Life Insurance for Stay at Home Mom: Why You Need It Too

The Short Version

A stay-at-home parent does tens of thousands of dollars of unpaid work every year. If that parent passed away, the family would have to pay someone for childcare, cooking, cleaning, and driving, often while one income is gone. Life insurance for a stay at home mom covers that gap so the surviving parent is not forced to choose between a paycheck and the kids.

Here is a question most families never sit with: if the parent who runs the home did not come back tomorrow, who would do everything they do, and what would it cost? For most households, life insurance for stay at home mom coverage is the missing piece, because the unpaid work that holds a family together does not stop being valuable just because no paycheck is attached to it. The bills for replacing that work are very real, and they tend to arrive all at once.

There is a stubborn myth that only the "breadwinner" needs life insurance. It sounds logical. No income means no income to replace, right? But that logic misses what a stay-at-home parent actually produces every single day. In more than a few honest conversations, I've watched a couple realize mid-sentence that they had insured the paycheck and left the person running the whole household completely exposed. This guide walks through what that work is worth, how much coverage makes sense, what it costs, the honest trade-offs between the main options, and how a non-working spouse actually qualifies. No pressure and no jargon, just straight answers.

One quick note before we dig in: every word of this applies just as much to stay at home dads. More fathers run the household full time than ever, and the math does not care about gender. If you are the parent who handles the kids, the home, and the day to day so your spouse can work, your role carries the same financial value and deserves the same protection. We say stay at home mom throughout because that is how most families search for this, but read it as stay at home parent.

The myth that costs families the most

The most expensive belief in family finance might be this one: "We only need to insure the person who earns the money." It feels responsible. It feels like you are being practical with the budget. And it quietly leaves half the family unprotected.

Think about what actually happens in a household where one parent stays home. That parent is the childcare provider, the cook, the housekeeper, the driver, the nurse for sick days, the tutor, the scheduler, and the person who keeps the whole operation running while the other parent is at work. None of that shows up on a pay stub. All of it would have to be paid for if that parent were suddenly gone.

This is not a small or rare gap. According to research published by LIMRA, a large share of households say they would feel financial hardship within just a few months if a primary wage earner died, and the gap is even wider for non-earning spouses, who are frequently left uninsured entirely. The reason is simple: families insure the obvious income and forget the invisible labor.

So the real question is not "does a stay-at-home parent earn money?" The question is "if this parent were gone, what new bills would land on the surviving spouse, and could that spouse pay them while grieving and still working a job?" When you frame it that way, the answer gets a lot clearer.

No medical exam for a ballpark. Free, and no pressure.

A week in the life, and what it would cost to hire out

Before we talk dollars, it helps to slow down and actually watch a normal week. Not a dramatic one. Just an ordinary stretch of Monday through Sunday in a home with young kids and one parent at home. The work is so constant and so woven into the day that most families genuinely lose sight of how much of it there is.

Here is a rough picture. Wake-ups, breakfast, and getting little bodies dressed and out the door. Drop-off and pickup runs, sometimes two or three per day once you count school, preschool, and activities. Lunch and snacks. Naps and the negotiations around them. Doctor and dentist appointments. Grocery runs and meal planning so there is actually food in the house. Laundry that never fully ends. Cleaning up the same floor four times. Homework help at the table. Bath time, bedtime, and the middle-of-the-night wake-ups when a kid is sick. Somewhere in there, managing the calendar, the bills, the school forms, and the hundred small decisions that keep a household from falling behind.

Now imagine the surviving parent trying to hold a full-time job and cover all of that alone. It is not that they are unwilling. It is that the day does not have enough hours, and the money to hire help has to come from somewhere. When you break the week into its parts, the invisible labor stops being invisible. Every task on that list is something a family can, and often must, pay another person to do. That is the point the rest of this guide is built on.

What it costs to replace unpaid work

Let's put numbers on the invisible. When a stay-at-home parent passes away, the surviving parent usually cannot simply absorb all the household duties and keep working full time. Something has to give. Either they cut back at work and lose income, or they pay other people to do the jobs that used to be free. Both cost money.

