Life Insurance With Pre-Existing Conditions Explained

The Short Version

A health condition almost never makes you uninsurable. It usually changes your price and which policy type fits, not whether you can get covered at all. Controlled diabetes, treated high blood pressure, and many other common conditions still qualify for real coverage, and for more serious situations there are simplified-issue and guaranteed-issue options that no one can turn down for health. The single biggest mistake is assuming you will be denied and never applying.

If you have ever been told, or quietly assumed, that a diagnosis closes the door on coverage, this article is written for you. The truth is that life insurance with pre-existing conditions is not only possible, it is ordinary. Millions of people who live with diabetes, high blood pressure, a past cancer, a heart event, depression, or a long list of other health conditions carry life insurance right now. Your condition is a factor in the math, not a verdict on whether you deserve protection for the people who count on you.

I write this as a licensed agent who places this kind of coverage for a living, not as a marketer trying to scare you into a quick decision. Some of what follows will set realistic expectations about price, and some of it will probably relieve a worry you have carried for years. Both are the point. Let us walk through what a pre-existing condition actually means to an insurer, the policy options on the table, how specific conditions like diabetes and high blood pressure are viewed, a real worked example, and the practical steps that get people approved at the best rate their health allows.

What this guide covers

- What counts as a pre-existing condition

- Can you get life insurance with pre-existing conditions?

- How underwriters actually read your health

- Your policy options when you have a condition

- Life insurance for diabetics

- High blood pressure life insurance

- Other common health conditions

- A real worked example

- How to improve your odds and your rate

- The mistake that actually gets people denied

- Why an independent agent matters here

- Frequently asked questions

What counts as a pre-existing condition

A pre-existing condition is simply any health issue you already have, or have had, before you apply for a new policy. That is a wide net, and on purpose. It includes the conditions you would expect and many you might not think to mention.

- Chronic conditions like Type 1 or Type 2 diabetes, high blood pressure, high cholesterol, asthma, or thyroid disorders.

- Heart and circulatory history such as a past heart attack, a stent, atrial fibrillation, or a stroke.

- A cancer history, whether you are in active treatment or years past remission.

- Mental health conditions like depression, anxiety, or bipolar disorder.

- Lifestyle and weight factors including obesity, a high body mass index, or sleep apnea.

- Past or present substance use, including tobacco, and a history of alcohol or drug treatment.

Here is the part most people get wrong. They lump every one of these into a single bucket marked "problem," when underwriters do almost the opposite. To an insurer, a pre-existing condition is a set of details: what it is, when it started, how severe it is, how well it is controlled, and what your records show over time. A diagnosis on paper and a well-managed condition in real life are treated as two very different risks, even when the label is identical.

No medical exam for a ballpark. Free, and no pressure.

Can you get life insurance with pre-existing conditions?

Yes. In the large majority of cases, you can get life insurance with pre-existing conditions, and often with better terms than you would guess. The question is rarely "will any company cover me," because for nearly everyone the answer is some form of yes. The real questions are which policy type fits your situation, which carrier views your specific condition most kindly, and what the coverage will cost.

That distinction matters because the fear of a flat rejection keeps people from ever applying, and not applying is the only guaranteed way to stay uninsured. Insurers are in the business of taking on measured risk, not avoiding it. A condition that is documented and stable is exactly the kind of risk they know how to price. Even when a fully underwritten policy is not the right path, simplified-issue and guaranteed-issue products exist so that almost no one with a health history is truly shut out.

It is worth clearing away a related myth while we are here, because it stops a lot of good people from picking up the phone. Plenty of folks believe coverage is unaffordable or that they will be denied on the spot, and both beliefs are usually wrong. If that sounds like the story in your head, our piece on the most common life insurance myths that cost families money is a useful companion to this one.

