Key Person Insurance: A Guide for Small Business Owners

The Short Version

Key person insurance is a life insurance policy your business buys on the one or two people it cannot easily replace, often an owner or a top producer. The company owns it, pays for it, and collects the benefit. That cash keeps the doors open, funds a buy-sell agreement so ownership passes cleanly, or repays a loan the bank tied to that person. Most small business owners insure the building and the trucks and forget to insure the person the whole thing runs on.

Ask most small business owners what would happen to their company if they did not wake up tomorrow, and you get a long pause. They have insured the building, the vehicles, the liability, the workers. The one asset holding the whole thing together, a person, usually has nothing on it. Key person insurance is the fix for that gap. It is life insurance the business owns on someone the company depends on, so that if that person dies, the business gets a check instead of a crisis. This guide walks through what it is, who counts as a key person, what it costs, how it pays for a buy-sell agreement, the tax rules owners get wrong, and a real worked example so the numbers feel concrete.

I sell this coverage, so read me with that in mind. But I also talk plenty of owners out of a bigger policy than they need, and I will point out below where a simple approach beats a fancy one. The goal is a business that survives a bad day, not a big premium.

What this guide covers

- What key person insurance actually is

- Who counts as a key person

- What it covers and what it does not

- How much key person insurance you need

- What key person insurance costs

- Term vs permanent business life insurance

- How a buy-sell agreement uses life insurance

- The tax rules business owners get wrong

- A worked example with real numbers

- How to set it up the right way

- When you probably do not need it

- Frequently asked questions

What key person insurance actually is

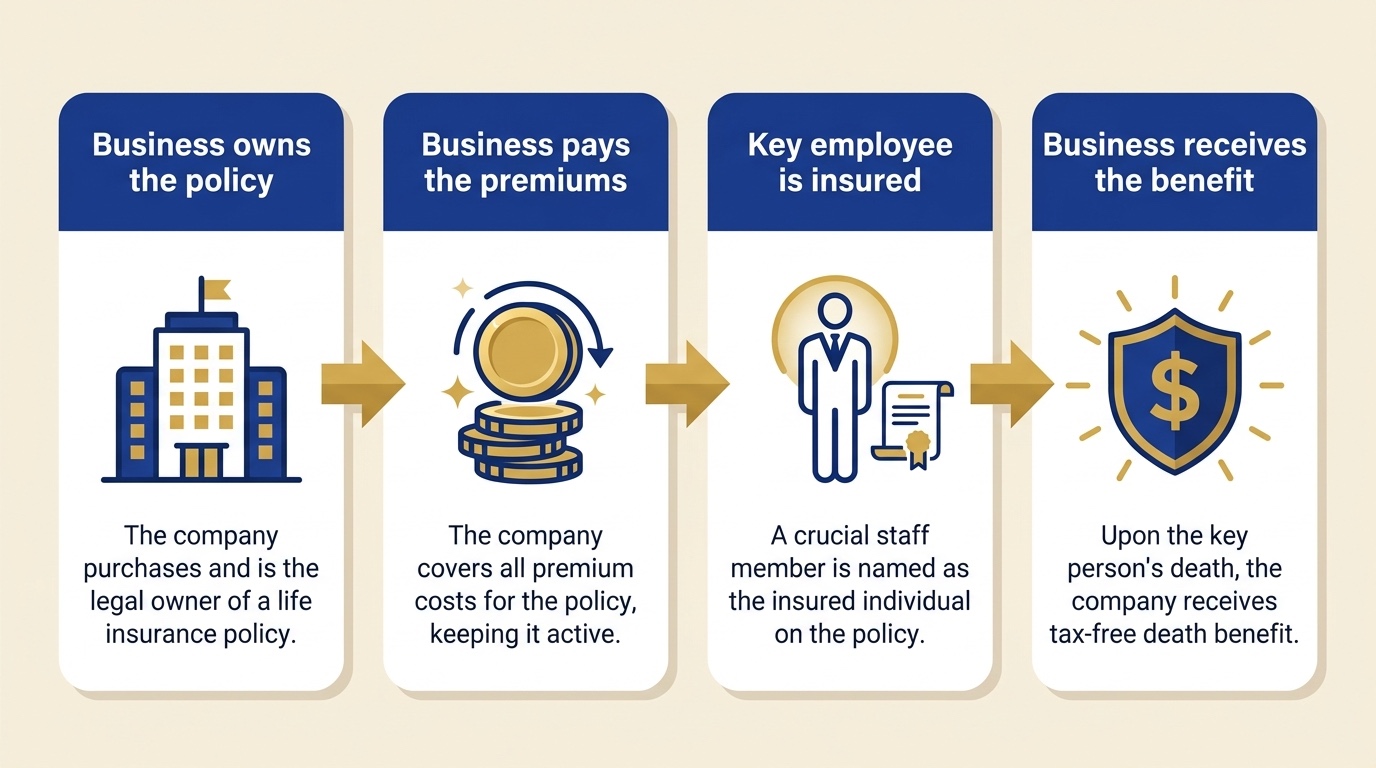

Key person insurance is a life insurance policy a business owns on an owner or employee the company cannot easily replace. The business applies for it, pays the premiums, and names itself as the beneficiary. If that person dies, the death benefit goes to the company, not the family, giving the business cash to steady itself, hire a replacement, or pay off debt.