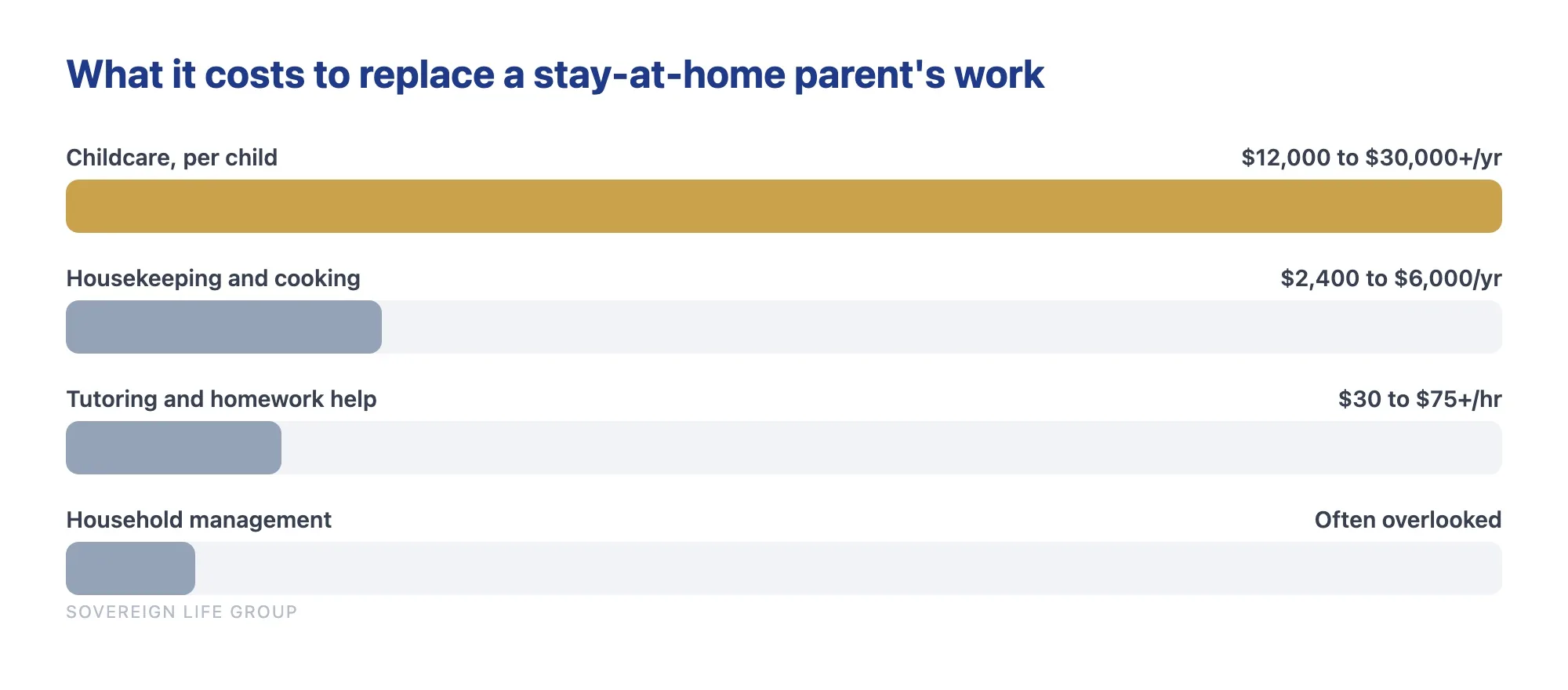

The phrase you will see in the industry is "replace unpaid work," and it is exactly what good coverage is built to do. Here is a rough, illustrative look at the kinds of roles a stay-at-home parent fills and what a family might pay to hire each one out. These figures are general national estimates for illustration, not quotes, and they vary widely by region and by how many children you have.

| Role the parent fills | What a replacement might cost | Why it adds up |

|---|---|---|

| Childcare | $12,000 to $30,000+ per year, per child | Full-time daycare or a nanny is the single biggest line item, especially for infants and toddlers. |

| Housekeeping and cooking | $200 to $500+ per month | Cleaning services and prepared meals replace hours of daily work. |

| Transportation | Hard to price | School runs, activities, and appointments often need a paid driver or after-care. |

| Tutoring and homework help | $30 to $75+ per hour | Academic support that used to happen at the table. |

| Household management | Often overlooked | Scheduling, bills, errands, and logistics still have to be handled by someone. |

One widely cited annual study from Salary.com has estimated that the combined "job" of a stay-at-home parent, if you paid market wages for every task, would be worth well over six figures a year. You do not have to take any single number as gospel to see the point: the work is not free to replace. It only feels free because one person in the family is doing it out of love.

Now stack one more reality on top. The surviving parent is also the one who must keep earning. They cannot quit their job to cover all of these new duties, because that paycheck is now the only one. So the family ends up paying for replacement help and trying to hold the income together. That is the squeeze that homemaker life insurance is designed to relieve.

Notice too that the biggest costs land exactly when a family is least able to shoulder them. Full-time childcare for an infant or toddler is the most expensive line item on the list, and it also runs for the most years. A family with a newborn is looking at a decade or more of paid care if the at-home parent is gone. That timing is why sizing coverage to the years your kids are young matters so much, which is the next thing we work through.

