Life Insurance for Parents: How to Protect Your Kids

The Short Version

Life insurance for parents replaces your income and your role if you are gone, so your kids can stay in their home, finish school, and grow up with the plan you wanted for them. Most young families need more coverage than they think, and term life usually buys the most protection for the least money during the years your children depend on you.

There is a question every parent quietly carries and almost nobody says out loud: if you did not come home tomorrow, would your kids be okay? Not emotionally. That wound never fully closes. I mean financially. Could your family stay in the house, keep the lights on, and keep your children pointed at the future you have been building for them?

That is the entire reason life insurance for parents exists. It will not bring you back, and it cannot replace you. What it can do is make sure your absence does not also cost your children their home, their school, and their stability all in the same brutal season. This guide walks through how much coverage a family really needs, what it costs, the honest trade-offs between term and whole life, the beneficiary and trust steps most people skip, and the special cases that trip parents up. No fear tactics, no jargon, no pressure. Just the straight version I would give a friend at my table.

What This Guide Covers

- Why life insurance for parents matters

- How much life insurance do parents need?

- Life insurance for new parents

- The stay-at-home parent nobody insures

- Types of policies for parents

- Term vs whole life for parents

- What coverage for young kids costs

- Riders worth knowing about

- Beneficiaries, guardians, and trusts

- Five mistakes parents make

- Single and divorced parents

- Should you insure your children?

- Your simple next steps

- Frequently asked questions

Why life insurance for parents matters more than most coverage

When you became a parent, a small group of people started depending on you in a way no one ever had before. Your paycheck buys their groceries. Your hours pay the mortgage that keeps a roof over their heads. Your presence handles a hundred quiet tasks a week that you never think about until they are gone. Life insurance for parents is simply a promise that those things keep happening even if you do not.

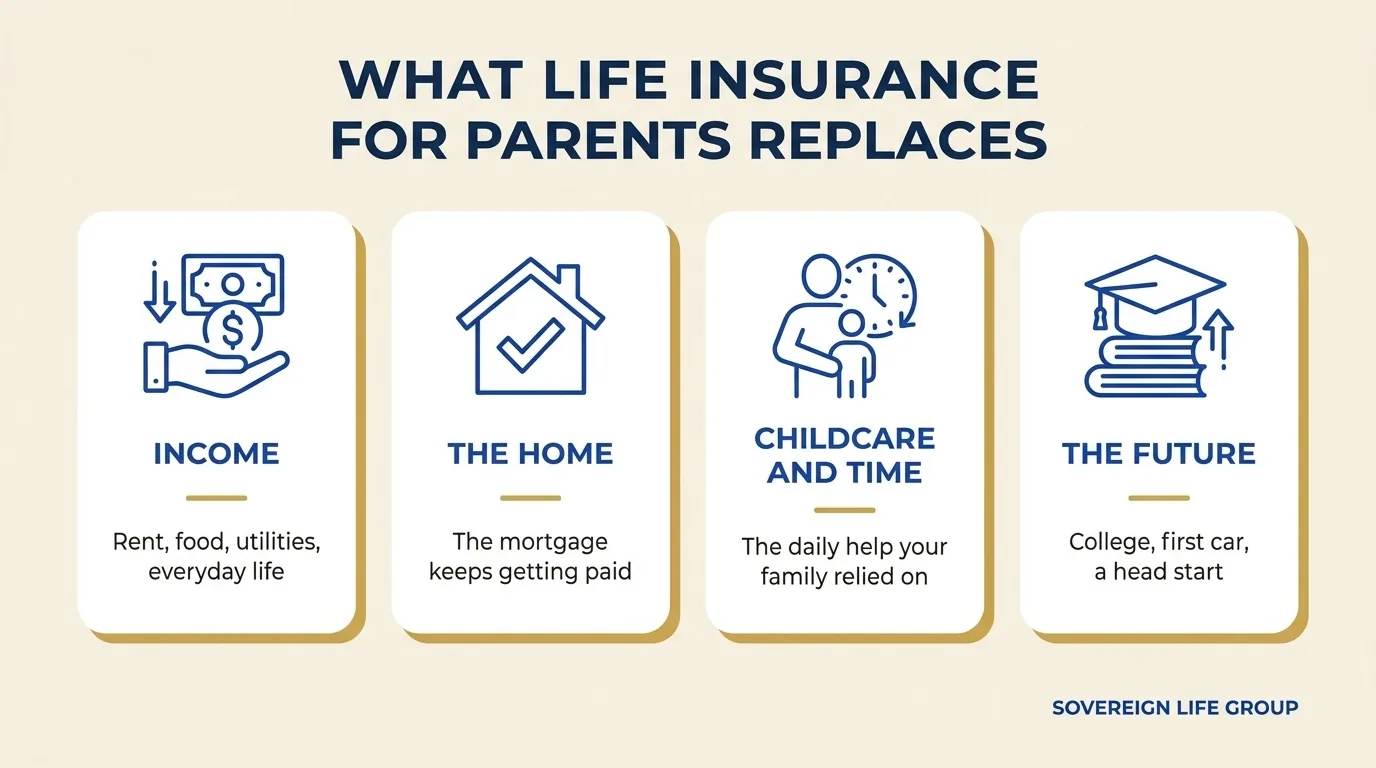

Think about what your family actually depends on you for. It is bigger than a single bill:

