Do I Need Key Man Insurance? A Business Owner's Guide

The Short Version

Key man insurance is a life insurance policy a business owns on a person it cannot easily afford to lose. If that person dies, the company gets a cash payout to survive the hit. You need it when one individual carries a big share of your revenue, relationships, or financing. You probably do not if the business would run fine without any single person.

Every business owner I talk to can name the one person the whole thing leans on. Sometimes it is the founder. Sometimes it is the salesperson who books half the revenue, or the partner the bank actually trusts. So when an owner asks me "do I need key man insurance," what they are really asking is: if that person did not show up tomorrow, does the company survive the year? This guide answers that honestly. We will cover what key man insurance is, who counts as a key person, how a claim pays, what it costs, how much to buy, how the tax treatment works, and the cases where you can skip it.

I write this as a licensed agent who places this coverage, not as a marketer chasing a sale. Part of doing it right is telling some owners they do not need it, or need less than they were pitched. That is in here too.

What this guide covers

- What key man insurance actually is

- Do I need key man insurance? The signs

- Who counts as a key person

- How key person insurance works

- What key man insurance costs

- How much coverage your business needs

- Key man insurance vs a buy-sell agreement

- How key person insurance is taxed

- Term or permanent for key coverage

- When you probably do not need it

- How to put a policy in place

- Frequently asked questions

What key man insurance actually is

Key man insurance, also called key person insurance, is a life insurance policy that a business buys on an owner or employee whose loss would seriously hurt the company. The business owns the policy, pays the premiums, and is the beneficiary. If that person dies, the company collects the payout and uses it to stay afloat.

That last part is what makes it different from the life insurance you might own personally. Your own policy pays your family. A key man policy pays your business. Same underlying product, a death benefit funded by premiums, aimed at a completely different problem. The purpose here is not to take care of a spouse and kids. It is to give the company enough cash to absorb the loss of someone it depends on, so a death does not turn into a second crisis on top of the first.

You will hear a few names for the same idea: key man insurance, key person insurance, key employee coverage, business life insurance. Do not get hung up on the label. "Key man" is just the old term that stuck. Plenty of key people are women, and the coverage works exactly the same. The point of the key person insurance purpose is simple: buy the business time and money to recover.

No medical exam for a ballpark. Free, and no pressure.

