Life Insurance Myths: What's True and What Costs You

The Short Version

Most of the reasons people skip life insurance are myths. The biggest one is cost. Coverage is usually far cheaper than folks guess, and the families who get hurt are the ones who believed the myth and went without.

Life insurance has a marketing problem. Not because it is complicated, but because so many of the "facts" people carry around about it are wrong. And these life insurance myths are not harmless. They talk people out of coverage they could afford, leave families short when it matters most, and quietly cost real money.

I am a life insurance agent, and I have these conversations every week. The same handful of myths come up again and again, usually said with total confidence, and almost always wrong. So this is the full list, with the real 2026 numbers next to each one. No scare tactics, no hard sell. Just what is true, what is not, and what believing the myth actually costs a family. Read it, push back on it, and then decide for yourself.

The myths we are busting

- "Life insurance is too expensive"

- "My coverage at work is enough"

- "Stay-at-home parents don't need it"

- "I'm young and healthy, I can wait"

- "I'm single, so I don't need it"

- "The payout gets taxed away"

- "My health means I can't qualify"

- "Only the breadwinner needs it"

- "I have savings, so I'm covered"

- "Term insurance is throwing money away"

- Quick reference: myth vs reality

- How to find your real number

- The pattern behind all of them

- Frequently asked questions

Myth 1: Life insurance is too expensive

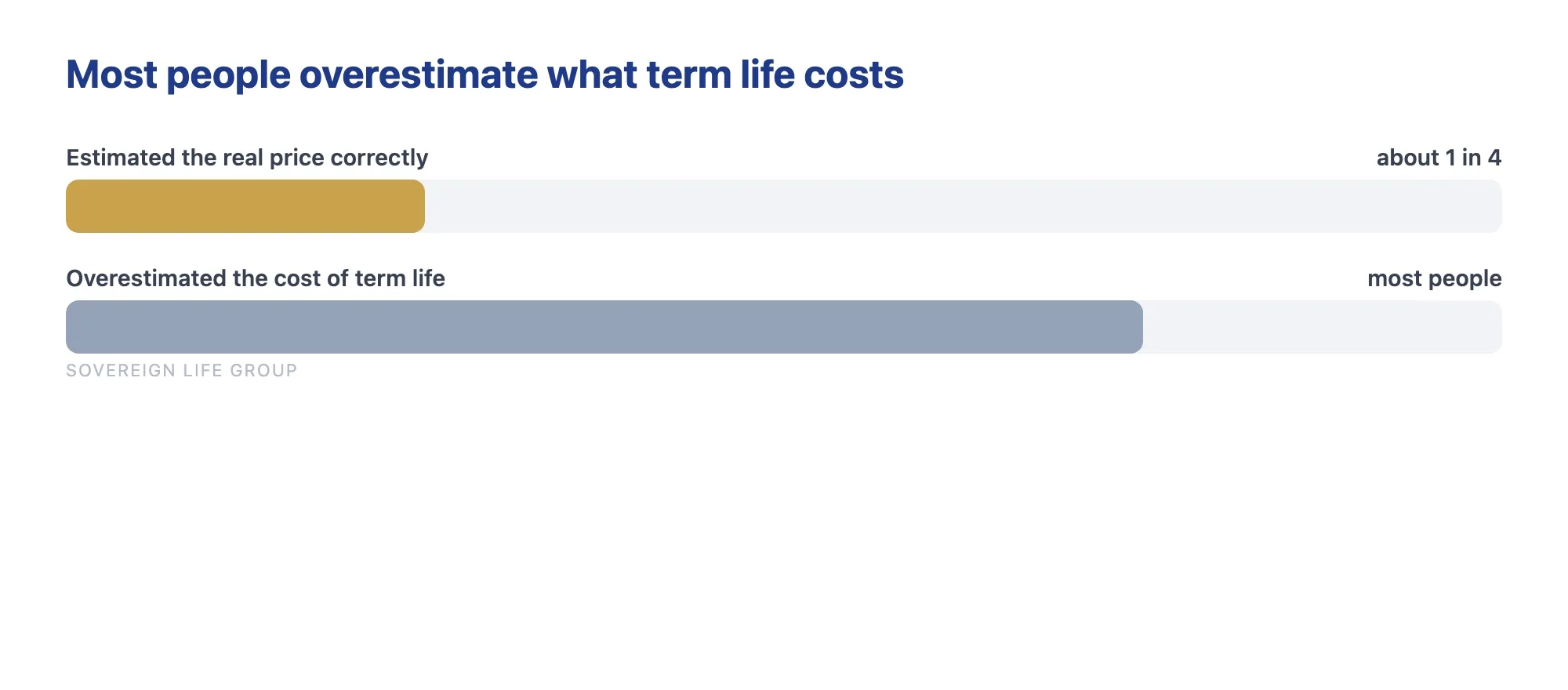

This is the big one, the myth that does the most damage. Most people who skip coverage do it because they assume it will cost a fortune, and the data says they are guessing wildly.

The truth: In the 2026 Insurance Barometer Study, a large share of Americans overestimated the cost of a basic 20-year term policy. Among younger adults the misjudgment was the worst, with many guessing several times the actual price of a $250,000 policy. Only about a quarter of people could put the real number in the right ballpark. The fear is real. The price tag behind it usually is not.

For a healthy person in their 20s or 30s, a solid term policy often runs about the cost of a couple of streaming subscriptions a month. That is it. Your real number depends on your age, your health, the coverage amount, and the term length, and no honest agent can promise you a specific figure from an article. But the point stands: you almost certainly think it costs more than it does. The only way to know your number is to get a real quote, which costs nothing and takes a few minutes.

It helps to picture what the myth is really comparing. People weigh life insurance against "money I would rather keep," when the honest comparison is "a small monthly amount" against "my family covering a mortgage, a funeral, and years of lost income on their own." Framed that way, the expensive option is going without.

No medical exam for a ballpark. Free, and no pressure.

