IUL vs 401k: An Honest Guide to Tax-Free Retirement

The Short Version

In the IUL vs 401k debate, there is no single winner, because they are built for different jobs. A 401(k) shines when your employer matches your money and you want simple, tax-deferred investing. An indexed universal life policy can add tax-free income flexibility and a death benefit, but it carries fees, caps, and needs steady funding. For many families the honest answer is not one or the other. It is both, in the right order.

When people first compare IUL vs 401k, they usually expect one to be the obvious answer. The truth is more honest and more useful: these are two different tools that solve two different problems. A 401(k) is a workplace retirement account. An indexed universal life policy is permanent life insurance that also builds cash value. Putting them in the same ring and asking which one wins misses the point. The better question is which of these retirement savings options fits the life you are actually building, and in what order they belong.

This guide walks through both in plain English. We will define each one, show how they are taxed, explain caps and floors and fees without the jargon, lay them side by side in a table, work through the order most families should fund them in, and be honest about who an IUL is wrong for. No hype, no pressure, just the trade-offs laid out so you can decide with your eyes open.

What this guide covers

- The quick comparison

- What a 401(k) actually does

- What an indexed universal life policy does

- Caps, floors, and participation rates

- IUL vs 401k: side-by-side table

- The tax story, compared honestly

- Fees on both sides, named out loud

- Why the employer match comes first

- The honest trade-offs of an IUL

- Who an IUL is not for

- The order most families should fund

- How to vet a properly structured IUL

- Frequently asked questions

IUL vs 401k: the quick comparison

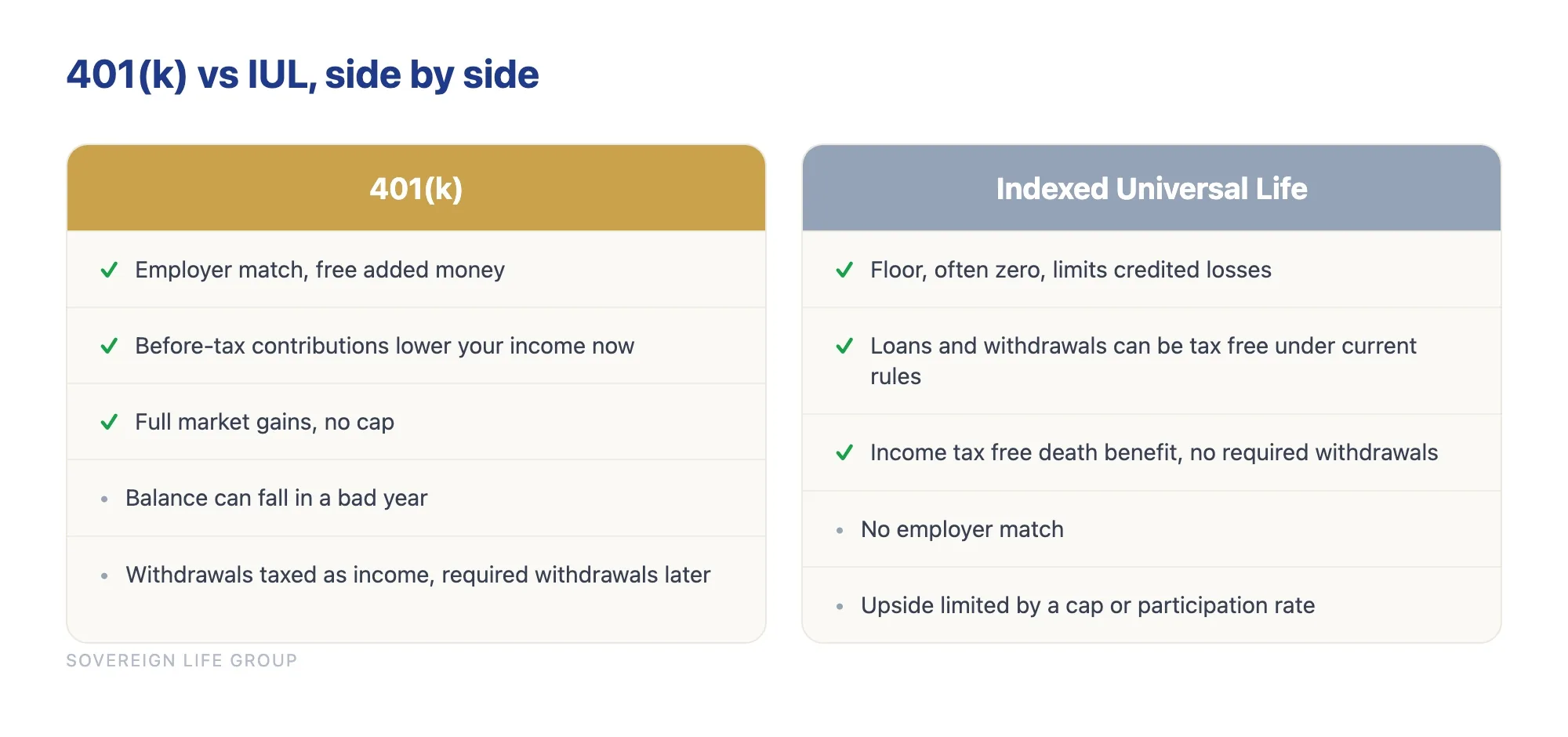

Here is the heart of it before we dig in. A 401(k) lets you set aside money from your paycheck, usually before tax, often with an employer match, and it grows until you draw on it in retirement, when withdrawals are taxed as ordinary income. An indexed universal life policy is life insurance first. Part of your premium covers the cost of insurance, and the rest can build cash value that is credited based on the movement of a market index, with limits on both the upside and the downside.