Do I need key man insurance? The signs your business is exposed

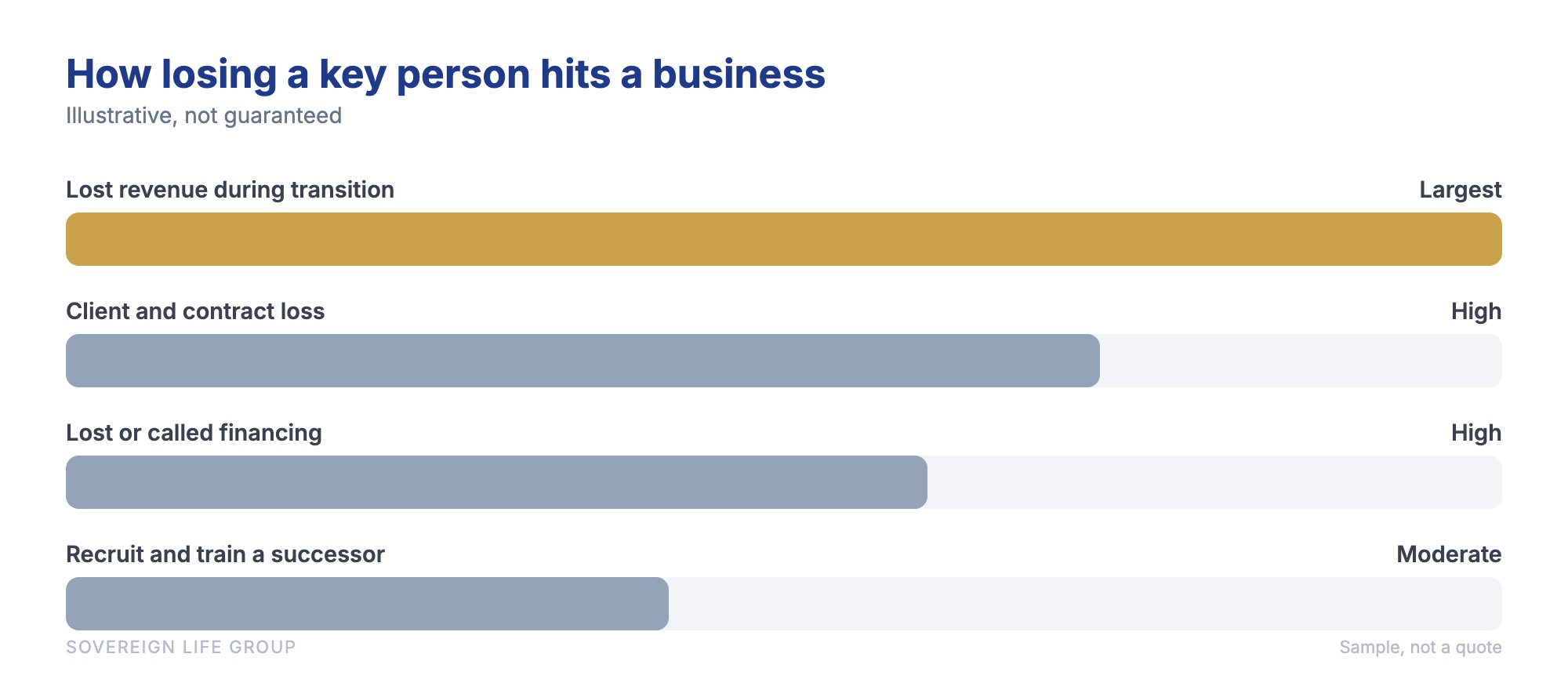

You need key man insurance when the death of one specific person would cause a real financial hit to your company, through lost revenue, lost relationships, or lost access to credit. If your business would run fine without any single individual, you probably do not need it. The honest test is dependence, not how many people are on payroll.

So the question "do I need key man insurance" is really a question about how concentrated your risk is. Here is where I usually see that concentration show up. Read these and be honest with yourself.

- One person drives a big slice of revenue. A founder who is the face of the company, or a producer who personally owns the top client relationships. If they are gone, so is a chunk of the top line, at least for a while.

- A lender or investor requires it. This is the reason a lot of owners find out about key man coverage in the first place. Banks and SBA lenders often want a policy on the owner as a condition of the loan, so the debt is covered if you die before it is repaid.

- You have partners. If two or three people own the business, the death of one throws ownership, control, and cash flow into question all at once.

- Someone holds knowledge or relationships nobody else has. The engineer who built the system. The estimator every bid runs through. The person the biggest customer only wants to deal with.

- The business personally depends on the owner's credit or guarantee. Many small business debts are personally guaranteed. If the guarantor dies, that can trigger real problems with the note.

The mistake I see most is an owner assuming the business "would just figure it out." Maybe it would. But figuring it out costs money and time, usually at the worst possible moment, while the team is grieving and clients are nervous. Key man coverage does not stop any of that pain. It just makes sure the company has cash in the bank while it works through it. That is the whole key person insurance purpose in one sentence. If you want to go deeper on how carriers structure this for companies, our overview of key person and business life insurance breaks it down further.

Who counts as a key person

A key person is anyone whose death would financially wound the business. That is usually the owner or founder, but it is not only them. A top salesperson who books a large share of revenue, a partner, a lead engineer, or a manager who holds the key client relationships can all qualify. The title matters less than the size of the hole they would leave.

When I sit with an owner to figure out who to insure, I ask one blunt question: if this person died next month, which line on your financials moves, and by how much? The people whose absence would move revenue, cost, or your ability to borrow are your key people. Here is who commonly makes the list.

The owner or founder

In most small businesses the owner is the business. They hold the vision, the banking relationship, the biggest accounts, and often the personal guarantee on the debt. For a lot of companies this is the only key person policy they will ever need, and it is usually the first one to put in place.

A top producer or rainmaker

Some companies have a salesperson or partner who personally controls a large share of revenue. If half your sales walk out the door with one person, that person is a key person, full stop, even if they do not own a single share of the company.

A technical or operational expert

This is the one owners forget. The person who wrote the code the whole product runs on, or the operations lead who is the only one who truly understands how the machine works. Losing them does not just cost a salary. It can stall delivery for months while you rebuild what lived in their head.

A partner or co-owner

When there is more than one owner, each of them is usually a key person, and there is a second layer to plan for around ownership itself. That is where buy-sell coverage comes in, which we get to below.

How key person insurance works, from application to payout

Key person insurance works like this: the business applies for a policy on the key individual, with that person's written consent, then owns and pays for the coverage. The insured goes through normal underwriting. If they die while the policy is in force, the business files a claim and receives the death benefit, tax-free in most cases, to spend as it needs.

Let me walk the steps, because the ownership setup trips people up.

The business applies and the person consents

The company is the applicant, owner, and beneficiary. The employee or owner is the insured, and they have to agree in writing to be covered. That consent is not just a courtesy. Under current tax rules, getting written notice and consent in place before the policy is issued is what keeps the death benefit income-tax-free later. Skip that step and you can accidentally make the payout taxable.

