Key Man Insurance for Small Business: Do You Need It?

The Short Version

Key man insurance for small business is a life insurance policy the company buys on its most critical person, with the business as beneficiary. If that person dies, the company receives a cash benefit to cover lost revenue, hire a replacement, or keep the doors open. For most small businesses with even one person the company truly depends on, this is not optional. The real question is how much and in what form.

Here is a scenario I have walked into more than once. A business owner calls me, not about their own personal coverage, but about a partner who just passed away. The business is intact, the clients are there, the revenue was real. But the person who drove 60 percent of it is gone, and nobody thought to put a plan in place. Now the surviving partner is fighting with the estate, scrambling for cash, and trying to hold a business together while grieving a friend.

Key man insurance for small business exists to prevent exactly that situation. It is one of the most underused tools I see when I sit down with business owners, and it gets skipped for the same reasons every time: assumed to be too expensive, assumed to be for bigger companies, or simply never raised in the right conversation. That conversation starts with one honest question. If your most important person was gone in thirty days, could the business survive the next twelve months?

This guide gives you straight answers on what key man insurance is, who qualifies as a key person, how much coverage makes sense and why, what the policies actually cost, how the tax treatment works, and how all of this connects to the buy-sell agreements that most business partners have never discussed. I have included a worked example with real math. No pressure, no pitch, just the information a business owner needs to make a clear decision.

What this guide covers

- What key man insurance actually is

- Does your small business need it?

- Who qualifies as a key person?

- How the policy works

- Term vs permanent: which fits the business?

- How much coverage to buy

- What key man insurance costs

- The tax rules you need to know

- Buy-sell agreements: the other big job

- How to apply

- Common mistakes business owners make

- Frequently asked questions

What key man insurance actually is

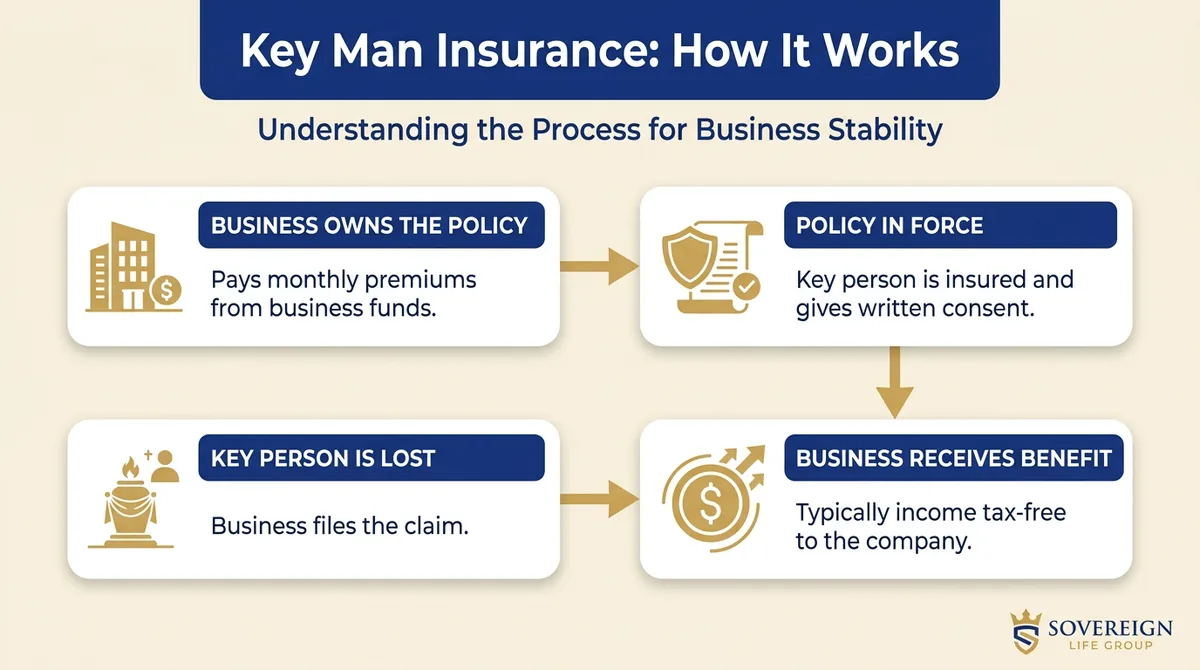

Key man insurance is a life insurance policy that a business purchases on one of its most essential people, with the company named as both the policy owner and the beneficiary. If that person passes away while the policy is in force, the business collects the death benefit. The key person's family does not receive this payout. The funds go directly to the company to use however the business needs them most.

The term "key man" is old industry shorthand. The modern, legally neutral version is key person insurance. Carriers, agents, and the IRS all use both names. For this guide, treat them as identical.

