How Much Does Key Man Insurance Cost?

The Short Version

Key man insurance is life insurance a business owns on the person it cannot afford to lose. For a healthy key person, term coverage often runs from about 50 dollars to a few hundred a month per million of benefit. Age, health, coverage amount, term length, and policy type set the price. Premiums are usually not deductible, but the payout is generally tax-free if the paperwork is done right.

Every business has at least one person it cannot easily replace. The founder who holds the client relationships. The engineer whose head carries half the product. The salesperson who quietly brings in a third of the revenue. If that person did not come back tomorrow, what would it cost the company, and could the company survive the bill? Key man insurance is built for that exact question, and the first thing owners want to know is the key man insurance cost. The honest answer is that it usually costs a lot less than the loss it protects against, but the range is wide and it depends on real details.

I write this as a licensed agent who has sat across the table from owners doing this math. Some of what follows will point you toward the cheaper tool, not the fancier one. That is on purpose. The job here is the right coverage for the business, not the biggest premium.

What this guide covers

- What key man insurance actually is

- How much key man insurance costs

- What drives the key man insurance cost

- Term vs permanent key man coverage

- How much coverage your business needs

- A worked example, start to finish

- The tax side of key man insurance

- Who counts as a key person

- The risk most owners forget

- How to buy it without overpaying

- Is key man insurance worth the cost?

- Frequently asked questions

What key man insurance actually is

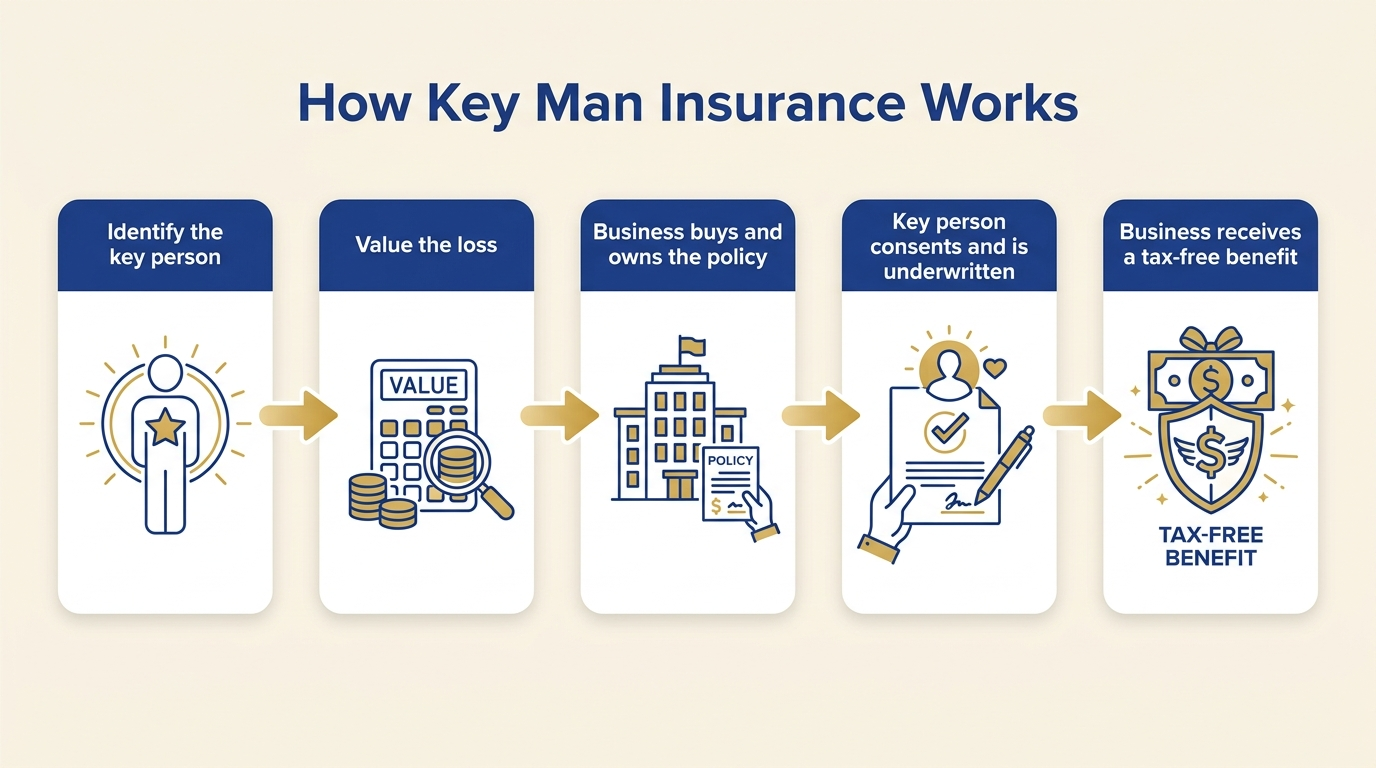

Key man insurance, also called key person insurance, is a life insurance policy that a business takes out on an employee or owner whose death would seriously hurt the company. The business applies for it, owns it, pays the premium, and is the beneficiary. If the insured person dies while the policy is in force, the money goes to the business, not the family, and it is there to keep the doors open through the disruption.

