Life Insurance for First Responders: What Police, Fire, and EMS Families Should Know

The Short Version

Life insurance for first responders is its own animal. Some carriers treat police, fire, corrections, and EMS work as hazardous and may add a charge or decline, while others do not penalize the job at all. Department coverage is small and not portable, and PSOB pays only for a line of duty death. A personal policy, placed with the right carrier and sized to your family, fills the gap.

If you run toward what everyone else runs from, you already understand risk better than most. So here is the question worth sitting with for a minute: if you did not come home from a shift, would your family be okay financially? Life insurance for first responders is built around that exact worry, and it works a little differently than it does for everyone else, mostly because of how carriers view the job.

This guide goes deep. We will cover why your occupation can change your rate, how dangerous occupation underwriting actually works, where department and federal coverage fall short, the policy types that fit police, fire, corrections, and EMS families, how much coverage you really need, what to disclose on the application, and how to shop a personal policy without the pressure. We will keep it plain. No jargon you need a dictionary for.

What this guide covers

- Why the job changes the underwriting

- Dangerous occupation underwriting, in plain English

- The department coverage gap and PSOB

- Department coverage vs PSOB vs a personal policy

- Policy types that fit first responders

- What police, fire, corrections, and EMS families each face

- How much coverage do you actually need

- Health, tobacco, and mental health on the application

- How to shop it the right way

- Common mistakes to avoid

- Frequently asked questions

Why life insurance for first responders is different

For a typical office worker, an insurance company mostly looks at age and health. For a first responder, the carrier also looks at the job itself. That single difference is why two healthy people the same age can be quoted very different rates: one drives a desk, the other runs into burning buildings or makes traffic stops at 2 a.m.

Here is the part most people do not realize. Carriers do not agree with each other. One company may add a charge for law enforcement or firefighting, and the next company down the street may not blink at it. Because the rules are not standardized, the carrier you apply to can matter as much as your blood pressure. That is the whole reason an independent broker, who can shop many carriers instead of just one, tends to matter more for this line of work, the same way it does for other trades carriers may treat as high risk, such as life insurance for truck drivers and owner operators.

It helps to know the scale of why this coverage exists. Firefighter line of duty deaths have run in the dozens each year for the last two decades, and law enforcement officers face fatal on the job injuries at rates well above the average occupation. But here is what those headlines miss, and it is the single most important fact in this entire guide: most first responders do not die in the line of duty. They die the same way most people do, from heart disease, cancer, or accidents off the clock, often years into retirement. That is exactly why a line of duty benefit alone leaves a family exposed, and why a personal policy that pays for nearly any cause of death is the foundation under everything else.

Coverage built for those who serve. Quick and free.

Dangerous occupation underwriting, explained simply

"Underwriting" is just the carrier's word for deciding whether to cover you and at what price. "Dangerous occupation underwriting" means the company is factoring your job's risk into that decision. A few things can happen:

- Standard rate. The carrier treats your job like any other and prices you on your health alone. This is the goal, and many carriers do exactly this for first responders.

- Rated up. The carrier moves you to a higher price class because it views the work as higher risk. Your policy still issues, it just costs more than it might elsewhere.

- Flat extra. Some carriers add a fixed dollar amount per thousand of coverage for certain hazardous duties, for example a few dollars per thousand for wildland firefighting or bomb squad work. A flat extra is often temporary and may come off after a set number of years.

- Declined. A small number of carriers will simply pass on certain occupations or certain specialty duties. A decline at one company is not a decline everywhere.

The honest truth is that some carriers treat law enforcement, fire, corrections, and EMS as hazardous and will rate or decline, while others do not. No one can promise you a specific rate or that any one carrier will approve you, because that depends on your health, the carrier, and your state. What a good broker can do is know the landscape and steer you toward the companies that have historically underwritten the job fairly.

Two practical notes. First, the application will usually ask about specialty assignments, not just your title. A patrol officer, a SWAT operator, and a K9 handler can be looked at differently. Be accurate about your actual duties. Second, the job is only one input. A healthy non-smoking firefighter will almost always be quoted better than a smoker in a low risk office job, because health still drives most of the price.