The 401(k) advantage is simple and powerful: free matching money, automatic payroll habits, and full market growth with no ceiling. The IUL advantage is flexibility and protection: cash value you can generally access without triggering income tax under current rules, a floor that limits credited losses, no required withdrawals, and a death benefit that pays your family income-tax-free if something happens to you. Neither is magic, and neither is a scam. They simply do different jobs, and the smartest plans often use each one for the job it is best at.

Tax-advantaged growth with a floor against losses. Quick and free.

What a 401(k) actually does

A 401(k) is an employer-sponsored retirement plan. You choose a percentage of your pay to contribute, and in a traditional 401(k) that money usually goes in before tax, which lowers your taxable income this year. The money is then invested, typically in mutual funds or target-date funds your plan offers, and it grows tax-deferred until you take it out. According to the IRS, contributions are capped each year, and there are rules about when you can take the money out without a penalty, generally after age 59 and a half.

There is also a Roth 401(k) option in many plans, where you contribute after-tax dollars and qualified withdrawals come out tax-free later. That matters for this comparison, because the Roth version shares one feature people love about an IUL: tax-free money in retirement. The difference is that the Roth still has annual contribution limits and required distribution rules in many cases, while an IUL works under insurance rules instead.

The biggest reason to love a 401(k) is the match. If your employer adds fifty cents or a dollar for every dollar you put in, up to a limit, that is an immediate increase on your savings that is very hard to find anywhere else. Skipping a match is usually leaving money on the table, and no insurance product changes that math.

The honest trade-offs of a 401(k):

- Taxes are deferred, not erased. In a traditional 401(k) you skip tax now, but every dollar you withdraw in retirement is taxed as ordinary income, at whatever rates exist then. You are essentially partnering with the government on a balance whose tax bill is not yet written.

- Market risk is yours. Your balance rises and falls with your investments. A strong decade helps you. A weak one right before retirement can force hard choices about when and how much to withdraw.

- Required minimum distributions. Current rules force you to start taking money out of a traditional 401(k) later in life, whether you need it or not, which can push up your taxable income in retirement.

- Limited menu and access. You can only pick from the funds your plan offers, and getting to the money before 59 and a half generally means taxes and a penalty, with narrow exceptions.