You will hear it called a few different things. Key man insurance is the older term. Key employee insurance and key person life insurance mean the same thing. The word "person" is the polite modern version, and it is more accurate anyway, because the person your business leans on is often not a man in a corner office. It might be the founder, sure. It might also be the one estimator who prices every job right, or the salesperson who personally owns half your client relationships.

The structure is what makes this different from a personal policy. With ordinary life insurance, you own the policy and your spouse or kids collect. With key person insurance, three roles split apart:

- The owner and payer is the business. The company signs the application and writes the premium checks.

- The insured is the key person. They have to consent in writing and go through underwriting, but they do not pay and they are not the beneficiary.

- The beneficiary is the business. The company collects the benefit and decides how to use it.

That last part surprises people. The insured person's family gets nothing from this specific policy, and that is by design. This coverage protects the enterprise, not the household. If you also want to protect the insured's family, that is a separate personal policy, and a good agent will size both without pretending one does the other's job.

Who counts as a key person

A key person is anyone whose sudden absence would cost the business real money, not just morale. That usually means an owner, a partner, a founder, or an employee who drives revenue, holds specialized knowledge, carries key client relationships, or personally secures the company's financing. If losing them would shrink profit or shake the bank's confidence, they qualify.

The test I use with owners is blunt on purpose. Picture that person gone for good on Monday. By Friday, what breaks? If the honest answer is "not much, we would reassign the work," they are valuable but probably not a key person. If the answer is "we lose the account that pays a third of payroll," or "no one else knows how the estimating model works," or "the line of credit was personally guaranteed by them," now you are looking at a key person.

The usual candidates

- Owners and partners. In a two-owner shop, each owner is almost always a key person, both for the work they do and for the ownership stake that has to go somewhere if they die.

- The rainmaker. The salesperson or relationship owner who carries client trust in their own name. When they leave, the clients often leave with them.

- The specialist. The engineer, coder, chemist, or master tradesperson whose knowledge is not written down anywhere and cannot be hired back in a week.

- The operator. The person who actually makes the place run day to day, the one whose calendar everyone else quietly depends on.

Here is the mistake I see most: owners insure themselves and stop there. The founder buys a policy on their own life, feels covered, and never looks at the employee who is arguably more irreplaceable. If your best estimator walked out and took two competitors' worth of pricing knowledge with them, that is a bigger short-term hole than losing the owner who mostly signs checks. Insure the risk, not the title.

This matters at scale. Small businesses make up 99.9 percent of all U.S. businesses according to the U.S. Small Business Administration's 2023 profile, and the vast majority of them run on a handful of people. When a company that size loses one of those people, there is usually no bench deep enough to absorb it quietly.

One more note. A key person does not have to be an owner to be insured, and an owner does not automatically need key person coverage. A silent partner who does no work and holds no relationships is an ownership question, handled by a buy-sell agreement, not a key person question. Keep those two ideas separate and the rest of this gets clearer.

What it covers and what it does not

Key person insurance pays a cash death benefit to the business when the insured person dies during the policy term. The company can use that money for anything: covering lost revenue, recruiting and training a replacement, reassuring clients and lenders, repaying business debt, or buying out the deceased owner's family. The base policy covers death. It does not cover someone quitting, retiring, or getting sick unless you add a rider.

What the money is really buying is time and stability. When a key person dies, the business loses their daily output, and then it loses momentum on top of that. Clients wonder if they should look elsewhere. Lenders get nervous. The remaining team scrambles. A benefit that lands in the company account buys breathing room to make good decisions instead of desperate ones. That is the whole point.

Common ways businesses use the benefit

- Replace lost revenue while the team stabilizes and a successor gets up to speed.

- Recruit and train a replacement, which for a specialized role can take many months and a real search budget.

- Repay business debt or satisfy a lender. Many small business loans are effectively tied to the owner. Some lenders require this coverage as a condition of financing.

- Fund a buy-sell agreement so a deceased owner's share can be bought from their heirs cleanly, which we cover in depth below.

- Wind the business down with dignity if the honest answer is that it cannot continue, so vendors and employees are paid rather than left holding the bag.

What it does not cover

Standard key person insurance is built around death, so read the contract for the edges. It generally does not pay because a key person quits, retires, or is recruited away. It does not cover a slow sales year. It does not cover disability on its own, though many carriers offer a key person disability policy or a rider, and honestly, disability is the more common way a key person suddenly stops contributing, so it is worth pricing alongside the life coverage. There is also a contestability period, usually the first two years, during which the insurer can review a claim for misstatements on the application. Answer the health questions honestly and that window is a non-issue.

A quick, no-pressure look at the numbers. About 2 minutes.