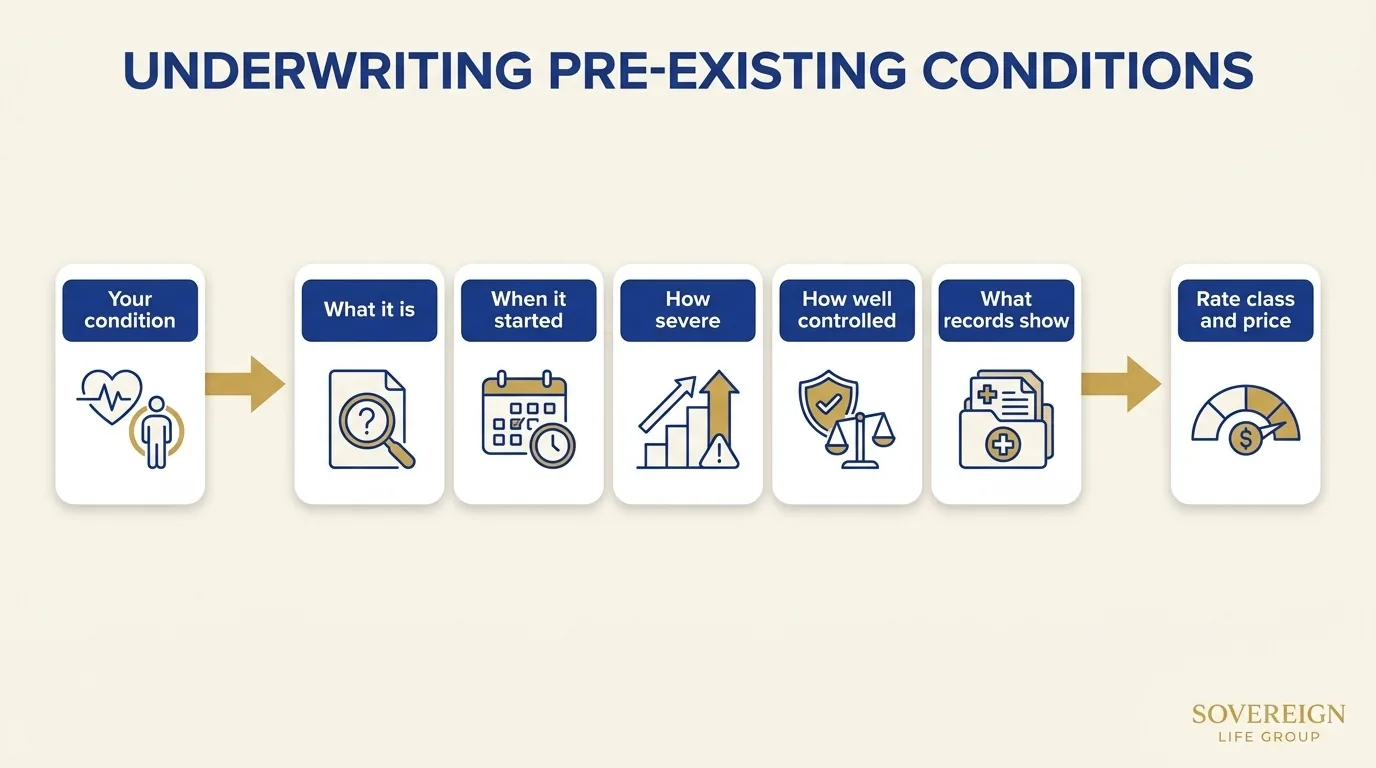

How underwriters actually read your health

To understand your options, it helps to see the process the way the insurance company does. When you apply for a fully underwritten policy, an underwriter builds a picture of your risk from several sources: your application answers, a possible medical exam, your prescription history, a database of past insurance and motor-vehicle records, and sometimes your actual medical records from your doctor. They are not hunting for a reason to reject you. They are sorting you into a rate class.