That last point trips people up, so it is worth saying plainly. This is not a benefit for the employee's household. It is a shock absorber for the business. The cash can cover the search and signing bonus for a replacement, service the debt a lender expected that person to help repay, buy out a partner's shares, or simply keep payroll steady while revenue dips during the gap. You will hear the same product called key man life insurance, keyman insurance, or business life insurance, and for the sake of your quote they mean the same thing. If you want the deeper primer on how businesses use it, our overview of key person business life insurance walks through the structure in full.

One quick distinction, because owners mix these up constantly. Key person insurance protects the company from losing a person. A buy-sell agreement, funded by life insurance, handles what happens to an owner's shares when a partner dies. They can involve the same kind of policy, but they solve different problems, and a business with multiple owners often needs both.

No medical exam for a ballpark. Free, and no pressure.

How much key man insurance costs

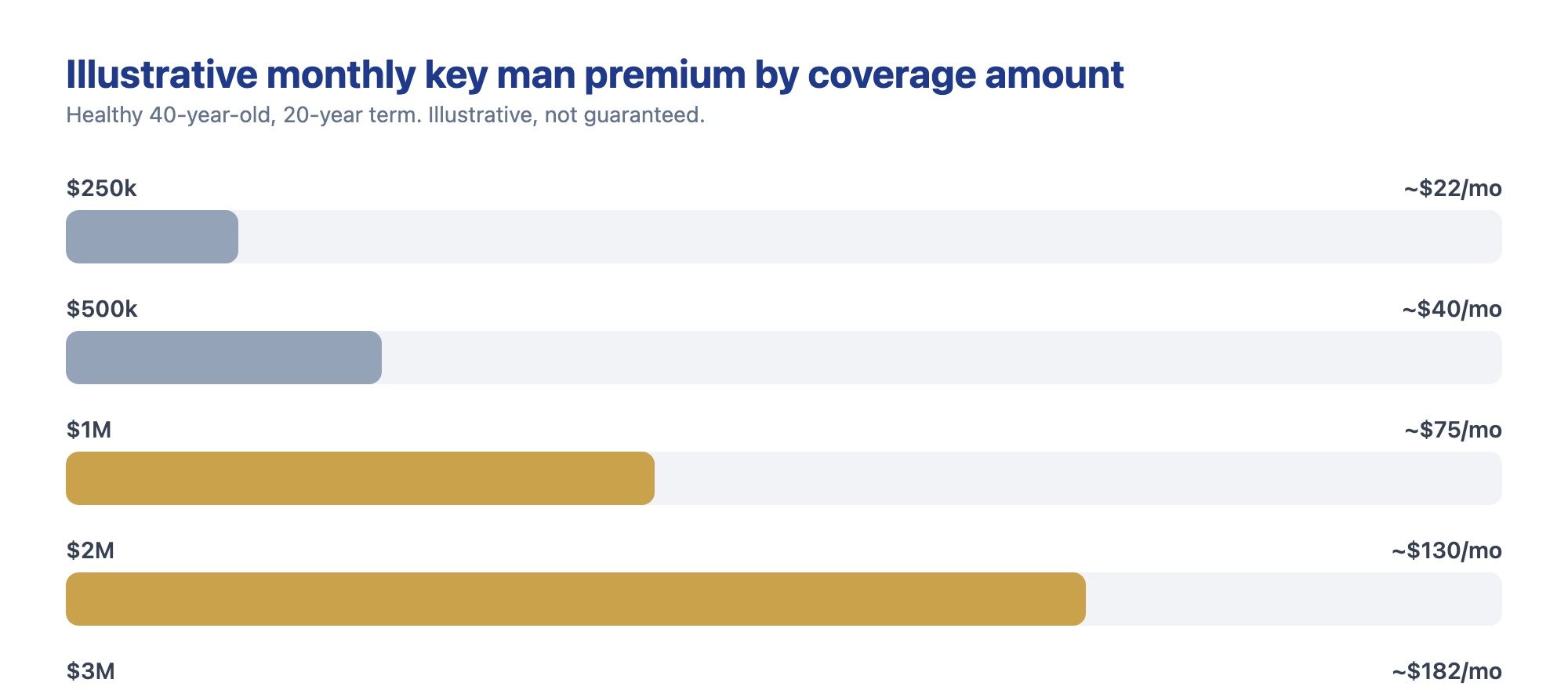

Key man insurance cost usually falls somewhere between about 50 dollars and a few hundred dollars a month for a healthy person on a term policy, and it climbs from there with age, larger coverage, or a permanent policy that builds cash value. Industry summaries put a common mid-range around 100 to 500 dollars a month, but the honest truth is that the range is wide because the inputs are wide.

Here is a set of illustrative figures to anchor the idea. These are sample numbers for a healthy applicant, not quotes, and your actual price depends on underwriting.

| Coverage amount | Illustrative monthly premium | Illustrative annual premium |

|---|---|---|

| $250,000 | About $22 | About $260 |

| $500,000 | About $40 | About $480 |

| $1,000,000 | About $75 | About $900 |

| $2,000,000 | About $130 | About $1,560 |

| $3,000,000 | About $182 | About $2,180 |

Notice how the premium does not double when the coverage doubles. That is normal. Carriers often price larger policies a touch more efficiently per dollar of benefit, so buying enough coverage the first time is usually cheaper than stacking small policies later. The mistake I see most is an owner insuring a founder for 250,000 dollars because it feels affordable, when the real exposure to the business is closer to two million. Cheap and wrong is still wrong.

For context on how this compares to personal coverage, the drivers are the same ones that set the average cost of life insurance for an individual. A key man policy is ordinary life insurance underwritten on one person. The business is just the owner and beneficiary instead of a spouse.

What drives the key man insurance cost

The premium is set by the risk the carrier is taking on one human being. The single biggest levers are the key person's age and health, followed by how much coverage you buy, how long the term runs, and whether you choose term or permanent. Get those five right and you can predict roughly where a quote will land before it ever prints.

Here is what moves the price and which direction it pushes.

