about 60 for the larger accelerated policies, while simplified issue and final-expense style coverage extend further into the senior years. If you have more serious health history, or you have been declined in the past, you still have paths for life insurance with a pre-existing condition. You may land in simplified or guaranteed issue instead of accelerated underwriting, which is the whole point of working with someone who knows which carriers say yes to what.

How much no-exam life insurance costs

Let me be straight about price, because the honest answer is more useful than a rosy one. No agent can promise you a specific premium from an article, since your rate depends on your age, health, the coverage amount, the term length, your state, and the carrier. What does hold true is the shape of the trade-off.

For a healthy person, skipping the exam usually costs a little more. The premium can run roughly 10 to 25 percent higher than a fully underwritten policy at the same coverage amount. For some accelerated-underwriting applicants the gap is smaller than that, and occasionally the rates come out close to identical. The reason is simple. When the carrier can verify a clean, low-risk profile from data alone, it does not need to charge much of a premium for skipping the exam.

But "more" is relative, and the dollars matter. For a healthy 40-year-old buying $500,000 of level term, choosing the no-exam path might add somewhere in the neighborhood of $12 to $17 a month versus the exam version. For a family that has been meaning to get covered for a year, that is often a fair price for being protected today instead of "someday." For a very healthy person who wants a large policy and does not mind the wait, the exam can pay for itself in lower premiums over the years of the term.