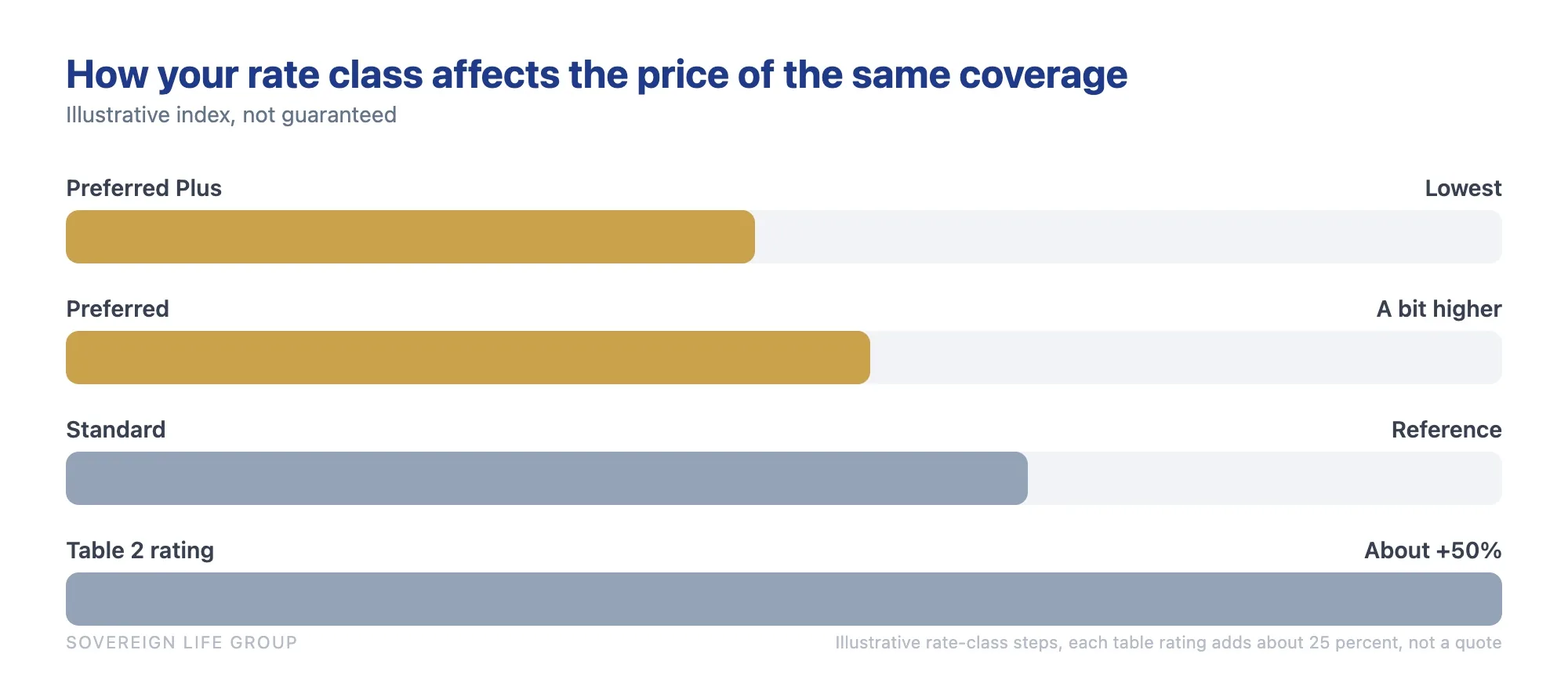

Rate classes, in plain terms

Most carriers use a ladder of health classes. The names vary slightly between companies, but the structure is consistent. Better health sits at the top with the lowest price, and as risk rises you move down the ladder to a higher price for the same benefit.

- Preferred Plus (sometimes Preferred Elite): excellent health, ideal numbers, no concerning history. The lowest rates.

- Preferred: very good health with maybe one minor, well-controlled item.

- Standard Plus and Standard: average health, common conditions kept in check. This is where a great many people with a pre-existing condition land, and the price is reasonable.

- Substandard, also called a table rating: a measurable health risk that is still insurable, priced above standard in steps.

What a table rating really means

This is the piece almost no consumer article explains clearly, so it tends to sound scarier than it is. When your risk is higher than standard but still insurable, the underwriter assigns a table rating, expressed as a number or a letter. Each step adds a set percentage to the standard premium, commonly around 25 percent per table. So a "Table 2" or "Table B" offer is roughly standard pricing plus about 50 percent, not double or triple what you imagined. A table rating is an offer of coverage, not a rejection. Many people who expect to be turned away instead receive a table-rated offer they can comfortably afford.

| Rate class | Who tends to land here | Relative price |

|---|---|---|

| Preferred Plus | Excellent health, no real history | Lowest |

| Preferred | Very good health, one minor item | Slightly higher |

| Standard | Common, well-controlled conditions | Moderate |

| Table rating (substandard) | A measurable but insurable risk | Standard plus steps |

| Simplified or guaranteed issue | Serious conditions or quick approval needed | Higher per dollar of benefit |

Two practical truths fall out of this ladder. First, the same person can be offered different classes by different carriers, because each company weighs conditions on its own schedule. Second, an offer that is not Preferred is still a real, usable offer. The goal is not always the top of the ladder. The goal is solid coverage in force at a price your family can keep paying.

Your policy options when you have a condition

There is no single product called "life insurance for people with conditions." Instead there is a menu, and the art is matching the product to your health and your goal. Here are the four paths that cover almost everyone, from the most thorough to the most forgiving.

Fully underwritten term or whole life

This is the traditional route, with a health questionnaire and usually a medical exam, and it is worth weighing how no-exam and traditional life insurance compare before you decide. It takes the longest and asks the most questions, and in exchange it offers the most coverage for the lowest price when you qualify. For a controlled condition, this is frequently the smartest choice, because the insurer can see the full, reassuring picture of a managed diagnosis rather than guessing. Do not assume your condition rules this out. It often does not.

Simplified issue

Simplified-issue policies skip the exam and ask a short set of health questions. Approval is faster, often days instead of weeks, and the trade-off is a higher price per dollar of benefit and lower maximum coverage amounts. This path suits someone whose condition would complicate a full exam, or who simply wants coverage in place quickly. If the needle or the wait is what has stopped you, our guide to no-exam life insurance and how it works walks through exactly when skipping the exam is the right call and when it is not.

Guaranteed issue

Guaranteed-issue policies ask no health questions at all and cannot decline you for health. They are the safety net for serious conditions. In return, the benefit amounts are smaller, the price per dollar is the highest of the group, and they almost always include a graded death benefit: if you pass away from natural causes within the first two or three years, the policy refunds your premiums plus interest rather than paying the full benefit. After that waiting period, the full benefit applies. For final expenses and a guaranteed yes, this product does an important job. Veterans with a service-connected disability have a parallel guaranteed-acceptance path in VALife, which our guide to life insurance for veterans walks through in detail.