The structural difference from personal life insurance is worth being clear about. With a personal policy, you own it, you pay the premiums, and your family receives the benefit. With a key man policy, the business does all three of those things: it owns the contract, pays the premiums out of business funds, and collects the death benefit. The insured person has no ownership of the policy and is not the beneficiary. They consent to being insured and that is the extent of their role. That consent, by the way, is legally required before the policy can be issued.

This is not a product built for large companies. According to the U.S. Small Business Administration, small businesses make up 99.9% of all U.S. businesses and employ nearly 46% of the private-sector workforce. The vast majority of those companies have at least one person whose sudden absence would be financially devastating. That is precisely the exposure key man insurance is designed to address.

No medical exam for a ballpark. Free, and no pressure.

Does your small business need key man insurance?

Most small businesses with even one essential person, including the owner, should have key man coverage in place. If losing one person would force the company to miss payrolls, lose major client relationships, default on a loan, or fail to deliver on existing contracts, the financial exposure is real. Key man insurance directly addresses it.

The companies that need this most tend to be the ones that skip it. A solo attorney whose clients follow the relationship rather than the firm name. A flooring contractor who runs every estimate and manages every crew himself. A small tech firm where one developer holds every critical system and every access credential. A restaurant where the executive chef is the entire reason regulars keep coming back.

The mistake I see constantly is owners assuming this coverage is for bigger companies. It runs exactly the other direction. A large company has organizational depth. When a senior vice president at a 2,000-person company leaves, three people can cover the function while a search is underway. When the owner of a seven-person landscaping business is hospitalized for three months, the whole operation stops. Key person risk is highest where the bench is thinnest, which describes almost every small business I have ever worked with.

There are honest situations where this coverage makes less sense. If the business has several principals who each carry significant client relationships and operational responsibilities, the concentration risk is lower. If the company already holds substantial liquid reserves the team could draw on, the financial gap from losing one person may be manageable. If the business model genuinely distributes knowledge and relationships across a team, a single key person may not exist.

For everyone else, the question is not whether key man insurance for small business makes sense. It is how much to buy and in what form.

Who qualifies as a key person?

A key person is anyone whose death or prolonged absence would cause a material financial loss to the business. This typically includes the business owner, partners, the top revenue-generating employee, or anyone with specialized expertise the company cannot replace quickly.

The threshold is financial impact, not seniority or title. The test I walk through with business owners is direct: if this person was gone in thirty days, what would it cost the company in lost revenue, emergency recruiting, client attrition, and operational disruption? Assign a number. If it makes you uncomfortable, you have found your key person.

- The business owner. In most small companies, the owner is the key person by default. They hold the lender relationships, the client relationships, the operational knowledge, and often the actual license or credential the business needs to function. An HVAC company whose owner holds the contractor's license cannot legally pull permits without them. That is a key person.

- The top revenue producer. A salesperson who drives 40 percent of the company's new business is a key person. Losing that pipeline is not just a revenue shortfall. For a small business running on tight margins, it is a survivability question.

- The technical specialist. The software architect who built the entire platform. The machinist who is the only one who can run a specific piece of equipment. The nurse practitioner in a three-person practice. When the skill set is rare enough that replacement takes twelve to eighteen months, the exposure during that window is quantifiable and real.

- The partner in a two-person firm. Law practices, CPA firms, consulting shops. When two people run a company and one dies, the survivor needs cash to buy out the estate and keep operating. Without a plan, the business often does not survive the resulting ownership dispute. This is where key man insurance and buy-sell agreements work together, and we cover that below.

Multiple people can be insured under separate policies. You are not limited to one. A business with two principals and a critical sales director might need three separate key man policies, each sized to the actual financial exposure that person represents.

How the policy works

The business applies for a life insurance policy on the key person, names itself as beneficiary, and pays the monthly premiums from business funds. The key person consents to the coverage and completes a health evaluation. If they pass away while the policy is in force, the company receives the death benefit as a lump-sum payment. The funds go to the business, not to the key person's family.

Consent and notification are required by federal law

Under the Pension Protection Act of 2006, employer-owned life insurance policies require the insured employee to provide written consent before the policy is issued. The employer must also notify the insured in writing of the coverage amount and the fact that the company will be the beneficiary. This is not a formality. Policies that skip this step risk losing the income-tax-free treatment of the death benefit, turning a tax-free benefit into taxable income at exactly the wrong moment. Keep the signed consent in the business's permanent records.

What the business does with the payout

When the key person dies and the company files a claim, the benefit arrives as a lump sum. The company decides how to use it. Cover the revenue gap while recruiting a replacement? Fund the buyout of the deceased partner's ownership stake from the estate? Repay a business loan that was personally guaranteed? All of those are legitimate uses. The payout has no restriction on purpose, which is one of the things that makes this tool genuinely useful in a crisis where the actual need is rarely predictable.