Life insurance for stay at home mom: what the coverage really protects

When people picture life insurance, they picture income replacement. Salary stops, a check arrives, the mortgage gets paid. For a stay-at-home parent, the math is different but no less important. Here, the coverage protects the surviving family from a wave of new costs and impossible scheduling, not from a lost salary.

A well-sized policy on a stay-at-home parent can give the surviving spouse the breathing room to:

- Pay for childcare so they can keep their job instead of being forced to step back at the worst possible moment.

- Take real bereavement time with the kids before returning to a full schedule, rather than rushing back to work out of pure financial necessity.

- Hire help for the cooking, cleaning, and driving that suddenly has no one to do it.

- Cover final expenses like a funeral and any medical bills, which on their own can run into the thousands.

- Keep the household stable for the children during a time when stability matters more than anything.

This is the same protective instinct behind coverage for the working parent, just pointed at a different risk. If you have already thought through life insurance for parents on the income side, this is the other half of the same plan. A family is not fully protected when only one of the two people raising the kids is insured.

There is also a quieter benefit that rarely gets mentioned: time. A death benefit does not just pay for services. It buys the surviving parent the ability to make decisions slowly instead of in a panic. Whether to move closer to family. Whether to change jobs to something with more flexibility. Whether to keep the kids in the same school so their world does not turn upside down all at once. Money cannot fix grief, but it can remove the second crisis that so often piles on top of the first one.

How much homemaker life insurance do you need?

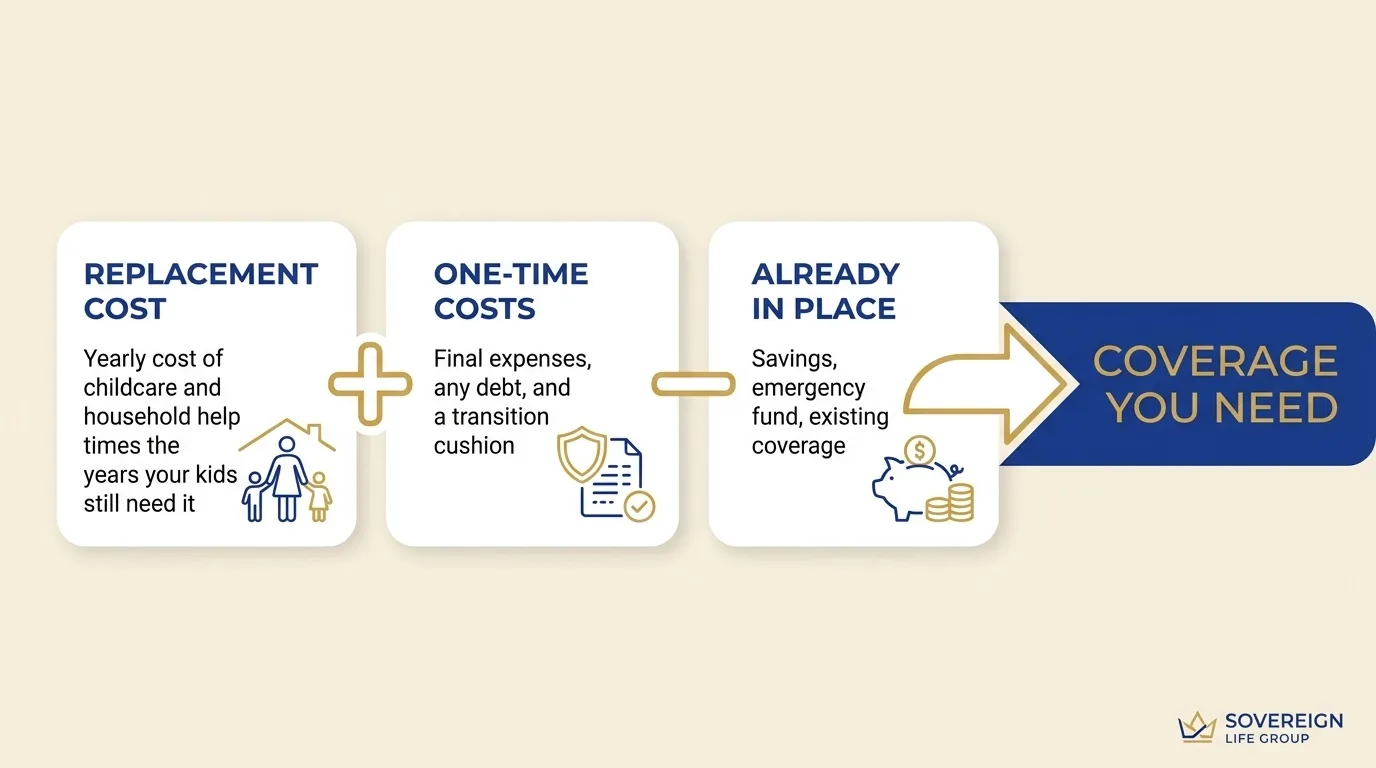

There is no universal number, and anyone who gives you one without asking questions is guessing. The honest answer is that it depends on your children, your debts, and how long the support would need to last. But here is a clear way to think it through.