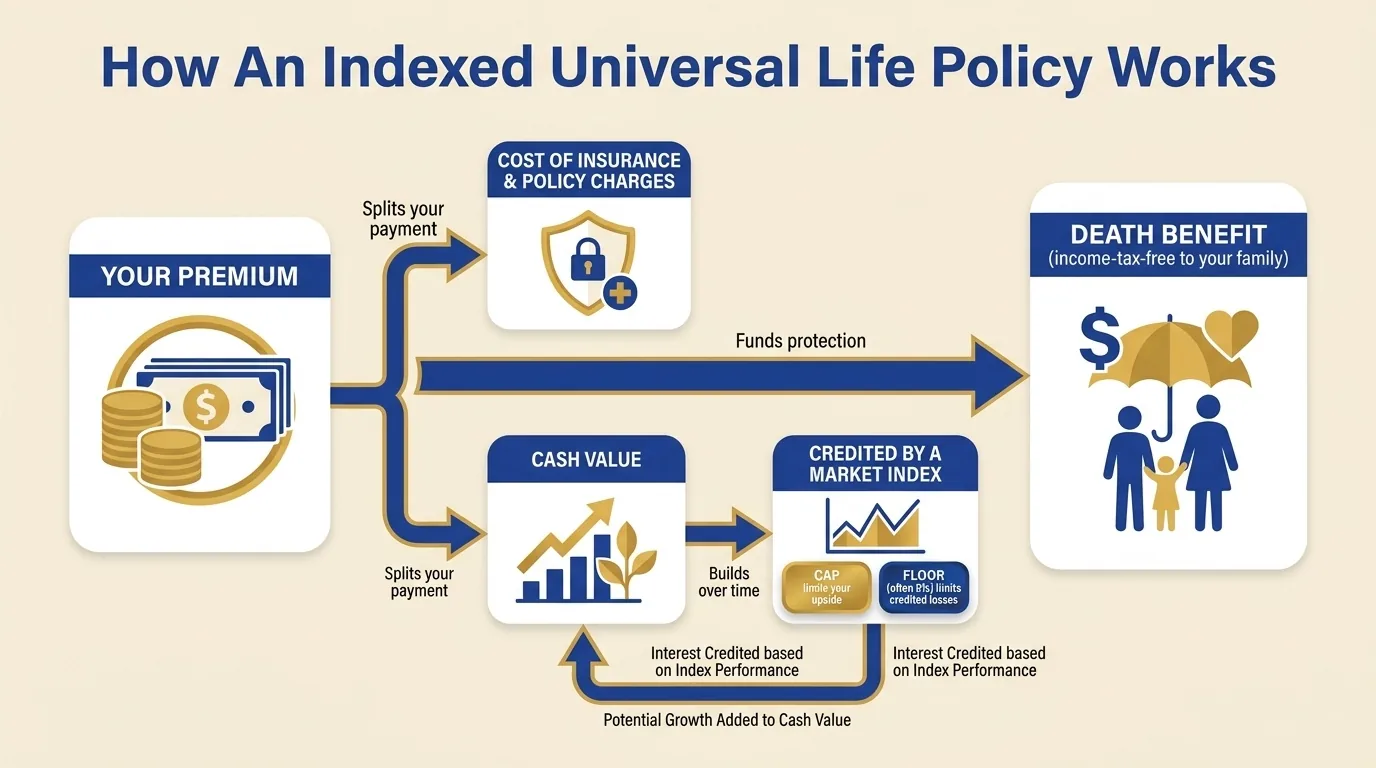

What an indexed universal life policy actually does

An indexed universal life policy, or IUL, is permanent life insurance. It is designed to last your whole life rather than for a set term. You pay premiums, a portion covers the insurance and policy charges, and the remainder can build cash value. That cash value earns interest tied to the performance of a market index, such as a broad stock index, but you are not invested directly in the market. Instead, the carrier credits your value based on index movement, within limits we will unpack in a moment.

The feature that draws most people into the indexed universal life vs 401k conversation is taxes. Cash value grows without annual taxes, and under current tax law you can generally access it through policy loans and withdrawals that are not treated as taxable income, as long as the policy stays in force and is structured correctly. That is the engine behind the idea of tax-free retirement income from an IUL. On top of that, the policy carries a death benefit, so your family is protected the entire time you are funding it, and that death benefit generally passes to them income-tax-free.

Some families also use a well-funded permanent policy as a private source of financing for big purchases, an idea often called the be your own bank strategy. It can be a smart fit for the right person, but it only works when the policy is designed and funded correctly. The thing to hold in your head is that an IUL is doing two jobs at once: protecting your family with a death benefit, and growing a pool of cash value you can tap later. That dual purpose is its strength and the reason it costs more than a plain investment account.

Caps, floors, and participation rates, explained simply

This is the part most articles skip or rush, and it is exactly where IUL gets misunderstood in both directions. The crediting on an IUL is governed by three dials. Understanding them is the difference between a realistic expectation and a sales pitch.