What a key man life policy does not cover

A life insurance policy pays on death. It pays nothing if the key person becomes disabled, is diagnosed with a serious illness, or simply cannot work for an extended period. That is a separate risk addressed by key person disability insurance, which is a different product entirely. The statistical risk of a key person being disabled for a year or more is higher than the risk of death for most people under 65. For many small businesses, the disability scenario is actually the more likely financial disruption. If a key person being sidelined for eighteen months would be as damaging as their death, that conversation belongs in the plan alongside the life coverage.

Term vs permanent: which structure fits the business?

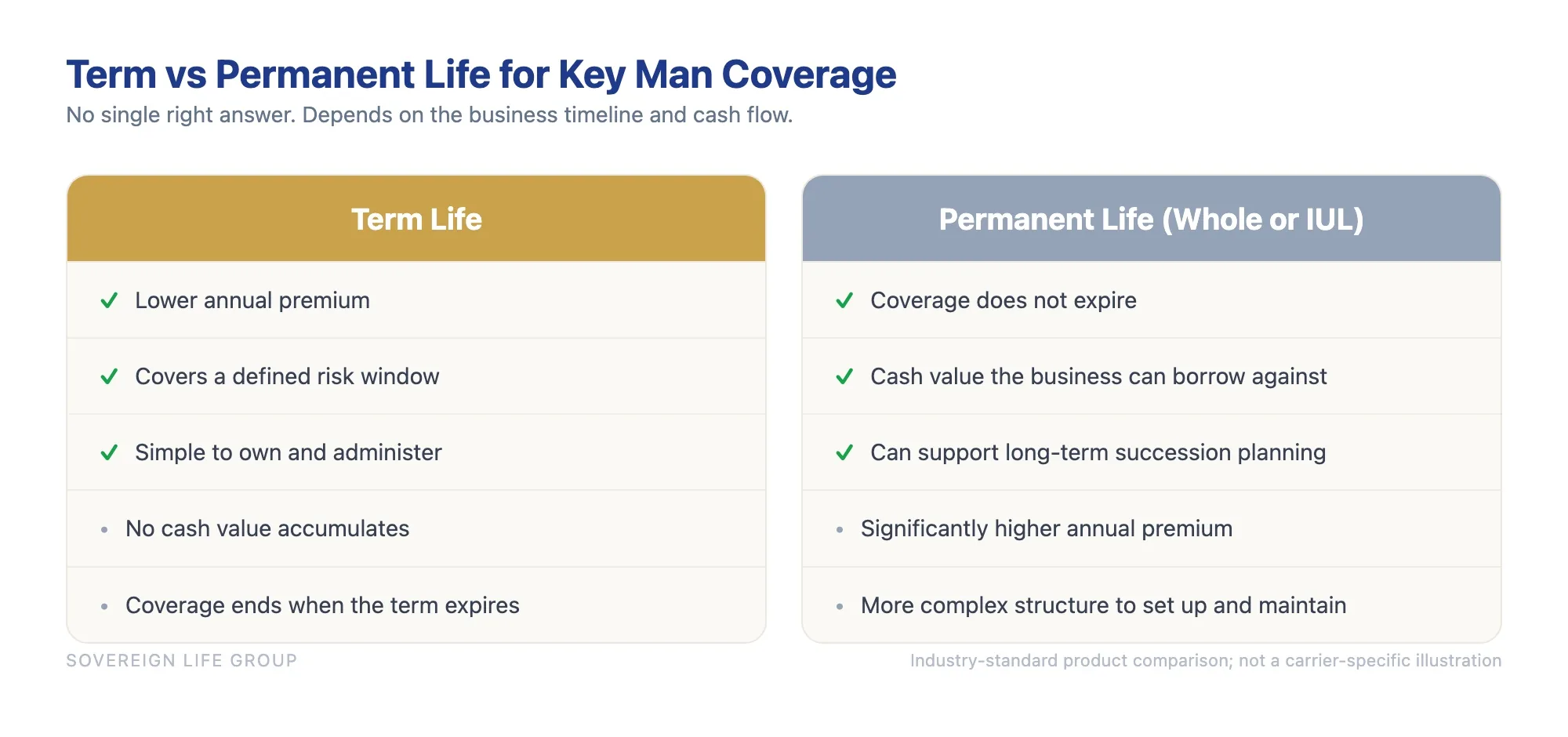

Term life insurance is the most common structure for key man coverage. It is cost-effective, runs for a defined period matched to the actual risk window, and is straightforward for the business to manage. Permanent life, specifically whole life or indexed universal life, adds a cash value component that some businesses use as a long-term financial asset. The choice depends on what the business actually needs, not on any general preference.