- Income. The salary that covers rent or mortgage, food, utilities, insurance, and the small extras that make childhood feel normal.

- The home. A house payment does not pause for grief. Without a plan, families often have to sell and move within a year, uprooting kids during the hardest moment of their lives.

- Childcare and time. If you are gone, someone has to do what you did. That often means paid help your spouse never had to budget for.

- The future. College, a first car, a wedding someday, the head start you always meant to give them.

A death benefit is money your family receives, generally income tax free, if you pass away while the policy is active. They can use it for any of the above, on their schedule, without asking a bank for permission. That flexibility is the whole point. It buys your family time and choices at a moment when they will have very little of either.

Here is the part people miss when they picture life insurance as a grim, morbid topic. In practice it is the opposite of morbid. It is the thing that lets a grieving spouse take a leave from work to be present for the kids instead of rushing back to a desk two weeks after a funeral. It is what keeps a fourth-grader in the same classroom, with the same friends, on the same soccer team, in a year when everything else in her world just changed. Money cannot fix grief. But the absence of money makes grief so much heavier, and that is the weight a policy lifts.

No medical exam for a ballpark. Free, and no pressure.

How much life insurance do parents need?

This is the question I hear more than any other, and the honest answer is "more than your job gave you, and probably more than you guessed." Many parents have a small policy through work and assume that covers it. It rarely does. Let's build a real number instead.