Underwriting happens on the insured person

The insured answers health questions and, depending on the amount and their age, may take a brief medical exam. Their age, health, and the coverage amount drive the price, the same way they would on a personal policy. A healthy 40-year-old will pay far less per dollar of coverage than a 60-year-old with a health history.

The company pays the premiums and keeps the policy in force

As long as the business pays, the coverage stays active. If the business ever wants to insure a different person, say the key employee leaves, some policies can be surrendered or, in certain cases, transferred, though a transfer has its own tax wrinkles worth a conversation with your accountant first.

If the insured dies, the business collects and decides how to use it

The company files the claim and receives the benefit. There are no strings on how the money is spent. Owners typically use it to cover payroll during the gap, pay down or pay off business debt, hire and train a replacement, reassure lenders and clients, or in a worst case fund an orderly wind-down that protects the family's remaining equity instead of a fire sale. That flexibility is the point.

What key man insurance costs and what drives the price

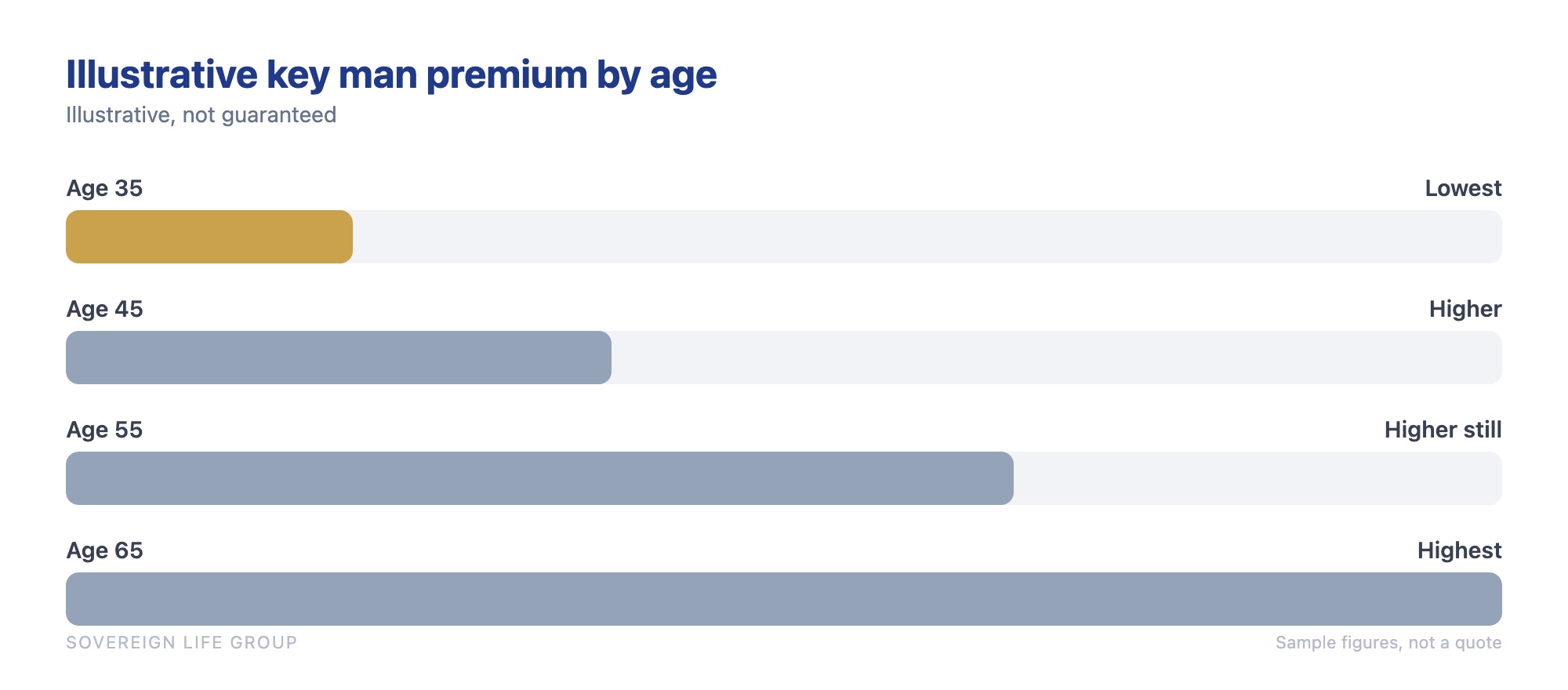

Key man insurance is often cheaper than owners expect, especially with term coverage. Price depends mostly on the insured person's age and health, the amount of coverage, the term length, and whether you choose term or permanent. A healthy person in their 30s or 40s can often be covered for a modest monthly premium relative to what the company would lose.