Most of the key man cases I work on use term. Here is the reasoning. The risk is tied to a specific window: the years when the business is most dependent on that person. If you are buying coverage on a 45-year-old partner because the two of you plan to retire or transition the business in twenty years, a 20-year term covers that exposure cleanly and costs a fraction of a permanent policy. You are paying for the risk window, not for decades beyond it.

Permanent life, either indexed universal life or whole life, adds something term does not: accumulated cash value inside the policy that the business can borrow against, use as loan collateral, or access as part of a business exit strategy. Some business owners use this structure deliberately, where the key man policy does double duty as near-term protection and as a tax-advantaged business asset over time. That is a legitimate strategy, but it requires a long time horizon and a higher near-term premium to justify. For a deeper look at how the term and permanent structures differ for families and businesses alike, see our breakdown of term versus whole life insurance.

| Factor | Term Life | Permanent Life (Whole or IUL) |

|---|---|---|

| Annual premium | Lower | Significantly higher |

| Coverage duration | Defined term (10, 15, 20, or 30 years) | Does not expire if premiums are paid |

| Cash value | None | Builds over time, accessible by the business |

| Complexity | Simple to own and administer | More variables to manage over time |

| Best fit | Covering a specific business risk window at the lowest cost | Long-term asset building alongside protection |

How much key man insurance does a small business need?

There is no single correct formula, but most approaches start with quantifying what the key person actually contributes to the business's ability to generate revenue and operate. Common valuation methods multiply salary by a factor, project at-risk revenue over a recovery timeline, or build a complete cost-to-replace estimate. Running all three and selecting a figure that honestly reflects the exposure is better than anchoring on any one method alone.

The salary multiple method

The simplest starting point. Take the key person's total annual compensation and multiply it by a factor, typically five to ten. A key person earning $200,000 per year might warrant $1 million to $2 million in coverage. The logic is that you are buying several years of financial runway to absorb the loss of that contribution. This method is fast and easy to defend, but it can undercount a key person whose personal compensation is low relative to their actual impact on the company's revenue.