| Factor | Effect on price | Why it matters |

|---|---|---|

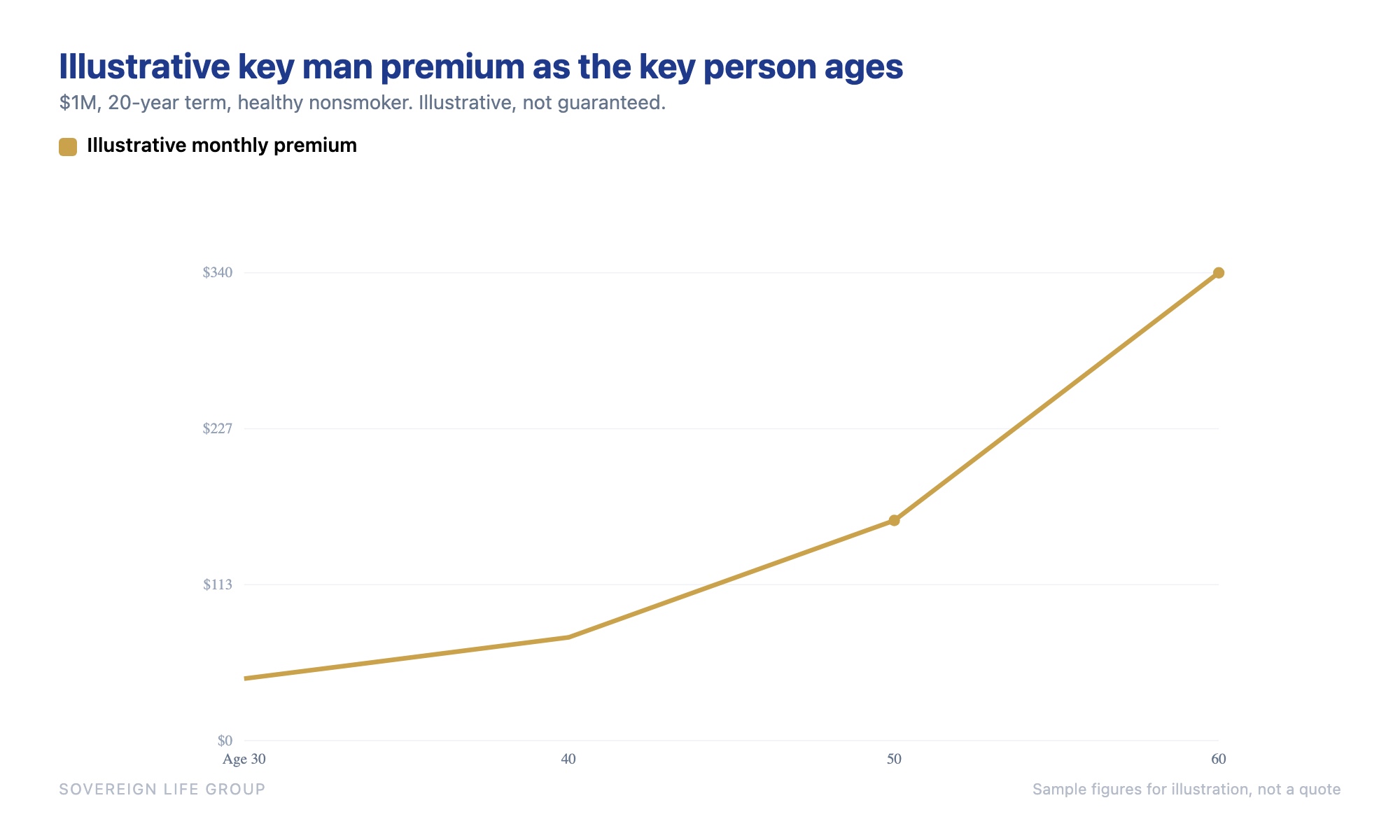

| Age of the key person | Older costs more | The statistical chance of a claim rises each year, so the premium rises with it |

| Health and history | Better health, lower price | Blood pressure, weight, family history, and past diagnoses all feed the rate class |

| Tobacco or nicotine use | Much higher | Underwriting treats nicotine as a major risk factor, often doubling the rate |

| Coverage amount | More benefit, more premium | A larger payout is a larger promise for the carrier to keep |

| Term length | Longer term, higher price | The carrier is on the hook for more years and more of the person's aging |

| Term vs permanent | Permanent costs much more | Cash-value policies fund a lifetime benefit plus a savings component |

| Industry and duties | Sometimes higher | Hazardous work or heavy travel can raise the rate for that individual |

| Underwriting type | No-exam often costs more | Skipping the exam shifts uncertainty to the carrier, who prices for it |

Two of these deserve a second look. The first is age, and the chart above says it better than I can. The same million-dollar policy that costs a healthy 30-year-old a modest monthly figure can cost several times more at 60. Waiting for a "better time" almost never makes the price drop, because the one variable you cannot improve is the calendar. If a key person is central to the business now, now is the cheapest they will be.

The second is health, and this is where a good agent earns their keep. Carriers grade the same person differently. One insurer treats controlled high blood pressure as a nonissue; another bumps the rate. Shopping the case across several carriers, rather than taking the first offer, is often the difference between an average price and a genuinely good one. That is the whole reason to work with an independent broker instead of a single company.

Term vs permanent key man coverage

Term key man insurance covers the person for a set number of years and costs the least, which is why most businesses start there. Permanent key man insurance lasts for life and builds cash value the business can borrow against, but it costs several times more per dollar of benefit. The right choice depends on whether the need is temporary or permanent, and on what the business wants the policy to do besides pay a death benefit.

Most owners I talk to are protecting a need with an end date. A loan that gets paid off in ten years. A founder who plans to retire at 65. A product still leaning on one engineer until the team is deep enough to carry it. For those, a term policy sized to the years of exposure is usually the cleanest fit. It is inexpensive, it is easy to understand, and when the need is gone you simply let it end.

Permanent coverage earns its higher cost in narrower cases. When the key person is also an owner and the policy doubles as part of a buy-sell or an exit plan, the lifetime guarantee and the cash value can be genuinely useful. Some businesses like that the cash value sits on the books as an asset they can tap in a pinch. The trade-off is real money, though, and the honest question is whether the business would rather pay several times the premium for the extra features or buy cheaper term and put the difference to work elsewhere. If you want the full structural comparison, our breakdown of term versus whole life insurance lays out where each one fits.