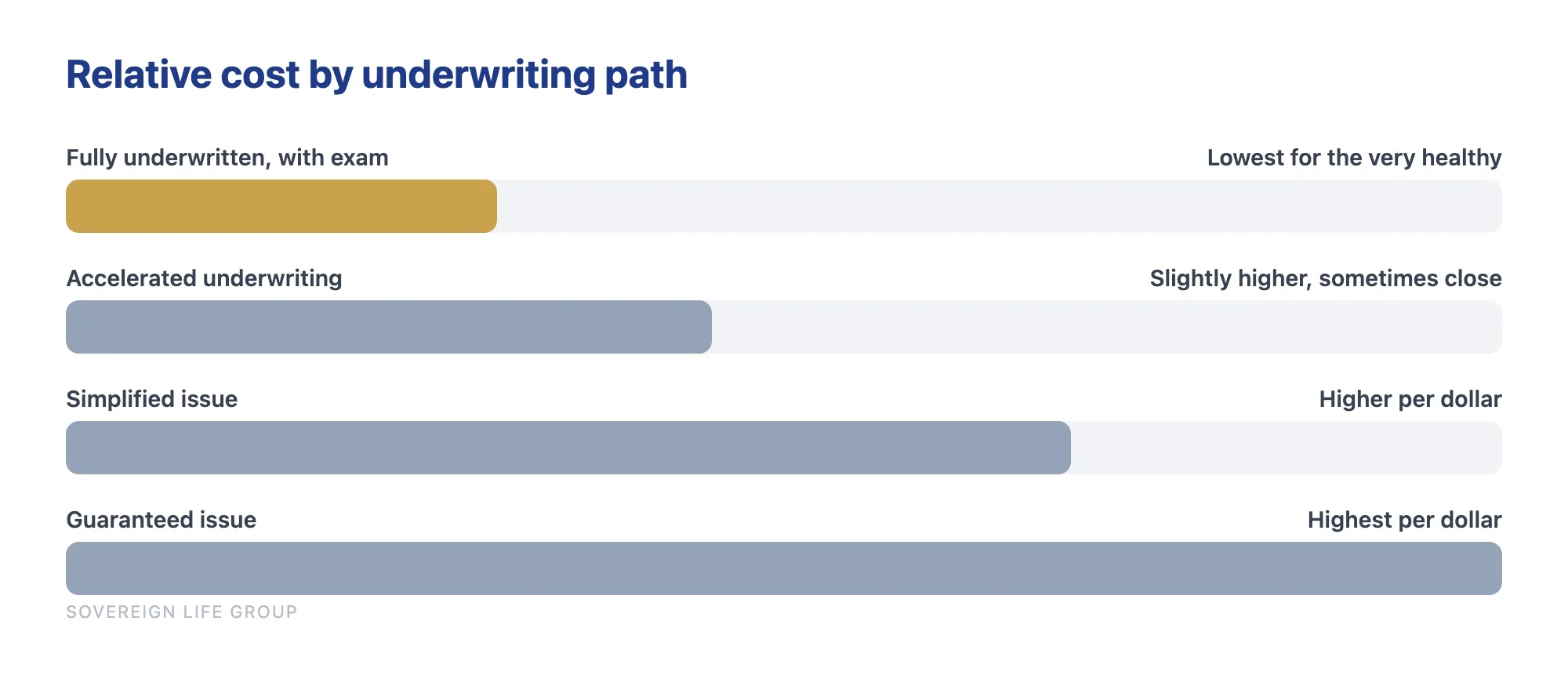

| Path | Relative cost | Typical speed | What you give up |

|---|---|---|---|

| Fully underwritten (with exam) | Lowest for the very healthy | Four to six weeks | Time and the hassle of the exam |

| Accelerated underwriting | Slightly higher, sometimes close | Minutes to a few days | A small premium for skipping fluids |

| Simplified issue | Higher per dollar | A few days | More cost in exchange for forgiveness |

| Guaranteed issue | Highest per dollar | Fast approval, waiting period applies | Small benefit and a graded benefit period |

Here is the honest rule I give people. If you are young, healthy, and you want the lowest possible rate on a big policy, take the exam. If your health is average, your time is tight, or you have stalled out for months, no-exam coverage is often the smarter real-world choice. According to research published by LIMRA, a large share of Americans say they own less life insurance than they know they need, and a common reason is the belief that it costs more or takes more effort than it actually does. The best policy is not the theoretical cheapest one. It is the one that actually gets in force and protects your family.