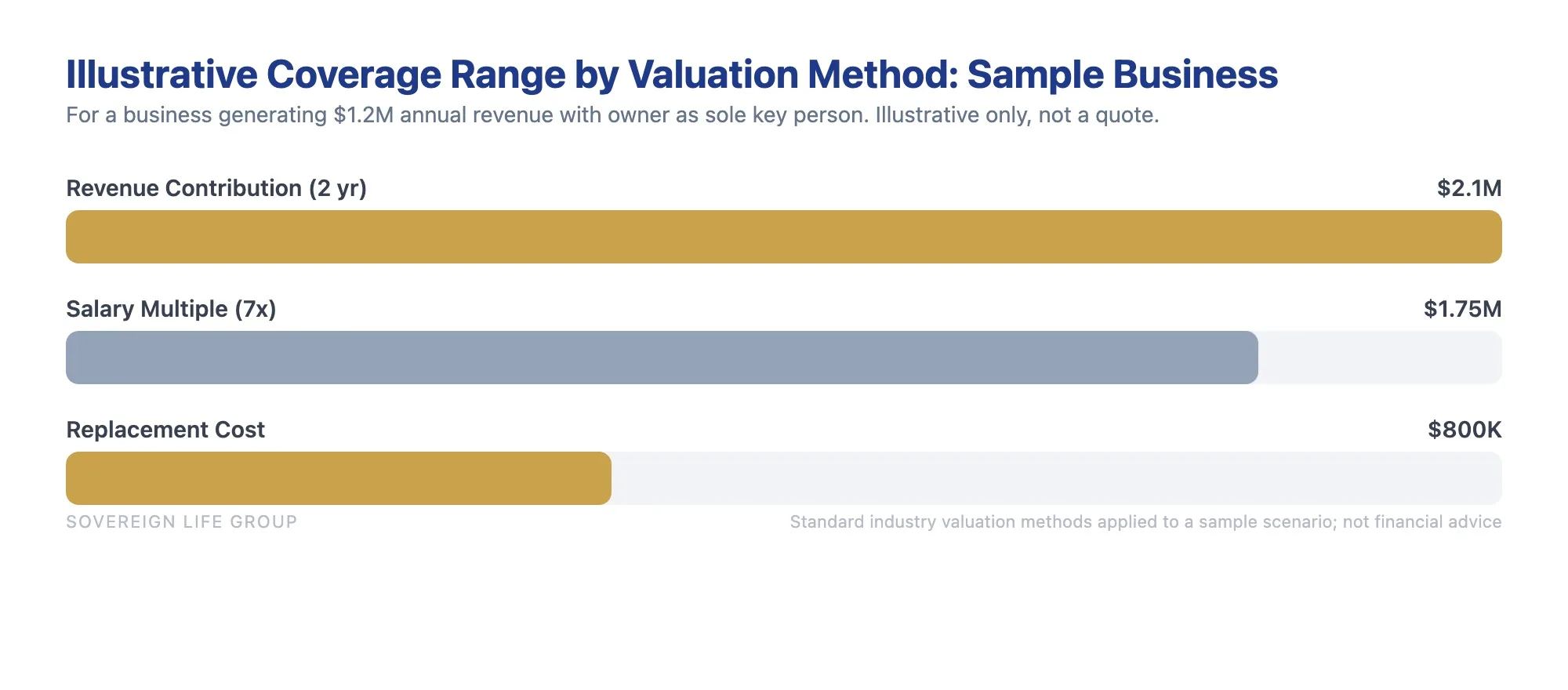

The revenue contribution method

More precise for revenue-dependent roles. Estimate what share of the company's gross revenue would genuinely be at risk if this person were gone, then multiply that amount by the number of years it would realistically take to recover. If a key salesperson drives $700,000 of the company's $1.2 million in annual revenue, and a credible recovery timeline is two to three years, the coverage target is $1.4 million to $2.1 million. This method tends to produce the highest number, but it also tends to reflect the actual business risk most accurately.

The replacement cost method

Add up all the real costs of replacing the key person: executive search fees, which typically run 20 to 30 percent of first-year salary; the salary premium often required to attract someone with equivalent skills; the productivity gap during onboarding and ramp-up, which can stretch twelve to eighteen months for specialized roles; and any direct client revenue lost during the transition. For a critical hire at $150,000 per year, the total replacement cost can easily exceed $600,000 when you account for everything a rushed senior search actually costs.

A worked example with real math

Say you own an HVAC company with eight employees generating $1.2 million per year. You are the estimator, the commercial account manager, and the license holder. Without your contractor's license, the company cannot legally pull permits in most states. Your passing means the commercial pipeline stops immediately, and the company cannot take on new commercial work until a licensed replacement is found and credentialed.

Revenue at risk: approximately $700,000 per year from the commercial accounts you manage directly. Time to find, hire, and credential a licensed replacement with comparable relationships: eighteen to twenty-four months at minimum. Hard replacement costs: search fees plus salary premium plus gap revenue easily adds up to $500,000 or more.

Working the revenue contribution method: $700,000 times two years equals $1.4 million. The salary multiple at seven times $180,000 compensation gives $1.26 million. Replacement cost adds $500,000 to $800,000 in hard and soft costs, which gives a floor rather than a ceiling. A reasonable target is $1.4 million to $2 million.

For a healthy 42-year-old nonsmoker, a 20-year term policy at $1.5 million is less expensive than most business owners expect. I would rather run the actual numbers with you, but that math gives you a credible target before our first conversation.

Get a fast, free estimate tailored to your age and health.

What key man insurance costs

Key man insurance for small business costs depend on the key person's age, health, tobacco use, the coverage amount, the term length, and whether the policy is term or permanent. For a healthy person in their 30s or 40s, a substantial term policy can cost less than a single business lunch per month. But the actual number requires a real application with real health details, and no honest agent can promise you a specific rate from an article.

Three cost factors consistently catch business owners off guard.