Myth 2: My coverage at work is enough

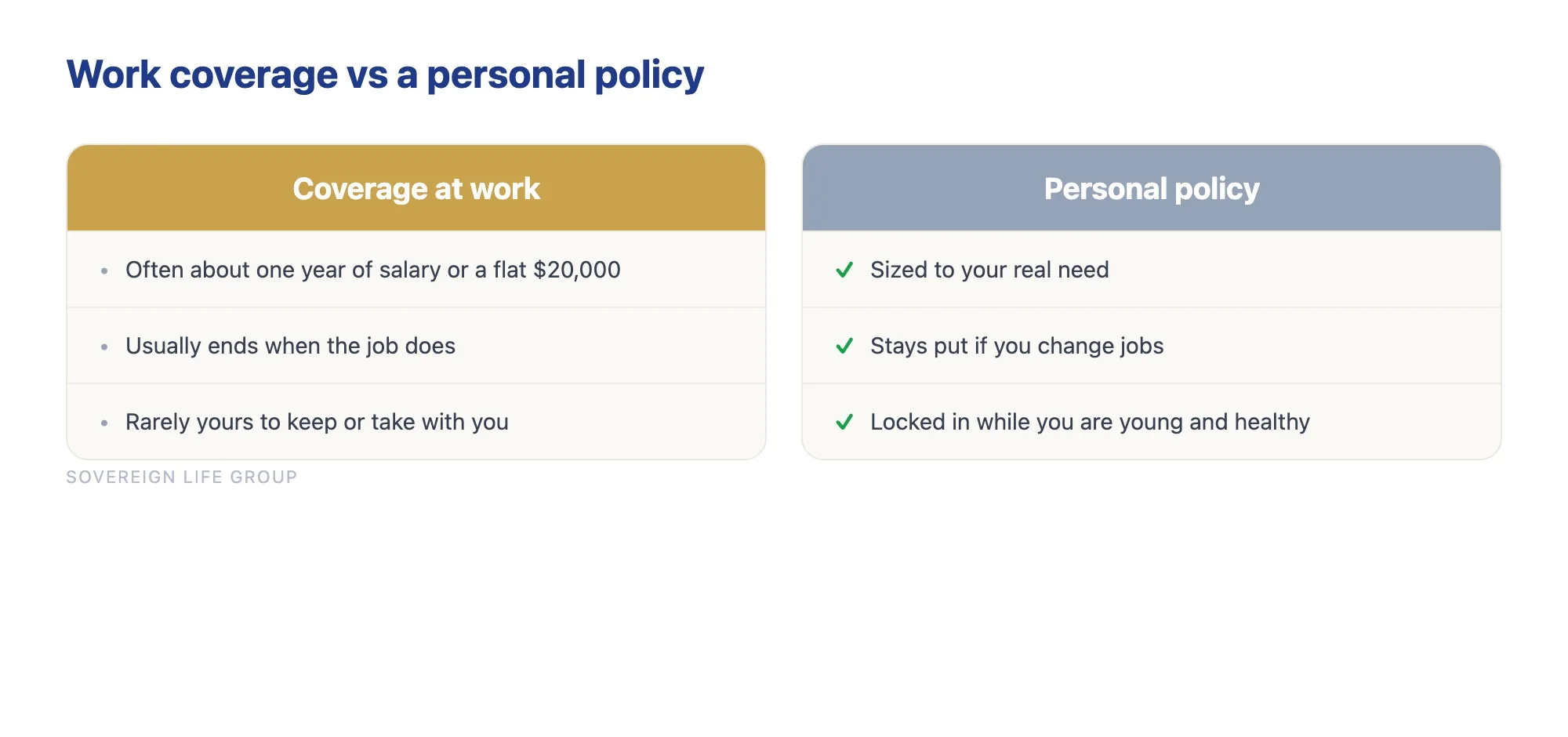

A lot of people check the "life insurance" box at their job and figure they are set. It feels handled, and that feeling is the trap.

The truth: Workplace coverage is a nice perk, but it is usually thin. The typical group policy is built around one year of salary or a flat amount near $20,000. For someone with a mortgage, kids, or a spouse who counts on their income, that does not go far. A single year of salary does not pay off a 30-year mortgage or raise a child to adulthood. Coverage-gap research from LIMRA has found that a large share of households relying only on workplace coverage say their family would struggle financially within six months of losing a wage earner.

There is a second catch that surprises people. That coverage usually is not yours to keep. It is tied to the job. Leave, get laid off, or retire, and it often walks out the door with you, frequently right when you are older and harder to insure. Some group plans let you convert to an individual policy, but the terms are rarely as good as a policy you would have shopped for on your own while healthy.

None of this means you should turn down the benefit. Free or cheap coverage through work is worth having. It just is not a plan on its own.

Myth 3: Stay-at-home parents don't need life insurance

The thinking goes like this. No paycheck, no need for insurance. It sounds logical, and it is flat wrong.

