Can Your Employer Take Out Life Insurance on You?

The Short Version

Yes, your employer can take life insurance out on you, but only with your written consent. Federal law changed that in 2006. There are two completely different scenarios here: corporate-owned life insurance where the company benefits, and group term life insurance where your family benefits. Neither one is enough to replace a personal policy you own and control.

Clients ask me this all the time. Someone fills out new-hire paperwork, signs a form about life insurance, and wonders weeks later whether their company just took out a policy on their life. Can my employer take life insurance out on me? The short answer is yes, legally they can. But the picture has two very different sides, and mixing them up has real consequences for your family's financial security.

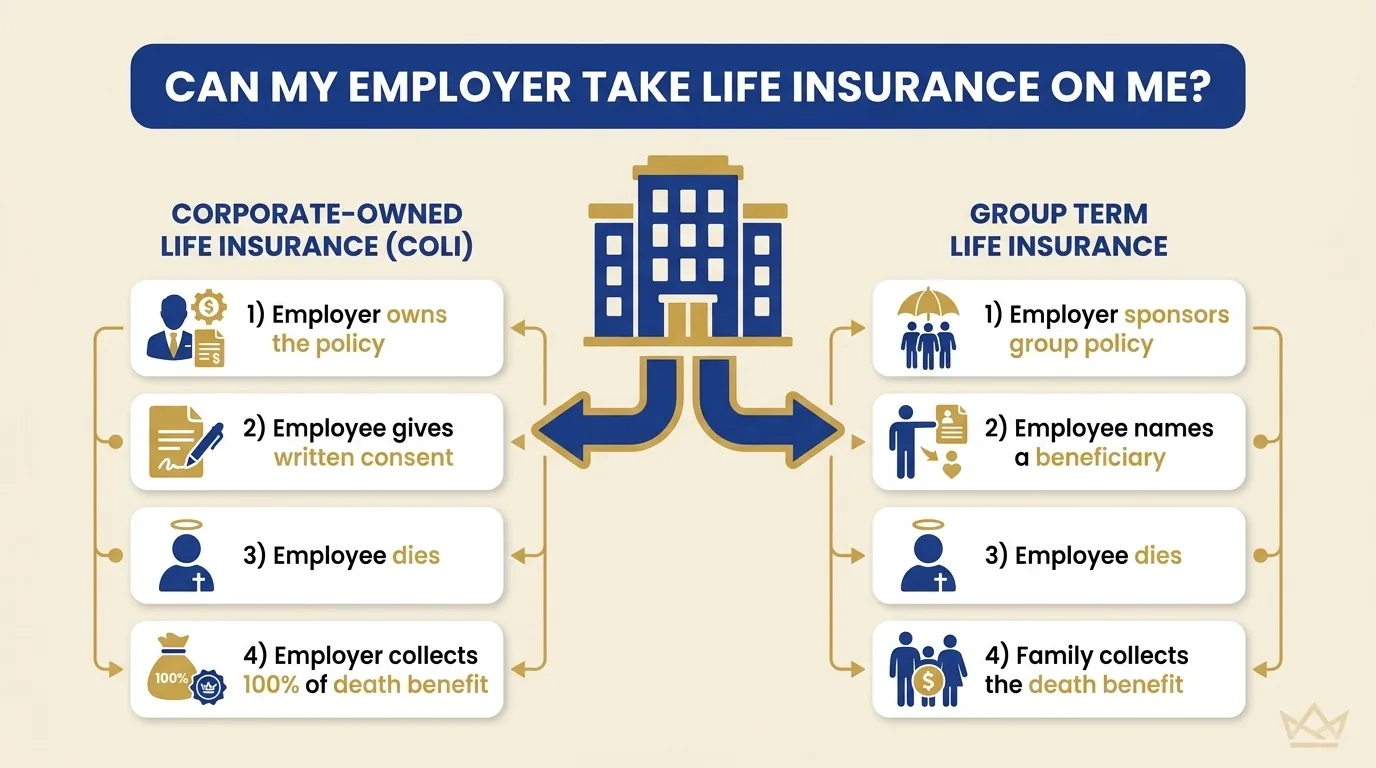

There are two completely different arrangements when employers get involved with life insurance. The first is corporate-owned life insurance, often called COLI, where the company buys a policy on your life and the company collects if you die. The second is group term life insurance, the benefit your HR department describes during open enrollment, where you are the insured, your family is the beneficiary, and the employer covers some or all of the cost. Same words floating around the same benefits paperwork. Opposite beneficiaries. Completely different financial experiences for your household.

This article walks through both, the federal law that governs consent, the controversial history behind employer-owned policies, and the practical decisions that actually matter for your family. If you've ever signed something at work and wondered what you agreed to, this will clear it up.

What this article covers

- Consent is required since 2006

- Two very different types of employer life insurance

- How corporate-owned life insurance works

- The dead peasants era and the 2006 law

- Key person insurance: what it means for you

- Group term: the benefit your employer buys for you

- Who actually collects when you die

- Your rights as the insured employee

- What happens to coverage when you leave

- Should you rely on employer life insurance alone?

- Frequently asked questions

Your employer can insure your life, but only with your written consent

Since August 2006, any employer who wants to take out a life insurance policy on an employee for the company's own benefit must give that employee written notice of the intent and receive written consent before the policy goes into force. A policy taken out without that consent does not give the employer a tax-free death benefit. That is a meaningful penalty, and it is the main reason the consent requirement has teeth.