| Factor | Term key man | Permanent key man |

|---|---|---|

| Relative cost | Lowest premium per dollar | Several times higher |

| How long it lasts | A set number of years | For life, if premiums are paid |

| Cash value | None | Builds cash value over time |

| Best fit | A need with an end date | Lifetime need or an exit or buy-sell plan |

| On the balance sheet | Pure expense | Can show as an asset |

How much coverage your business needs

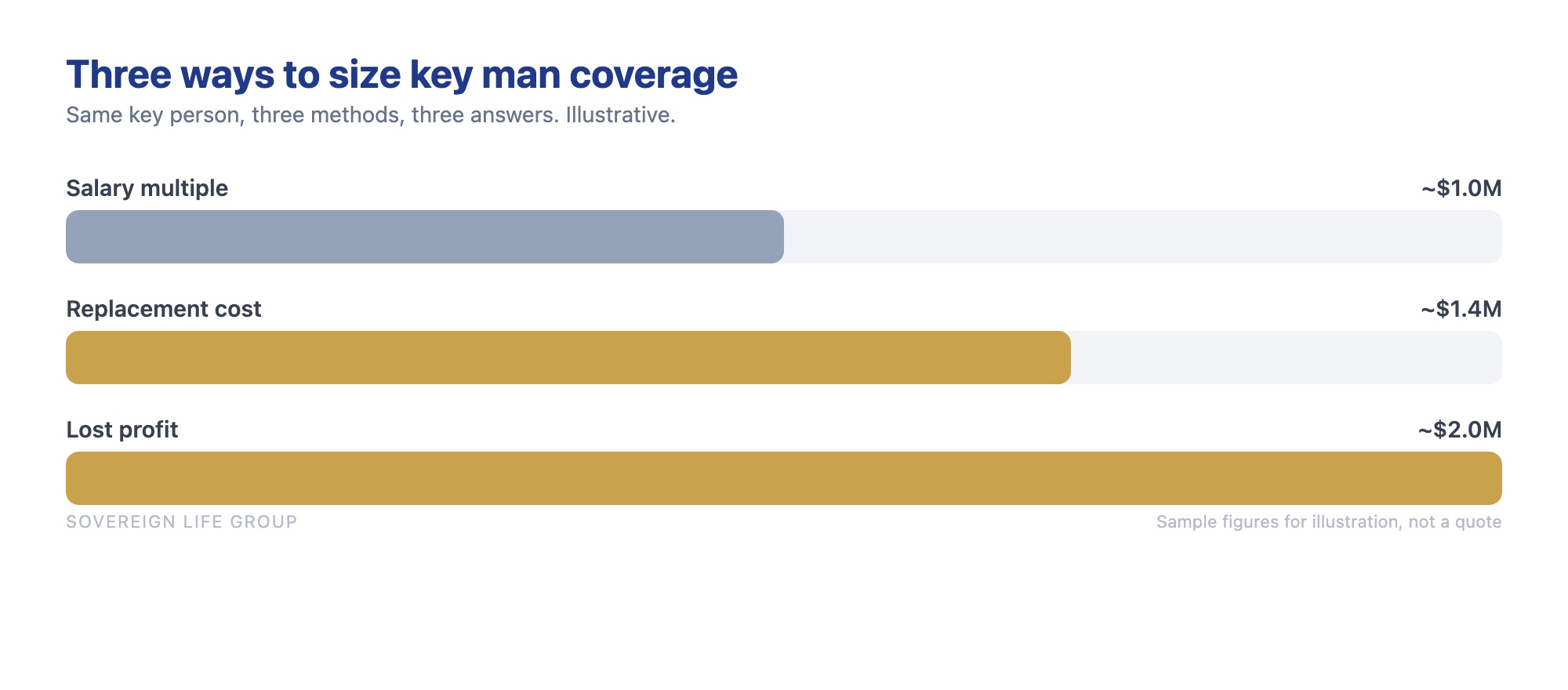

There is no legal formula for how much key man coverage a business needs, but three methods do most of the work. A multiple of the key person's salary, usually five to ten times. The full cost to find, hire, and ramp up a replacement. And that person's measurable contribution to profit over the years it would take to recover. Run all three, then choose a number that reflects the real disruption.

Each method looks at the loss from a different angle, which is why they rarely agree, and that is fine. Here is how I walk an owner through them.

- Salary multiple. Quick and rough. Take the key person's total compensation and multiply by five to ten. It is easy, and it is a reasonable floor, but it ignores that some people are worth far more to the business than their paycheck suggests.

- Replacement cost. Add up the recruiter fees, the signing bonus, the months of a search, and the ramp time before a successor is fully productive. For a specialized role this number can be startling, and it is often the most concrete of the three.

- Contribution to profit. Estimate the revenue or margin that flows through this person, then multiply by the years it would take the business to rebuild it. For a rainmaker or a technical founder, this is usually the largest figure and the truest picture of the exposure.

Most owners land somewhere between the replacement cost and the profit-contribution numbers. There is no prize for buying the biggest policy, and there is real danger in buying one so small it barely dents the actual loss. Size it to the disruption you are honestly trying to survive, not to a round number that looks tidy on a page.