The truth: A stay-at-home parent does a job that would cost serious money to replace. Childcare, driving, cooking, cleaning, scheduling, all of it. National childcare averages alone run close to $18,000 per child per year in 2026. Add housekeeping, transportation, and the rest, and replacement-cost estimates for a stay-at-home parent commonly land somewhere in the range of $45,000 to $60,000 a year, with some analyses putting the full market value far higher.

If that parent passed away, the surviving spouse would have to pay for all of it out of pocket while still going to work, and often while grieving and trying to hold a family together. Putting life insurance on the stay-at-home parent funds that help, so the family is not forced to choose between earning a living and caring for the kids. That is why many families cover both parents, not just the earner. The death benefit on the at-home parent does not replace a salary, it replaces the cost of everything that parent quietly handled.

The honest counterpoint: the coverage on a non-earning parent is usually smaller than on the primary earner, because the job it is doing is different. You are funding replacement help and breathing room, not decades of income. So this is rarely an either/or. It is a matter of sizing each policy to the real role.

Myth 4: I'm young and healthy, so I can wait

This one feels smart. Why pay now when you could buy it later, closer to when you "need" it? Because waiting is one of the most expensive moves you can make.

The truth: Life insurance is priced mostly on two things: your age and your health. Both tend to move against you over time. Industry rate charts in 2026 show a 40-year-old often pays well over 50 percent more than a 30-year-old for the same $500,000 20-year term policy. Wait until 50 and that same policy can cost more than double what it would have at 40.