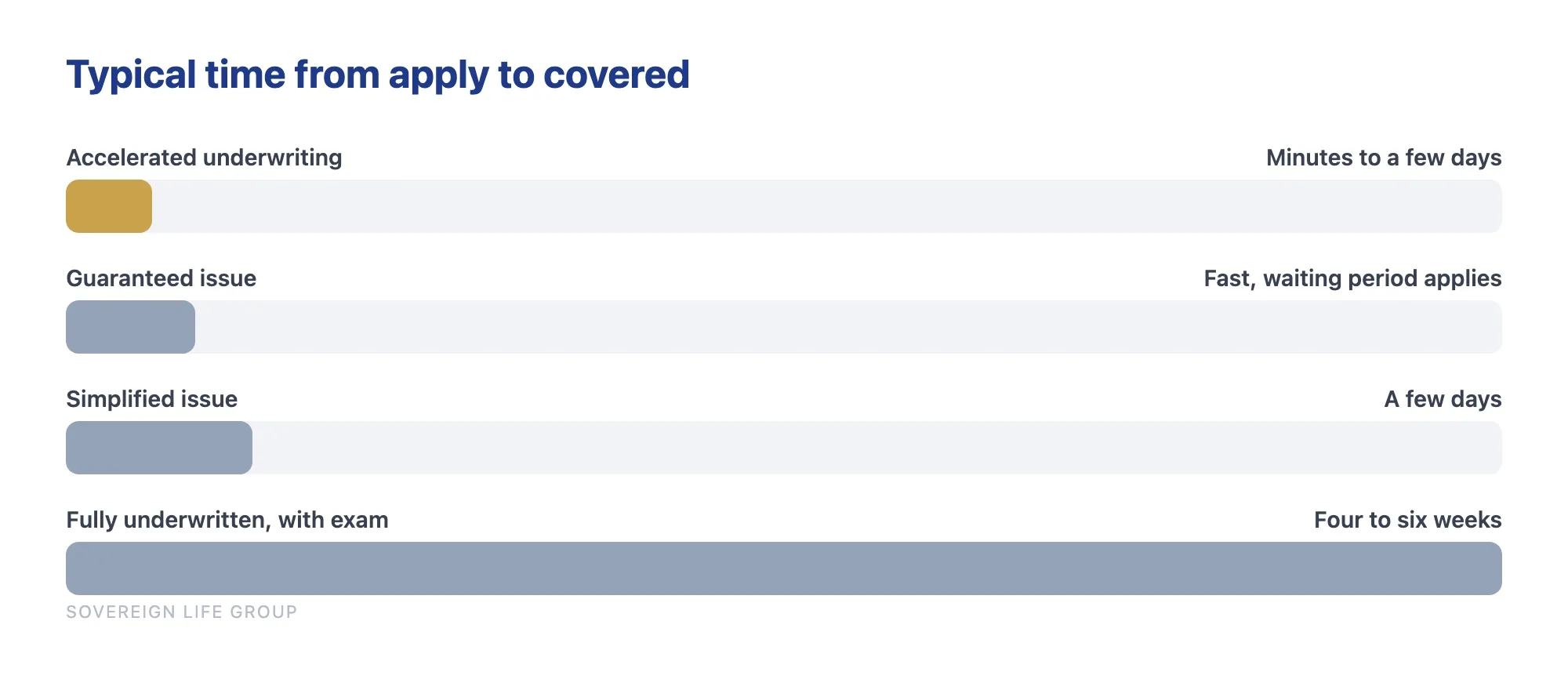

How fast you can be covered

This is the part people love, and it is the single biggest practical reason no-exam coverage exists. A fully underwritten policy with an exam can take four to six weeks from application to approval, because the carrier has to schedule the exam, wait for lab results, and review everything. No-exam coverage compresses that timeline hard.

- Accelerated underwriting: often instant to a few business days for clean applications. Some carriers can issue a same-day decision online.

- Simplified issue: usually a few days, sometimes faster, depending on how the health questions are answered.

- Guaranteed issue: fast approval, but remember the benefit waiting period before full natural-cause coverage applies.

Speed always depends on the carrier and your answers. If your data is clean and your responses are consistent, you can be the person who applies on a lunch break and is covered before dinner. If something needs a second look, the timeline stretches, and occasionally the carrier asks for an exam to finish the file. For a lot of families, though, no medical exam life insurance means real coverage in days instead of waiting a month and a half, which is often the difference between getting it done and letting it slide again.

Coverage limits, age ranges, and term lengths

Three practical constraints decide whether no-exam coverage can do the job you need it to do. It is worth understanding all three before you fall in love with the convenience.

Coverage amount

This is where the paths diverge most. Accelerated underwriting can reach into the hundreds of thousands and, for healthy younger applicants at some carriers, into the millions. Simplified issue commonly caps around $500,000. Guaranteed issue is built small, usually $5,000 to $50,000. If you need a large death benefit to replace years of income and pay off a mortgage, the exam-based or accelerated paths are where the big numbers live. If you need a modest, purpose-built benefit, the smaller products fit fine.

Age

Most no-exam products serve applicants from 18 up through roughly 60 to 65 for the larger accelerated policies, with simplified issue and final-expense coverage extending into the 70s and 80s. The older you are, the more the market tilts toward simplified and guaranteed issue, and the more the price reflects your age. This is one reason the best age to buy life insurance is usually younger than people expect: your options are widest and cheapest before the candles pile up.

Term length

No-exam term policies commonly come in level terms such as 10, 15, 20, and 30 years, matched to how long your family will depend on your income. Permanent no-exam options exist too. The exam status and the term length are separate choices. You can often pick the coverage length that fits the job and still skip the needle.

Health conditions and no-exam coverage

One of the biggest myths I run into is that any health condition disqualifies you from no-exam coverage. It does not. What a condition usually changes is which path you take and what you pay, not whether you can be covered at all. Here is a realistic map, keeping in mind that every carrier draws its lines differently.

- Often fine for accelerated underwriting: well controlled high blood pressure, treated high cholesterol, a stable thyroid condition, mild and well managed anxiety or depression, and a healthy weight range. These are common, and clean data often carries them through.

- More likely to land in simplified issue: well managed type 2 diabetes, a past condition that is now resolved, a build that is outside the preferred range, or a controlled condition that an algorithm flags for a closer human look.

- More likely to point toward guaranteed issue: a recent serious diagnosis, an organ condition, a history that has drawn declines elsewhere, or a combination of conditions that no questionnaire can forgive.

If you are managing a diagnosis, the worst thing you can do is assume the answer is no and never apply. Carriers vary enormously in how they treat the same condition, and an honest application routed to the right company is the only way to find your real number. Our page on life insurance with health conditions walks through how underwriters actually look at the most common ones, and it is a better starting point than guessing.

Get a fast, free estimate tailored to your age and health.

Graded benefits and waiting periods: read this twice

If there is one feature that surprises families at the worst possible moment, it is the graded benefit, also called a waiting period. It applies mostly to guaranteed-issue policies and some simplified-issue final-expense plans, and it is the trade-off you accept in exchange for skipping health questions.