A worked example, start to finish

Let me put numbers to it with an illustrative example. These figures are made up for teaching, not a real client and not a quote, but the shape of the math is exactly what plays out in real conversations.

Picture a design and build firm with three owners and about 30 employees. One partner, call the role the lead estimator and rainmaker, personally sources roughly 40 percent of the firm's new work and holds the relationships with the biggest repeat clients. The bank that financed the firm's equipment specifically wanted to know who carries that revenue. If that partner died, the firm would not close overnight, but the pipeline would thin fast, a couple of major clients might drift, and the remaining owners would be scrambling to cover a loan payment while trying to rebuild the sales engine.

Run the three methods on that person. A salary multiple on 200,000 dollars of compensation at seven times lands near 1.4 million. The replacement cost, given how long it would take to hire and season someone who can do the estimating and hold the relationships, might be 1 million once you count the lost momentum. The profit-contribution method, using the margin that flows through that pipeline over the two to three years it would take to recover, pushes toward 2 million. The owners settle on 1.5 million as the coverage that reflects the real exposure without overbuying.

Now the cost. That partner is 46, healthy, and does not use tobacco. A 15-year term policy for 1.5 million, sized to the years until a planned exit, might run in the range of 120 to 160 dollars a month on an illustrative basis, again depending entirely on underwriting. Set against a loss the firm measures in the millions, that premium is the kind of number owners tend to describe as a rounding error once they see the two figures side by side. The business owns the policy, names itself beneficiary, and the partner signs the consent. Done.

The lesson in that example is not the exact dollars. It is the ratio. The key man insurance cost is small relative to the hole the loss would leave, which is the entire reason the product exists. When owners hesitate, it is almost always because they have looked at the premium without first putting a real number on the loss.

Get a fast, free estimate tailored to your age and health.