Then there is health, and this is the part people forget. You are likely the healthiest you will ever be right now. A single new diagnosis between now and "later," even something manageable like high blood pressure or elevated blood sugar, can raise your rate or move some options off the table, though life insurance with a pre-existing condition is still very much within reach. When you lock in a level term policy young, that low price holds for the whole term, even if your health changes the next year.

Waiting does not save you money. It costs you the best rate you will ever qualify for, which is exactly why the best age to buy life insurance is almost always sooner than you think. If needles or a medical exam are the holdup, there are no-exam options worth a look that can shorten the whole process to days.

Myth 5: I'm single, so I don't need it

No spouse, no kids, no reason for life insurance. Right? Not so fast. It depends on what you would leave behind, and most people leave behind more than they think.

The truth: Plenty of single people have real financial obligations that do not vanish when they are gone. A few common ones:

- Co-signed debt. If a parent co-signed a private student loan or a car, they can be on the hook for the balance. A small policy clears it instead of passing it on at the worst possible time.

- A mortgage or other shared loans. Anyone tied to the property or the note inherits the problem, and a forced sale is a hard way to settle it.

- Final expenses. A funeral can run well into five figures. Without coverage, that bill often lands on family, who may turn to savings or even a fundraiser to pay it.

- Aging parents or siblings you help support. If people lean on you financially, a policy keeps that support going for a while after you are gone.

And there is the timing angle from the last myth. Buying a modest policy while you are young, single, and healthy locks in a low rate and protects your insurability before life gets more complicated and more expensive to insure. If you marry or have kids in five years, you will be glad the coverage was already in place at a young person's price.

Myth 6: The payout gets taxed away

This is a quieter myth, but it talks a lot of people out of buying enough. The worry is that the government takes a big bite of the death benefit, so why bother insuring for the full amount.

The truth: In most cases, a life insurance death benefit paid to a named beneficiary is not counted as taxable income. According to guidance published by the IRS, proceeds you receive as a beneficiary because of the insured person's death generally are not included in your gross income and do not have to be reported. In plain terms, if you are the beneficiary, the lump sum usually arrives whole.

There are exceptions worth knowing, which is exactly why this is a "talk to a professional" topic and not a promise. If the payout is held by the insurer and earns interest before it is paid out, that interest can be taxable. If the policy is owned in a way that makes the death benefit part of a large estate, estate tax rules can come into play for high-net-worth families. And the rules around who owns the policy, who pays for it, and who collects can matter. This is general education, not tax advice, so confirm your specific situation with a qualified tax professional.

The takeaway is simple: do not shrink your coverage because you assume taxes will gut it. For most families, the benefit is not taxed as income, so size the policy to the real need.

Myth 7: My health means I can't qualify

This myth keeps some of the people who need coverage most from ever applying. They had a diagnosis, or they take a daily medication, so they assume the answer is automatically no.

The truth: A health condition usually changes the price or the type of policy, not whether you can get covered at all. Carriers insure people with managed conditions every day. Well-controlled high blood pressure, type 2 diabetes, a past cancer that is years behind you, anxiety, sleep apnea on treatment, and many other conditions are commonly insurable. The outcome depends on the details: how the condition is managed, how long it has been stable, and which carrier you apply with, because underwriting guidelines vary a lot from one company to the next.