Group coverage through work

Many employers offer a base amount of group life insurance with little or no health screening. It is a genuine benefit and worth taking, but treat it as a supplement, not your whole plan. It usually ends when the job does, and the amount is often modest. Building your own policy that you own and control is how you make sure your coverage does not depend on staying at one employer.

| Path | Health questions | Best fit | Trade-off |

|---|---|---|---|

| Fully underwritten | Full questionnaire and usually an exam | Controlled conditions, want the most coverage per dollar | Takes longer, more questions |

| Simplified issue | A few health questions, no exam | Want speed, or an exam is a barrier | Higher price, lower limits |

| Guaranteed issue | None | Serious conditions, need a guaranteed yes | Small benefit, waiting period |

| Group through work | Little or none | A free or cheap supplement | Ends with the job, often modest |

Life insurance for diabetics

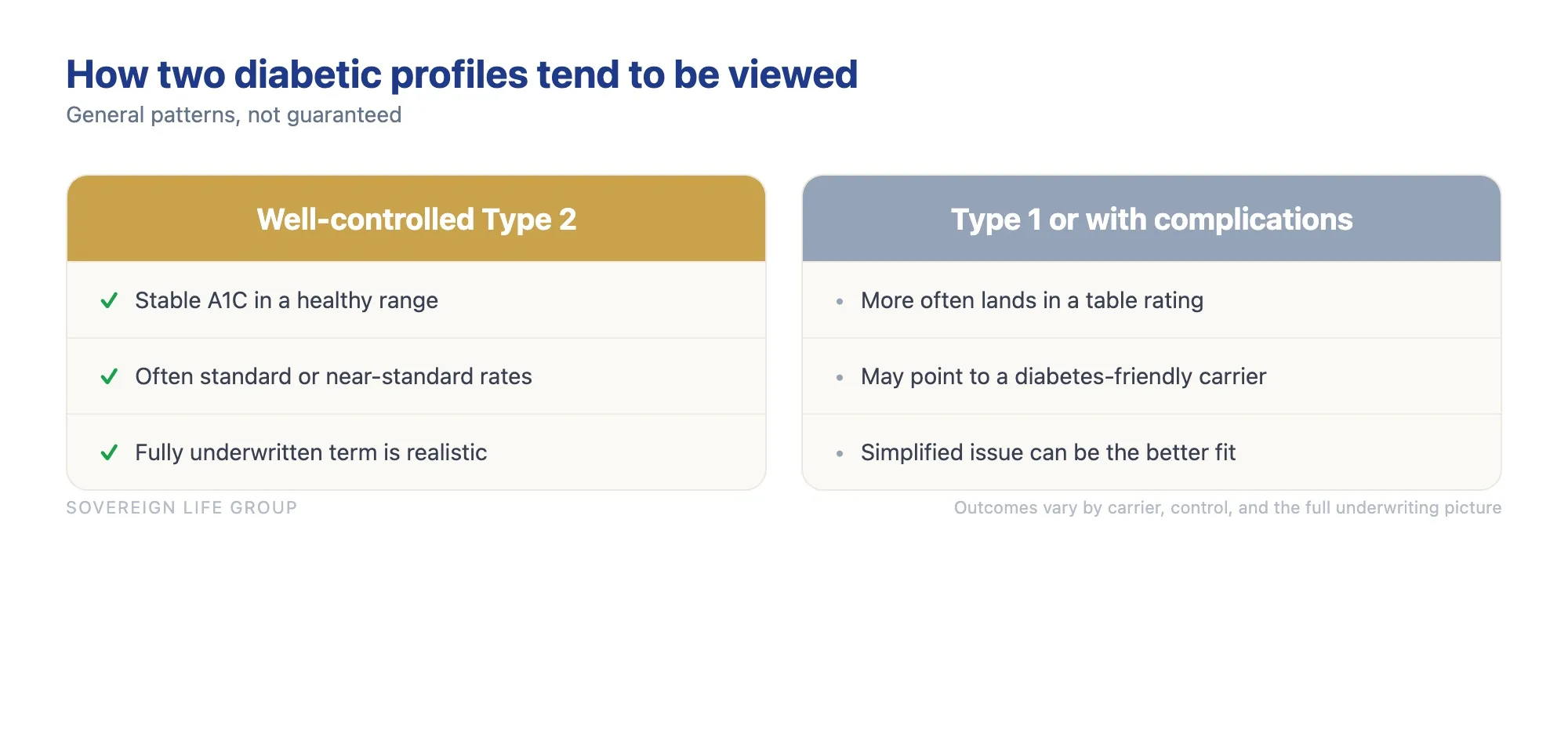

Diabetes is one of the most common pre-existing conditions in life insurance applications, and one of the most misunderstood. Many diabetics assume they are limited to expensive last-resort policies. In reality, life insurance for diabetics spans the entire menu above, and a well-managed diabetic often qualifies for far better terms than expected.