Here is how it usually works. For the first two to three years, if you pass away from natural causes such as illness, the policy does not pay the full face amount. Instead it typically returns the premiums you paid plus some interest. If you pass away from an accident, the full benefit is generally available from day one. After the graded period ends, the policy pays the full benefit for any cause. This is not a scam or fine-print trickery. It is how a carrier can promise to cover someone without asking a single health question. But you have to know it is there, because a guaranteed-issue policy bought to cover a funeral next year may not do what the family expects if the insured passes from illness inside the window.

Accelerated underwriting and most standard term policies do not have graded benefits. They pay the full death benefit from the start once the policy is in force, subject to the usual contestability rules that apply to all life insurance for the first two years, which exist to catch fraud rather than to limit honest claims.

No exam versus a medical exam: the honest trade-offs

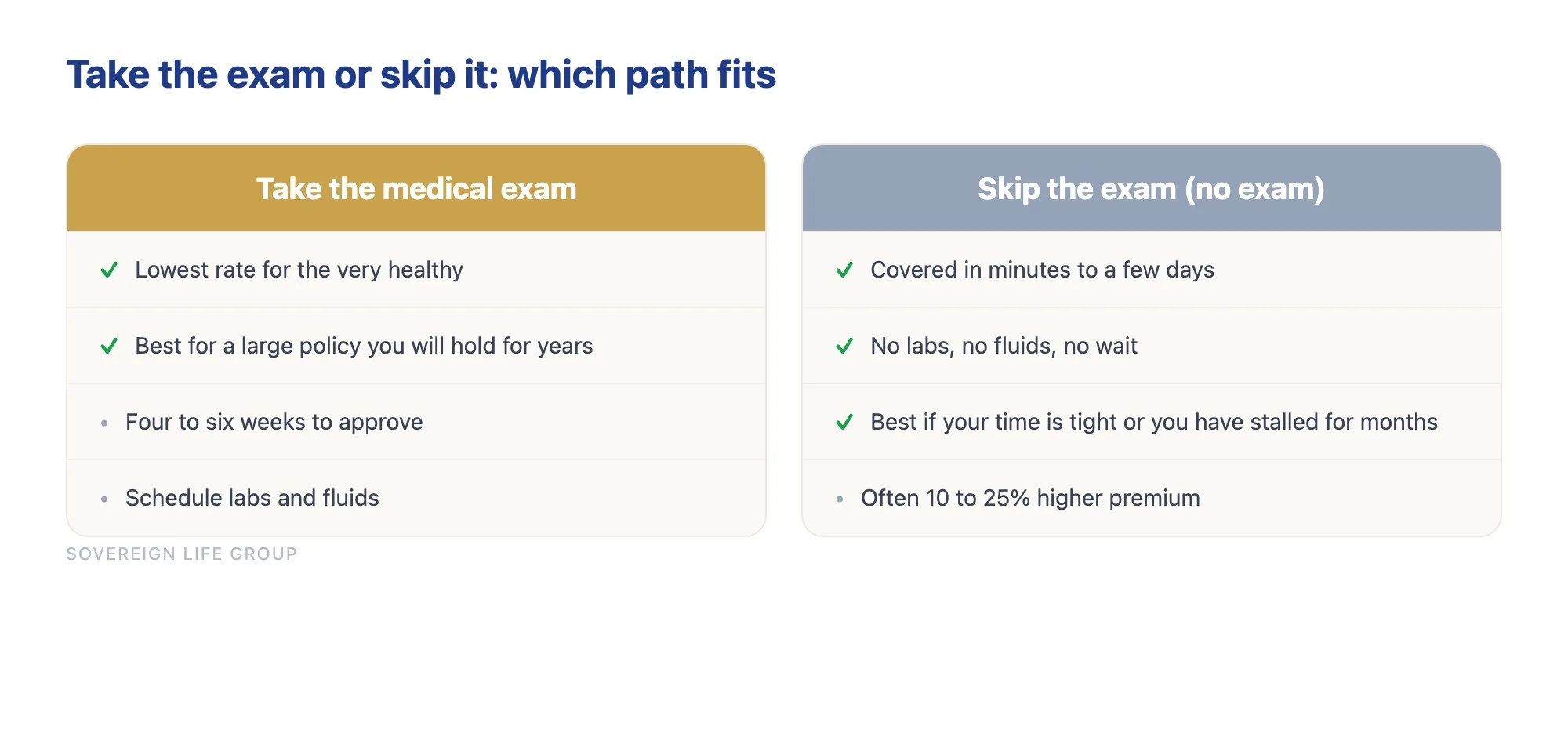

No product is free of trade-offs, and you deserve to hear them straight rather than as a sales pitch. The exam still has real advantages, and pretending otherwise would not serve you.