Start with the replacement cost

Add up what it would realistically cost to hire out the work for the years your children still need it. If you have a toddler, that childcare bill could run for a decade or more. If your kids are teenagers, the window is shorter. Multiply the annual cost of help by the number of years you would want it covered.

Add the one-time costs

Layer in final expenses, any debt that would become a burden, and a cushion for the transition period. Even a modest amount here keeps the family from going into debt during the first hard year.

Subtract what is already in place

If there are savings, an emergency fund, or existing coverage that could help, factor that in. The goal is to fill the gap, not to over-insure.

For many families, this exercise lands somewhere in the range of $250,000 to $500,000 of coverage on the stay-at-home parent, though plenty of families need more or less. The point is to do the math for your own home rather than copy a number off the internet. If running these figures feels overwhelming, that is exactly the kind of thing a licensed agent can walk through with you in a few minutes.

The shortcut methods, and where they fall short

You will see two quick rules of thumb online. The first is a flat "income multiple," usually ten to twelve times income. That one does not translate cleanly to a stay-at-home parent, because there is no salary to multiply. The second is a fixed round number like $250,000 or $500,000 because it sounds sensible. Both can get you in the neighborhood, and honestly, a round-number policy bought today beats the perfect policy you never buy. But neither actually looks at your kids' ages or your real childcare costs, which are the two numbers that move the answer the most. A family with a newborn and a toddler has a very different need than a family whose kids are in high school. Use the shortcut to start the conversation, not to end it.

Two real-world examples, with numbers

Abstract advice is easy to nod along to and hard to act on, so let's walk through two made-up families to see how the math comes together. The numbers are illustrative, not quotes, and the details are composites rather than real clients.