How much key person insurance you need

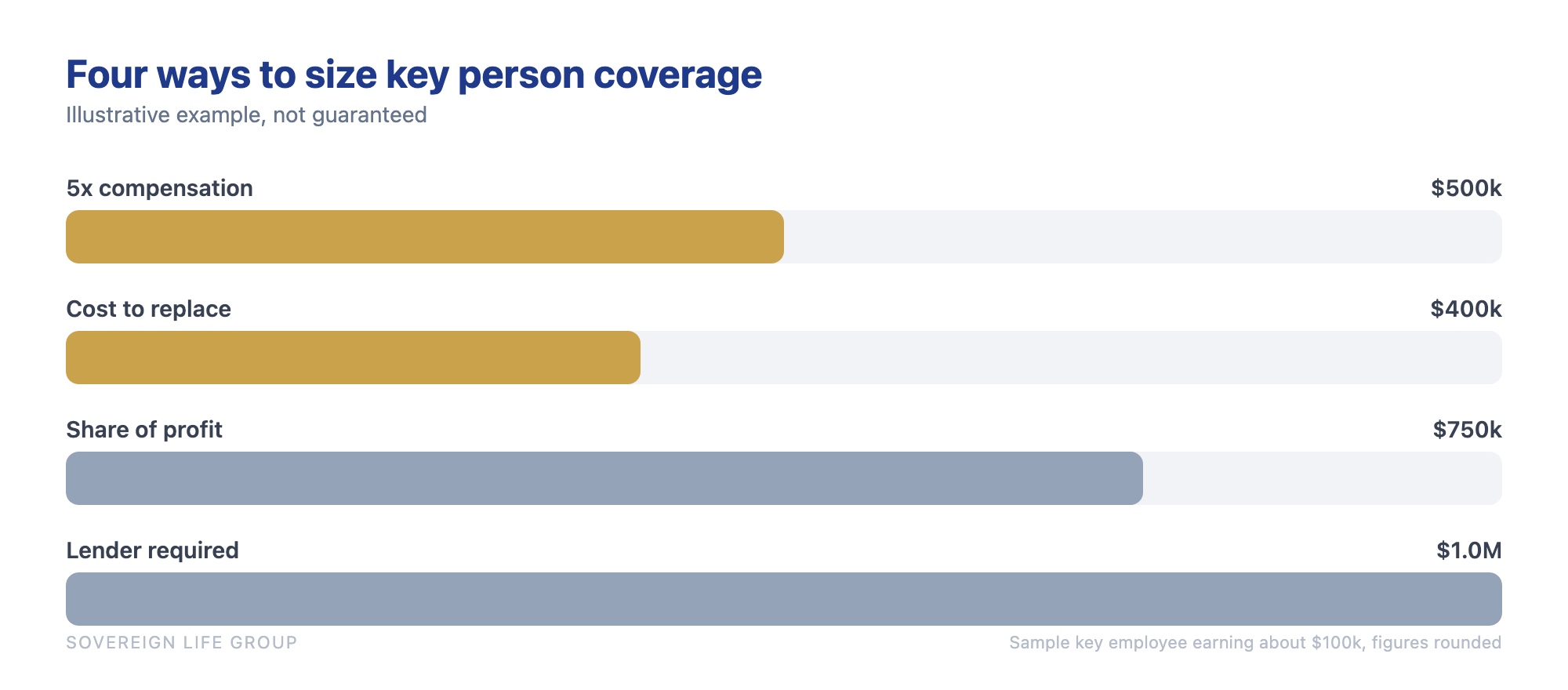

There is no single formula for how much key person insurance to buy. Most owners land on one of four methods: a multiple of the person's compensation, usually five to ten times; the real cost to find and train a replacement; that person's share of company profits over a few years; or the amount a lender requires for financing. The right number is the one that genuinely covers the hole their absence would leave.

Each method answers a slightly different question, so it helps to run more than one and then use judgment.

The four common methods

- Multiple of compensation. Take total pay, salary plus bonus, and multiply by five to ten. Simple, defensible, and the one carriers see most. A key person earning 150,000 dollars a year might justify roughly 750,000 to 1.5 million in coverage on this method alone.

- Replacement cost. Add up recruiting fees, signing costs, training time, and the productivity dip while a new hire ramps. For a hard to fill specialist, this number is often bigger than owners expect.

- Contribution to profit. Estimate the share of gross profit that person is directly responsible for, then multiply by the number of years it would take the business to recover. This is the most honest method for a rainmaker.

- Lender requirement. If a bank or SBA loan requires life insurance on the owner as a condition, the loan balance sets a floor. This one is not optional, so start there and build up if the other methods point higher.

My practical take: pick the highest reasonable figure your budget comfortably supports, because the loss from a dead key person is almost never small, and term coverage is cheap enough that buying a little extra rarely hurts. Just do not pull a number from thin air. Underwriters want to see the business math behind the amount, especially on larger policies, and a benefit wildly out of line with the person's economic value can slow down or complicate approval.