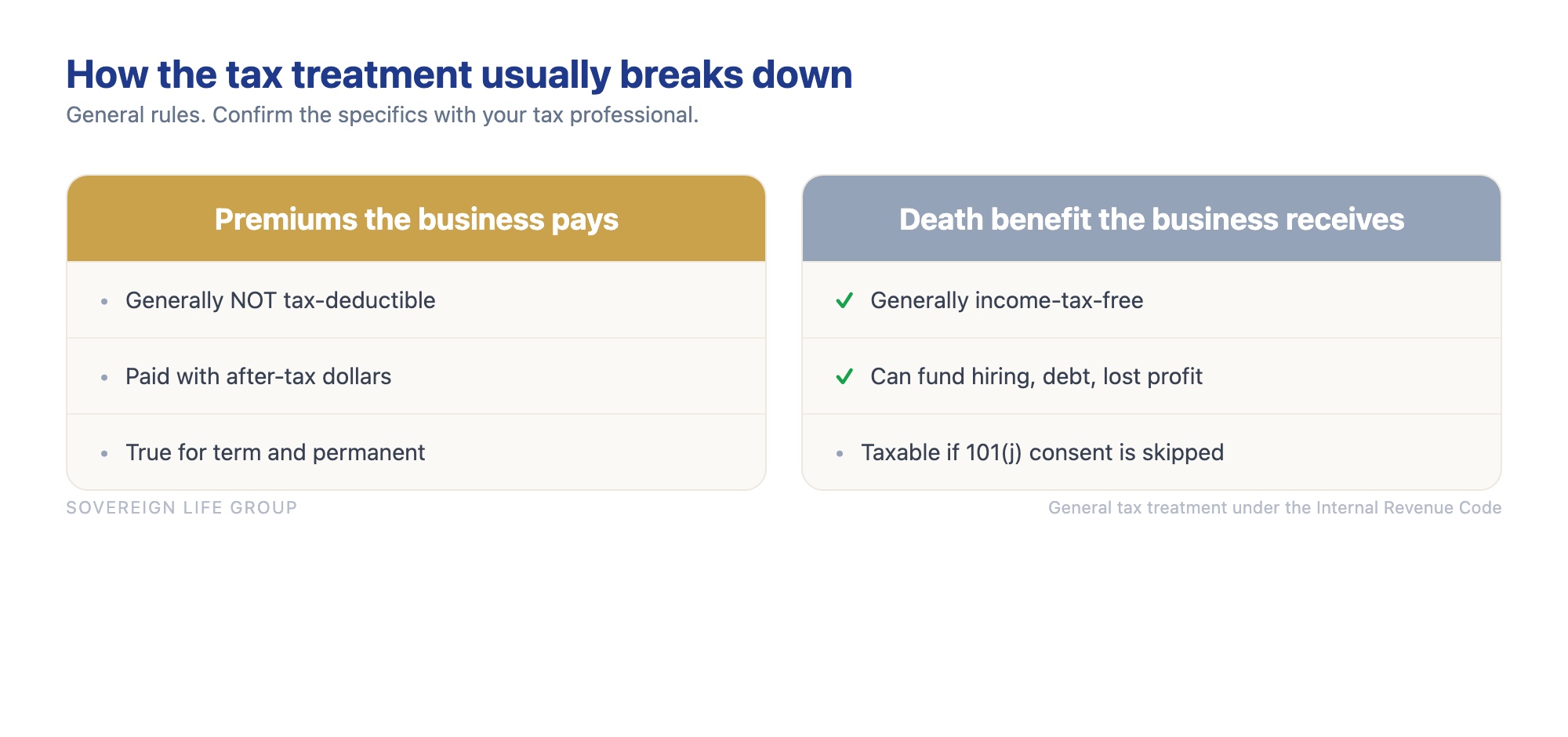

The tax side of key man insurance

The tax rules on key man insurance surprise a lot of owners, so learn them before you buy. In general, the premiums are not tax-deductible when the business owns the policy and is the beneficiary, so you pay them with after-tax dollars. In exchange, the death benefit is usually received income-tax-free, as long as you follow the employer-owned life insurance notice and consent rules first. Get the order wrong and you can taint an otherwise tax-free payout.

That notice and consent step is the part people skip, and it matters. Under the rules for employer-owned life insurance, the business generally must notify the insured in writing, get their written consent before the policy is issued, and file the right form with its tax return. Miss that, and the portion of the benefit above the premiums the business paid can become taxable income. It is a paperwork problem, not a hard one, but it has to happen up front, not after a claim. You can read the framework in IRS guidance on business insurance expenses, and you should confirm your specific situation with a tax professional, because this is genuinely their lane, not mine.

None of this is a reason to hesitate. It is a reason to do the setup correctly. The whole appeal of key man coverage is that a modest, non-deductible premium can turn into a large, tax-free infusion exactly when the business is reeling. That trade only works cleanly if the consent is signed before the ink is dry on the policy.

Who counts as a key person

A key person is anyone whose loss would measurably hurt the company's revenue, financing, or ability to operate. That is usually an owner or founder, but it can just as easily be a top salesperson, a lead engineer, a specialist with rare credentials, or the one person who holds the client relationships. The test is simple. If this person vanished, would the business feel it in the bank account?

In a small business the key person is often the owner, because so much runs through them. But do not stop there. I have watched owners insure themselves and completely overlook the salesperson driving half the pipeline, or the operations lead who is the only one who knows how the whole machine actually runs. Lenders and investors think about this too, which is why a bank financing your growth may ask whether the person carrying the revenue is insured before they sign.

Here are the roles that most often qualify:

- Owners and founders whose reputation or relationships drive the business.

- Top producers or salespeople responsible for a large share of revenue.

- Technical leads or specialists whose knowledge is hard to replace quickly.

- Executives whose departure would rattle clients, lenders, or investors.

- A partner whose share the others would need to buy out, which ties into buy-sell planning.

If your business runs on one or two people who would be genuinely hard to replace, that is your answer. For a fuller look at how coverage is structured around these roles, our key person insurance coverage page breaks down the options by business type and situation.

The risk most owners forget

Key man life insurance pays if the person dies. It does nothing if that person survives but can no longer work, and disability is the far more common event. This is the gap most owners never think about, and it is worth naming because a serious injury or illness that sidelines a key person for a year can do nearly the same damage to a business as a death, without triggering a life policy at all.

There are two ways businesses close that gap. The first is a key person disability policy, which pays the business a benefit if the insured is disabled and unable to perform their role. The second is adding a living-benefits or chronic-illness rider to the key man life policy, which can let the business access part of the benefit early if the insured is diagnosed with a qualifying serious illness. Both add cost, and neither is automatic, so you have to ask for them.

I am not saying every business needs disability coverage on top of life. I am saying the question deserves a real answer instead of silence. If your key person is a physical worker, or if the business could not absorb a year of that person being out, the disability side is worth pricing. Most competitor articles on key man cost skip this entirely, and I think that does owners a quiet disservice. The point of this exercise is protecting against the loss of a person's contribution, and death is only one way that contribution disappears.

How to buy it without overpaying

Buying key man insurance well is mostly about doing a few things in the right order. Size the coverage to the real loss, shop the case across multiple carriers, keep the term matched to the years of exposure, and handle the consent paperwork before the policy is issued. Do those, and you avoid the two most common outcomes: overpaying for the wrong policy, or underinsuring the person who matters most.