Example one: young kids, long runway

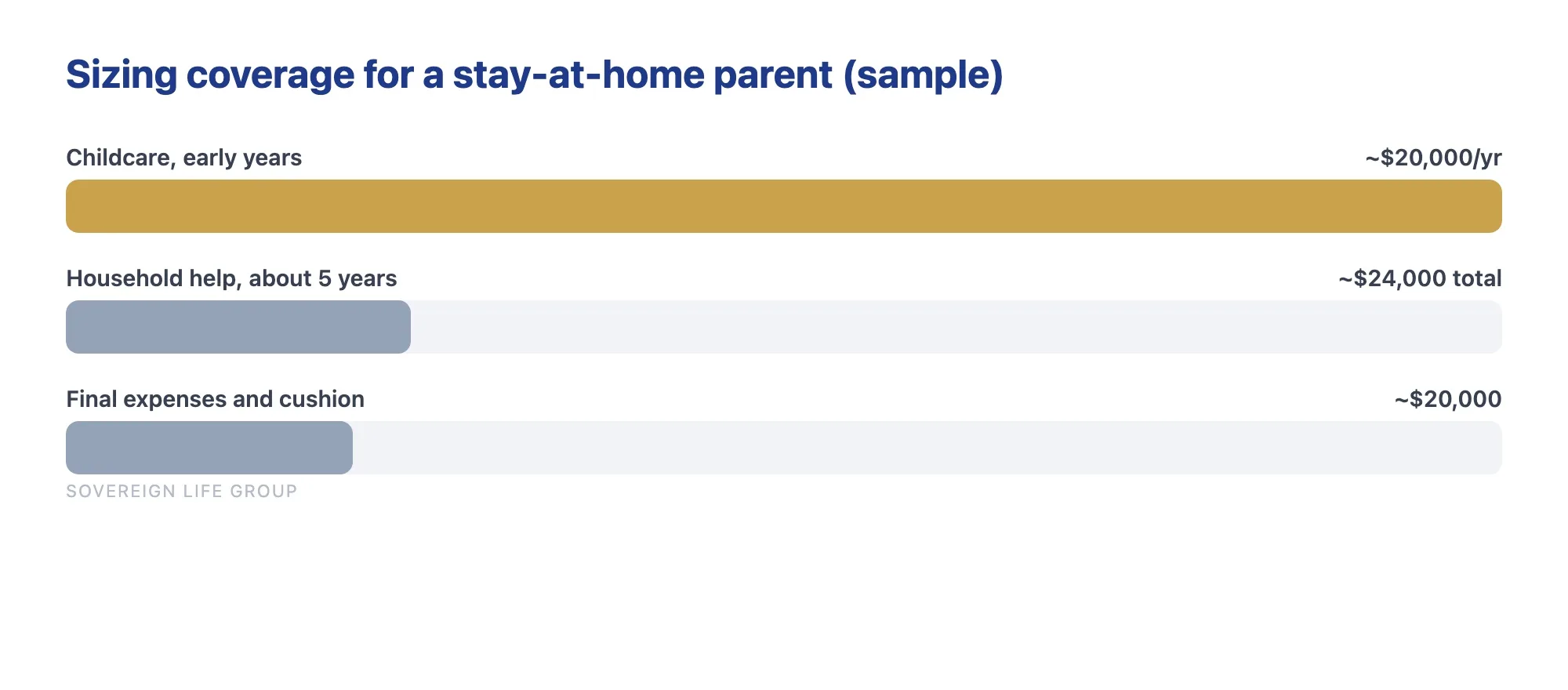

Picture a household with two children, ages 3 and 6. One parent works full time, and the other stays home. The working parent already has a term policy in place. The question is how much coverage to put on the stay-at-home parent.

Here is one reasonable way to size it:

- Childcare and after-school care: roughly $20,000 a year for two young children. The youngest is 3, so the family wants this covered for about 12 years until that child is more independent. That alone points toward a large multi-year need.

- Household help: say $400 a month, or about $4,800 a year, for cleaning and some prepared meals during the hardest stretch. The family decides to plan for 5 years of this.

- Final expenses and a transition cushion: roughly $20,000 to cover a funeral, any medical bills, and a few months where the surviving parent can step back from work.

You do not have to fully fund every year of every line item with insurance, because savings and the surviving parent's income still help. But even a conservative version of this picture, perhaps covering childcare for the early years plus the one-time costs, points many families toward something in the $250,000 to $400,000 range of coverage. A more cautious family that wants the full childcare window covered might choose more.

Example two: older kids, shorter window

Now picture a different family. The kids are 12 and 15, and the at-home parent has recently gone back to part-time work. The intense daycare years are behind them, so the childcare line item is smaller. But there is still a real need: several years of household management, driving to activities and jobs, homework and college-prep support, plus final expenses. This family might land closer to $150,000 to $250,000, and a shorter term, maybe 10 or 15 years, fits the runway better than a 30-year policy would.

The two examples show the same principle from opposite ends. Younger kids mean a bigger, longer need. Older kids mean a smaller, shorter one. Neither family needs zero coverage, which is the myth we started with. The exact figure is less important than the exercise. When you actually price out the work, the idea that a stay-at-home parent does not need coverage falls apart fast. These numbers are illustrative and will look different for your family, your region, and your number of children, which is exactly why a short conversation with a licensed agent beats guessing.

Types of stay at home parent coverage

Once you know roughly how much coverage you want, the next decision is what kind. There are two broad families of life insurance, and a couple of practical variations. None of them is universally "best." Each trades something for something else.