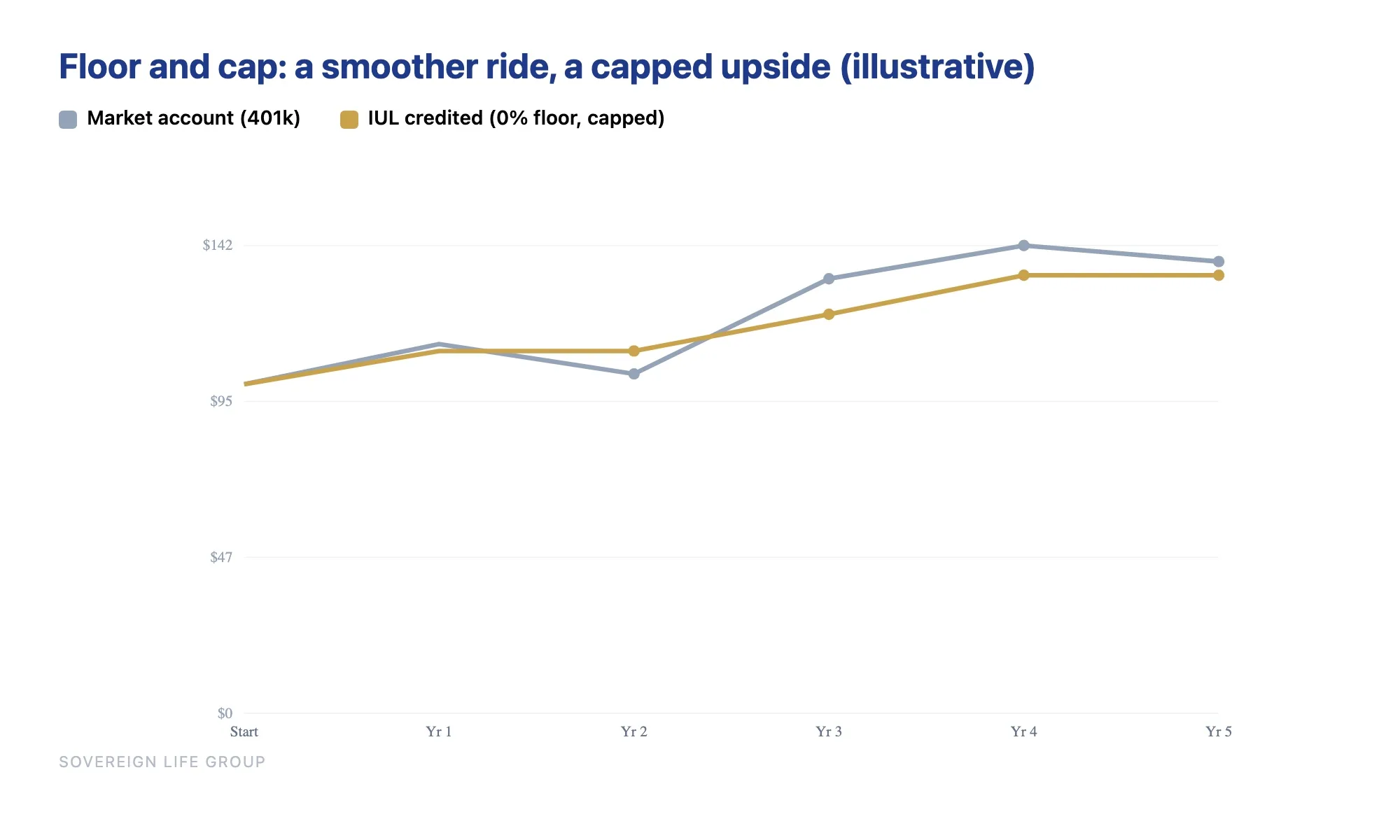

The floor protects your credited value

The floor is the lowest amount your cash value can be credited in a bad index year, and it is often zero percent. A zero floor means that if the index drops, your credited interest for that period does not go negative from market losses. This is the headline benefit people repeat. It is real, but read it precisely: the floor protects against index losses, not against the policy charges, which still come out. So a flat market year is not the same as a free year. Your cash value can still dip a little because the cost of insurance is being deducted even when the index credits zero.

The cap limits your upside

The cap is the ceiling on how much you can be credited in a good year. If the index climbs well past the cap, you are credited only up to that cap. This is the price you pay for the floor. You trade some of the high-market upside for protection against the low-market downside. In a banner year for stocks, a 401(k) invested in the market may capture more growth than a capped IUL. Caps are set by the carrier and can change over time, which is one of the honest uncertainties of the product.

The participation rate decides how much of the move counts

The participation rate is the percentage of the index's gain that gets applied to your crediting before the cap. A participation rate of 100 percent means you count the full move up to the cap. A rate above or below that changes the math. Some products use participation rates instead of caps, some use both, and some add other features. None of these are guaranteed for life. The takeaway is simple: the index going up 20 percent does not mean your policy is credited 20 percent. The dials decide what you actually receive.

If anyone shows you an IUL illustration that assumes a high, smooth return every year for decades, slow down. Index crediting is uneven, the dials can move, and the guaranteed columns of an illustration usually look very different from the projected ones. A good strategist walks you through both.