No honest agent can quote you a real number from an article, and you should be skeptical of anyone who does. What I can do is show you which direction each factor pushes the price.

| Factor | Effect on price | Why |

|---|---|---|

| The insured's age | Older costs more | Risk of a claim rises each year, so the premium rises with it |

| The insured's health | Better health, lower price | The rate is built on their health at the time of application |

| Tobacco use | Smokers pay much more | Underwriting treats nicotine as a major risk factor |

| Coverage amount | More benefit, more premium | A larger payout costs more to insure |

| Term length | Longer term, higher price | The insurer is on the hook for more years |

| Term vs permanent | Permanent costs more | It lasts for life and can build cash value the business owns |

| Underwriting type | No-exam often costs more | Skipping the exam shifts risk to the insurer, who prices for it |

Here is the part worth sitting with. The cost of the coverage is almost never the real question. The real question is what the loss would cost the business. If a term policy runs a few hundred dollars a month and the person it covers drives a million dollars of profit, the math is not close. I have watched owners agonize over the premium and completely skip past the size of the exposure it protects. Price the risk first, then the premium tends to look small.

One more note on timing. The rate is set by the version of the insured who applies, and their health today is, on average, the best it will be going forward. Waiting rarely makes coverage cheaper. Our companion piece on the best age to buy life insurance walks through why that is, and the same logic applies to insuring a key person.

How much coverage does your business need

There is no single formula for how much key man insurance to buy. Most owners size the benefit using some mix of the profit the person drives, a multiple of their compensation, the cost to recruit and train a replacement, and any business debt they personally guarantee. Many small businesses land between five and ten times the person's pay, then adjust up for debt and revenue impact.