Term life insurance

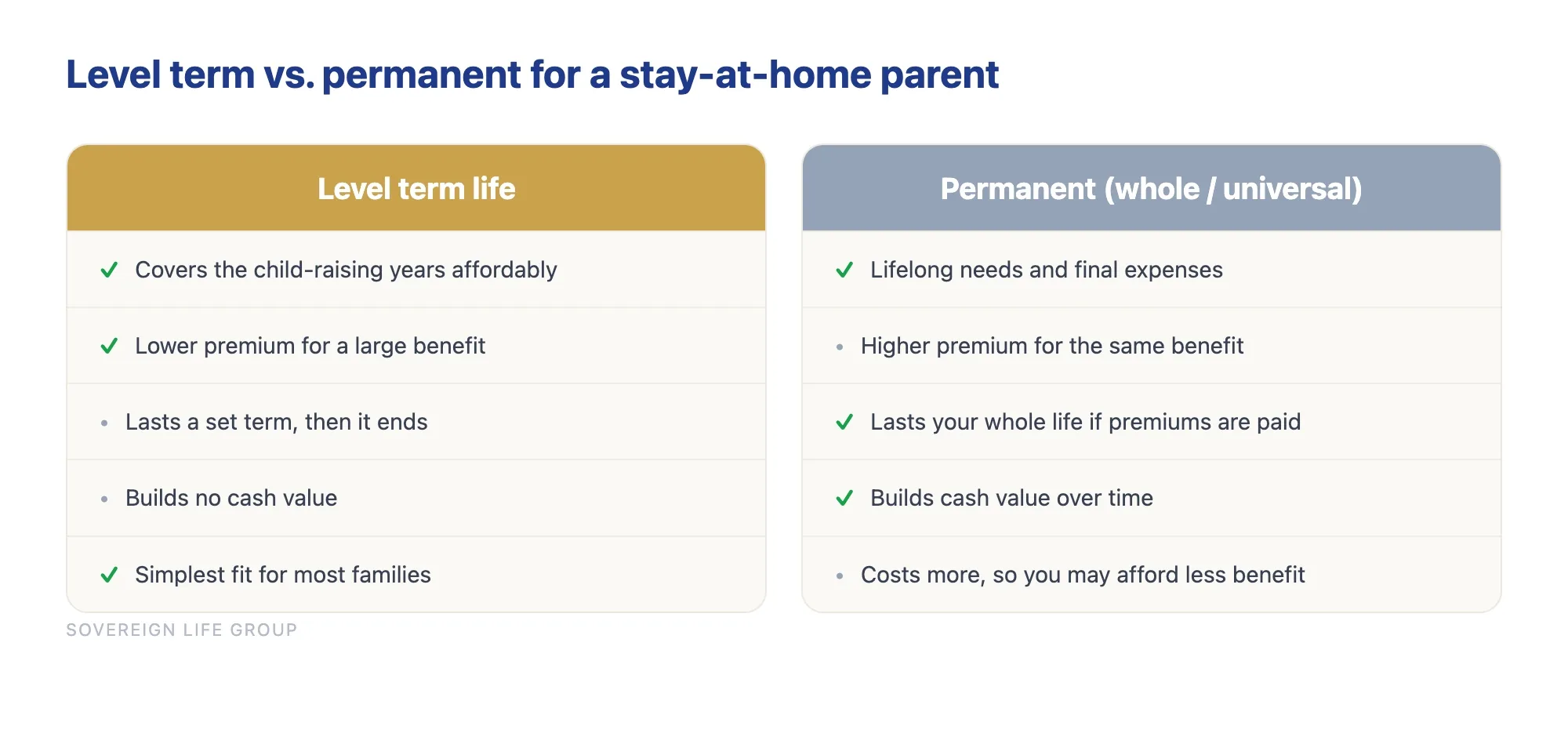

Term life covers you for a set number of years, often 10, 20, or 30. If you pass away during the term, it pays a benefit. If the term ends and you are still here, the coverage simply expires. It is the simplest and usually the most affordable option, which is why it fits so well for the child-raising years. For a deeper look at how term stacks up against permanent coverage, see our breakdown of term vs whole life insurance.

Permanent (whole or universal) life insurance

Permanent coverage is designed to last your whole life and can build cash value over time. It costs more than term for the same death benefit because it is doing more and lasting longer. Some families add a smaller permanent policy on top of term for lifelong needs or final expenses, while keeping the big coverage in affordable term.

No-exam coverage

Many carriers offer policies that skip the in-person medical exam and use health questions and data checks instead. Approval can be faster, which is appealing for busy parents. The trade-off is that coverage amounts may be capped and the price can differ from a fully underwritten policy. For a parent who has been putting this off precisely because scheduling a medical exam felt impossible with little kids underfoot, a no-exam path can be the thing that finally gets coverage in place.

The laddering approach

Some families use a simple technique called laddering, where you stack two or more term policies of different lengths. For a stay-at-home parent, that might mean a larger 15-year term to cover the expensive early childcare years and a smaller 30-year term underneath for the longer tail of household support. As the biggest need shrinks, the larger policy expires and your total premium drops, but you still have coverage in force. It is a way to match the coverage to the shape of the need instead of paying for a flat block of protection you do not need the whole time.

Here is how the main options compare for a stay-at-home parent:

| Feature | Level term life | Permanent (whole / universal) |

|---|---|---|

| Best for | Covering the child-raising years affordably | Lifelong needs and final expenses |

| Typical cost | Lower premium for a large benefit | Higher premium for the same benefit |

| How long it lasts | A set term, then it ends | Your whole life, if premiums are paid |

| Builds cash value | No | Yes, over time |

| Main trade-off | Coverage can expire before you want it to | Costs more, so you may afford less benefit |

For most stay-at-home parents, level term carries the heavy load because the biggest financial risk, paying for years of replacement help, is concentrated in the years the kids are at home. A good agent will sometimes tell you the simplest term policy is all you need, and that is a feature, not a sales failure. The job is to match the product to your situation, not to your agent's commission.

Get a fast, free estimate tailored to your age and health.