What key person insurance costs

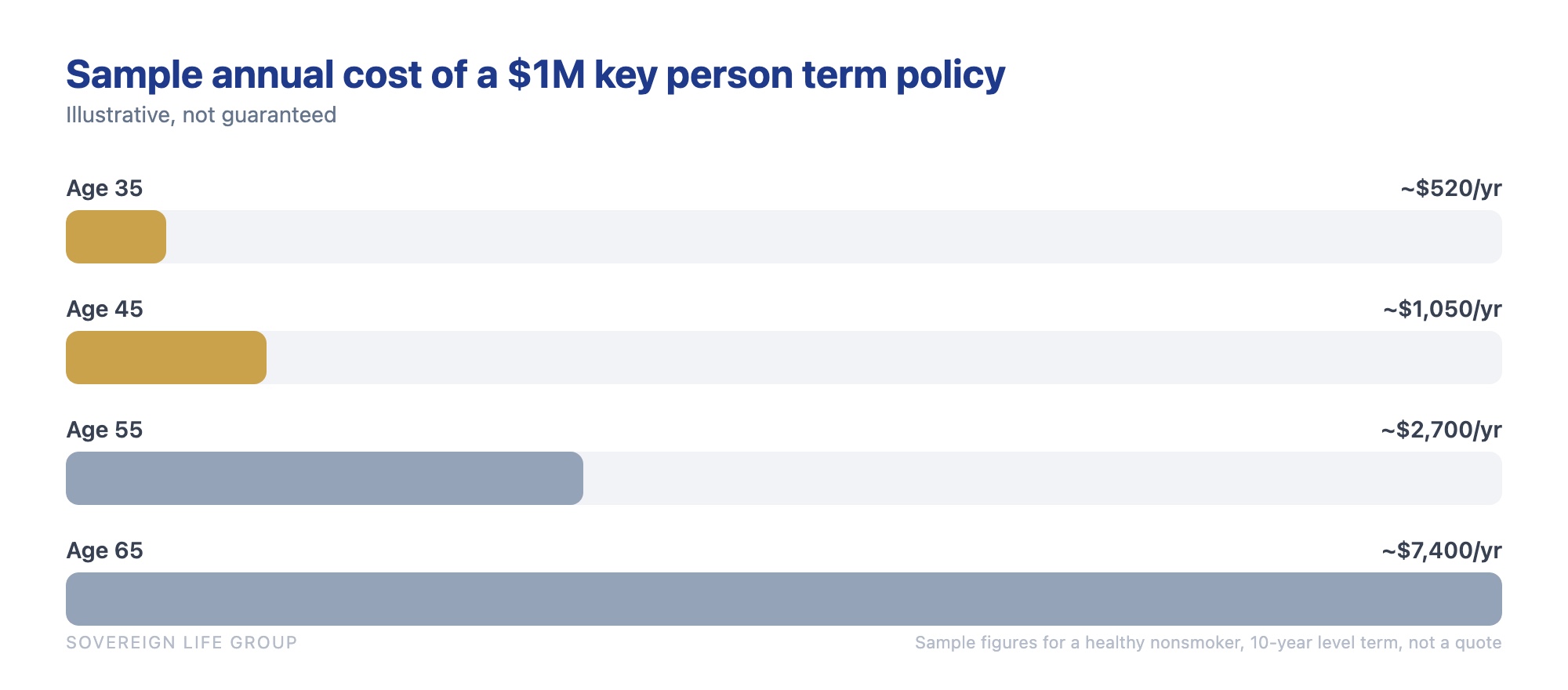

Key person insurance often costs less than owners expect, because most of it is term coverage. A healthy key person in their 30s or 40s can frequently be insured for 1 million dollars of term coverage for a modest monthly premium, sometimes in the range of a phone bill. For the full price ranges laid out by coverage amount and age, our breakdown of how much key man insurance costs puts real numbers to it. Price rises sharply with age, tobacco use, health history, the size of the benefit, and whether you choose term or permanent coverage.

No article can quote your exact rate, and you should be wary of anyone who does before they know the insured person's age and health. What I can show you is direction. The single biggest driver is age, because the statistical risk of a claim climbs every year. Here is a sample of how a level term premium tends to move for the same benefit as the insured gets older.

Those figures are a sample to show the shape of the curve, not a promise. Your real rate depends on the full underwriting picture and is subject to approval. Still, the lesson holds every time: the cheapest day to insure a key person is the youngest and healthiest they will ever be, which is today. I have watched owners put this off for two years and then pay noticeably more, or find the person now has a condition that changes the conversation. Waiting is rarely the money-saver it feels like.

Here is what moves the premium, and in which direction.

| Factor | Effect on price | Why |

|---|---|---|

| Insured person's age | Older costs more | Claim risk rises each year, so premium rises with it |

| Health and history | Better health, lower price | Underwriting prices the risk it can see today |

| Tobacco or nicotine use | Significantly higher | Nicotine is treated as a major risk factor |

| Coverage amount | More benefit, more premium | A larger benefit is a larger promise to insure |

| Term vs permanent | Permanent costs much more | Permanent lasts for life and builds cash value |

| Term length | Longer term, higher price | The insurer is on the hook for more years |

| Underwriting type | No-exam often costs more | Skipping the exam shifts risk to the insurer |