Underwriters look closely at a handful of specifics. The type of diabetes matters: Type 2, especially when controlled with diet, exercise, or oral medication, is generally viewed more favorably than Type 1. Your age at diagnosis matters, since a diagnosis later in life is often seen as lower risk than one in childhood. And your control matters most of all, measured largely by your A1C, the test that reflects your average blood sugar over roughly three months.

What helps a diabetic application

- An A1C in a healthy, stable range, documented over time rather than a single recent reading.

- No diabetes-related complications such as neuropathy, kidney issues, or eye disease.

- Regular care: routine checkups, follow-through on medication, and notes that show you manage the condition.

- Healthy companion numbers, since blood pressure, cholesterol, and weight all feed into the same risk picture.

A person with well-controlled Type 2 diabetes and otherwise good health can sometimes reach standard or near-standard rates on fully underwritten coverage. Type 1 diabetes, or diabetes with complications, more often lands in a table rating or points toward a diabetes-friendly carrier or a simplified-issue policy. None of these outcomes is a closed door. They are different rooms in the same house. Because carriers underwrite diabetes so differently from one another, this is a condition where shopping multiple companies pays off more than almost any other.

High blood pressure life insurance

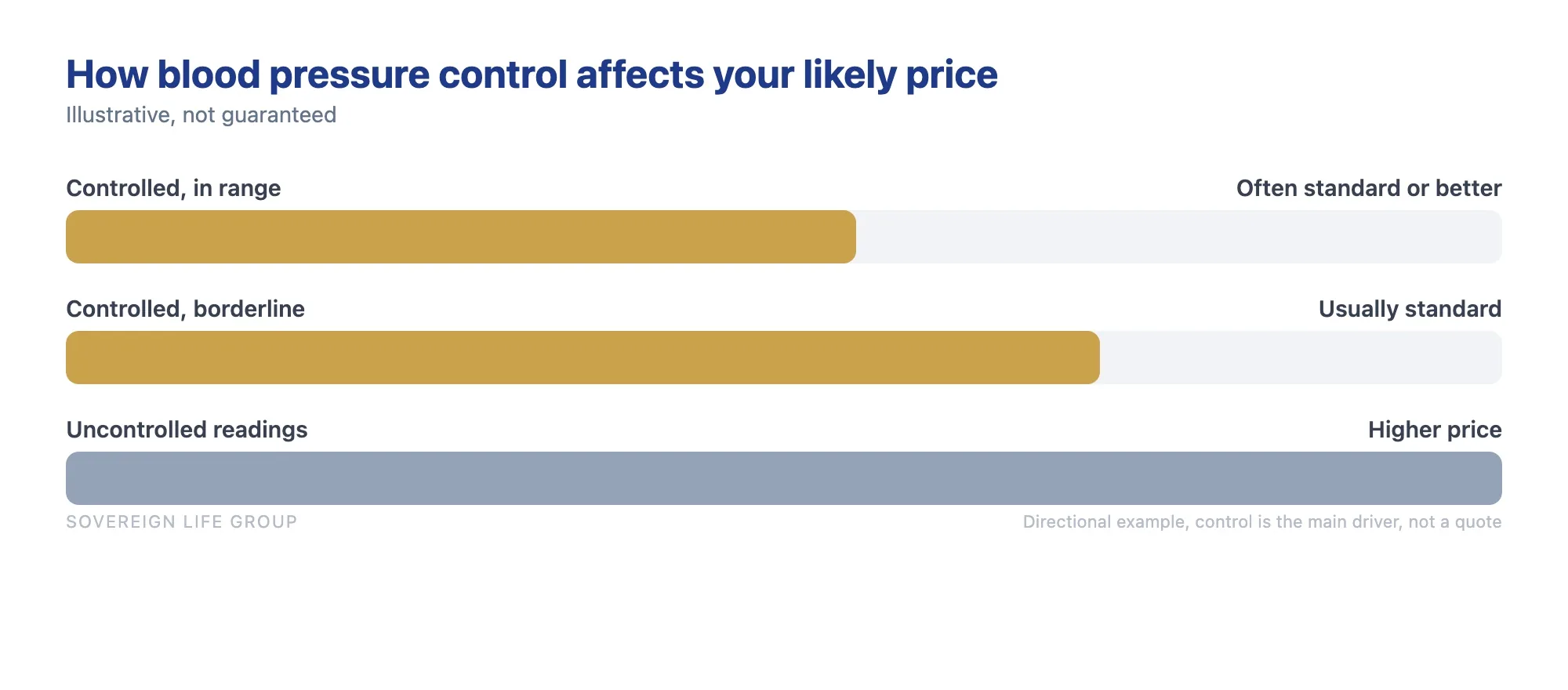

If diabetes is the most misunderstood condition, high blood pressure is the most over-worried. Hypertension is extremely common, very well understood by underwriters, and frequently one of the easiest conditions to insure well. Many people with treated high blood pressure still qualify for standard or even better rate classes, because controlled hypertension is a low-drama risk from the insurer's point of view.