The simple starting point

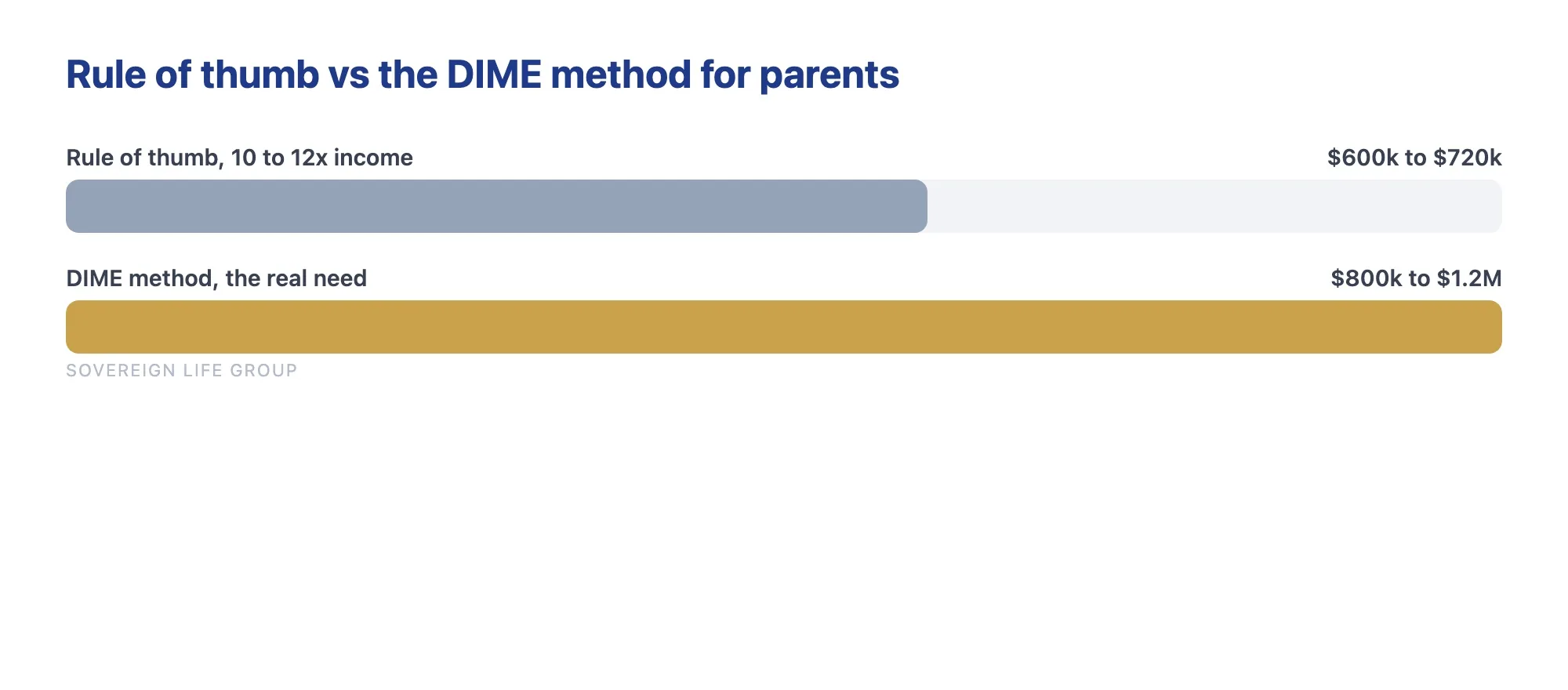

A common rule of thumb is 10 to 12 times your annual income. If you earn 60,000 dollars a year, that points you toward roughly 600,000 to 720,000 dollars of coverage as a baseline. The logic is that this amount, managed carefully, can replace your paycheck for the years your family needs it most. It is a starting line, not a finish line. The multiple is fast and it is easy to remember, but it ignores your actual mortgage, your actual debts, and how many years of childhood are still ahead of you. Two parents who both earn 60,000 dollars can have wildly different real needs if one rents with no kids at home and the other owes 300,000 dollars on a house with a newborn and a three-year-old.

The DIME method, which is more honest

A better approach adds up what your family would actually face. Insurance folks call it DIME, and it is just four buckets:

- D is for Debt. Add up credit cards, car loans, student loans, and any other balances that would not vanish.

- I is for Income. Multiply your yearly income by the number of years your family would need it, often until your youngest child is grown and independent.

- M is for Mortgage. Add the full balance remaining on your home, so the house can be paid off or kept comfortably.

- E is for Education. Add the estimated cost of getting your kids through school and into adulthood.

Total those four buckets, subtract any savings or existing coverage, and you have a number rooted in your real life rather than a generic multiple. For a deeper walk-through with examples, our guide on how much life insurance you actually need runs the math step by step.

Two sample families, side by side

Numbers make this real, so here are two composite households drawn from the kind of conversations I have every week. The figures are illustrative and rounded, not quotes.

| DIME bucket | The Rivera family (one income) | The Bennett family (two incomes) |

|---|---|---|

| Debt (cards, cars, student loans) | $28,000 | $15,000 |

| Income replacement | $55,000 x 18 years = $990,000 | $45,000 x 12 years = $540,000 |

| Mortgage balance | $265,000 | $190,000 |

| Education for the kids | $120,000 (two kids) | $70,000 (one kid) |

| Minus savings and existing coverage | Minus $40,000 | Minus $120,000 |

| Rough coverage need | About $1.36 million | About $695,000 |

Notice what drives the gap. The Riveras live on one income with two young kids and a bigger mortgage, so their family would need many years of replaced income and both kids raised on the death benefit. The Bennetts have a second earner, more savings, and one child closer to independence, so their need is real but smaller. Neither number is "right" in the abstract. Each is right for that family. That sounds like a lot of coverage until you price it, which we will get to below, because term life on a healthy young parent is usually far cheaper per dollar than people expect.

Life insurance for new parents: where to start

If a baby just arrived or is on the way, congratulations, and welcome to the club of people who suddenly care a lot about boring financial topics. Life insurance for new parents is one of the highest-value things you can set up early, for one simple reason: premiums are based largely on your age and health, and you will likely never be younger or healthier than you are right now.

Here is the order I suggest for new parents:

- Insure both parents. Even if one stays home, both play a role worth protecting. We cover the stay-at-home case in detail just below.

- Start with enough term coverage to carry the family for 20 to 30 years, long enough to get a newborn all the way to independence.

- Name your beneficiaries clearly, and think through how the money would be managed for minor children. Young kids cannot legally receive a large payout directly, so families often use a trust or a custodial arrangement. There is a full section on this below.

- Revisit it after big changes: another baby, a new home, a jump in income.

One thing I tell every expecting parent: do not wait for the baby to actually arrive to start. You can often apply while your spouse is still pregnant, and getting the paperwork moving before the sleepless newborn weeks hit is a gift to your future exhausted self. The cheapest policy is almost always the one you buy today rather than next year, because both your age and your health can only move in one direction from here.

New parents also tend to underestimate how long "dependence" really lasts. A newborn today is financially reliant on you through high school and, for most families, well into college and sometimes the first shaky years of adulthood. That is why a 20-year term can be too short for a brand-new baby. A 30-year term lines up much better with the real arc of raising a child from the crib to a first job. If you want a parent-specific deep dive on structuring coverage around a growing family, our dedicated page on life insurance for new parents goes further than we can here.