Term vs permanent business life insurance

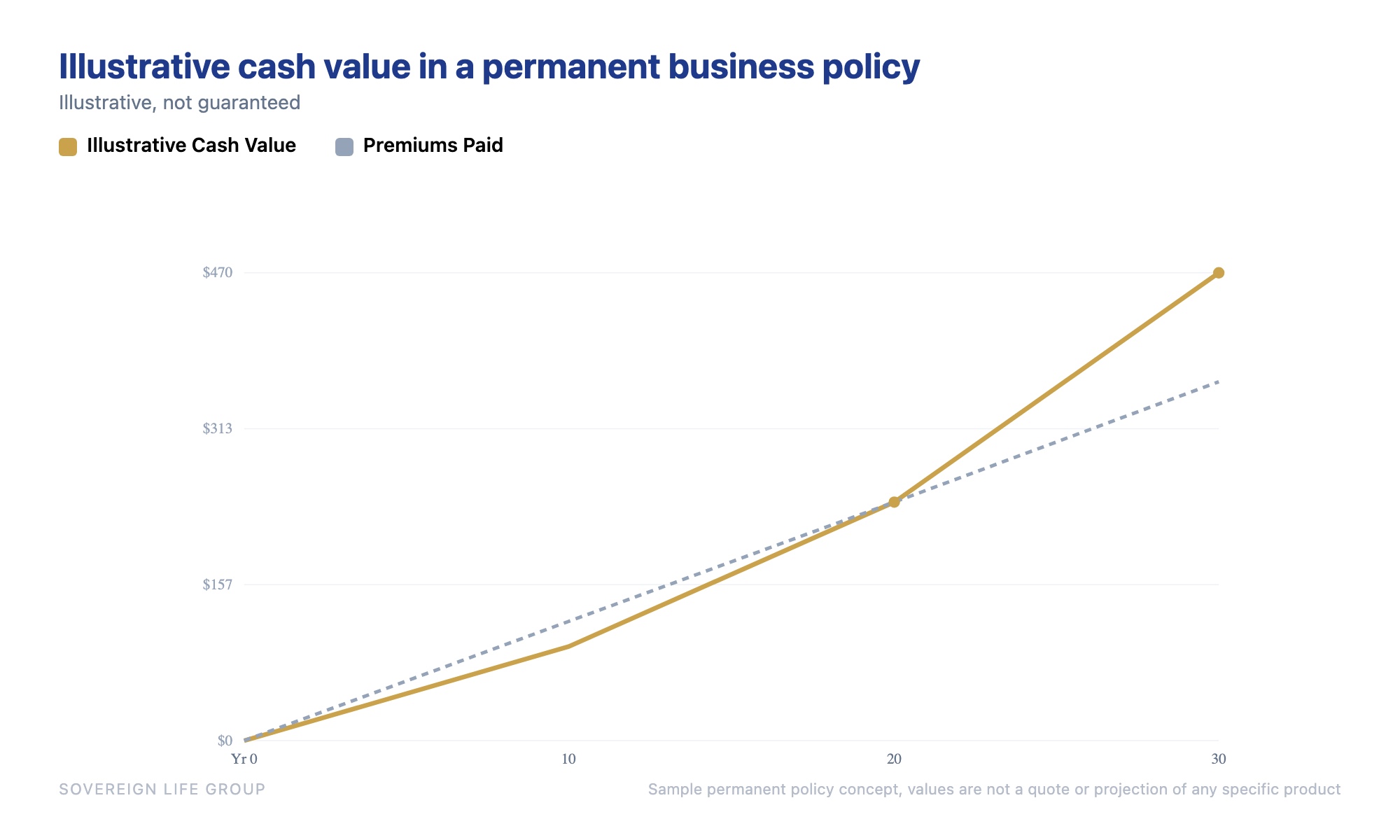

Business life insurance comes in two broad shapes. Term covers the key person for a set number of years at a low, level premium and pays only if they die during that window. Permanent coverage lasts for life and builds cash value the business can access, but it costs far more per dollar of benefit. Most key person needs are temporary, so term does the job for a lot less.

The right pick comes down to how long the risk lasts and whether you want the policy to double as a business asset.

When term is the right tool

If you are protecting against the loss of a key person over a defined stretch, say the years until a loan is paid off, a successor is trained, or the owner plans to retire, term is usually the smart, cheap answer. You get a large benefit for a small premium, you keep the business's cash free for the business, and when the risk ends, the coverage ends. For pure key person protection on an employee, I lean toward term the large majority of the time. If you want the deeper structural comparison, our breakdown of term versus whole life insurance lays out the trade-offs in plain language.