The Pension Protection Act of 2006 added Section 101(j) to the Internal Revenue Code. Before that law passed, employers could and did insure employees without telling them. After August 17, 2006, any employer-owned life insurance contract must meet two conditions before the death benefit qualifies for income-tax exclusion. First, the employee must have received written notice before the policy was issued. That notice must state that the employer intends to insure the employee's life, the maximum face amount of coverage, and that the employer will be a beneficiary of the death proceeds. Second, the employee must have given written consent to be insured before the policy was issued.

If the employer skips either step, the death benefit becomes taxable income to the company when it is eventually paid. For a $5 million key person policy, that tax consequence is significant, which is why employers now take the consent documentation seriously.

According to IRS guidance published as IRS Notice 2009-48, employers who own life insurance on employees must also file Form 8925 annually, disclosing the number of employees covered, the total face amount of all employer-owned policies in force, and whether the required notice and consent procedures were followed. For public companies, portions of this are reflected in public filings.

The word consent is important to understand correctly here. You are not being asked whether the company is allowed to profit from your life. You are being told it intends to, and your signature acknowledges that. In most situations, especially key person arrangements, the business rationale is legitimate. But you have the right to understand what you're signing and to ask questions before you sign it.

No medical exam for a ballpark. Free, and no pressure.

Two very different types of employer life insurance

At the heart of the confusion is that the phrase "employer life insurance" gets used for two arrangements that share almost nothing beyond the word life insurance. One is a corporate financial tool. The other is an employee benefit. Getting them mixed up leads to a very dangerous assumption: that your family is protected when, under one type, they receive nothing.

Corporate-owned life insurance, or COLI, is a policy the employer owns and pays for. The employer names itself as beneficiary. When the covered employee dies, the company collects the death benefit. Your family has no claim on those proceeds unless a separate written arrangement says otherwise. Companies use COLI for specific business purposes: protecting against the financial impact of losing a key person, informally funding deferred compensation plans for executives, or holding a stable tax-advantaged asset on the balance sheet.