The deciding factor is control. High blood pressure life insurance pricing leans heavily on whether your readings sit in a healthy range and whether they stay there. Being on medication is not a strike against you. If anything, a record of treated, stable readings reassures the underwriter that the condition is managed. Untreated or poorly controlled blood pressure, or readings paired with other heart-risk factors, is what raises the price.

What helps a high blood pressure application

- Readings consistently in a healthy range, with a recent set on file.

- Steady, documented use of any prescribed medication.

- No related complications, and clean companion numbers on cholesterol and weight.

- Honesty about the diagnosis even when your numbers are now normal, since the history is verifiable and disclosure works in your favor.

The takeaway is encouraging: for a great many applicants, high blood pressure barely moves the needle on price once it is controlled. It is a textbook example of why a managed condition and an unmanaged one are different risks even under the same name.

Get a fast, free estimate tailored to your age and health.

Other common health conditions

The same logic applies across most of the conditions that send people searching for answers. Severity, control, time since the event, and documentation drive the outcome, which matters even more in jobs that require passing a medical to keep working, like life insurance for truck drivers. Here is a quick tour of how several common conditions tend to be viewed. For a broader, condition-by-condition reference that goes deeper than we can here, see our overview of life insurance for common health conditions.

- High cholesterol: very insurable when controlled, much like blood pressure. A good ratio of total to HDL cholesterol can matter as much as the raw number.

- Heart disease: highly individual. A single event years ago with strong follow-up care looks very different from recent or ongoing problems. Time and stability help.

- Cancer history: the type, stage, and years since treatment ended drive everything. Many cancer survivors qualify for fully underwritten coverage once they are far enough past treatment; others use simplified or guaranteed issue in the meantime.

- Mental health: well-managed depression or anxiety is commonly insurable at good rates. Underwriters look at stability, treatment, and any history of hospitalization rather than the diagnosis alone.

- Sleep apnea: often a modest factor when treated, for example with consistent use of a CPAP machine. Untreated apnea, especially with related conditions, weighs more.

- Obesity or high BMI: a common factor that interacts with other numbers. Even a modest, sustained improvement in weight can move you to a better class.

Notice the pattern threaded through every one of these: the insurer is asking the same questions. How serious is it, how well is it managed, how long has it been stable, and can your records prove it. Answer those well, with documentation behind you, and most conditions become a question of price rather than possibility.