When permanent earns its keep

Permanent coverage, whole life or indexed universal life, makes more sense when the need is permanent or when you want the policy to build a business asset. Because a permanent policy accumulates cash value the company can borrow against or draw on, some owners use it for buy-sell funding that has to last a lifetime, or as a place to hold reserves with a death benefit attached. The trade-off is real, though: the premium is many times higher, the early cash value is modest, and the fees matter. Permanent life insurance is a legitimate tool, not a free lunch, and it should be sold to you with the costs on the table, not just the upside. Our explainer on how cash value life insurance builds shows where those dollars actually go in the early years.

| Factor | Term | Permanent (whole or IUL) |

|---|---|---|

| How long it lasts | A set number of years | For life, if funded |

| Cost per dollar of benefit | Low | Much higher |

| Builds cash value | No | Yes, over time |

| Best for | Temporary risk, loans, employee coverage | Lifetime needs, some buy-sell funding |

| Main trade-off | Ends with no payout if unused | Higher cost and fees to carry |

How a buy-sell agreement uses life insurance

A buy-sell agreement is a written contract among business owners that sets what happens to an owner's share if they die, leave, or become disabled. Life insurance is what funds it. When an owner dies, the policy provides the cash to buy that owner's share from their family at a price the agreement already set, so ownership passes cleanly and the surviving owners keep control.

This is the part most small business owners have never had explained to them, and it is the one that saves families and partnerships the most grief. Picture two owners, each with half the company. One dies. Without a plan, that half of the business now belongs to the deceased owner's spouse or kids, who may know nothing about the work and may want to be bought out immediately, sold to a stranger, or worse, want to run it themselves. A buy-sell agreement prevents all of that by settling the terms in advance. The life insurance makes sure the money to honor those terms actually exists.

There are two main ways to structure the funding, and the difference has real tax and paperwork consequences.

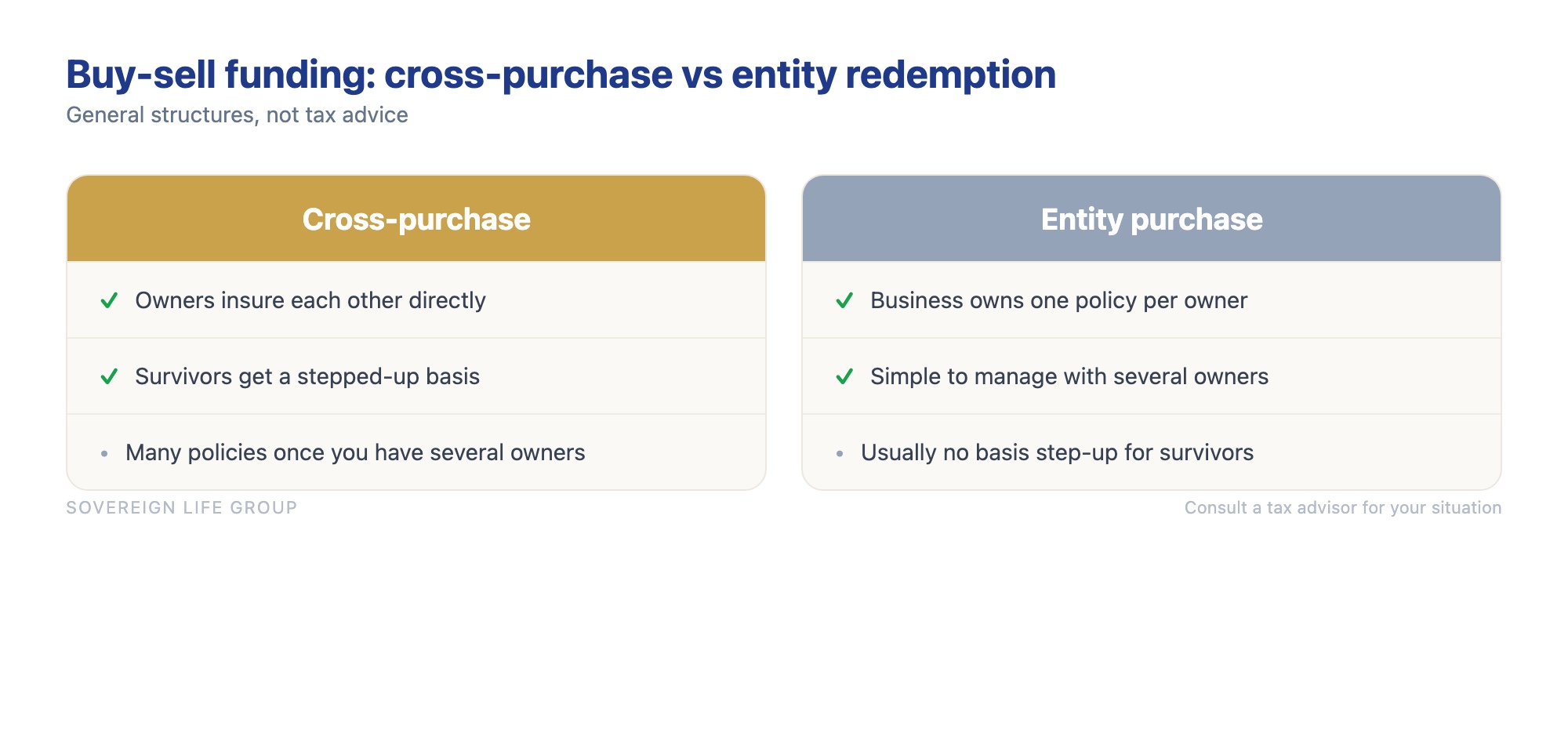

Cross-purchase

In a cross-purchase, each owner buys a policy on each of the other owners and is the beneficiary. When one dies, the survivors receive the benefit personally and use it to buy the deceased owner's share directly from the estate. The upside is that the surviving owners get a stepped-up cost basis in the shares they buy, which can lower their capital gains tax if they sell later. The downside shows up with more owners: three owners need six policies, four owners need twelve, and it gets unwieldy fast.