The department coverage gap, and what PSOB really does

Most first responders have some coverage through work, and that is a good thing. The trouble is assuming it is enough. There are two common blind spots.

Department or union group coverage is usually small and not portable. It is often one or two times your salary, which sounds like a lot until you weigh it against a mortgage, a couple of kids, and years of lost income. More importantly, it is tied to the job. The day you change departments or retire, that coverage typically ends. It does not follow you, and you usually cannot take it with you at the same price. That is the department coverage gap in one sentence: it is small, and it is borrowed.

Some unions and associations offer a conversion or portability option when you leave, but the converted rate is frequently much higher than a personal policy you would have qualified for on your own years earlier. Relying on conversion later is a gamble on your future health and your future budget.

PSOB is a line of duty benefit, not life insurance. The Public Safety Officers Benefits program is a one time federal payment for the survivors of an eligible public safety officer who dies, or who is permanently and totally disabled, in the line of duty. It is meaningful and it matters. But it only pays for a line of duty event. It does not pay if you pass away off duty, from an illness, or from anything unrelated to the job. And as we covered above, most first responder deaths are not line of duty. You can read how the federal Public Safety Officers Benefits program defines a covered death, and you will quickly see why families still need a personal policy underneath it.

A personal policy is the piece that does not have those holes. You own it, so it follows you between departments and into retirement. It pays for nearly any cause of death, on duty or off. And the amount is whatever you qualify for and choose, not whatever your employer happens to offer. Industry research keeps finding the same thing: a large share of households say they do not have enough life insurance, and many underestimate how affordable a simple term policy can be. According to research published by LIMRA, the gap between the coverage people know they need and the coverage they actually own remains wide, and first responder families, leaning on group and federal benefits, are right in the middle of it.