IUL vs 401k: side-by-side comparison table

This table is a starting point, not a verdict. Your numbers, your health, your employer plan, and your tax situation all change the picture.

| Feature | 401(k) | Indexed Universal Life (IUL) |

|---|---|---|

| What it is | Workplace retirement account | Permanent life insurance with cash value |

| Primary job | Tax-advantaged investing for retirement | Death benefit protection plus tax-flexible cash value |

| Employer match | Often yes, free added money | No |

| Tax on contributions | Usually before tax (lowers income now) | After tax (paid with money you keep) |

| Tax on money you take out | Taxed as ordinary income (traditional) | Loans and withdrawals can generally be tax-free under current rules |

| Market downside | Your balance can fall in a bad year | Floor (often zero) limits credited losses |

| Market upside | Full market gains, no cap | Limited by a cap or participation rate |

| Death benefit | Only the account balance | Yes, generally income-tax-free to your family |

| Contribution limits | Capped by the IRS each year | More flexible, set by policy design and tax rules |

| Early access before 59½ | Generally taxes plus a penalty | Loans and withdrawals available, subject to policy terms |

| Required withdrawals | Yes, later in life (traditional) | No required withdrawals |

| Main fees | Fund expense ratios and plan fees | Cost of insurance and policy charges |

| Best at | Capturing a match and simple growth | Protection, tax diversification, no-RMD flexibility |