Group term life insurance is the familiar employee benefit. Your employer sponsors a group policy and pays some or all of the premium as part of your compensation package. You enroll, you name a beneficiary, typically a spouse or children, and if you die while employed, your named beneficiary collects the death benefit. This is the one your benefits guide describes.

| Factor | COLI (employer-owned) | Group term (employee benefit) |

|---|---|---|

| Who owns the policy | Employer | Employer (group contract) |

| Who pays premiums | Employer | Employer, sometimes with employee supplement |

| Who is the beneficiary | Employer | Your named beneficiary |

| Who collects at death | The company | Your family |

| Employee consent required | Yes, written consent since 2006 | Enrollment is voluntary |

| Portable when you leave | No, employer keeps the policy | No, usually ends with employment |

| Main purpose | Business protection or financial planning | Employee compensation benefit |

Both types exist in the same company at the same time. It's common for a business to offer group term life as a benefit to all employees while maintaining separate COLI on two or three executives whose loss would be most disruptive. If you're a senior leader, you may be covered under both simultaneously, though for very different reasons and with very different outcomes for your household.

How corporate-owned life insurance actually works

In a COLI arrangement, the employer applies for and owns a permanent or term life insurance policy on a covered employee. The employer pays all premiums and names itself as the sole beneficiary. If the insured employee dies while the policy is in force, the company receives the death benefit, which is income-tax-free to the employer if all the consent and notice requirements under Section 101(j) have been met. The employee's family receives nothing from this specific policy.

Why would a company do this? The reasons are practical, even if the arrangement sounds unusual from an employee's perspective.

Key person protection

The most straightforward use. A company that would face serious financial harm if its CEO, founder, or top-producing salesperson died buys a policy on that person. The death benefit can cover recruiting costs, give the company time to replace the revenue the person was generating, and fund any buyout obligations in a partnership or buy-sell agreement. Most lenders who extend credit to a business on the strength of one person require that person to be insured. The policy is sized to the business risk, not to the employee's personal financial needs.

Funding executive deferred compensation

Some companies use COLI as an informal funding vehicle for executive deferred compensation plans. A senior officer agrees to defer some current compensation in exchange for a larger payout at retirement. The company holds a permanent life insurance policy on that executive, the cash value accumulates tax-deferred, and the company eventually uses those assets to fund the deferred compensation obligation. The executive never owns the policy and has no direct claim on the cash value.

Bank-owned life insurance (BOLI)

Banks and financial institutions use a variation called BOLI, or bank-owned life insurance, to hold stable, tax-advantaged assets on the balance sheet. A bank purchases permanent life insurance on senior officers, the cash value appears as a bank asset, and the death benefit eventually offsets the cost of employee benefit programs. The Office of the Comptroller of the Currency issues separate guidance regulating BOLI for national banks.

In all of these uses, the employer is running a financial calculation. The life insurance is an asset or a risk management tool on their books. It is not a benefit to your household.

The dead peasants era and the 2006 law that ended it

Before 2006, companies could legally buy life insurance on any employee, at any level, without telling them and without their consent. Large retailers, banks, and manufacturers insured tens of thousands of employees in what critics labeled "dead peasants insurance." When those employees died, the company collected tax-free death benefits. The employees' families received nothing from those policies.

The name came from congressional critics drawing a comparison to feudal landlords who insured the lives of serfs. It was pointed. It stuck.

Wal-Mart Stores, Winn-Dixie Stores, American Express, and other large companies were publicly disclosed as holding broad-based COLI on rank-and-file workers, often without the workers' knowledge. A typical arrangement involved purchasing policies on thousands of employees, sometimes including former employees and retirees. When any of them died, the company collected the benefit. In some documented cases, surviving families learned about the policy only when they tried to collect on their own life insurance, discovered a policy existed, and found the company, not them, had been the named beneficiary all along.

The practice was legal. It generated substantial tax-free income for large corporations. And it generated exactly the kind of public outrage that moves Congress.