What it actually costs

Less than most people expect. Because a stay-at-home parent is usually insured for an amount tied to replacement costs rather than a large salary, and because many are relatively young and healthy, premiums tend to be modest. For a healthy parent in their 30s, a level term policy can often cost roughly the price of a few coffees a month. That is a general illustration, not a quote.

Your actual rate depends on a handful of honest factors:

- Age: younger generally means lower premiums, which is why waiting rarely pays off.

- Health: your medical history and current health influence the rate and whether an exam is required.

- Tobacco use: this typically raises premiums noticeably.

- Coverage amount and term length: more coverage for more years costs more.

- Policy type: permanent coverage costs more than term for the same death benefit.

No one can promise you a specific rate or guarantee approval before an application, and you should be skeptical of anyone who does. What an agent can do is shop your profile across carriers and show you real options. If you want to see how this fits alongside coverage for the working parent, our guide to life insurance for new parents walks through building a plan that covers both spouses together.

If the premium feels tight, there are honest ways to keep it manageable without leaving your family exposed. You can match the term length to the years your children actually need support rather than buying the longest term out of habit. You can right-size the coverage to your real replacement-cost math instead of an inflated round number. Some families also use the ladder approach described above, pairing a larger shorter term for the intense early childcare years with a smaller longer term underneath, so coverage steps down as the need shrinks. The goal is to protect the real risk at a price you can keep paying, because a policy only works if it stays in force.

How a non-working spouse qualifies

A common worry sounds like this: "Can you even buy life insurance on someone who does not earn an income?" The answer is yes, and it is routine. Two ideas explain how it works.

Insurable interest

To insure someone, you need what is called insurable interest, meaning you would suffer real loss if they passed away. Spouses have insurable interest in each other automatically. So a working spouse can absolutely take out a policy on a stay-at-home spouse. In practice, the at-home parent still applies and signs, since a policy is taken out with the insured person's knowledge and consent, but the working spouse is typically the owner and payer.

How much they will issue

Because there is no salary to anchor the coverage amount, carriers usually look at the working spouse's income and existing coverage to decide how much homemaker life insurance to offer. As a general guideline, they often want the working spouse to carry at least as much coverage as the non-working spouse, and sometimes more. This is normal underwriting, not a roadblock. It simply keeps coverage proportional across the household. If the working parent is underinsured or has no coverage at all, an agent will often suggest fixing that at the same time, so the whole plan is balanced.

The application itself looks much like any other: some health questions, possibly an exam or a no-exam path, and a decision. Honesty on the application matters. Misstating health or habits can cause problems at claim time, which is the worst possible moment for a surprise.

What the process actually looks like

Start to finish, applying is more ordinary than people expect. You pick a coverage amount and term, answer a set of health and lifestyle questions, and either complete a brief exam or take a no-exam route depending on the policy. The carrier reviews your answers, checks a few standard databases, and comes back with a decision and a rate. Fully underwritten policies can take a few weeks; some accelerated and no-exam options come back in days or even faster. None of it requires you to become an expert. A good agent handles the paperwork and translates the jargon.

A word for stay-at-home dads

The keyword says mom, but stay-at-home dads deserve their own paragraph, because they are often the most under-insured group of all. There are millions of fathers running the household full time now, and the same replacement-cost logic applies to them exactly. The childcare, the cooking, the driving, the household management, all of it costs the same to hire out regardless of which parent was doing it for free.

The reason dads get overlooked is usually a lingering assumption that life insurance is about replacing a paycheck, and if the dad is not bringing one in, people wrongly conclude there is nothing to insure. That is the same myth we opened with, just wearing different clothes. If you are a father at home with the kids while your spouse works, your role carries real economic value, and your family would face the same wave of new bills if you were gone. Size your coverage to the work you do, not to a salary you do not draw.

Common mistakes to avoid

A few patterns trip families up again and again. Knowing them in advance saves money and heartache.

- Insuring only the breadwinner. This is the big one. It leaves the family exposed to tens of thousands in replacement costs if the stay-at-home parent is lost.

- Buying far too little "just to have something." A tiny policy that does not cover even a year of childcare gives a false sense of security. Size it to the real need.

- Leaning only on employer coverage. A small group policy through the working spouse's job may extend a token amount to the other spouse, but it is usually far too little and it disappears if the job does. Treat it as a bonus, not the plan.

- Waiting until "later." Premiums are generally lowest when you are young and healthy. Health can change without warning, and so can eligibility.

- Believing the myths. A surprising number of families skip coverage based on ideas that are simply wrong. We cleared up several in our look at the most common life insurance myths that cost families money.

- Naming the wrong beneficiary or forgetting to update it. Review your beneficiary after any major life change, such as a birth or a move.