The stay-at-home parent nobody insures

Here is the gap I see most often. A family insures the working parent, looks at the stay-at-home parent, and thinks, "They do not earn an income, so they do not need coverage." That logic is understandable and expensive.

A stay-at-home parent is doing work that has a real market price, which is exactly why life insurance for a stay-at-home parent matters as much as a policy on the earner. If that parent passed away, the surviving spouse would suddenly be paying for childcare, after-school care, transportation, meal preparation, housekeeping, and the dozens of other things that were happening for "free." Many families discover that replacing a stay-at-home parent's labor would cost tens of thousands of dollars a year, on top of grieving and trying to hold down a job.

Run the arithmetic for a second. Full-time childcare for two young kids can run 20,000 to 40,000 dollars a year in a lot of the country. Add housekeeping, the driving, the meal planning, the sick days when someone has to stay home, and the number climbs fast. Now imagine the working parent trying to earn a living and personally cover all of that at the same time. It does not work without paid help, and paid help costs money the household never budgeted for.

For that reason, coverage of 250,000 to 500,000 dollars on a stay-at-home parent is a reasonable range for many families, and because that parent is often young and healthy, the premium tends to be modest. The goal is not to put a price on a person. It is to make sure the surviving parent can afford the help they would suddenly need, and can be present for grieving children instead of drowning in logistics.

Types of life insurance parents actually consider

Before we compare term and whole life head to head, it helps to know the small handful of policy types that come up for parents. You do not need to memorize the industry catalog. These are the ones that matter for a family:

- Level term life. Coverage for a set number of years at a fixed premium. The workhorse for parents, because it is affordable and it lines up with the child-raising window.

- Whole life. Permanent coverage that lasts your whole life and builds a guaranteed cash value. Costs more, but it never expires as long as premiums are paid.

- Indexed universal life (IUL). A flexible permanent policy whose cash value growth is tied to a market index with a floor and a cap. It is a specialized tool with real fees and moving parts, and the growth is not guaranteed. If cash-value strategies interest you, read our plain look at how an indexed universal life policy works before assuming it fits.

- Final expense whole life. Small permanent policies built to cover a funeral and final bills, usually bought by older parents and grandparents rather than young families. If you are looking into coverage for an aging mom or dad, our guide to life insurance for elderly parents walks through that situation in full.

- No-exam and simplified issue. Not a separate product so much as a faster path. Many carriers now approve healthy applicants without a medical exam, trading a possibly slightly higher rate for speed and convenience.

For the vast majority of parents raising kids, the real decision comes down to the first two, so let's put them side by side.

Term vs whole life for parents

Once you know roughly how much coverage you need, the next fork is what kind. Parents get pulled in both directions, often by people with an incentive to sell one over the other. Here is the plain version.