The Pension Protection Act of 2006, signed into law on August 17, 2006, added Section 101(j) to the Internal Revenue Code and effectively ended the broad-based version of the practice. For policies issued after that date, the death benefit under an employer-owned life insurance contract is only excluded from the employer's gross income if the employee received written notice and gave written consent before the policy was issued, and at least one of these conditions is met: the insured was an employee within 12 months of death, the insured was a director or highly compensated employee at the time the policy was issued, or the death benefit is paid to a family member of the insured or used to fund the purchase of a business interest from the employee's estate.

That third condition is what killed broad-based COLI on hourly workers. Under the post-2006 rules, a company cannot collect a tax-free death benefit on a front-line employee who left years before. The economic case for insuring thousands of warehouse workers evaporated.

Pre-2006 policies were grandfathered. Contracts in force before August 17, 2006 were not required to be restructured. Some of those policies may still be active. For new policies, the law represents a genuine shift in what employers can do and how it must be documented.

Key person insurance: what it means when your employer names you

Key person insurance, sometimes called key man insurance, is the most common form of employer-owned life insurance in use today. An employer buys a policy on a specific employee whose death would cause measurable financial harm to the business. The employer owns the policy, pays all premiums, and collects the entire death benefit. Your written consent is required before the policy can be issued.

The typical candidates are founders, chief executives, top salespeople who generate a disproportionate share of revenue, technical leads whose expertise would be nearly impossible to replace quickly, and partners in professional firms. If a company's lender has required key person coverage as a condition of a loan, the person being insured is usually whoever the bank considers essential to the business's ability to repay.

How the coverage is sized varies by carrier and by use case. Underwriters typically apply one of several approaches: a multiple of the key person's salary, a multiple of the revenue or profit that person generates, the outstanding loan amount the coverage is meant to secure, or an estimate of the equity value in a buy-sell agreement. Our breakdown of how key person and business life insurance works covers the sizing methods and the buy-sell connection in more detail. And if you are a business owner evaluating what coverage you need, the key person insurance page is a good starting point.

What key person coverage means for you personally

Your employer has concluded that your life has measurable financial value to the business. That is a legitimate recognition. But nothing in the policy protects your household. If you die holding only the employer's key person policy, your employer collects the benefit and your family receives nothing from that specific contract.

That reality gets lost in a lot of key person conversations. The HR paperwork, the consent forms, the discussion of "life insurance" at the executive level can all feel like something is being done for you. Something is being done about you, for the business. Your own coverage needs are entirely separate.

Can you decline?

Legally, yes. You have the right to withhold consent. A company cannot insure you for their tax-free benefit without your written agreement. Whether declining affects your employment relationship is a different and more practical question. For most executives, refusing consent for a key person policy tied to a business loan or a buy-sell agreement creates real friction. Most sign. But you are entitled to ask what you're signing, what the face amount is, who benefits, and whether any portion flows to your family before the ink goes down.

Get a fast, free estimate tailored to your age and health.

Group term life insurance: the benefit your employer provides for you

Group term life insurance is the product most employees think of when they hear "life insurance at work." The setup is straightforward. Your employer negotiates a group contract with a carrier. You enroll during open enrollment, name a beneficiary, typically your spouse or children, and the coverage is active as long as you work there and the employer maintains the policy. The premium is usually paid entirely by the employer or split between employer and employee at a subsidized rate.

What employers typically offer

Basic group term coverage is usually one or two times your annual salary, sometimes expressed as a flat dollar amount like $50,000. Most plans also offer supplemental elections where you can buy additional coverage, often in multiples of your salary up to five or eight times your annual pay. Higher elections sometimes require evidence of insurability, meaning a health questionnaire or brief exam, especially above a certain threshold. Basic coverage typically requires nothing beyond enrollment.

The no-exam feature is genuinely useful for employees with health conditions that would make individual underwriting expensive or complicated. For someone who has dealt with a significant diagnosis and struggles to qualify for standard rates individually, group enrollment at work can be the most accessible path to some coverage. It doesn't replace the need for an individual policy, but it can supplement it in ways worth using.