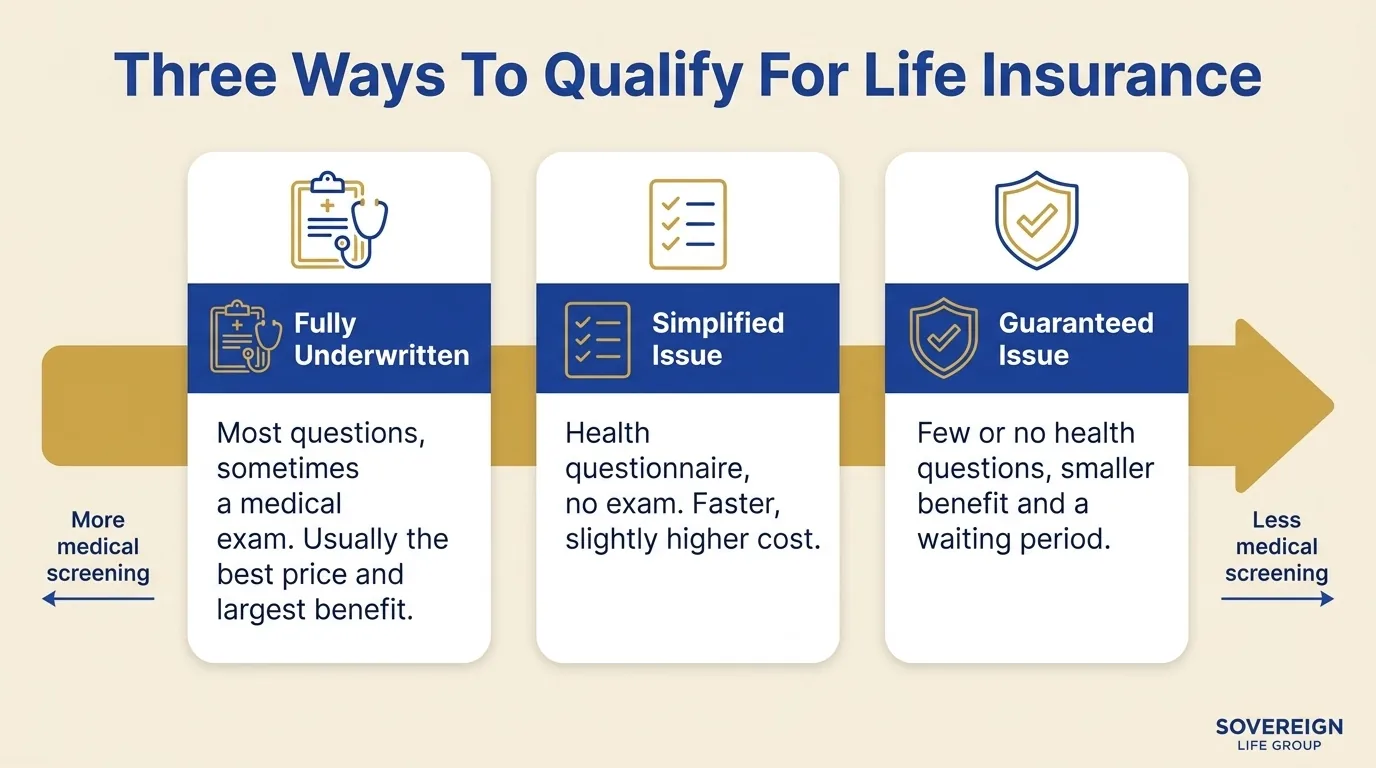

Here is the range of options, from most to least medical screening:

- Fully underwritten term or permanent. The most questions and sometimes an exam, but usually the best price for the coverage. Often the right fit even with a managed condition.

- Simplified issue. A health questionnaire and database checks, no exam. Faster, slightly higher cost, helpful when an exam is the obstacle.

- Guaranteed issue. Few or no health questions and no decline for health, in exchange for a smaller benefit and a waiting period before the full benefit applies. A real option for serious conditions or older ages.

The honest trade-off is cost and benefit size, not an automatic rejection. Because guidelines differ so much, the worst thing you can do is assume you are uninsurable and never ask. A good agent shops the carriers most likely to look favorably on your specific situation. Our deeper look at life insurance with pre-existing conditions walks through how this works condition by condition.

Get a fast, free estimate tailored to your age and health.

Myth 8: Only the breadwinner needs it

This one sounds reasonable. Insure the big paycheck, skip everyone else. But it leaves real gaps, and it overlaps with the stay-at-home-parent myth in a way worth separating out.

The truth: A death has a financial impact even when the person was not the top earner, or not an earner at all. A second income, even a smaller one, often covers real bills, and losing it can tip a household budget into the red. The unpaid work a partner does, from childcare to running the household, would cost money to replace whether or not they brought home a paycheck. And in a two-income home, the surviving partner may need to cut hours or take time off, which makes the loss bigger, not smaller.