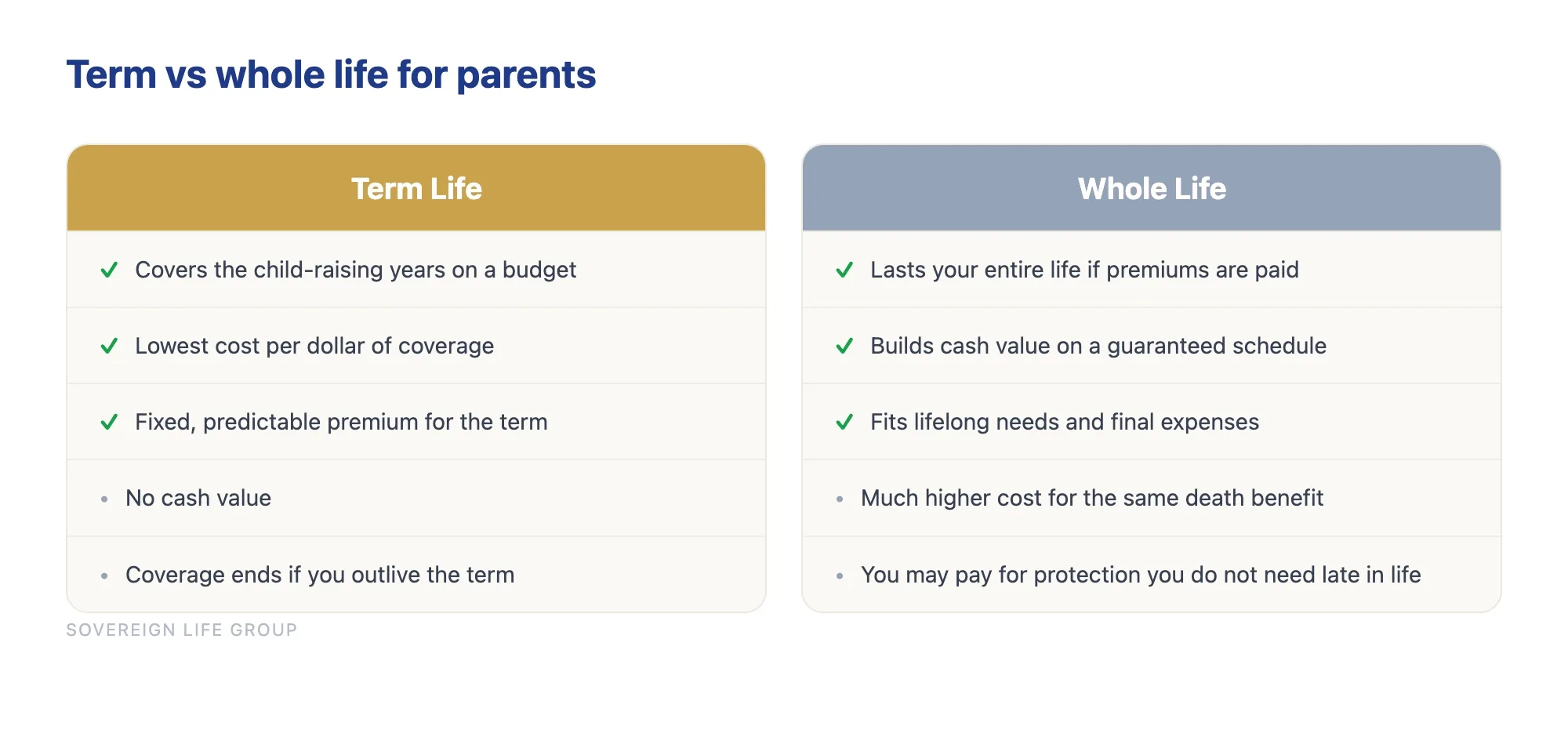

Term life covers you for a set number of years, say 20 or 30, for a fixed premium. If you pass away during the term, your family gets the death benefit. If you outlive the term, coverage ends. It is pure protection, which is why it costs the least. For a parent, a 20 or 30 year term can line up almost perfectly with the years your kids depend on you.

Whole life (a form of permanent insurance) covers you for your entire life as long as premiums are paid, and it builds a cash value over time that you can borrow against. It costs significantly more than term for the same death benefit because part of your premium funds that cash value and the lifelong guarantee.

| Feature | Term Life | Whole Life |

|---|---|---|

| Best for | Covering the child-raising years on a budget | Lifelong needs, final expenses, estate planning |

| How long it lasts | A set term (often 10 to 30 years) | Your entire life, if premiums are paid |

| Relative cost | Lowest cost per dollar of coverage | Much higher for the same death benefit |

| Builds cash value | No | Yes, slowly, on a guaranteed schedule |

| Premium | Fixed and predictable for the term | Fixed, but higher |

| The trade-off | Coverage ends; no payout if you outlive it | You pay more for protection you may not need late in life |

For most parents on a budget, the math favors buying a large term policy and investing the difference into retirement accounts or college savings. A big term policy protects your kids during the exact window they need it, and it leaves more money in your monthly budget to actually raise them. That is not the right answer for everyone, but it is the right starting point for many young families.

That said, whole life and other permanent policies have a real place: covering a lifelong dependent such as a child with special needs, locking in coverage for someone with health changes on the horizon, or building a small guaranteed foundation alongside a large term policy. Many families use a blend, a large term policy for the income-replacement years plus a smaller permanent policy for the needs that never expire. If you want to go deeper on the differences, our breakdown of term vs whole life insurance lays out who each one tends to fit. The key is that a good agent shows you the honest trade-offs rather than steering you toward whatever pays the biggest commission.

Get a fast, free estimate tailored to your age and health.