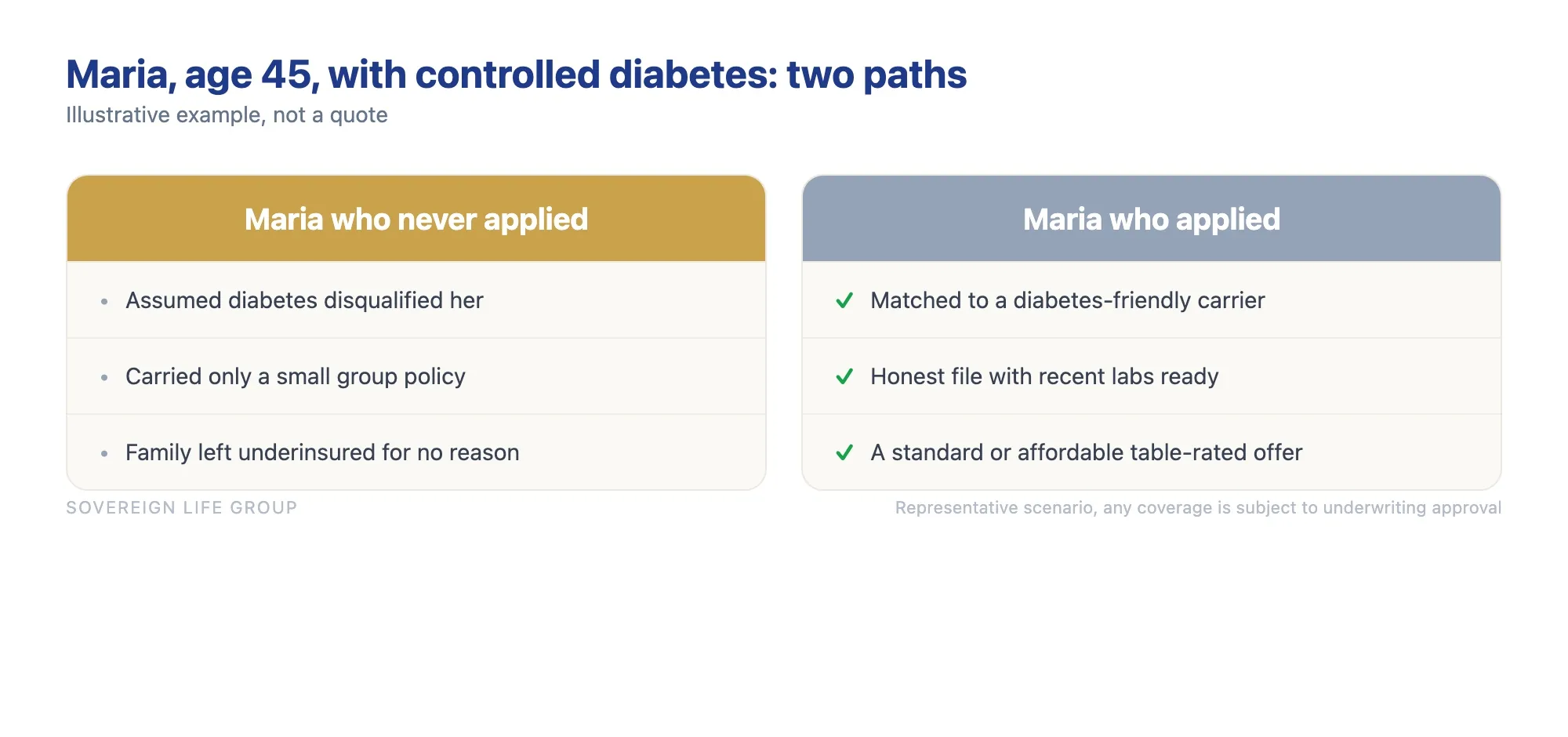

A real worked example

Numbers make this concrete in a way bullet points cannot, so here is a representative example. The figures are illustrative and rounded to show how the process unfolds. They are not a quote, and your own outcome depends on your full picture and on underwriting approval.

Picture Maria, age 45, a working mother of two with a 20-year mortgage and a teenager headed for college. She has Type 2 diabetes diagnosed four years ago, controlled with one oral medication and a steady A1C in a healthy range. She also takes a medication for high blood pressure, and her readings sit comfortably in a normal zone. She does not use tobacco. For years she assumed her diabetes made decent coverage impossible, so she carried only a small group policy through work and never looked further.

Here is roughly how her application would actually move. An honest agent would gather her details first: the type and date of her diagnosis, her recent A1C, her blood pressure readings, her medications, her height and weight, and her state. Rather than send that profile to one company and hope, the agent would compare how several diabetes-friendly carriers view it, because the spread between them can be a full rate class.

- Step one, set the target. Maria wants enough coverage to clear the mortgage and help with college, plus a cushion, for the years her kids are still dependent. That points to a level term policy sized to those obligations.

- Step two, match the carrier. Because her diabetes is well controlled and her companion numbers are healthy, fully underwritten term is realistic. The agent identifies the carriers most favorable to controlled Type 2 diabetes rather than applying blindly.

- Step three, set expectations. Given a stable A1C and treated, normal blood pressure, a standard or table-rated offer is a reasonable expectation. The agent explains that even a table rating here would be affordable, and that her controlled blood pressure is unlikely to be the sticking point.

- Step four, apply with the record ready. Maria gathers her recent lab work and her prescription details so the file tells a clean, reassuring story from day one.

The lesson in Maria's case is not a specific premium. It is the shape of the path. A condition she assumed was disqualifying turned out to be a manageable input that an informed approach could work around. The version of Maria who never applied stayed underinsured for no reason. The version who applied, with the right carrier and an honest file, got her family protected. The difference between those two outcomes was not her health. It was whether she tried.

How to improve your odds and your rate

You have real influence over the offer you receive, sometimes more than your diagnosis does. None of these steps require you to become a medical expert. They are about presenting a true, well-documented, stable picture of your health.

- Get your condition controlled and keep it there. Underwriters reward stability over time, not a single good reading. Several months of steady numbers tells a far better story than one recent result.

- Document everything. Regular checkups, lab work, and consistent medication use create a record that proves management. A clean, current file is one of your strongest assets.

- Address the factors you can change. If you use tobacco, stopping moves the needle more than almost anything else. Modest, sustained improvements in weight, blood pressure, or cholesterol can lift you a class.

- Apply sooner rather than later. Your rate is set by the version of you who applies, and a level policy locks it in. Health and age rarely improve quietly while you wait. Our look at the best age to buy life insurance walks through why the math usually favors acting now.

- Match the carrier to the condition before you apply. This is the highest-leverage move of all, and it is the part most people cannot do alone. Carriers vary enormously in how they treat the same condition.

- Consider the right amount, not just any amount. A policy you can comfortably keep paying for the full term beats a larger one you cancel in year three. Coverage only protects your family while it is in force.

For context on how common the underlying conditions are, federal health data from the Centers for Disease Control and Prevention shows that tens of millions of American adults live with diabetes alone, and far more manage high blood pressure. Insurers know these numbers as well as anyone, which is precisely why they have built underwriting around managed conditions rather than against them.

The mistake that actually gets people denied

Here is the angle most articles skip, and it is the one that matters most for protecting your family. The thing most likely to cost you coverage is not your condition. It is leaving a condition off the application, or shading the truth about how well it is controlled. Do not do it, ever.