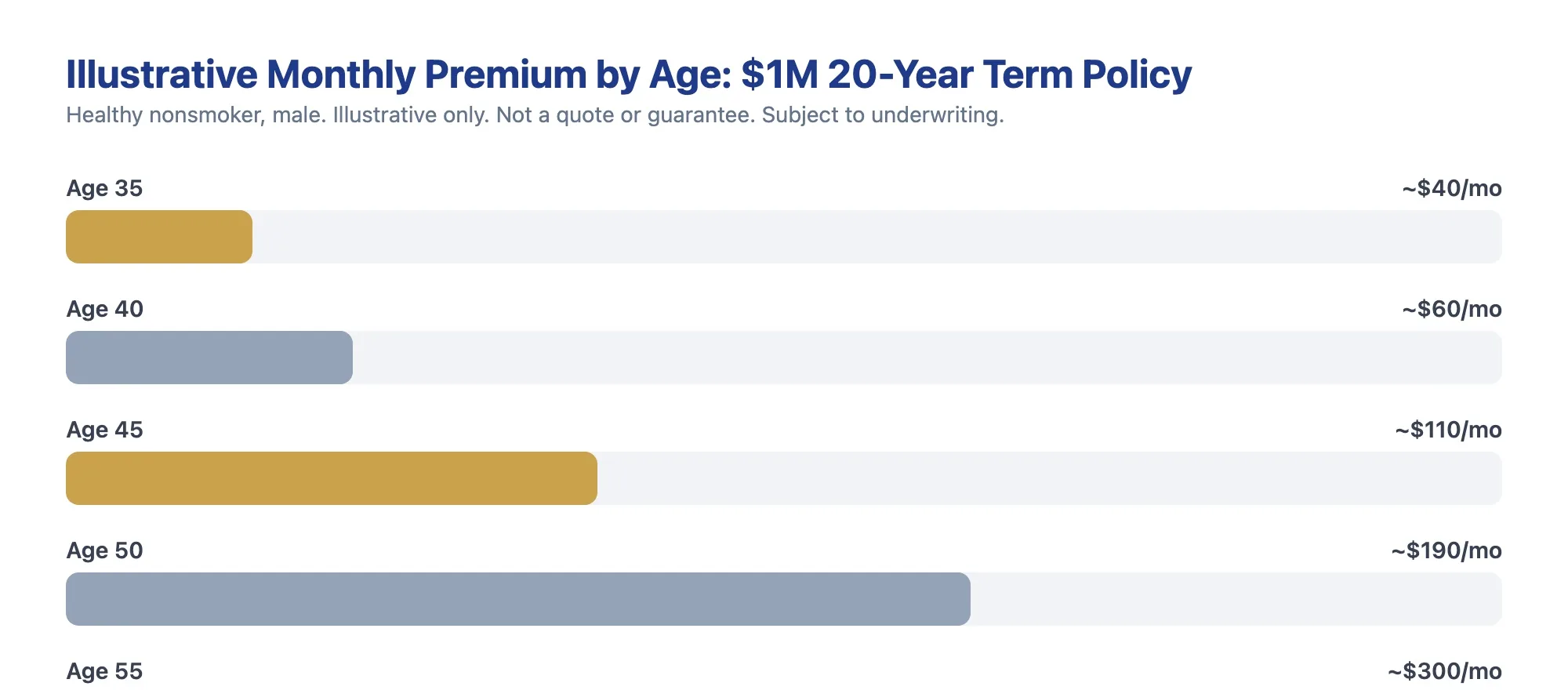

Age is the biggest lever. The difference between insuring a 40-year-old key person and a 52-year-old key person is not marginal. It is roughly two to three times more expensive for the same coverage amount. Every year a business waits is a year of higher premiums for the remaining policy term. This is not a scare tactic. It is just actuarial math, and it is consistent across every carrier I have ever quoted.

Health history changes the outcome significantly. A healthy key person at standard or preferred rates is one situation. A key person with hypertension, diabetes, a prior cancer history, or other rated conditions is a different conversation. Coverage may still be available, but it could carry a rated premium surcharge. In some cases, a simplified issue or guaranteed issue product makes more sense. If health is a factor, working with an agent who can shop across carriers matters, because one carrier's table-rated result is another's standard offer for certain conditions. Our overview of key person insurance for business owners covers how underwriting works across different health profiles.

Simplified issue costs more per dollar of coverage. For businesses that need coverage quickly, or for key people who cannot qualify for fully underwritten policies, simplified issue underwriting is available. It uses only health questions rather than a full exam, and approval can happen in days. That speed comes at a cost: higher premiums for equivalent coverage, and often a ceiling on the maximum face amount. If the key person is healthy, a fully underwritten policy almost always delivers better value.

Research from LIMRA's 2023 Insurance Barometer Study found that many small business owners significantly overestimate what life insurance costs, often by a factor of two or three compared to actual market rates for healthy applicants in their 30s and 40s. The perceived cost barrier keeps people from getting quotes that would actually surprise them in a good direction.

The tax rules on key man insurance

In most standard key man arrangements, premiums paid by the business are not tax-deductible. The death benefit paid to the company is typically received income tax-free under IRS Code Section 101(a). The consent and notification requirements under the Pension Protection Act must be followed for this favorable treatment to apply. This section gives you the foundation, not a substitute for advice from your CPA on your specific entity structure.

Premiums are not deductible in the standard setup

When the business is both the owner and the sole beneficiary of a key man policy, the IRS treats the premiums as a non-deductible business expense. You cannot write them off the way you would deduct employee health insurance premiums or equipment depreciation. The business pays from after-tax dollars.

There is a narrow exception sometimes raised: if the policy is structured as an employee benefit where the insured receives coverage as taxable compensation, part of the premium might be deductible. But in a straightforward key man arrangement where the company is the beneficiary, deductibility does not apply. Do not accept that framing without seeing the specific legal structure in writing confirmed by a CPA.

Death benefit is typically received income tax-free

Here is the meaningful trade-off that offsets the non-deductible premiums. When the key person passes and the business files a claim, the death benefit is generally received income tax-free under Section 101(a) of the Internal Revenue Code. A $1.5 million death benefit arrives as $1.5 million of usable cash, not as taxable income the company has to gross up for federal and state taxes. For a business absorbing the financial shock of losing its most important person, that matters.

The consent requirement protects the tax-free treatment

Under the Pension Protection Act of 2006, employer-owned life insurance is subject to notice and consent requirements codified under IRS guidance on Code Section 101(j). The insured must give written consent before the policy is issued. The employer must notify the insured of the coverage amount and the employer's status as beneficiary. If those steps are not documented, the death benefit can be reclassified as taxable income. This is a real exposure for businesses that move through applications without a licensed agent walking them through the paperwork. Keep a copy of every consent and notification document in permanent business records.