What coverage for young kids actually costs

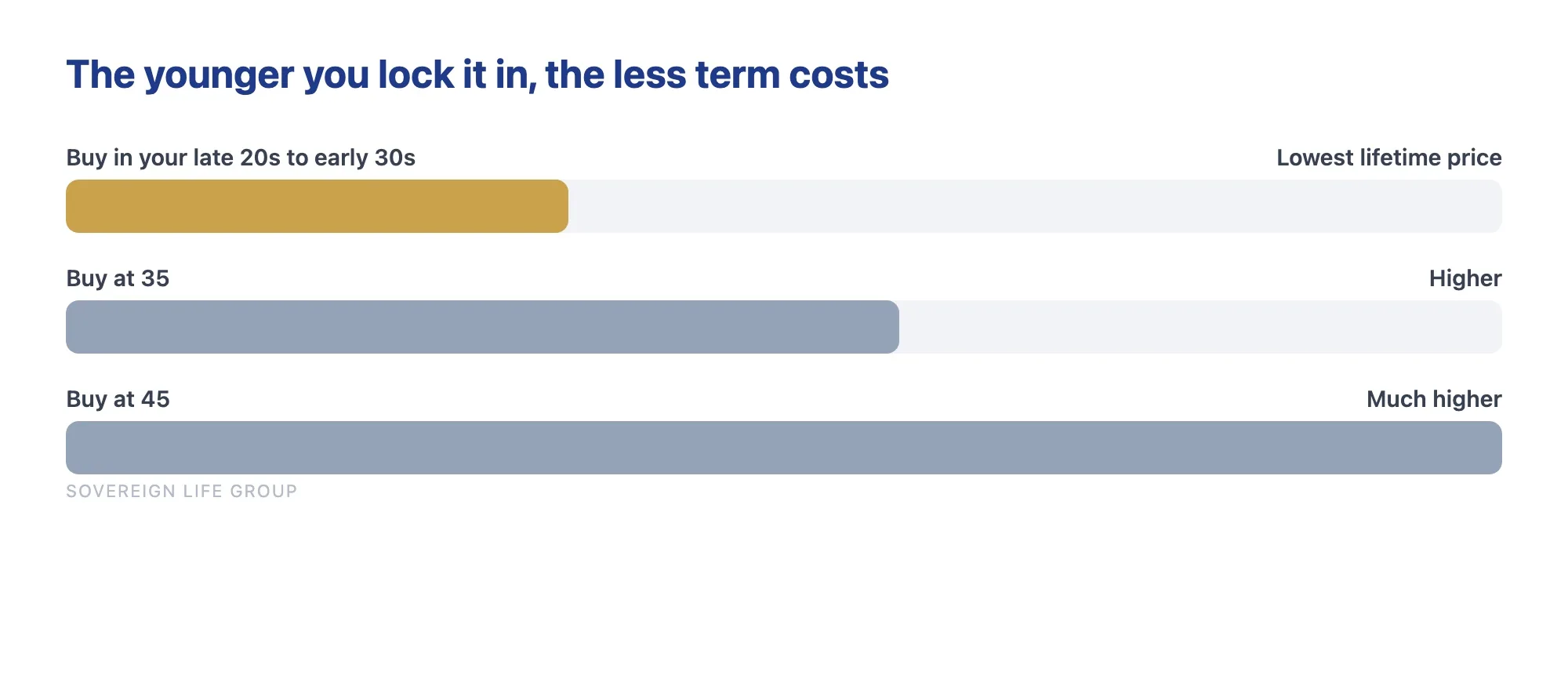

This is where parents usually exhale. Protecting young kids with a solid term policy tends to cost a lot less than people fear, especially when you buy while you are young and healthy. Your actual premium depends on your age, health, tobacco use, the coverage amount, and the term length, so the only way to know your real number is to get quoted. But the pattern is consistent: the younger and healthier you are, the cheaper it is to lock in coverage for decades.

The relationship is simple to picture:

- Age: A parent in their late 20s or early 30s generally pays far less than the same coverage bought at 45. Every year you wait tends to nudge the price up.

- Health: Better health usually means a better rate. Conditions can still be covered, often at a fair price, especially with the right carrier.

- Tobacco: Smoking raises rates meaningfully. Many parents quit and requalify later at a lower rate.

- Coverage amount and term: More coverage and longer terms cost more, but the per-dollar price of term life is low enough that going bigger is often surprisingly affordable.

According to industry research from LIMRA, a large share of Americans either have no life insurance or know they do not have enough, and many overestimate the cost by a wide margin. Surveys have found that people routinely guess term life costs several times what it actually does. The fix for that is not guesswork. It is a quick, no-obligation quote based on your real situation, which often comes in below what families budgeted for a single streaming bundle.

Here is a mindset shift that helps parents commit. Do not think of the premium as a monthly bill you are grudgingly paying. Think of it as the price of a promise, spread over years, that your kids keep their home and their future no matter what happens to you. Framed that way, a modest monthly amount to guarantee a six or seven figure safety net is one of the highest-leverage dollars a young family will ever spend.

One honest caveat: there is no single policy that is the smartest fit for every family, and no agent can promise you the lowest rate without knowing your health. The carrier that offers a healthy 30 year old a friendly rate may not be the one that treats a parent with a health condition fairly. Pricing varies by carrier and by state, which is exactly why comparing options with someone who can shop several carriers matters more than chasing a headline rate online.

Riders worth knowing about

A rider is an optional add-on that customizes a base policy. Most cost little or nothing, and a few are genuinely useful for parents. You do not need all of them, but it is worth knowing they exist so you can ask.

- Waiver of premium. If you become disabled and cannot work, this keeps your policy in force without you paying premiums. For a family living on that income, it protects the protection itself.