The tax treatment under Section 79

The first $50,000 of employer-provided group term life insurance is a tax-free benefit to you under Section 79 of the Internal Revenue Code. If your employer provides more than $50,000 of coverage, the IRS calculates "imputed income" on the excess using an age-based cost table from IRS Publication 15-B. At age 40, the imputed income on an additional $50,000 of coverage works out to about $8 per month in additional taxable income. Not a dramatic number, but it shows up as an addition to wages on your W-2.

The portability problem

Here is what rarely gets mentioned during open enrollment: you don't own this policy. Your employer does. When your employment ends, for any reason including a layoff, a merger, or simply accepting a better opportunity elsewhere, the coverage typically ends the same day. The timing can be brutal. Someone who has been relying on employer coverage for fifteen years, who now has a health history and is suddenly out of work, faces a very different market for individual coverage than they did at age 30 when they were healthy and employed.

Many group plans include a conversion option: a short window, usually 31 days after separation, to convert the group policy to an individual whole life policy without a medical exam. That sounds like a safety net. But whole life converted from a group plan at age 50 costs significantly more than a new individual term policy. If you're healthy and have options, you're almost always better off shopping individually. If your health has changed and you cannot qualify for favorable individual rates, the conversion option can be worth using, but it's not the plan you want to be counting on.

The mistake I see most consistently is employees who assume the group coverage at work is enough, then hit a health event, a job change, or a life change right when they would need to buy individual coverage. By that point, the rates have moved and the options have narrowed. The right time to buy your own policy is while you're healthy, not after you need it.

Who actually collects when you die

This depends entirely on which type of employer policy covers you. Under a COLI or key person arrangement, the employer is the beneficiary and collects the full death benefit. Your family receives nothing from that policy. Under a group term life insurance benefit, your named beneficiary collects the death benefit. The employer owns both contracts. The beneficiary is what determines where the money goes.

That distinction sounds obvious, but it gets lost in a surprising number of conversations I've had with clients who thought their work "had them covered" without understanding what that actually meant for their spouse and children.

A worked example

Say you're the director of sales at a mid-size company. Your employer holds a $600,000 key person policy on your life. You also have $90,000 of group term coverage through your benefits package, with your spouse named as beneficiary.

You die unexpectedly.

Your employer collects $600,000 from the key person policy. They use those funds to manage the transition, cover the revenue gap during the search for your replacement, and satisfy any obligation to their lender who required the coverage. Your family receives none of it.

Your spouse collects $90,000 from the group term policy. That is the benefit your employment relationship provided for your household.

If $90,000 is not close to replacing your income, covering the mortgage, or giving your family time to stabilize, which for most households it isn't, the remaining gap is the part your own individual policy would have covered. Getting your beneficiary designation right is also essential. The wrong person named, or a designation never updated after a divorce, can redirect that $90,000 away from the people who need it. If you are not sure what that number should be, our guide on how much life insurance you actually need walks through the math.

Split-dollar arrangements

Some companies, particularly at the executive level, use a split-dollar arrangement that divides either the premiums or the death benefit between the employer and the employee. Under a split-dollar plan, the employee or the employee's family might receive a portion of the death benefit, or the right to transfer the policy at some point. These arrangements carry their own tax rules under Treasury Regulation 1.61-22 and IRS Notice 2002-8. If anyone at your company mentions a split-dollar plan with your name on it, the plan documents are worth reviewing with an advisor before you sign anything. The economic terms matter and they vary widely.

Your rights as an insured employee

Since the Pension Protection Act of 2006, you have the right to written notice before your employer takes out a life insurance policy on you for the company's benefit. That notice must tell you in writing that coverage is being purchased, the maximum face amount, and that the employer will receive some or all of the proceeds. You have the right to give or withhold written consent. The employer cannot take out a COLI policy that qualifies for tax-free death benefits without that signed acknowledgment.