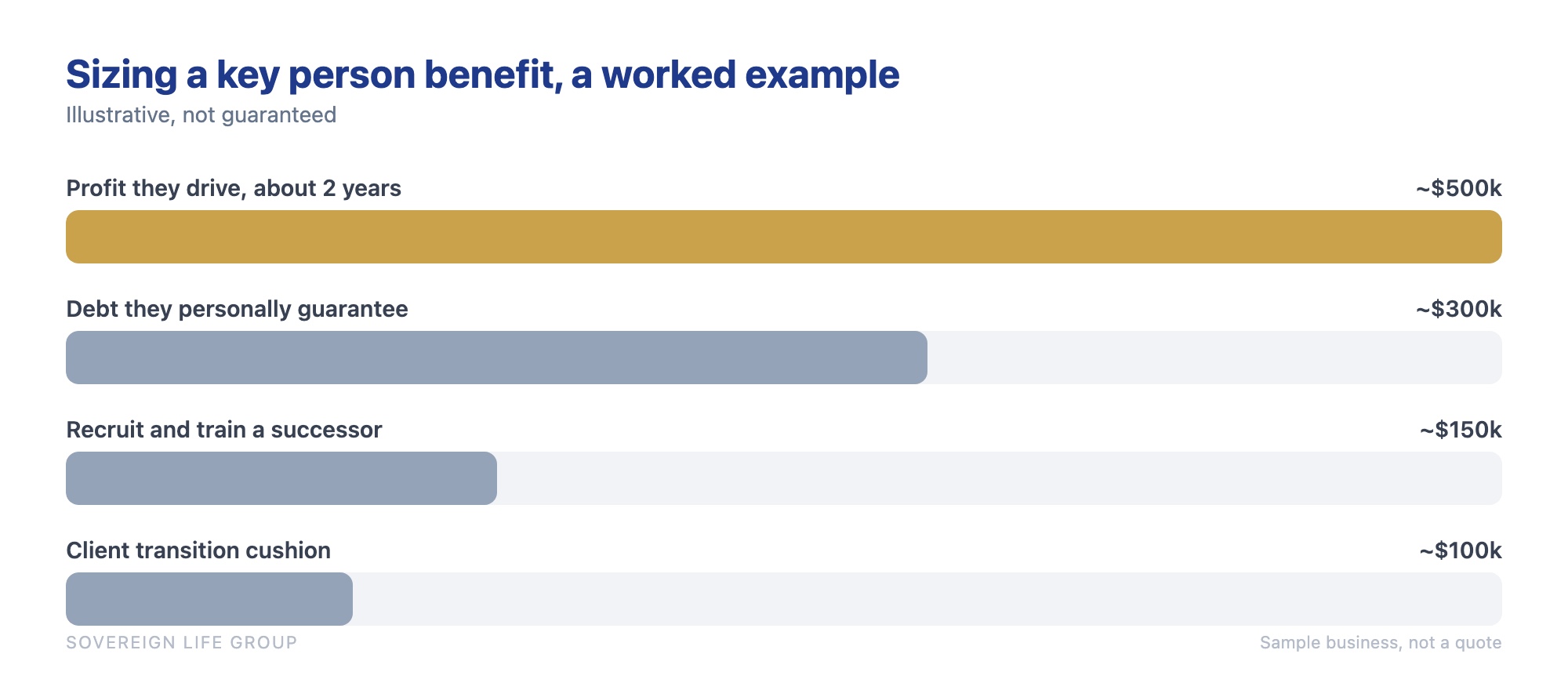

Formulas are a starting point, not the answer. I would rather build the number from what the money actually has to do. Let me show you with a hypothetical, so the pieces are concrete. These figures are illustrative, not a quote.

Say you run a small design firm. Your lead partner personally manages the accounts that produce about 250,000 dollars a year in profit. Here is one way to size a benefit for them.

- Replace the profit while you recover. If it would take roughly two years to rebuild those relationships, that is about 500,000 dollars of profit to bridge.

- Clear the debt they backstop. Suppose the firm carries a 300,000 dollar loan the partner personally guaranteed. You may want the payout to retire it so the note does not become a problem.

- Fund the search and ramp. Recruiting, hiring, and training a capable replacement might run 150,000 dollars once you count the salary overlap and lost productivity during ramp-up.

- Add a cushion for client transition. A little extra, say 100,000 dollars, to keep clients calm and cover the accounts that drift away during the change.

Stack those and you are near 1,050,000 dollars, so you might round to a 1,000,000 dollar policy. A different business would weight these pieces differently. A company with no debt and an easily replaced role needs far less. A firm where one person is the entire sales engine might need more. The point is to build the number from your actual exposure, not to pull a multiple out of the air and hope.

One caution from experience: do not oversize it just because a bigger policy sounds safer. Insurers will underwrite the amount against the person's actual economic value to the business, and a benefit wildly out of line with that value can get questioned or trimmed. Right-size it to a number you can justify on paper.

Get a fast, free estimate tailored to your age and health.