- Accelerated death benefit. Often included at no extra cost, this lets you access part of your own death benefit early if you are diagnosed with a qualifying terminal or chronic illness. It can help a family manage costs during a hard diagnosis rather than waiting until after.

- Child rider. A small amount of coverage on your children, added to your policy for a modest flat cost. It covers final expenses in the unthinkable case and, just as importantly, can lock in their future insurability. More on children's coverage below.

- Term conversion. The right to convert a term policy into permanent coverage later without a new medical exam. This is a quiet but powerful option for a young parent, because it protects your ability to keep coverage even if your health changes during the term.

- Spousal rider. A way to add some coverage on a spouse to the same policy. Often two separate policies serve a family better, but the rider can be a simple starting point.

Riders are where a good agent earns their keep, because the right one or two can matter a great deal and the rest are just noise. Ask which are included for free, which cost extra, and which actually fit your situation. Do not let anyone talk you into a pile of riders you do not need, and do not skip the one or two, like conversion and waiver of premium, that genuinely protect a young family.

Beneficiaries, guardians, and money for minor children

This is the step parents skip most, and it is one of the most important. Buying the policy is only half the job. Making sure the money lands in the right hands, managed the right way, is the other half.

You cannot leave a large sum directly to a young child

A minor child usually cannot legally receive and manage a large life insurance payout. If you simply name your six-year-old as the beneficiary, a court may have to appoint someone to oversee the money, which is slow, public, and not always who you would have chosen. The fix is straightforward, but it takes a little planning.

Three common ways families handle it

- Name an adult you trust. Some parents name a responsible spouse or co-parent as the primary beneficiary, with the understanding they will use it for the kids. Simple, but it relies entirely on that person and offers no structure.

- Use a custodial account (UTMA/UGMA). You can direct funds to a custodian who manages the money for the child until they reach adulthood under your state's rules. Easy to set up, though the child gains full control at a relatively young age.

- Set up a trust. A trust lets a trustee manage the money for your child's benefit and release it on terms you choose, for example some at 25, more at 30, rather than a lump sum the moment they turn 18. This is the most control, and it is worth a conversation with an estate attorney, especially for larger death benefits.

Name a guardian, and keep the forms current

Deciding who would raise your children and who would manage the money for them are two separate choices, and they do not have to be the same person. The most organized parent is not always the most loving guardian, and vice versa. Name both deliberately in your will, and revisit it after any big life change. And please, check your beneficiary form after a marriage, a divorce, or a new baby. An outdated form is one of the quiet tragedies of this business, because the policy pays exactly who is named, even if that is an ex-spouse you never meant to leave it to.

Five mistakes parents make with coverage

After enough honest conversations, the same avoidable mistakes show up again and again. Here are the ones to sidestep.

1. Relying only on the policy from work

It is usually too small and it leaves with the job. Own a policy that does not depend on your employer, so a layoff or a job change never leaves your kids exposed.

2. Insuring far too little

A 50,000 dollar policy feels like "doing something," but it would not cover a mortgage, let alone replace years of income. Size the policy to the actual job it has to do, using DIME rather than a round number that feels comfortable.

3. Skipping coverage on the stay-at-home parent

As covered above, that parent's daily work would cost real money to replace. Leaving them uninsured is a quiet gap that hurts later.

4. Waiting for the "right time"

Health can change without warning, and age only moves one direction. The right time for most parents was a year ago. The second-best time is now, because today you are almost certainly younger and healthier than you will be at renewal.

5. Forgetting to update beneficiaries

After a divorce, a remarriage, or a new baby, an outdated beneficiary form can send money to the wrong person. Review it whenever life changes, and confirm it matches your will.

Single parents and divorced parents

If you are raising kids on your own, life insurance is not optional, it is the safety net your children would otherwise live without. There is no second income in the house to fall back on. A policy is what stands between your kids and a sudden, total loss of support.

A few things matter especially for single and divorced parents:

- Choose a guardian and a money manager. Decide who would raise your children and who would manage the money for them. They do not have to be the same person, and naming them deliberately is one of the most loving things you can do.

- Use a trust or custodial setup for minors. A large payout should not land directly in a young child's lap. A simple structure lets a trusted adult manage it for their benefit until they are grown.

- Coordinate with any court orders. Divorce agreements sometimes require a parent to carry life insurance for the children's benefit. Make sure your coverage actually satisfies what was agreed, and that the named beneficiary matches it.

- Do not assume your ex's policy is enough. Carry your own. Your kids deserve protection from both directions, and you control your own policy in a way you never control someone else's.

Single parents also carry a mental load that two-parent households can split, and that is exactly why the structure matters so much here. There is no backup plan built into the household, so the policy and the paperwork around it have to be the plan. If you want to see how we think about protecting households like yours, our overview for families and the coverage they rely on is a good next read.