There is also the future to think about. Even an adult with no dependents today may have them in a few years. Locking in coverage and a low rate while young and healthy protects the family that does not exist yet. The smarter rule is not "insure the breadwinner." It is "insure anyone whose death would create a financial hole," which, in most families, is more than one person.

Myth 9: I have savings, so I'm covered

This is a confident person's myth. You have been disciplined, you have an emergency fund and maybe an investment account, so why pay for insurance on top of it?

The truth: Savings and life insurance solve different problems, and savings rarely solve this one at scale. The math is the issue. To self-insure the way a policy does, you would need enough set aside to replace years of income, pay off the mortgage, fund the kids through college, and cover final expenses, all at once, today. Almost nobody has that, and the people who do usually got there over decades. Life insurance exists precisely to bridge the gap between the savings you have now and the much larger sum your family would need if your income stopped early.

Think of it as leverage on your dollars during the years your family is most exposed. A modest monthly premium can control a six-figure death benefit, which is something no savings account can match in the early years when you have the most people depending on you and the least money saved. As your savings grow and your obligations shrink, you may genuinely need less coverage later, and that is fine. The point is that for most people, in the years that matter most, savings are the backup and insurance is the safety net, not the other way around.

There is a fair counterpoint, and it is the only honest one: if you have truly accumulated enough that your family could absorb the loss of your income, pay every debt, and fund every future cost from assets alone, you may be in a position to carry less coverage, or none. That is real, and it is worth checking the math rather than assuming it either way.

Myth 10: Term insurance is throwing money away

This myth runs in the opposite direction from the others. Instead of talking people out of coverage, it talks them into the wrong kind, or out of buying because they think term is a "waste" if they outlive it.

The truth: Term insurance does its job whether or not it ever pays a claim. You are buying protection for a defined window, usually the 20 or 30 years when your family depends on your income, your mortgage is large, and your kids are at home. If you outlive the term, that means the worst case did not happen and your family was protected the whole way. That is not wasted money any more than a year of car insurance with no accident is wasted. You paid for protection during the risk, and the risk passed.

The flip side of this myth is the belief that permanent insurance is always the better buy. Permanent policies like whole life or an indexed universal life policy can fit specific lifelong needs, build cash value, and serve estate or legacy goals. But they cost significantly more per dollar of death benefit than term, the cash value growth is not guaranteed in indexed products, and fees and structure matter a great deal. Permanent coverage is better for certain jobs and worse as a way to get the most death benefit for the least money. The right answer depends on what you need the policy to do, which is why our breakdown of term vs whole life insurance is a useful next read.