What the notice must include

The IRS does not require a specific form, but the written notice must communicate three things: that the employer intends to insure your life, the maximum dollar amount of coverage being purchased, and the fact that the employer will be a beneficiary of the death proceeds. Notice that is vague or that omits the face amount does not satisfy the legal requirement. If you receive a consent form and the coverage amount is blank, ask for that number before you sign.

Can you refuse?

Yes. Your written consent is a legal requirement, not a courtesy. You can decline to sign. The company cannot issue a qualifying COLI policy on your life without it. What that refusal means for your employment relationship depends on your role. A key executive declining consent on a key person policy tied to a business loan is a more complicated conversation than an ordinary employee asked to sign. But the right to decline is real and it's yours.

Finding out what your employer holds

If you want to know whether your employer currently holds a COLI policy on your life, ask HR directly. Publicly traded companies file Form 8925 with the IRS annually, disclosing the total number of employees covered under employer-owned policies and the aggregate face amount. The form itself is part of the corporate tax return, and the total figures are disclosed in the notes to financial statements for public companies. If you work for a corporation that makes its annual report public, the disclosure is there.

What happens to your coverage when you leave your job

Group term life insurance through your employer typically ends when your employment ends. No grace period, no automatic continuation. In most plans, your coverage runs to the end of the month in which you separate. After that, you're on your own unless the plan includes a conversion or portability option.

Conversion

Most group term plans offer a conversion right: a window, usually 31 days from your separation date, to convert your group coverage to an individual whole life policy issued by the same carrier. You don't need a medical exam. The coverage converts automatically if you elect it and pay the premium.

The catch is cost. Whole life insurance converted from a group plan is priced based on your age and the carrier's individual rates for a permanent policy, not the group rate you were paying. For a 45-year-old converting $200,000 of coverage, the premium is often two to four times what that same person would pay for a new individual term policy if they are in good health. The conversion option is a safety net for people who have developed health conditions that would otherwise make individual underwriting difficult. It's not a good deal for someone who can qualify for standard individual rates. Use the window to get covered quickly if health is the issue. Skip it and shop individually if you can qualify.

Portability

Some group plans include a portability provision, separate from conversion, that lets you continue the term coverage at the group rate for a limited period after separation. Not all plans offer this. If portability is available in your plan, the election window is typically the same 31 days. Check the terms during employment, not after you've received the separation notice.

What happens to the COLI policy on you

Any corporate-owned life insurance your employer holds on your life stays with your employer when you leave. The policy does not transfer to you. The employer continues to own it and pay premiums as long as they choose. The 2006 law does limit the tax-free treatment: to qualify for income-tax exclusion on the death benefit, the insured employee generally must have been an employee within 12 months of death. Employers typically review COLI policies when key people separate. But the policy itself is their asset, not yours.

Should you rely on employer-provided life insurance alone?

For most families, employer group term life insurance is not enough on its own. Not because the benefit is worthless, it isn't. But one to two times your annual salary covers a fraction of what your household actually needs to remain financially stable if you're gone.

According to LIMRA's Insurance Barometer research, a significant portion of Americans who have life insurance rely solely on their employer-provided plan. The same research consistently shows that those households are underinsured, sometimes severely. The typical recommendation from financial planners is ten to twelve times your income, plus outstanding debts, plus any major near-term expenses like childcare or college. For a household earning $75,000 a year with a $236,000 mortgage and two kids, the real coverage need is close to $1 million. Employer group term at one times salary covers $75,000 of that.

The math isn't the only problem. There's also the control problem. You don't own your employer's group policy. Your employer does. A layoff, a company merger, a benefits cost-cutting decision, or a career move you make by choice can end that coverage on short notice. The worst version of this I've seen: a client who had relied on work coverage for fifteen years, developed a health condition, then got laid off during a company restructuring. Buying individual coverage at that point was expensive and limited. The window they had for a cheaper, healthier rate had closed years earlier.