When the exam is worth it. If you are young, very healthy, and you want the largest possible policy at the lowest possible rate, the exam often wins. The carrier rewards verified good health with its best pricing, and over a 20 or 30 year term those savings can add up. If you have the time and the patience, and a few weeks does not change anything for your family, the exam can be the financially smarter route for a big policy.

When skipping the exam is worth it. If your time is tight, if your health is average, if you have a needle aversion, or if you have stalled out for months and the exam is the actual reason you are still uninsured, no-exam coverage usually beats a traditional policy as the real-world decision. Coverage that exists beats a slightly cheaper policy you never finish buying. The same logic applies if you have a fresh need, like a new baby or a closing on a house, and you want protection in place now rather than in six weeks.

There is also a quieter benefit to the exam path that rarely gets mentioned. The exam sometimes turns up a health issue you did not know about, which is unpleasant to learn but genuinely useful to catch early. And if you are on the fence about policy structure entirely, it is worth understanding the difference between term versus whole life insurance before you lock in, because the exam-versus-no-exam decision sits on top of the term-versus-permanent decision, not in place of it.

A real worked example: two paths, one family

Numbers in a table are easy to skim past, so let me make it concrete with a composite example drawn from the kind of calls I take every week. Names and details are changed, and the figures are illustrative rather than a quote.

Dana is 38, a non-smoker, in good shape, with one well managed thyroid condition and a low-dose daily medication for it. She and her husband just bought a house, and she has been meaning to get covered since the baby arrived two years ago. She wants about $500,000 of 20-year term so the mortgage and her income are protected while the kids are home. She has two realistic routes.

The first is the fully underwritten path with an exam. Given her health, she would likely earn a strong health class and the lowest available premium, but it means scheduling a nurse, waiting on labs, and roughly four to six weeks before the policy is in force. The second is accelerated underwriting. Her prescription and medical data are clean and consistent, her thyroid condition is the kind algorithms handle well, and she could plausibly get a decision in a day or two at a rate modestly higher than the exam version, often a difference measured in a few dollars a week rather than a transformation of the budget.

Here is how I would talk it through with her. If those few weeks genuinely do not matter and she will absolutely complete the exam, the fully underwritten route may save her a little each month over the 20 years. But she has already let two years slip by. For Dana, the honest recommendation is usually the accelerated path, because the small premium difference is a fair price for being protected this week instead of risking another season of "we will get to it." The coverage that exists is worth more than the slightly cheaper coverage she keeps not finishing. That is the whole decision in a sentence: match the path to the person you actually are, not the disciplined person you wish you were.

Does no-exam coverage build cash value?

This question comes up a lot, and the answer is that the exam decision and the cash-value decision are two separate things people often tangle together. Whether you take an exam has nothing to do with whether a policy builds cash value. That is determined by the type of policy.

No-exam term insurance has no cash value. It is pure protection for a set number of years, which is exactly why it delivers the most death benefit for the least money. Some no-exam permanent policies, on the other hand, can build cash value over time. That includes certain whole life designs and an indexed universal life policy, both of which some carriers offer with simplified or accelerated underwriting rather than a full exam. The honest trade-off, and it is a real one, is that permanent coverage costs significantly more per dollar of death benefit than term, the cash-value growth in indexed products is not guaranteed, and fees and policy structure matter a great deal. Permanent coverage is not automatically better. It is better for specific lifelong jobs, like leaving a legacy or covering final costs, and worse as a way to get the largest death benefit for the smallest premium. If a cash-value strategy is on your mind, treat it as its own conversation rather than a bonus feature of skipping the needle.

Common mistakes people make with no-exam coverage

After enough of these conversations, the same avoidable missteps show up again and again. Steering around them costs you nothing and can save your family a lot.

- Assuming all "no exam" policies are the same. Buying a small, expensive guaranteed-issue plan with a waiting period when you would have qualified for a large, cheaper accelerated policy is the most expensive mistake in this whole category. Always ask which of the three you are actually being offered.

- Overlooking the waiting period. If you buy guaranteed issue to cover a near-term need, the graded benefit can leave your family with returned premiums instead of the full face amount. Know the rule before you sign.

- Shading the truth to get a faster yes. The data pull will surface what the questions miss, and a misstatement can give the carrier grounds to contest a claim. Honesty is not just principled, it is what makes the policy reliable.