C-corporation owners: one additional consideration

For C-corporations specifically, life insurance proceeds can factor into alternative minimum tax calculations. This is less relevant for businesses structured as S-corps, LLCs, or partnerships, but C-corp owners should confirm the AMT treatment with their CPA before placing a policy. Most small businesses are not C-corps, but it is worth knowing if yours is.

Buy-sell agreements: key man insurance's other big job

A buy-sell agreement funded by life insurance lets business partners legally pre-arrange what happens to ownership if one of them dies. The surviving partner uses the death benefit to purchase the deceased partner's ownership share from the estate, keeping the business in the hands of the people who actually run it rather than heirs who may not want involvement and may not agree on what to do.

This is the use case that surprises business owners the most when I explain it. And I genuinely think it saves companies more often than a straight replacement-cost policy does, because the death without a funded buy-sell creates a situation with no clean answer.

Picture two partners who own a contracting business 50/50. One dies. The business does not disappear. The equipment is there, the contracts are active, the accounts receivable are real. But the deceased partner's half of the company now passes through the estate to the heirs. Those heirs could be a spouse with no interest in running a contracting business who simply wants cash. Or adult children who disagree about whether to sell or hold their stake. The surviving partner now has an involuntary co-owner they did not choose, and no automatic legal or financial mechanism to resolve it cleanly.

A buy-sell agreement funded by life insurance solves this. The partners agree in writing, before anything happens, on three things: if one of us dies, the other has the right and the obligation to buy the deceased's ownership stake; here is how we value the business; and here is the life insurance that will fund the purchase when the time comes. The agreement and the coverage work in lockstep. The death benefit arrives at exactly the moment the cash is needed.

Cross-purchase agreement

Each partner owns a life insurance policy on the other. Two partners means two policies. When one partner dies, the surviving partner collects the death benefit and uses it to buy the deceased partner's ownership stake from the estate. The survivor ends up owning 100 percent of the business. This structure scales awkwardly as the number of partners increases because the number of required policies multiplies, but for two-person businesses it is clean and widely used.

Entity purchase agreement

The business itself owns the policies on each partner. When a partner dies, the company collects the death benefit and uses it to repurchase the deceased partner's shares from the estate. The surviving partners end up owning a larger percentage of a smaller ownership pool. Fewer policies than a cross-purchase structure, but the tax treatment of the buyout can differ depending on entity type, which is why the business attorney and the insurance agent need to work together on the structure.

Getting the policy design and the legal agreement aligned is the critical piece. A mismatch between what the buy-sell agreement requires and what the insurance actually provides can leave the surviving partner in a worse position than if there had been no agreement at all. Our companion piece on key person business life insurance and how it works in partnership structures goes deeper on the funding mechanics.

How to apply for key man insurance

The application process for key man insurance follows the same general path as personal life insurance, with one additional layer of business paperwork: the COLI consent and notification form required under federal law. For most small businesses, fully underwritten coverage takes two to four weeks from application to policy in force. Simplified issue can happen in days.

Here is what the actual process looks like.

- Identify the right key person and the coverage target. This sounds obvious, but it often takes a real conversation. Many businesses insure the highest-paid employee rather than the one whose departure would actually break the operation.

- Decide on the structure. Term or permanent. How much coverage based on the valuation methods above. Any riders worth adding, such as a waiver of premium if the key person becomes disabled, or a conversion option to move a term policy to permanent coverage later without new underwriting.

- Shop across carriers with a licensed agent. Premium differences for the same coverage can be meaningful, and underwriting guidelines vary considerably by carrier, especially when the key person has any health history. One carrier's table-rated result is another's standard class for certain conditions. The independent life insurance approach we use at Sovereign Life Group means we shop a dozen or more A-rated carriers rather than pushing one product.

- The key person completes the health evaluation. For fully underwritten amounts, a paramedical exam is typical: a nurse visits, collects blood, takes blood pressure and basic vitals, and may do an EKG for older applicants or larger amounts. For simplified issue, just the application health questions are needed.

- The business signs the COLI consent and notification form. This is the document that preserves the death benefit's income-tax-free status. Keep a copy in permanent business records.

- Underwriting review and policy issuance. Full underwriting takes two to four weeks. Once approved, the first premium payment puts coverage in force.

One thing that catches people off guard: if the key person has a significant health history, coverage may be issued with a rated premium surcharge, modified face amount, or in some cases declined by a specific carrier. That is not unique to business policies. It is the same underwriting any individual applicant faces. Working with a broker who knows which carriers are favorable for which health profiles makes a material difference in both the price and the outcome.