Entity purchase (stock redemption)

In an entity purchase, the business itself owns one policy on each owner and is the beneficiary. When an owner dies, the company collects the benefit and buys back, or redeems, that owner's share. It is far simpler with several owners, since each person needs only one policy owned by the business. The trade-off is that the surviving owners generally do not get the same basis step-up, and for C corporations there can be alternative minimum tax considerations on the benefit. This is exactly the kind of thing to run past a tax advisor before you choose.

Key person coverage and buy-sell coverage often get bought together, and people blur them, so let me draw the line clearly. Key person insurance protects the business from the economic loss of a person's productivity. Buy-sell insurance protects the ownership structure by funding the transfer of a share. A two-owner company frequently needs both: coverage so the business survives the lost work, and coverage so the surviving owner can buy out the departed owner's stake. One policy can sometimes be structured to serve a role in both, but they answer different questions, and a good review sizes each on purpose rather than hoping one covers the other.

The tax rules business owners get wrong

Here is the rule that trips up almost every owner: key person insurance premiums are generally not tax deductible. Because the business is the beneficiary, the IRS does not let you write off the premiums as a business expense under Internal Revenue Code Section 264. The trade-off is that the death benefit is usually received income-tax-free, as long as the notice and consent paperwork was handled correctly before the policy was issued.

Owners hear "life insurance for the business" and assume it is a deductible expense like the rent or the software. It is not, and treating it that way can cause problems at tax time. Think of it the way you think about paying premiums with after-tax dollars so the payout comes through clean. You give up the deduction now to get a tax-free benefit later, which for most businesses is the better end of the trade.

Two rules worth knowing by name

- Notice and consent (the 2006 rules). For employer-owned life insurance issued after August 17, 2006, the business must notify the insured in writing, get their written consent, and meet certain reporting requirements before the policy is issued. Miss this step and part of the death benefit can become taxable. It is a simple form. Skipping it is an expensive mistake, so make sure your agent handles it up front.

- Transfer-for-value. If a life insurance policy is sold or transferred for something of value, the death benefit can lose its tax-free status. This comes up when owners restructure a buy-sell or move policies between parties. There are safe-harbor exceptions, but it is a genuine trap, so loop in a tax professional before moving any policy around.

None of this is tax advice, and I am not your accountant. What I can tell you as an agent is that the paperwork matters as much as the policy, and the businesses that run into trouble are almost always the ones that treated the tax forms as an afterthought. You can read the ground rules straight from the IRS small business pages, and then confirm your specific setup with your own tax advisor before you sign anything.

A worked example with real numbers

Numbers make this concrete, so here is a simple, made-up example to show the mechanics. It is illustrative, not a quote or a real client, and the figures are round on purpose so the logic is easy to follow. Picture a small design-build firm with two owners and one irreplaceable lead estimator.

Say the firm does 4 million dollars a year in revenue. The two owners each hold 50 percent. The lead estimator, call the role "the estimator," earns 130,000 dollars a year and personally prices roughly 70 percent of the jobs the company wins. The business also carries a 600,000 dollar line of credit that the bank tied to the owners.

Sizing the key person policy on the estimator

Run the methods from earlier. Five to ten times compensation on 130,000 dollars points to somewhere between 650,000 and 1.3 million. The replacement-cost view, a recruiter fee, several months of overlap, and a productivity dip while a new estimator learns the firm's pricing, easily reaches 300,000 to 500,000 dollars of hard cost. The contribution-to-profit view is the scary one, because if the estimator drives 70 percent of won work, even a temporary stumble could cost the firm a meaningful slice of a year's profit. Weighing all three, a 1 million dollar term policy owned by the business on the estimator is a reasonable, defensible number. The premium for that, on a healthy person in their 40s, is often a manageable monthly cost rather than the budget-breaker owners fear.

Sizing the owner coverage and the buy-sell

Now the ownership side. Each owner's 50 percent stake needs somewhere to go if they die, so the two of them put a buy-sell agreement in place that values the company at, say, 3 million dollars, making each half worth about 1.5 million. They fund it with life insurance so that if one owner dies, the other has 1.5 million to buy the deceased owner's share from their family at the agreed price. Separately, they each carry enough coverage for the business to clear the 600,000 dollar line of credit so a lender is not chasing a grieving spouse.

Add it up and this modest two-owner firm is looking at a key person policy on the estimator, buy-sell funding on each owner, and enough to retire the loan. It sounds like a lot until you compare it to the alternative, which is a company that loses its best estimator or half its ownership overnight with no cash to respond. The premiums are a rounding error against 4 million dollars of revenue. The missing coverage is what actually threatens the business.

That is the pattern I see over and over. The coverage is affordable. The exposure is enormous. The only thing standing between the two is a conversation nobody scheduled.