Individual term life insurance stays with you through every job change. The premium is locked for the full term. The coverage can't be cancelled by a company decision. And buying it while you're young and healthy, before any diagnosis enters the picture, is reliably cheaper than buying it later.

My recommendation to every client who brings up their work coverage: treat the employer policy as a supplement. Use it while you have it, because it's often free or close to it. But do not count on it as your family's primary protection. Get your own policy while your health is on your side and while the rates still favor you. The difference between buying at 32 and buying at 47 is not small.

If you want to see what life insurance through Sovereign Life Group actually costs for your situation, or you're not sure whether what you have at work is enough, the fastest path is a short conversation with no commitment. And if you'd rather start with a quick written question, reaching out directly works just as well. I'll tell you what I actually see in your situation, not what's most profitable for me to recommend.

For a deeper look at how individual term compares to whole life and which option fits different households, the breakdown of term versus whole life insurance is worth reading before you make a decision.

Not sure your work coverage is enough?

Most people don't know what they actually need until they see their household numbers on paper. Takes about fifteen minutes to figure out, and the answer is often simpler than expected.

Check My Coverage Book a 15-Min Review Or start with the key person insurance page if you're a business owner evaluating your own coverage needs.Frequently asked questions

Can my employer take out life insurance on me without my knowledge?

No, not legally since August 2006. The Pension Protection Act added Section 101(j) to the Internal Revenue Code, which requires employers to give written notice and obtain written employee consent before issuing an employer-owned life insurance policy. If an employer skips that step, the death benefit becomes taxable income to the company. Before 2006, employers could and did insure employees without their knowledge. Policies issued before August 17, 2006 were grandfathered.

What is COLI or dead peasant insurance?

COLI stands for corporate-owned life insurance. It's a policy an employer buys on an employee's life where the employer is the beneficiary and collects the death benefit. The nickname "dead peasants insurance" refers to the pre-2006 practice of large corporations insuring thousands of low-level employees without consent. When those employees died, the company collected a tax-free payout while the employee's family received nothing from the policy. The 2006 Pension Protection Act ended the broad-based version of this practice.

Does my family get any money from my employer's COLI policy?

Generally no. In a standard corporate-owned life insurance arrangement, the employer is both the policy owner and the beneficiary. The full death benefit goes to the company. Your family receives nothing from that specific policy. Some split-dollar arrangements, typically at the executive level, share a portion of the benefit with the employee's family, but that must be specifically written into the plan documents before the policy is issued.

What is key man insurance and does it require employee consent?

Key person or key man insurance is the most common form of employer-owned life insurance in use today. The employer insures a high-value employee, such as a founder, CEO, or top salesperson, to protect the business from the financial loss that person's death would cause. Yes, your written consent is legally required before the policy can be issued under post-2006 rules. The employer collects the entire death benefit. Your family receives nothing from this policy unless a separate arrangement says otherwise.

Is the life insurance my employer provides enough coverage?

For most families, no. Typical employer group term life insurance covers one to two times your annual salary. Most financial guidance recommends ten to twelve times income plus outstanding debts. A household earning $75,000 per year might have $75,000 to $150,000 of employer coverage but genuinely need $800,000 to $1,000,000 or more to protect the family long-term. Employer coverage is a useful supplement. It is not a complete plan on its own, and it ends the day your employment ends.

What happens to my employer life insurance if I quit or get fired?

Group term life insurance through your employer usually ends when your employment ends, typically at the end of that month. Some plans offer a conversion option, letting you convert to an individual whole life policy within a 31-day window without a medical exam. That converted policy almost always costs significantly more than a new individual term policy purchased while in good health. Any corporate-owned life insurance your employer holds on your life stays with the employer even after you leave. It does not transfer to you.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is for educational purposes only and is not financial, tax, or legal advice. Consult a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, and carrier. Any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company. IRS guidance referenced in this article includes Section 101(j) of the Internal Revenue Code and IRS Notice 2009-48.