Common mistakes small business owners make

The most common errors with key man insurance are waiting too long, insuring the wrong person, underestimating the coverage amount, and failing to update the policy when the business changes. Each of these is fixable before a claim and significantly harder to resolve after one.

Waiting until a lender requires it. Some business owners discover key man coverage for the first time when a bank requires it as collateral for an SBA loan or a commercial credit line. At that point, you are shopping under a deadline, possibly at an older age, without time to compare carriers properly. Coverage bought before the bank asks is almost always better priced and leaves the business with more structural options.

Insuring the highest-paid person instead of the most critical one. Salary and key-person status often match, but not always. A mid-level employee who is the only person who understands the company's proprietary manufacturing process, or who holds a credential the business legally needs to operate, can represent a bigger financial risk than a well-paid executive you could replace in ninety days with a good recruiter. The test is financial impact, not title.

Anchoring on the premium rather than the exposure. Business owners often size the policy to fit a comfortable monthly payment rather than working backward from the actual financial risk. A $500,000 policy feels substantial until you run the revenue contribution math and realize the company would need two years at full revenue to weather the transition, and those two years represent $1.4 million of business activity. Get to an honest coverage number first, then figure out how to pay for it.

Not reviewing policies when things change. A key man policy on a partner who has since retired, sold their stake, or left the company is paying premiums for a risk that no longer exists. Conversely, a policy sized for a $600,000 business is not the right coverage for a $1.8 million operation four years later. Review key man policies as part of the annual business review, and definitely revisit them when ownership or key personnel change in any way.

Forgetting disability. This is the most common gap I see. The probability of a key person being disabled for twelve or more months is meaningfully higher than the probability of death for most people under 65. A life insurance policy pays nothing for disability. Key person disability insurance is a separate product that requires its own conversation. Most businesses I work with have not thought through both sides of the risk.

Most people overthink the carrier selection and underthink the coverage amount. Both matter, but getting the sizing wrong means the policy might not actually accomplish what you bought it to do when you need it most.

Ready to protect the business you built?

Fifteen minutes. We look at who your key person is, run the coverage math together, and show you what the options actually cost. No jargon, no pressure, just the numbers.

Get a quick quote Prefer a conversation first? Book a free 15-minute review or read more on the key person insurance overview page.Frequently asked questions

Is key man insurance the same as key person insurance?

Yes. Both names describe the same coverage: a business-owned life insurance policy on an essential employee, with the company as beneficiary. Key man is the older term; key person is the modern, gender-neutral version. You will see both used interchangeably by carriers, agents, and the IRS. For educational purposes only. Not financial or tax advice. Consult a licensed professional.

Are key man insurance premiums tax deductible?

In most standard arrangements, no. When the business is both the owner and the beneficiary of the policy, the IRS treats the premiums as a non-deductible business expense. The trade-off is that the death benefit is typically received income tax-free under IRS Code Section 101(a). Confirm the specific treatment with a CPA before assuming any deduction applies to your arrangement. Structure and entity type can affect the answer.

How much key man insurance does a small business need?

Three methods are commonly used: a multiple of the key person's salary (5 to 10 times), a projection of revenue at risk multiplied by the years needed to recover it, or a total replacement cost calculation adding search fees, onboarding, and lost revenue. Running all three and selecting the figure that honestly reflects the business exposure is better than anchoring on any single formula. Most small businesses with a genuine key person find the right range falls somewhere between one and three times annual revenue, but the actual number depends on the specific business and the specific role.

Can a sole proprietor get key man insurance?

Sole proprietors generally cannot take out a standard key man policy on themselves because the business and the individual are the same legal entity. A sole proprietor with employees can insure a critical employee. For protecting your own income stream for your family, a personal term or permanent life insurance policy is typically the right tool. For educational purposes only. Not financial or tax advice. Consult a licensed professional.

What happens to a key man policy if the key person leaves the company?

The business owns the policy, so it has several options: continue paying premiums if the risk now exists in another form, surrender the policy for any accumulated cash value on a permanent product, transfer the policy to the departing employee as part of a retirement or separation arrangement, or let it lapse. Reviewing key man coverage whenever key personnel change is part of sound business financial planning.

Does key man insurance require a medical exam?

Not always. For larger coverage amounts, most carriers require a paramedical exam where a nurse collects blood and basic vitals. For lower amounts, simplified issue underwriting using only health questions on the application is available. Simplified issue typically carries a higher premium or a coverage ceiling but can get the policy in force in days rather than weeks. The right choice depends on the key person's health profile and how quickly the business needs coverage.

For educational purposes only. Not financial or tax advice. Consult a licensed professional about your specific situation. Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. Product availability, features, riders, and rates vary by state, age, health, and carrier. Coverage is subject to underwriting approval. Guarantees are subject to the claims-paying ability of the issuing insurance company.