Key man insurance vs a buy-sell agreement

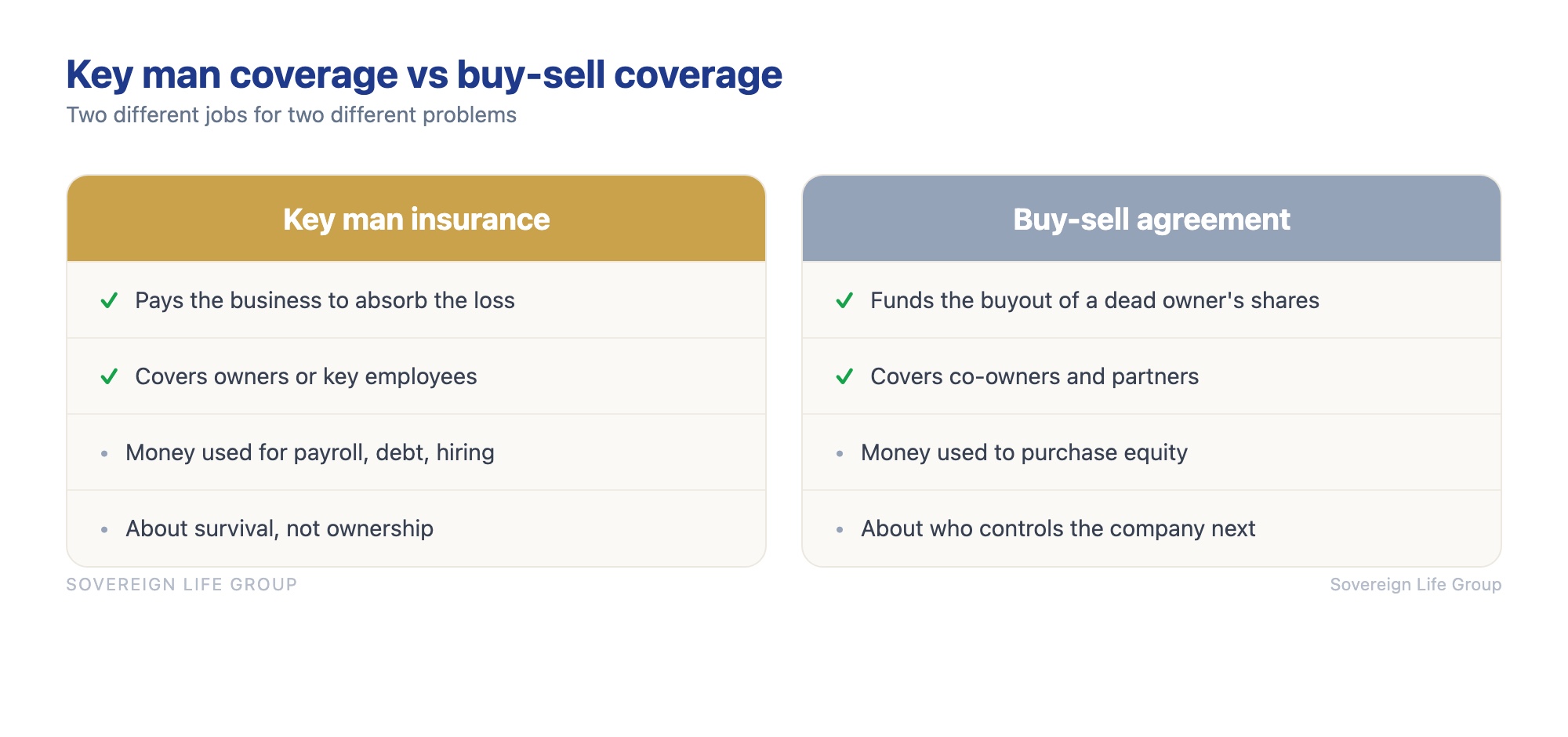

Key man insurance and a buy-sell agreement are both funded with life insurance, so people mix them up, but they solve different problems. Key man coverage pays the business to survive the loss of a key person. A buy-sell agreement funds the purchase of a deceased owner's shares so the surviving owners keep control. Many businesses with partners need both.

Picture a two-owner company. If one partner dies, two separate problems land at the same time. First, the company just lost half its leadership and maybe a big share of its revenue. That is the key man problem, and key man insurance is the fix. Second, that partner's ownership stake now belongs to their estate, which usually means their spouse or heirs, people who may know nothing about running the business and would rather have cash. That is the buy-sell problem.

A buy-sell agreement, funded with life insurance, solves the second one. The agreement says that when an owner dies, the surviving owners (or the company) will buy the shares at an agreed value, and the insurance provides the cash to do it. The heirs get a fair price, the surviving owners keep clean control, and nobody ends up in business with a grieving spouse who never signed up for it.

| Question | Key man insurance | Buy-sell agreement |

|---|---|---|

| What problem does it solve? | The business losing a vital person | The transfer of a dead owner's shares |

| Who is covered? | Owners or key employees | Co-owners and partners |

| Where does the money go? | Into the business to keep it running | To buy the deceased owner's equity |

| What is the goal? | Survival and continuity | Clean ownership and control |

| Who typically needs it? | Any business with a key person | Businesses with two or more owners |

If you own a business with partners and you only have one of these two, you have a gap. It is worth mapping both on the same afternoon so you are not solving one problem while ignoring the other. You can reach out and talk it through with a licensed agent before you commit to anything.

How key person insurance is taxed

In most cases, premiums on key man insurance are not tax deductible, and the death benefit is received income-tax-free. The tradeoff is intentional: because the business cannot deduct what it pays in, the government generally does not tax what comes out. To keep the payout tax-free, the employer-owned life insurance notice and consent rules must be met before the policy is issued.

That notice and consent step is the one owners skip and later regret. The rules around employer-owned life insurance, added to the tax code back in 2006, require that before the policy is issued the employee is told in writing that the business will insure them and be the beneficiary, and that they consent to it. The business also files a form with its return each year to report these policies. Get that paperwork right up front and the benefit is normally income-tax-free. Get it wrong and part of the payout can become taxable, which defeats much of the point. You can read the government's own summary of the employer-owned life insurance reporting rules on IRS.gov, and you should confirm your setup with a tax professional, because this is exactly the kind of detail that is easy to fumble.

A couple of other tax notes worth knowing. If the business is a C corporation, a large tax-free benefit can interact with the corporate alternative minimum tax in some situations, so run big policies past your accountant. And if you ever transfer an existing policy to a new owner for value, the transfer-for-value rules can pull the death benefit into taxable income. None of this should scare you off. It just means the setup deserves a few minutes with someone who does tax for a living, not a handshake.