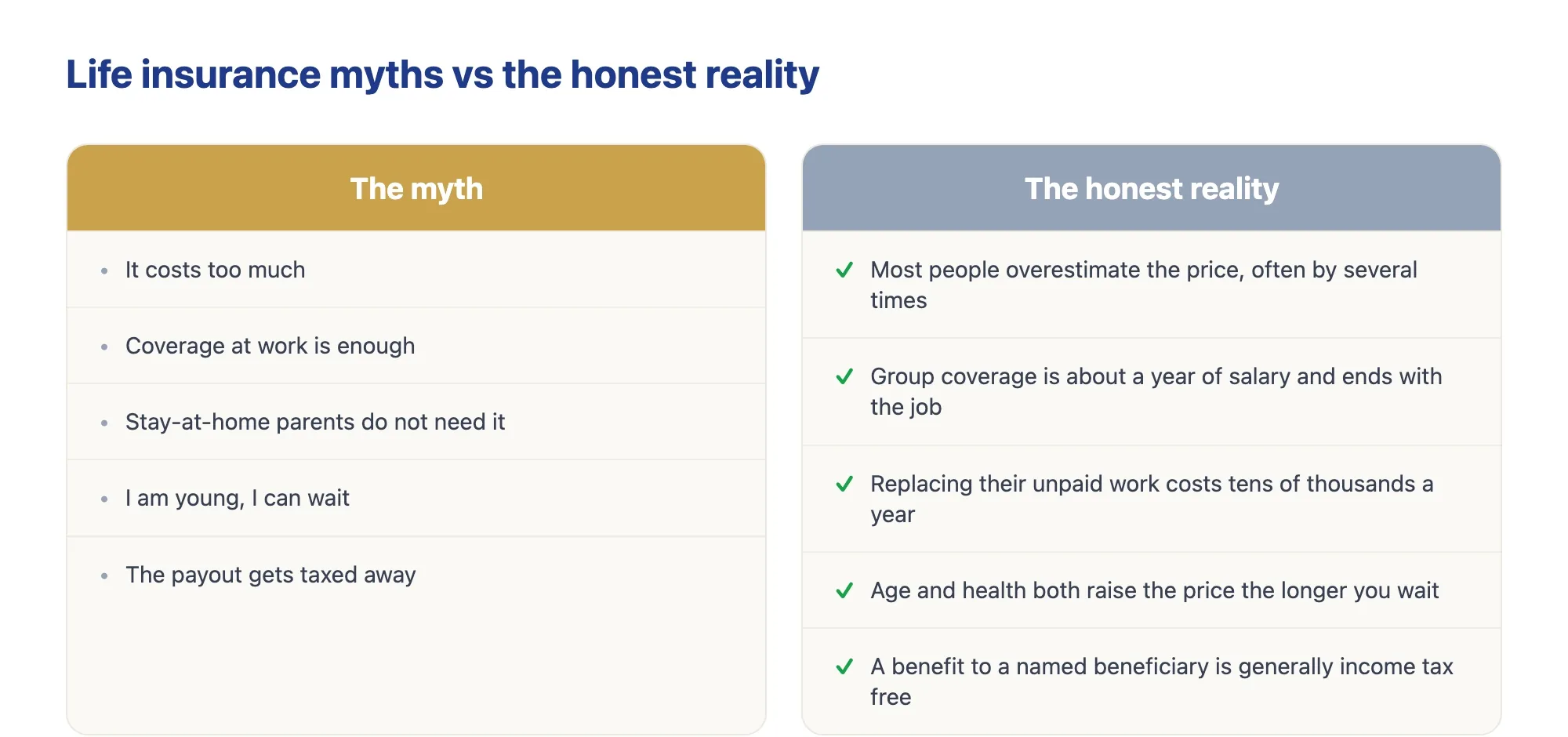

Quick reference: myth vs reality

If you only skim one part of this article, make it this. The table below puts each myth next to the short, honest version of the truth. The figures and ranges are general patterns to show direction, not a quote or an offer of coverage, and your real numbers depend on your age, health, coverage amount, state, and carrier.

| The myth | The reality |

|---|---|

| It costs too much | Most people overestimate the price, often by several times. A healthy young adult can frequently get meaningful term coverage for a small monthly amount. |

| Work coverage is enough | Group coverage is often about one year of salary and ends when the job does. It is a bonus, not a foundation. |

| Stay-at-home parents don't need it | Their unpaid work would cost tens of thousands a year to replace. Many families cover both parents. |

| I'm young, I can wait | Age and health both raise the price over time. Waiting forfeits the lowest rate you will ever qualify for. |

| I'm single, so I don't need it | Co-signed debt, shared loans, final expenses, and supported relatives can all outlive you. |

| The payout gets taxed away | A death benefit to a named beneficiary is generally not taxed as income, per IRS guidance, with limited exceptions. |

| My health disqualifies me | Many managed conditions are insurable. Health usually changes the price or policy type, not whether you can get covered. |

| Only the breadwinner needs it | Any death that creates a financial hole, including a second income or unpaid household work, is worth insuring. |

| My savings cover it | Few people have saved enough to replace income, clear debt, and fund the future at once. Insurance bridges that gap. |

| Term is a waste if I outlive it | Term protects the years your family is most exposed. Outliving it means the worst case never happened. |

Not sure which myths apply to you?

Give me 15 minutes. We will look at your real situation, your budget, and your actual number. No pressure, no jargon, no guessing.

Get a Quote Book a Free 15-Min Review Prefer to start small? Save my card or get a quick term life quote.How to replace a myth with a real number

Myths thrive in the absence of facts, so the antidote is a number that is actually yours. You do not need to become an insurance expert to get one. Here is the simple path I walk people through, and it usually takes one short conversation.