- Buying too little because it was easy to buy. Convenience can tempt people into a small policy that does not actually replace their income or cover the mortgage. Size the benefit to the job, then find the easiest honest way to get that amount.

- Never applying because of an assumption. Plenty of people who assume they will not qualify actually do. The only way to know your real number is to run it, and assuming the answer is no is one of the most common myths I see.

Who no-exam life insurance is best for

No-exam coverage tends to be the right fit when one or more of these is true:

- You want mortgage protection in place quickly so your family keeps the house if your income stops.

- You are a busy parent and the exam has been the one thing stopping you from finishing.

- You need final expense coverage and want to keep it simple, with a modest benefit built for funeral and final costs.

- You have a fresh life event, a new baby, a marriage, a home purchase, and you want protection now rather than in six weeks.

- You have a needle aversion or a schedule that never seems to allow for a paramedical visit.

And if you have been holding off because you assumed you would not qualify, please do not let an assumption decide this for you. The widest, cheapest options sit with younger and healthier applicants, but there is a no-exam path for a remarkable range of situations. The honest move is to check rather than to guess, and to decide up front whether buying life insurance online or working with an agent fits you better.

How to apply: a simple checklist

If you have decided no-exam coverage is worth a look, here is the practical path. None of it requires you to become an insurance expert.

- Decide what the money is for. Replace income, pay off the mortgage, cover final expenses, fund the kids to adulthood, or some mix. The job determines the amount and the type of policy.

- Size the benefit honestly. A common starting point is several years of income plus outstanding debts and future costs like education, minus what you already have saved or covered.

- Match the path to your health. If you are healthy, aim at accelerated underwriting. A managed condition often points to simplified issue. A history of declines points to guaranteed issue as a fallback.

- Answer every question honestly. The data pull verifies your answers, and accuracy is what keeps the policy reliable when it is needed most.

- Compare, then act. Look at more than one carrier, understand the trade-offs, and then actually finish. The most expensive policy is the one you keep meaning to buy. If you want a clear, no-pressure look at your options with a real human and not a robot, start with Sovereign Life Group, your life insurance strategist.

Not sure which type fits you?

Give me fifteen minutes. We will look at your health, your budget, and the fastest honest way to get your family covered, with no pressure and no jargon, just a straight answer for your situation.

Get a Quote Book a 15-Min Review Prefer to start small? Save my card or get a quick term life quote.Frequently asked questions

Is no-exam life insurance more expensive?

For a healthy person it usually costs a little more, often in the range of 10 to 25 percent over a fully underwritten policy at the same coverage. For some accelerated-underwriting applicants the gap is smaller, and occasionally the rates come out close to identical. If you are very healthy and have time, an exam can earn you a lower rate. If your health is average or you want speed, the gap is often small.

How fast can I get covered?

Accelerated underwriting can approve clean applications in minutes to a few business days. Simplified issue often takes a few days. Guaranteed issue approves quickly but applies a benefit waiting period for natural causes. A fully underwritten policy with an exam can take four to six weeks. Speed varies by carrier and your answers.

Who qualifies for no-exam life insurance?

Healthy applicants roughly 18 to 60 often qualify for the best accelerated options. People with well managed conditions like controlled blood pressure, treated cholesterol, or a stable thyroid issue can frequently qualify too, sometimes through simplified issue. Older applicants or those with serious conditions may use guaranteed issue, which asks no health questions in exchange for a smaller benefit and a waiting period.

How much coverage can I get without a medical exam?

It depends on the type. Accelerated underwriting can reach roughly $500,000 to several million for healthy applicants. Simplified issue commonly runs up to about $500,000. Guaranteed issue is much smaller, usually $5,000 to $50,000, and is built for final expenses.

Can I be denied no-exam life insurance?

Yes, with two of the three types. Accelerated underwriting and simplified issue still ask health questions and pull data, so an application can be declined or routed to a different product. Guaranteed issue cannot decline you for health, but it carries the smallest benefit, the highest cost per dollar, and a waiting period before the full benefit pays for natural causes.

Does no-exam life insurance build cash value?

It can, depending on the product. No-exam term has no cash value. Some no-exam permanent policies, such as certain whole life or indexed universal life designs, can build cash value over time, though values are not guaranteed in indexed products and fees and structure matter. The exam status and the cash-value question are two separate decisions.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company. Have a question? Contact us.