How to set it up the right way

Setting up key person insurance is not complicated, but the order matters. Identify the people the business truly depends on, agree internally on why and how much, get the insured's written consent, apply with a carrier through an independent agent who can shop the market, and coordinate the policy with any buy-sell agreement and your tax advisor. Rushing the paperwork is where owners create problems.

Here is the path I walk business owners through, roughly in order.

- Name the key people honestly. Not everyone with a title, just the ones whose loss would actually hurt. Usually that is one to three people in a small business.

- Decide what the money is for. Replacing lost work, funding a buy-sell, repaying a loan, or all three. The purpose sets the amount and the policy type.

- Get written consent up front. The notice and consent form for employer-owned coverage is not optional. Handle it before the policy is issued, not after.

- Shop the market with an independent agent. Different carriers view age, build, and health conditions very differently. An agent who works with many A-rated carriers can find the one that treats your key person best. If you have a candidate with a health history, our overview of life insurance with health conditions is a useful read before you apply.

- Coordinate with the buy-sell and your advisors. Make sure the policy ownership matches the agreement, and run the structure past a tax professional so the transfer-for-value and consent rules are covered.

- Review it every couple of years. Businesses change. New key people emerge, loans get paid off, valuations climb. Coverage that fit three years ago may be too small or aimed at the wrong person now.

As a reference point on why this is worth doing at all, a lot of businesses run with the person the whole thing depends on completely uninsured. According to LIMRA's 2024 research, roughly 4 in 10 households say they would feel a financial strain within about six months if a primary wage earner died, and a big reason coverage lags is simply the assumption that it costs far more than it does. The same blind spot shows up in businesses that never insure their key people. You can also read general guidance on business coverage from the Insurance Information Institute before you talk to anyone selling it. When you are ready to price it for your own business, you can start with a clear, no-pressure look at your numbers from Sovereign Life Group, an independent life insurance strategist, or read more on our key person and business coverage page.

When you probably do not need it

An article that only says "buy more" is a sales pitch, not advice. Key person insurance makes sense when the loss of a person would genuinely damage the business. It makes far less sense for a solo operator with no employees and no debt, a business whose value lives in equipment or property rather than people, or a company with enough cash reserves to absorb the hit and hire calmly. Match the coverage to real exposure.

Some honest cases where you can skip it or buy less:

- You are a true solo business with no employees, no partners, and no business debt. There may be no key person to protect beyond your own personal life insurance for your family.

- The business could hire a replacement quickly without losing meaningful revenue, because the work is well documented and the relationships belong to the company, not one person.

- You hold deep cash reserves the business could use to weather the loss and recruit without pressure.

- The "value" is really assets, not people. A rental portfolio or an equipment-heavy operation may need property and liability coverage far more than key person coverage.

Even here, I would still ask one question before you close the book on it. Is there a loan somewhere with your name personally on it? Because if the answer is yes, your family could inherit that obligation, and a modest term policy is a cheap way to make sure they do not. The goal is right-sized coverage for real risk, not the biggest policy in the room.

Not sure who in your business is a key person?

Fifteen minutes. We will look at who the company truly depends on, how much coverage fits, and whether a buy-sell agreement belongs in the plan. No pressure, no jargon, just options laid out plainly.

Book a 15-Min Review Prefer to start small? Save my card and get a quick quote or talk through your business coverage with a licensed agent.Frequently asked questions

What is key person insurance?

Key person insurance is a life insurance policy a business buys on an owner or an employee the company cannot easily do without. The business owns the policy, pays the premiums, and is the beneficiary. If that person dies, the benefit gives the company cash to stay stable, hire a replacement, or repay debt.

Who pays for and owns a key person insurance policy?

The business does. The company applies for the policy, owns it, pays the premiums, and names itself as the beneficiary. The insured key person has to consent in writing and take part in underwriting, but they do not pay for it and their family is not the beneficiary. This is company-owned coverage, not personal coverage.

Is key person insurance tax deductible?

Usually no. Because the business is the beneficiary, the IRS generally does not let you deduct the premiums as a business expense under Internal Revenue Code Section 264. The trade-off is that the death benefit is generally received income-tax-free when the notice and consent rules are met. Confirm the details with your own tax advisor.

How much key person insurance do I need?

There is no single formula. Common approaches size it at five to ten times the person's compensation, the cost to find and train a replacement, that person's share of profits over a few years, or the amount a lender requires. Many owners take the highest reasonable figure their budget supports, because the loss is rarely small.

Can key person insurance fund a buy-sell agreement?

Yes, and it is one of the most common uses. A buy-sell agreement spells out what happens to an owner's share if they die, and life insurance provides the cash to actually buy that share. The policy can be structured as a cross-purchase between owners or as an entity purchase owned by the business.

Does a small business really need key person insurance?

If the company would lose real revenue, relationships, or its ability to repay a loan when one person is gone, then yes, it is worth pricing. A solo business with no employees and no debt may not need it. The honest test is simple: if that person did not show up again, would the business survive comfortably?

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation, and consult a qualified tax advisor about the tax treatment of any business-owned policy. Product availability, features, riders, and rates vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.