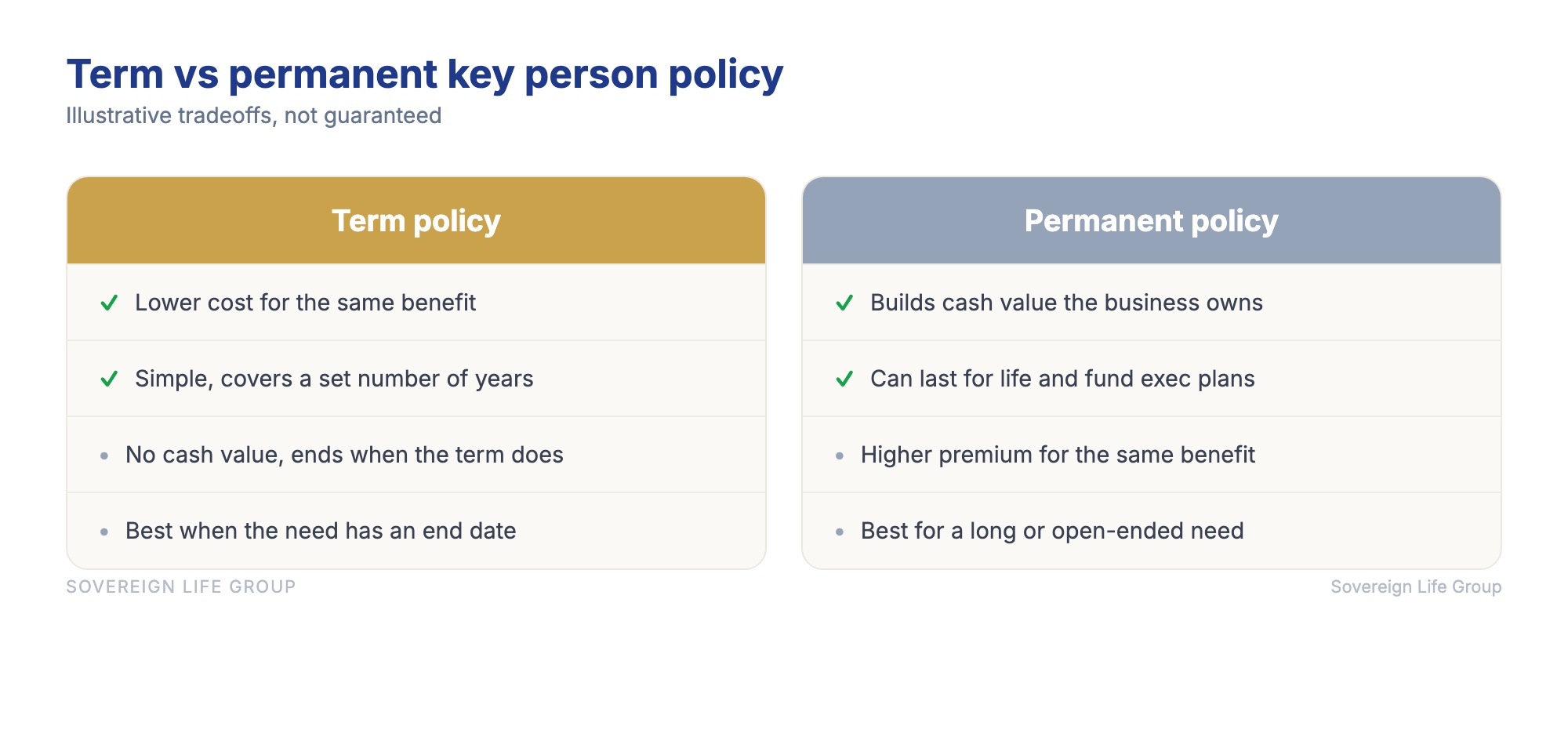

Term or permanent for key person coverage

Key person coverage comes in term and permanent versions. Term is cheaper and covers a set number of years, which fits a need with an end date, like a loan payoff or the years until a successor is ready. Permanent costs more but lasts for life and builds cash value the business owns, which can double as a retention tool for the key person.

Most of the time, for a straightforward "protect the business if this person dies in the next 10 to 20 years" need, term does the job for the least money. It is clean, it is affordable, and it lines up neatly with a loan term or a planning horizon. If that is your situation, term is usually where I start.

Permanent coverage earns its higher premium when the need does not have an expiration date, or when you want the policy to do a second job. Because a permanent policy builds cash value the company owns, some businesses use it as the backbone of an executive bonus or retention plan, a way to keep the key person and insure them at the same time. Indexed universal life is one structure owners ask me about for this, and the tradeoffs there deserve their own conversation, which our overview of how a key person and business coverage program is built gets into. The right answer depends on how long the need lasts and whether you want an asset at the end of it. If you want the broader term-versus-permanent picture first, our breakdown of term versus whole life insurance lays out the structural differences.