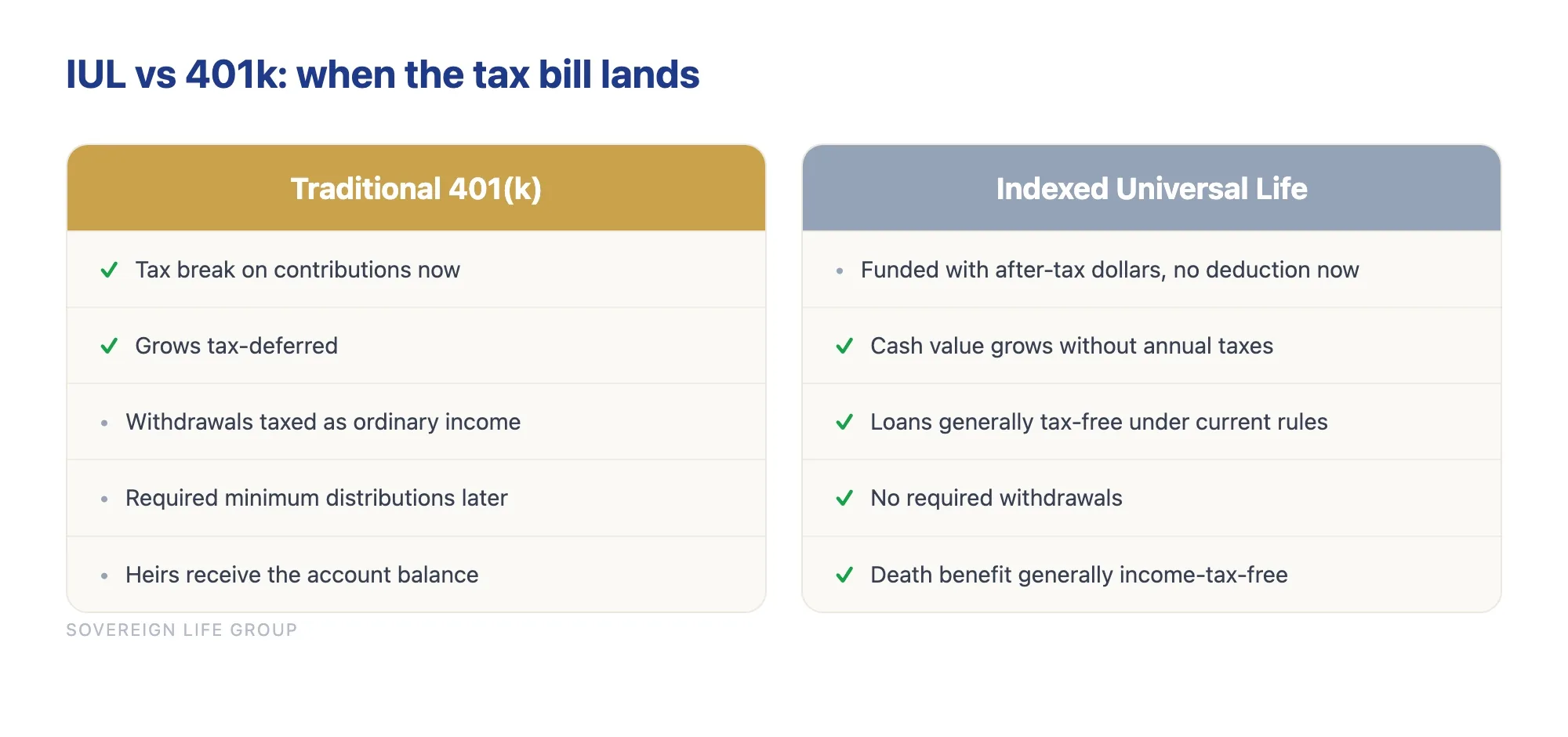

The tax story, compared honestly

Taxes are where this comparison earns its keep, so let me lay it out without spin. A traditional 401(k) gives you a tax break today and a tax bill later. You deduct contributions now, the money grows untaxed, and then every withdrawal in retirement is taxed as ordinary income. The open question nobody can answer is what tax rates will be when you retire. If rates are higher then, or your own income is higher, that deferred bill grows.

An IUL flips the timing. You fund it with after-tax dollars, so there is no deduction today. In exchange, the cash value grows without annual taxes, and under current law you can generally access it through policy loans that are not treated as taxable income. The death benefit also generally passes income-tax-free to your beneficiaries. The trade is straightforward: you give up the tax break now to aim for tax-free flexibility later.

This is why the phrase tax-free retirement gets attached to IUL so often, and why it deserves a careful asterisk. The tax treatment depends on the policy staying in force and being structured correctly, not lapsing, and not becoming a modified endowment contract, which is what happens when you overfund a policy relative to its death benefit and changes how distributions are taxed. Tax law can also change. None of this is a loophole or a guarantee. It is a feature of how permanent life insurance is currently taxed, and it should be confirmed with a licensed tax professional for your situation.

The practical insight is about tax diversification. If every retirement dollar you own sits in a traditional 401(k), every dollar you spend in retirement is taxable, and you have no control over future rates. Having a second bucket that behaves differently, whether that is a Roth account or an IUL, gives you choices about which source to draw from in a given year; our honest IUL versus Roth IRA comparison walks through how those two tax-free buckets really differ. That control is the real prize, more than any single product winning a return contest.

See the strategy applied to your age and goals. No pressure.

Fees on both sides, named out loud

Any honest comparison names the costs on both sides, because both have them. A 401(k) is not free, and an IUL is not a money pit. They simply charge for different things.

What a 401(k) costs. You pay fund expense ratios on the investments you hold, and many plans add administrative fees. These are often small in percentage terms, but they compound over decades, so a high-fee fund menu can quietly cost you real money. The fix is to favor low-cost funds where your plan offers them.

What an IUL costs. An IUL carries a cost of insurance that pays for the death benefit, plus policy charges and sometimes rider costs. These are heaviest in the early years, which is why an IUL surrendered early often looks like a bad deal: you paid the upfront costs and did not give the cash value time to grow past them. This is the single biggest reason an IUL goes wrong in practice. It is a long-game vehicle, and short-game behavior breaks it.

Here is the fair way to hold both facts at once. The 401(k) fee is the price of investing. The IUL fee is the price of carrying lifelong insurance protection alongside your savings. You are not paying the IUL charge for nothing. You are paying it for a death benefit your family keeps the whole time. Whether that protection is worth the cost depends entirely on whether you need the protection. If you do, the cost buys something real. If you do not, the same money invested simply may serve you better. That is the honest hinge of the whole decision.

Why the employer match almost always comes first

If your employer offers a match, capturing it is usually the highest-return move available to an ordinary saver, and it comes before any conversation about an IUL. Think about what a match is. When you contribute a dollar and your employer adds fifty cents, your money is increased the instant it lands, before any market return at all. No insurance product and no investment can promise that kind of immediate boost, because it is not a return on risk. It is part of your compensation that you only receive if you participate.

So the order is not really controversial among honest advisors. Fund the 401(k) at least up to the full match first. Anyone who tells you to skip free matching dollars to fund an insurance policy instead is putting a commission ahead of your math, and you should walk away from that conversation. An IUL earns its place after the match, not in front of it.

Where the conversation gets interesting is what happens above the match. Once you have captured the free money, the next dollars do not have that automatic boost, and the question becomes how you want those dollars taxed and protected. That is the point where tax diversification and a death benefit start to matter, and where an IUL can enter the picture as a complement. Plenty of households we work with at Sovereign Life Group run both, which is the whole idea behind protecting your family while building wealth.