- Letting "perfect" block "done." A solid term policy in place today beats the ideal plan you never get around to buying.

Where this fits in your safety net

Life insurance for a stay-at-home parent is one important piece, but it works best as part of a larger plan. A policy pays a benefit, but it does not, by itself, decide who raises your children or how the money is managed. A few other pieces deserve attention at the same time.

- An emergency fund. Even a few months of expenses in savings gives the surviving parent breathing room before any claim is paid and reduces how much insurance has to do alone.

- A will and guardianship designation. This is where you name who would care for your children. Insurance funds the plan, but the will and guardianship decide the people. These belong together.

- Beneficiary setup. Make sure the policy names the right person, and consider how a benefit would be managed for the children's benefit if both parents were gone. An attorney can advise on trusts and similar tools.

- Employer coverage, with eyes open. Group life through a job is a nice extra, but it is often modest and usually does not move with you if you change employers. It rarely covers a non-working spouse at a meaningful level. Treat it as a supplement, not the whole plan.

One piece worth its own line: if the children are minors, life insurance money usually should not be left directly to them. Minors cannot control a large sum, and leaving it to them outright can trigger a court process and hand them the full amount the day they turn 18, which is rarely what a parent wants. Most families handle this by naming an adult custodian or setting up a simple trust, so the money is managed for the kids' benefit over time. This is a legal detail, not an insurance one, which is exactly why the policy and the paperwork around it should be built to agree with each other. Because some of these pieces are legal and tax matters, talk with a licensed professional about your specific situation rather than relying on a single article.

How to get started

You do not need to have everything figured out before you talk to someone. The process is more straightforward than most families expect, and it usually goes like this:

- Run the rough numbers. Estimate the annual cost of replacement help, multiply by the years you would want it covered, and add final expenses and any debt.

- Decide on a coverage length. For most families, a term that reaches until the youngest child is grown is the natural fit.

- Get honest options. A licensed agent can shop several carriers and show you real choices rather than one product. There is no obligation to buy.

- Apply. Answer the health questions truthfully, complete an exam if required (or choose a no-exam path), and review the offer.

- Put it in place and revisit it. Life changes. Check your coverage every few years or after any big event.

If you would rather not do this alone, that is exactly what we are here for. You can learn more about how we help households on our life insurance strategy page, or read more about protecting your household at every stage in our resources for families building a plan. This is general education and not financial, tax, or legal advice, so please talk with a licensed professional about your specific situation before you decide.

Frequently asked questions

Does a stay-at-home mom need life insurance if she has no income?

Yes, in most cases. A stay-at-home parent does real work the family would otherwise have to pay for, such as childcare, transportation, and household management. Life insurance for a stay at home mom replaces the cost of that unpaid work so the surviving parent is not forced to choose between earning a paycheck and caring for the kids.

How much life insurance does a stay-at-home parent need?

A common starting point is enough to cover several years of replacement childcare and household help, plus any debt and final expenses. Many families land between $250,000 and $500,000, but the right amount depends on the number and ages of your children, your debt, and how long the support would be needed. A licensed agent can help you run the numbers for your situation.

Can you buy life insurance on a spouse who does not work?

Yes. A non-working spouse can be insured as long as there is insurable interest, which a married couple has by definition. Carriers usually look at the working spouse's income and existing coverage to decide how much homemaker life insurance they will issue, since the policy is replacing economic value rather than a salary.

What type of life insurance is best for a homemaker?

For most families, level term life insurance covers the years children are at home for the lowest cost. Some families add a smaller permanent policy for lifelong needs. There is no single best product for everyone. The right fit depends on your budget, how long you need the coverage, and whether you also want cash value.

How much does life insurance for a stay-at-home mom cost?

For a healthy parent in their 30s, a level term policy on a stay-at-home mom often costs roughly the price of a few coffees a month, though your actual rate depends on age, health, coverage amount, and term length. Permanent coverage costs more because it lasts for life and can build cash value.

Can a stay-at-home parent get coverage with no medical exam?

Often, yes. Many carriers offer no-exam options that use health questions and data checks instead of a paramedical visit. Approval can be faster, though coverage amounts may be capped and rates can differ from a fully underwritten policy.

Find out what protecting your family would actually cost

Fifteen minutes. We will run the replacement-cost numbers for your home, look at your budget, and show you honest options for both parents. No pressure, no jargon.

Get a Quote Book a 15-Min Call Prefer to start small? Save my card or get a quick term life quote.Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life. This article is educational and not financial, tax, or legal advice. Product availability, features, and rates vary by state and carrier. Guarantees are subject to the claims-paying ability of the issuing insurance company. Please talk with a licensed professional about your specific situation.