Here is the path I would walk a business owner through, in order.

- Name the key people honestly. Not just yourself. Who actually carries revenue, relationships, or knowledge the business could not quickly replace? Write the short list first.

- Put a number on the loss. Run the salary multiple, the replacement cost, and the profit-contribution methods. Land on a coverage amount that reflects the real disruption, not the budget.

- Decide term or permanent. If the need has an end date, term is usually the efficient answer. Reach for permanent only when a lifetime need or an exit plan justifies the extra cost.

- Shop the case, do not take the first offer. Carriers grade the same person differently, especially with any health history. An independent broker can run it across several and bring back the best fit.

- Get the consent signed up front. Handle the employer-owned life insurance notice and consent before the policy is issued so the death benefit stays tax-free. This is a five-minute step that protects a large payout.

- Review it when the business changes. A new loan, a new partner, a role that grows, a person who leaves. Coverage that fit two years ago may be wrong now.

The recurring theme is that the price follows the plan. When owners overpay, it is usually because they bought a product before they defined the need. Define the need first and the right policy, and the right key man insurance cost, tends to reveal itself.

Is key man insurance worth the cost?

For most businesses that genuinely lean on one or two people, key man insurance is worth the cost, because the premium is small relative to the loss it covers and the payout is usually tax-free. The harder question is not whether to protect the person, but which person, how much, and with what type of policy. That is where an honest conversation beats a rushed purchase.

Consider the backdrop. According to research from LIMRA, about 42 percent of U.S. adults said in 2024 that they need more life insurance than they carry, and a recurring finding in that same body of research is that people routinely overestimate what coverage costs, often by roughly threefold. Business owners are not immune to either blind spot. Plenty of companies that would be crippled by the loss of a founder carry no key person coverage at all, usually because nobody ever put the loss and the premium next to each other.

So here is my honest verdict. If your business would take a real financial hit from losing a specific person, get coverage in place, and get it sized to the actual exposure rather than to whatever fits comfortably this month. If the business could genuinely absorb that loss from cash flow or reserves, you may not need much, or any. The wrong move is the one in the middle: knowing a key person is irreplaceable and doing nothing because the topic felt complicated. It is not that complicated, and a good agent makes it simple. When you are ready to put a real number on it, you can start with Sovereign Life Group, your life insurance strategist.

Want a straight number for your business?

Fifteen minutes. We will name your key people, size the real exposure, and price a policy that fits, with the tax setup done right from the start. No pressure, no jargon.

Book a 15-Min Review Prefer to start with a quick quote? Save my card and get a fast key man quote.Frequently asked questions

How much does key man insurance cost per month?

For a healthy key person in their 30s or 40s, term key man insurance often runs from about 50 to a few hundred dollars a month per one million dollars of coverage, depending on age, health, and the amount. Permanent policies that build cash value typically cost several times more. Your real number depends on underwriting, so treat any figure in an article as a starting range, not a quote.

Who pays for key man insurance, the business or the employee?

The business pays for it. The company applies for the policy, owns it, pays the premium, and is named as the beneficiary. The key person consents in writing and completes underwriting, but the employee is not out of pocket and does not receive the benefit. The money is meant to keep the business steady if that person is lost.

Is key man insurance tax-deductible?

Generally no. When the business owns the policy and is the beneficiary, the premiums are not tax-deductible, so they are paid with after-tax dollars. The upside is that the death benefit is usually received income-tax-free, as long as the employer-owned life insurance notice and consent rules under IRC section 101(j) are followed before the policy is issued. Confirm the details with your tax professional.

How much key man coverage does a business need?

There is no single rule, but three common methods are a multiple of the key person's salary (often five to ten times), the cost to replace and ramp up a successor, and that person's measurable contribution to profit over the years it would take to recover. Many owners run all three and land somewhere in the middle. The goal is to cover the real disruption, not a round number.

Does key man insurance cost more for older or unhealthy employees?

Yes. Age and health are the two biggest drivers of the premium. An older key person, a tobacco user, or someone with a serious health history will cost more to insure because the statistical risk of a claim is higher. This is also why locking in coverage while a key person is younger and healthier usually costs less over the life of the policy.

What happens to the policy if the key person leaves the company?

Because the business owns the policy, it stays with the business. If the person leaves, the company can stop the coverage, keep it, or in some cases transfer or sell it to the departing employee, though a transfer can carry tax consequences. Many owners simply cancel a term policy on someone who is no longer key and open a new one on the person who now fills that role.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, business, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.