The honest trade-offs of an IUL

Any agent who only shows you the upside of an IUL is not doing right by you. So here are the parts that do not fit on a billboard:

- It has real costs. The cost of insurance and policy charges come out of your premium, especially in the early years. That is the price of carrying lifelong protection alongside the cash value, and it is why early surrenders hurt.

- Your upside is capped. In a banner market year, a 401(k) invested in stocks may capture more growth than an IUL, because the IUL trades some of that upside for its downside floor. Returns are not guaranteed and depend on the index, the cap, the participation rate, and how the policy is funded.

- It needs consistent funding. An IUL is a long game. Underfund it, borrow too aggressively, or surrender it early, and it may lapse or fail to perform the way the illustration suggested. A lapsed policy with an outstanding loan can even create a tax bill, the opposite of what you wanted.

- Illustrations are not promises. The hypothetical numbers on a sales illustration show how a policy could behave, not how it will. Always read the guaranteed columns, not just the projected ones, and ask what assumptions are baked into the projection.

- The dials can change. Caps and participation rates are set by the carrier and can move over the life of the policy, so the crediting you see today is not locked in forever.

None of this makes an IUL bad. It makes it a tool that rewards honest design and steady habits, and punishes shortcuts. That is exactly why it deserves a careful look rather than a quick yes or no, and why the design of the policy matters as much as the decision to buy one.

Who an IUL is not for

The most useful thing an honest guide can do is tell you when to say no. An IUL is the wrong tool for a meaningful number of people, and pretending otherwise is how it earns its bad reputation. Consider passing, or at least waiting, if any of these describe you:

- You have not captured your full employer match yet. Free matching dollars come first. Funding an IUL instead of capturing a match is almost always the wrong order.

- Your income is unstable or your budget is tight. An IUL depends on consistent funding for many years. If a job change or a lean stretch could force you to stop paying, the early costs may leave you worse off than if you had never started.

- You do not actually need life insurance. If no one depends on your income and you have no legacy or estate goal, you may be paying for a death benefit you do not need. In that case, a simple investment account may serve you better for pure growth.

- You want the most growth for the least cost. If your only goal is maximum long-term return and you can stomach market swings, the insurance charges inside an IUL are a drag you may not want. A low-cost investment approach is built for that job.

- You are being rushed. If anyone pressures you to sign quickly, skip the trade-offs, or focus only on the projected column, that is a reason to slow down, not speed up.

If you are weighing protection products more broadly, it can help to understand how permanent and temporary coverage differ first, which our guide on term versus whole life insurance lays out simply. Sometimes the right answer is a large, inexpensive term policy plus a fully funded 401(k), and no IUL at all. A strategist who is willing to say that is one worth trusting.

The order most families should fund their retirement savings options

For most working families, the sensible sequence looks something like this. It is not a rigid law, but it reflects the math of where each dollar does the most good.

- First, capture the full employer match in your 401(k). This is the highest-return, lowest-effort move available, because the match increases your money immediately.

- Second, handle high-interest debt and a basic emergency fund. Paying off expensive debt is a guaranteed return, and an emergency fund keeps a surprise from forcing you to raid long-term accounts.

- Third, make sure your family is actually protected. If people depend on your income, the death benefit comes before fancy strategies. This may be term insurance, permanent insurance, or a mix, sized to the real job.

- Fourth, consider tax diversification for the dollars above the match. This is where a Roth account or an IUL can earn a place, giving you a second bucket that is taxed differently in retirement.

- Fifth, layer in additional strategies if they fit. For some families, a well-funded permanent policy supports goals like legacy planning, estate liquidity, or a private financing pool. For others, simple investing is plenty.

An IUL tends to fit best if you are already saving steadily, you have captured your match, you expect taxes to matter in retirement, you want a death benefit while you build, and you can commit to funding the policy for the long haul. A 401(k) tends to fit nearly everyone with access to a match. If you want to see how an IUL is structured as a product rather than just a concept, our indexed universal life coverage page walks through the moving parts.

Industry research underlines why protection belongs in the plan at all. As noted by LIMRA, a large share of households say they would feel financial hardship quickly if a primary earner passed away, which is exactly the gap a cash-value life insurance policy is built to close while it also grows. If you want a foundation in how permanent coverage protects households, start with our overview of life insurance built around real families.

How to vet a properly structured IUL

Most of the horror stories about IUL trace back to one thing: a policy that was sold to maximize the agent's commission rather than designed to maximize your cash value. If you do decide an IUL belongs in your plan, the structure is everything. Here is what to ask about and look for, in plain terms.