Insurers verify what you tell them. They check prescription databases, prior insurance records, motor-vehicle history, and often your actual medical records. If you take a medication for a condition you did not disclose, the prescription history can reveal it. So the odds of a misstatement slipping through are low, and the cost if it surfaces is severe.

That cost lives in the contestability period. Most life insurance policies include a clause, usually the first two years, during which the insurer can review a claim and the application behind it. If a material misstatement turns up, the claim can be reduced or denied, exactly when your family is counting on the money. A policy that does not pay is worse than no policy at all, because you paid premiums believing you were covered.

There is also an upside to honesty beyond avoiding disaster. Full, accurate disclosure lets your agent steer you to the carrier that treats your specific condition most favorably. The truth is not just the safe choice. It is the strategic one. An underwriter who sees a complete, well-documented file is far more comfortable than one who senses gaps, and comfort tends to translate into a better offer.

Why an independent agent matters here

For straightforward, excellent health, you can shop life insurance many ways and do fine. With a pre-existing condition, the game changes, and who you work with starts to matter as much as which product you choose. The reason is that one company's standard offer can be another company's table rating for the exact same person.

An agent who works with many carriers can do something you cannot easily do yourself: match your specific condition to the company that underwrites it most favorably, before a single application goes out. Applying blindly to the wrong carrier can mean a higher rate, or a decline that then has to be disclosed on future applications. Applying to the right one can mean a clean approval at a price that surprises you. The difference is knowledge of how each carrier reads each condition, and that knowledge is the entire value of doing this with a professional.

A good agent also tells you the honest trade-offs. Sometimes the answer is fully underwritten term despite your condition. Sometimes it is a simplified-issue policy because speed and certainty matter more than squeezing out the lowest rate. Sometimes it is guaranteed issue because that is the realistic path, and a guaranteed yes for a smaller benefit beats chasing a larger policy you cannot get. The job is to lay out the real options and let you choose, not to push the one with the biggest commission. If you would rather start with a few questions than an application, you can always reach out and talk it through with a licensed human first.

When you are ready to look at your own numbers without pressure, that is the work we do every day at Sovereign Life Group, your life insurance strategist. According to research published by LIMRA, a large share of Americans say they own less life insurance than they know they need, often because they overestimate the cost or assume a health issue disqualifies them. For people with pre-existing conditions, that gap between fear and reality is the whole problem, and closing it usually starts with one honest conversation.

Find out what you actually qualify for

Fifteen minutes, no exam to start, no pressure. We will look at your condition, your goals, and which carriers view your situation most favorably, then lay out your real options in plain language.

Get a Quote Book a 15-Min Call Prefer to move fast? Save my card and get a quick quote for your situation.Frequently asked questions

Can you get life insurance with a pre-existing condition?

Yes. Most people with a pre-existing condition can get life insurance. The condition usually affects your price and which policy type fits best, not whether coverage exists at all. Well-managed conditions like controlled diabetes or treated high blood pressure often still qualify for fully underwritten coverage, while more serious situations can use simplified-issue or guaranteed-issue policies. The right fit depends on the condition, how well it is controlled, your age, and the carrier.

Does a pre-existing condition mean I will pay more for life insurance?

Often, but not always, and not as much as people fear. Insurers price your risk, so a health condition can move you into a higher rate class or add a table rating that raises the premium. A condition that is well controlled, documented, and stable for a year or more frequently earns a much better rate than people expect. Pricing varies widely by carrier, which is why comparing several is worth the effort.

What is the best life insurance for diabetics?

There is no single best policy for everyone with diabetes, because carriers underwrite diabetes very differently. A person with well-controlled Type 2 diabetes and a healthy A1C can often qualify for standard or near-standard rates on fully underwritten term life. Someone with Type 1 or with complications may do better with a diabetes-friendly carrier or a simplified-issue policy. The key is matching your specific numbers to a carrier that is favorable to your situation.

Can I get life insurance with high blood pressure?

Usually yes, and often at good rates. High blood pressure that is controlled with medication and within a healthy range is one of the most insurable common conditions. Many applicants with treated hypertension still qualify for standard or even better rate classes. Uncontrolled readings or related complications can raise the price, so documented, stable control works in your favor.

Will I be denied life insurance for a pre-existing condition?

A specific carrier can decline a specific application, but being shut out entirely is rare. If a fully underwritten policy is declined, simplified-issue and guaranteed-issue options exist precisely so people with serious conditions can still get coverage. Guaranteed-issue policies ask no health questions and cannot turn you down for health, though they carry smaller benefits and a waiting period. There is almost always a path to some coverage.

Should I leave a health condition off my life insurance application?

No. Never omit or misstate a condition. Insurers verify your history through prescription databases, medical records, and other checks, and most policies have a two-year contestability period during which the insurer can review a claim. A misstatement can lead to a denied claim when your family needs the money most. Honesty also helps your agent steer you to a carrier that views your condition favorably.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.