Should you insure your children too?

Parents often ask whether they should buy a policy on their kids. It is a fair question, and the honest answer is: it can be worthwhile, but it comes after protecting the parents who provide the income, not before.

A small child policy or a child rider added to a parent's policy does two useful things. First, it can cover the unthinkable costs of a child's final expenses, which no parent wants to imagine but which exist. Second, and more practically, it can guarantee your child's future insurability. If your child later develops a health condition, a policy locked in during childhood generally stays in force and can often grow with them, regardless of what their health does later.

That said, a child does not earn an income, so a child policy is not about income replacement. It is a small, optional layer. Be cautious of anyone who pitches a child policy as an investment or a college-savings vehicle, because there are usually more efficient tools for those specific goals. Make sure both parents are properly covered first, then consider a modest child policy if it fits your budget and goals. It is a nice-to-have built on top of a must-have.

Your simple next steps

If this feels like a lot, here is the whole thing boiled down to a short path you can actually follow this week.

- Step 1. Run a rough number using DIME, or use our calculator-style guide on figuring out how much coverage you need.

- Step 2. Decide your starting structure: for most parents, a large 20 or 30 year term policy on each working or caregiving adult.

- Step 3. Get quoted across multiple carriers so you are comparing real options, not a single rate.

- Step 4. Name your beneficiaries and set up how the money would be managed for minor children.

- Step 5. Put a reminder to revisit your coverage after any major life change.

You do not have to figure this out alone, and you should not be pressured into the biggest policy in the room either. The goal is the right amount of the right kind of coverage for your family, at a price you can actually keep paying for decades. If you want a second set of eyes, you can learn more about our approach to family life insurance at Sovereign Life Group or simply book a short, no-pressure review below.

Frequently asked questions

How much life insurance do parents need?

A common starting point is 10 to 12 times your annual income, then add the mortgage balance, any debts, and the future cost of raising and educating your kids. A parent earning 60,000 dollars a year with a young family often lands somewhere between 500,000 and 1 million dollars of coverage. The right number depends on your debts, your spouse's income, and how many years your children still depend on you.

Can I get life insurance for my elderly parents?

Yes, you can buy life insurance on a parent, but you need two things: their consent and what is called insurable interest, meaning you would face a real financial loss when they pass, such as funeral costs or shared debt. Your parent signs the application and usually answers a short health questionnaire. For older parents, final expense whole life is the most common fit because it is easy to qualify for and covers burial and end-of-life costs. Our full guide to life insurance for elderly parents walks through the whole process step by step.

How do you buy life insurance on a parent?

Your parent has to agree and take part in the application, since you cannot insure someone without their knowledge. You are typically the owner and the beneficiary, while your parent is the insured. Have their date of birth, health history, and current medications ready. For most aging parents, a final expense policy is the simplest path, with coverage sized to cover the funeral and final costs.

Should stay-at-home parents have life insurance?

Yes. A stay-at-home parent provides childcare, transportation, meals, and household management that would cost real money to replace. If that parent passed away, the surviving spouse would likely need to pay for childcare and other help. Coverage of 250,000 to 500,000 dollars is a reasonable range for many families, and the premium is usually modest.

Is term or whole life better for parents?

For most parents on a budget, level term life covers the years your kids depend on you for the lowest cost, which frees up money to actually raise them. Whole life costs more but lasts your whole life and builds cash value. Many families use a large term policy for the child-raising years and a smaller permanent policy for lifelong needs. The best fit depends on your budget and goals.

When should new parents buy life insurance?

The best time is before or right after a baby arrives, while you are young and healthy. Premiums are based largely on age and health, so locking in coverage early generally means a lower rate for the life of the policy. Waiting rarely makes coverage cheaper.

Does life insurance through my job cover my family enough?

Usually not on its own. Employer coverage is often one to two times your salary and ends if you leave or lose the job. It is a helpful supplement, but most parents need an individual policy they own and control to fully protect their children.

Can I get life insurance for my children too?

Yes. Child life insurance or a child rider on a parent's policy can lock in a small amount of coverage and guarantee your child's future insurability regardless of later health issues. It is optional, and protecting the parents who provide the income usually comes first.

Want a straight answer for your family?

Fifteen minutes. We will look at your income, your mortgage, and the simplest way to make sure your kids are protected. No pressure, no jargon, no upsell.

Get a Quote Book a 15-Min Call Prefer to start small? Save my card or get a quick term life quote.Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life. This article is educational and not financial, tax, or legal advice. Coverage availability, features, and rates vary by state, carrier, age, and health, and any coverage is subject to underwriting approval. Please talk with a licensed professional about your specific situation. Guarantees are subject to the claims-paying ability of the issuing insurance company.