- How is it funded relative to the death benefit? A policy designed for cash value generally carries the lowest death benefit the rules allow for the premium going in, so more of your money builds value instead of buying insurance you do not need. Ask the agent to explain this choice out loud.

- Where does it sit against the modified endowment contract line? Overfund a policy past a certain point relative to its death benefit and it becomes a modified endowment contract, which changes the tax treatment of access. A well-designed policy is funded right up to, but not past, that line when cash value is the goal.

- What do the guaranteed columns show? Look at the worst-case guaranteed illustration, not just the projected one. If the policy only makes sense in the rosy projection, that is a warning.

- How do the loan provisions work? Understand the difference between the loan types offered, what the loan charges are, and what happens to the policy if loans and interest outpace the cash value. This is where over-borrowing quietly lapses policies.

- What are the surrender charges and for how long? Know the early-exit cost and the years it applies, so you go in understanding this is a long-term commitment, not a savings account you dip into freely.

If you want a deeper look at how the cash value mechanics function on their own, our breakdown of how an IUL builds tax-free income goes step by step. And if a policy ever feels too good to be true on the page, it usually is. The honest version of an IUL has costs, caps, and conditions, and a strategist worth your time will say so before you sign anything.

Frequently asked questions

Is an IUL better than a 401(k)?

Neither is universally better, because they do different jobs. A 401(k) is hard to beat when an employer matches your contributions, because that match is an immediate boost. An IUL can be attractive for tax-free income flexibility and a death benefit, but it carries policy fees and is not guaranteed to perform a certain way. The right answer depends on your income, tax picture, time horizon, and goals.

What is the difference between an IUL and a 401(k)?

A 401(k) invests your money directly in the market, often with an employer match and pretax contributions, but the balance rises and falls with the market and withdrawals in retirement are taxed. An IUL is a life insurance policy that ties growth to a market index with a floor that protects against losses, builds cash value you can access tax-free through loans, and pays a death benefit. In short, a 401(k) is pure investing, while an IUL is protection plus tax-advantaged cash value.

Should you max out a 401(k) before funding an IUL?

For most people, funding a 401(k) up to the full employer match comes first, because that match is an immediate guaranteed return you cannot beat. After the match, some people direct extra dollars into a properly funded IUL for tax-free access and downside protection a 401(k) does not offer. The right split depends on your income, tax picture, and how the IUL is designed, so run the numbers before choosing.

Can you have both an IUL and a 401(k)?

Yes, and many families do. A common approach is to contribute to a 401(k) at least up to any employer match, then fund an IUL for tax diversification and a death benefit. Using both lets you balance taxable and tax-free sources of retirement income so you are not betting everything on one tax outcome decades from now.

How is IUL retirement income tax-free?

Cash value inside a properly structured indexed universal life policy can generally be accessed through policy loans and withdrawals that are not treated as taxable income under current tax law, as long as the policy stays in force and is not a modified endowment contract. The rules are specific and can change, so confirm your situation with a licensed tax professional.

What are the downsides of an IUL?

An IUL has a cost of insurance and policy charges, caps and participation rates that can limit how much of an index gain you receive, and it needs to be funded consistently over many years to work as intended. If a policy is underfunded, over-loaned, or surrendered early, it may lapse or fail to perform the way it was illustrated. These trade-offs are why honest design matters.

Is an IUL a good replacement for a 401(k) match?

For most people, no. An employer match increases your contribution the moment you make it, so it usually makes sense to capture that first. An IUL is better viewed as a complement for tax-free flexibility and protection rather than a replacement for free matching dollars.

Does an IUL have contribution limits like a 401(k)?

An IUL does not use the same annual IRS contribution limit as a 401(k), so it can hold larger amounts, but it has its own funding rules. Pay in too much relative to the death benefit and the policy can become a modified endowment contract, which changes how the money is taxed when you access it. Within those limits, an IUL offers more funding flexibility than a 401(k).

Want a straight answer for your situation?

Fifteen minutes. We will look at your goals, your tax picture, and whether a 401(k), an IUL, or both make sense for you. No pressure, no jargon, just an honest read on your numbers.

Get a Quote Book a 15-Min Call Prefer to start fast? Save my card or get a quick IUL quote.Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, or legal advice. Please talk with a licensed professional about your situation before making a decision. Product availability, features, caps, and fees vary by state, age, health, and carrier, and any coverage is subject to underwriting approval. IUL policy values are not guaranteed and are subject to the claims-paying ability of the issuing insurance company.