- Add up what would have to be paid. Start with the mortgage and any other debts, then add the income your household would lose for the years it depends on you, plus future costs like raising or educating children, plus final expenses. That total is the hole.

- Subtract what is already in place. Existing coverage, including any work policy, plus savings and other assets your family could use. What is left is the gap a new policy needs to fill.

- Match the term to the need. If the worry is the 20 years your kids are at home or the 30 years left on the mortgage, a level term policy that lasts that long usually does the job for the least money. If the need is lifelong, that is where permanent coverage earns a look.

- Get a real quote at today's age and health. This is the step that kills the cost myth for good. A quote costs nothing, and it replaces a scary guess with the actual price for your situation. There are even no-exam paths if a medical visit is what has been stopping you.

- Buy what you can keep. The right amount of coverage you can comfortably afford for the whole term beats a larger or fancier policy you cancel in two years. A lapsed policy protects no one, so build a premium that fits your budget today.

That is the whole method. Notice that none of it requires believing a sales pitch. It is just arithmetic and an honest quote, which is exactly what every myth on this list is designed to keep you from doing.

The pattern behind these life insurance myths

Step back and every one of these myths leads to the same place: a family or a loved one left covering a bill they did not see coming. The cost myth keeps people from asking. The work-coverage and savings myths give them false confidence. The single, breadwinner, and stay-at-home myths convince whole groups of people that the rules do not apply to them. The tax and health myths shrink coverage or stop applications that should have happened. Different stories, same ending.

Notice the common thread: each myth gives you permission to do nothing. That is what makes them so sticky. They are not just wrong, they are comfortable, because they confirm the easy choice. The cost of that comfort is paid later, by the people you were trying to protect, at the moment they can least afford it.

The fix is not to buy the biggest policy someone tries to sell you. It is to know your real number, get a real quote, and make the call with facts instead of guesses. Honest coverage planning means looking at honest trade-offs too: the right amount, the right type, and a premium you can actually keep paying, because a policy you cancel in two years protects no one.

If you want help sorting out which type fits your family, start with our breakdown of term vs whole life, and if a home loan is your main worry, the mortgage protection guide is a good next step. When you are ready for a straight answer about your own situation, you can find a real human and not a robot at Sovereign Life Group, your life insurance strategist.

Frequently asked questions

What is the most common life insurance myth?

That it costs too much. In the 2026 Insurance Barometer Study, most people overestimated the price of a basic term policy, and many guessed several times the real cost. A healthy young adult can often get meaningful term coverage for about the price of a couple of streaming subscriptions a month, though your real number depends on age, health, coverage amount, and carrier.

Is the life insurance I get through work enough?

Usually not on its own. Workplace coverage often equals one year of salary or a flat amount around $20,000, and it typically ends when the job does. Research has found that many households relying only on workplace coverage say their family would struggle financially within six months of losing a wage earner. Treat group coverage as a bonus and build a personal policy as the foundation.

Do stay-at-home parents need life insurance?

Yes, in most cases. The work a stay-at-home parent does, like childcare, transportation, and running the household, would cost real money to replace. Estimates put that value in the tens of thousands of dollars a year, so a policy helps the surviving parent pay for that help without choosing between a job and the kids.

Are life insurance payouts taxed?

Generally, a life insurance death benefit paid to a named beneficiary is not counted as taxable income. According to the IRS, proceeds are usually not included in the beneficiary's gross income. There are exceptions, such as interest paid on the benefit or certain estate situations, so it is worth confirming your specific case with a tax professional.

Can I get life insurance with a pre-existing condition?

Often, yes. A pre-existing condition may raise your rate or change which policies fit, but many common conditions, such as well-managed high blood pressure or diabetes, are insurable. Options range from fully underwritten term to simplified-issue and guaranteed-issue policies. The honest trade-off is cost and benefit size, not an automatic decline.

Should I wait until I am older to buy life insurance?

Waiting almost always costs more. Rates rise with age and can jump if your health changes. A level term rate locked in your late 20s or 30s is generally lower than the same coverage bought a decade later, and a new diagnosis in between can raise the price or limit options. Locking in young keeps the price low for the whole term.

Have a question that is not covered here? Reach out anytime. Straight answers, every time.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.