When you probably do not need key man insurance

You probably do not need key man insurance if no single person's death would meaningfully hurt the business. If your revenue, relationships, and financing are spread across a team, if the roles are easily filled, or if the company holds enough cash to weather a loss on its own, a key person policy may be coverage you do not need. Honest advice includes when to say no.

Here are the cases where I tell an owner to hold off or buy less.

- No one is irreplaceable. If any role could be filled in weeks without a real revenue dent, there may be no key person to insure.

- The business already has deep reserves. A company sitting on enough cash or a strong line of credit to absorb the loss may not need to insure against it.

- You are being sold a huge permanent policy when a small term one fits. If the need has a clear end date, paying for lifelong coverage and cash value can be more product than the problem calls for.

- The "key person" is really a personal need in disguise. If the goal is to take care of the owner's family, that is personal life insurance, owned by the individual, not a key man policy owned by the business. Do not blur the two.

An article that only ever says "buy more" is a sales pitch, not advice. The goal is coverage that matches your actual exposure. Sometimes that is a seven-figure policy on the founder. Sometimes it is nothing at all, and the right move is to keep your premium and put it back into the business.

How to put a policy in place without overpaying

Setting up key man insurance is straightforward once you know the order of operations. Identify the key person and the exposure, size the benefit, choose term or permanent, get the written notice and consent in place before issue, then apply with the business as owner and beneficiary. A licensed agent who shops multiple carriers keeps the price honest.

Here is the practical path, in the order I would walk a fellow owner through it.

- Name the key person and the real exposure. Be specific about which line on your financials moves if they are gone, and by how much. That number anchors everything else.

- Size the benefit to the job. Use the build-up from the sizing section: lost profit, debt, replacement cost, a cushion. Justify the amount so underwriting goes smoothly.

- Choose term or permanent on purpose. Match the coverage length to how long the need lasts. Do not buy permanent for a temporary problem, or term for a lifelong one.

- Handle the notice and consent first. Get the employee's written consent in place before the policy is issued so the death benefit stays tax-free. This is the step people skip.

- Set ownership and beneficiary correctly. The business owns it, pays for it, and is the beneficiary. Confirm this in writing so there is no confusion at claim time.

- Use an agent who shops carriers. Health and business type affect which carrier is most favorable. One agent presenting one product is a flag. You want options and tradeoffs.

As a reference point on how underinsured businesses tend to be, according to research published by LIMRA, a large share of small business owners recognize they need more coverage than they carry, and cost is consistently overestimated as the reason to wait. The Insurance Information Institute is another neutral place to read up on how business life insurance is structured before you talk to anyone selling it. When you want a clear, no-pressure look at your own numbers, you can start with Sovereign Life Group, your life insurance strategist.

Want a straight answer for your business?

Fifteen minutes. We will map your key people, size a sensible benefit, and lay out term versus permanent in plain English. No pressure, no jargon, just options.

Book a 15-Min Review Prefer to start online? Save my card and get a quick quote and I will follow up.Frequently asked questions

Do I need key man insurance for a small business?

If losing one specific person would sharply cut your revenue, put your financing at risk, or make it hard to keep the doors open, then key man insurance usually makes sense. A business that would run fine without any single individual probably does not need it. The test is dependence, not headcount.

Who is considered a key person in a business?

A key person is anyone whose death would seriously hurt the company financially. That is often the owner or founder, but it can also be a top salesperson who drives a large share of revenue, a partner, a lead engineer, or anyone with relationships or knowledge the business would struggle to replace quickly.

How much key man insurance do I need?

There is no single formula. Common approaches size the benefit to a multiple of the person's salary or the profit they drive, the cost to recruit and train a replacement, and any business debt they personally guarantee. Many small businesses land somewhere between five and ten times the person's compensation, then adjust for debt and revenue impact.

Is key man insurance tax deductible?

Generally no. The IRS does not let a business deduct premiums on a policy where the business is the beneficiary. In exchange, the death benefit is usually received income-tax-free if the employer-owned life insurance notice and consent rules are met before the policy is issued. Ask a tax professional about your situation.

Who owns and who receives a key man insurance policy?

With key man insurance the business applies for, owns, pays for, and is the beneficiary of the policy. The insured is the key employee or owner. When that person dies, the payout goes to the company, not to the family, which is what separates it from a personal life insurance policy.

Is key man insurance the same as a buy-sell agreement?

No. Key man insurance replaces lost value and keeps the business running after a key person dies. Buy-sell life insurance funds the purchase of a deceased owner's shares so the remaining owners keep control. Many businesses with partners need both, because they solve different problems.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your specific situation. Product availability, features, riders, and rates vary by state, age, health, business type, and carrier, and any coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.