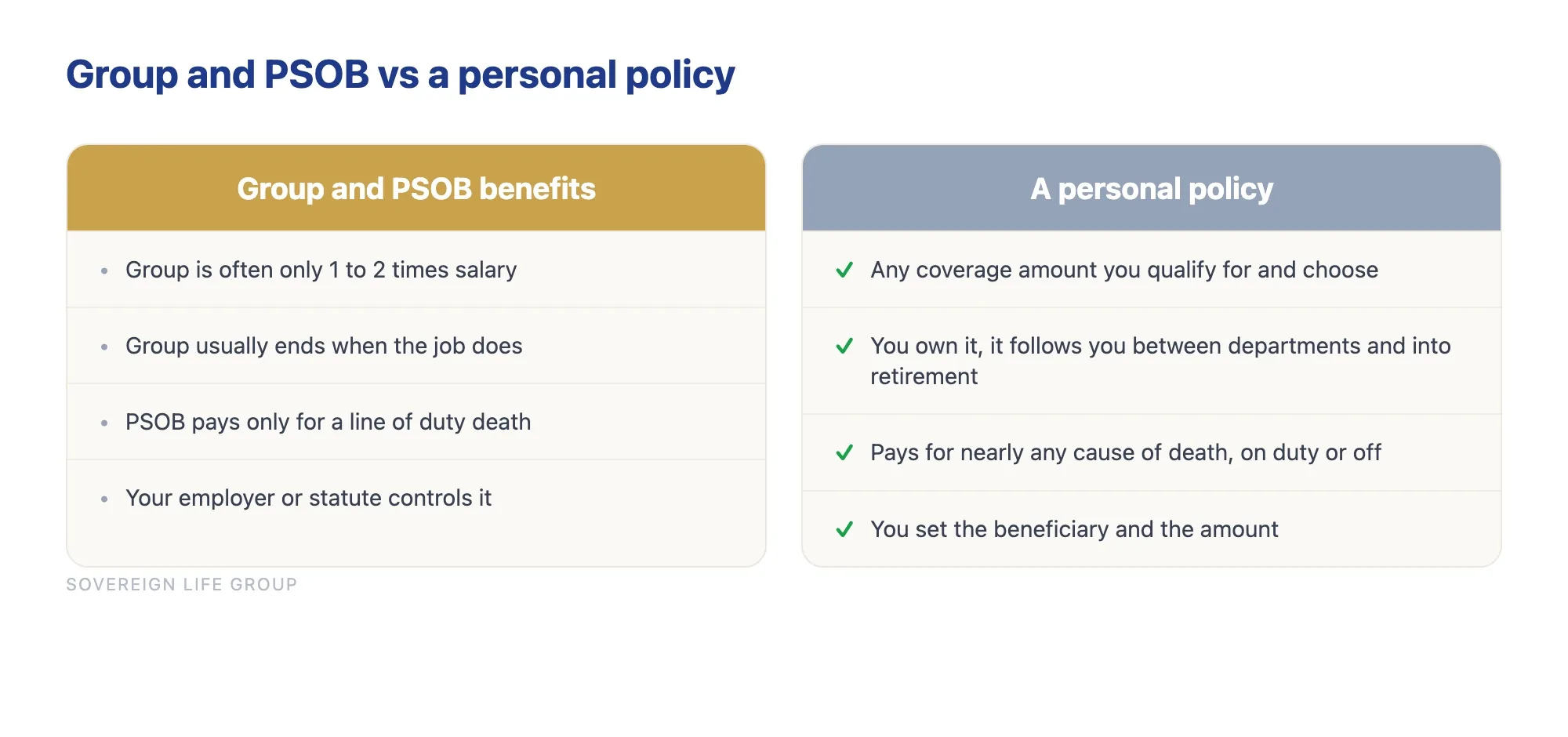

Department coverage vs PSOB vs a personal policy

It helps to see the three side by side. Most first responder families end up using all three together, with a personal policy as the foundation that fills the gaps the other two leave open.

| What to know | Department or union group coverage | PSOB (federal) | Personal life insurance policy |

|---|---|---|---|

| What triggers a payout | Death while employed and covered | Line of duty death or permanent and total disability only | Nearly any cause of death, on duty or off |

| Typical size | Often one to two times salary | A set federal amount, adjusted over time | Whatever coverage amount you qualify for and choose |

| Do you keep it if you leave or retire | No, it usually ends with the job | Not applicable, it is a one time benefit | Yes, you own it for the term or for life |

| Covers off duty death or illness | Often yes while employed, but ends when the job does | No | Yes |

| Who controls it | Your employer | The federal program | You |

| Can you set the beneficiary and amount | Limited | Set by statute | Yes, your choice within what you qualify for |

Policy types that fit first responders

There is no single "first responder policy" you must buy. There are standard policy types, and the right one depends on the job your money needs to do. Here is the plain version of each.

Term life insurance

Term covers you for a set number of years, often 10, 20, or 30, and pays a death benefit if you pass during that window. It is the most affordable way to get a large benefit, which is why it is the workhorse for most working first responders with a mortgage and kids at home. You match the term length to how long your family will depend on your income. If your youngest is two, a 30 year term carries them to independence. If your need ends when the mortgage does, match the term to the loan.

The honest trade-off: term has no cash value, and coverage ends when the term does. If you still need protection at the end of the term, you renew, convert, or buy new at an older age. Many term policies include a conversion option that lets you switch to permanent coverage later without a new medical exam, which can be valuable if your health changes.

Permanent coverage: whole life and IUL

Permanent insurance is designed to last your whole life and can build cash value over time. Whole life offers fixed premiums and guaranteed cash value growth. An indexed universal life policy ties cash value growth to a market index with a floor and a cap, which means more upside potential but values that are not guaranteed. Permanent coverage fits lasting needs: final expenses that never expire, leaving a legacy, or certain estate goals.

The honest trade-off, and it is a real one: permanent insurance costs significantly more per dollar of death benefit than term, and on indexed products the cash value growth is not guaranteed and fees and structure matter a great deal. Permanent coverage is not automatically better. It is better for specific jobs and worse as a way to get the most death benefit for the least money. Many first responder families use a large term policy for the income replacement years and a smaller permanent policy for the needs that never go away.

Final expense and guaranteed issue

For older first responders or retirees, or for those managing a health condition, final expense whole life is built for modest benefit amounts to cover a funeral and final bills, with simpler underwriting. Guaranteed issue policies ask few or no health questions and cannot decline you for health, in exchange for a smaller benefit and a waiting period before the full benefit applies. These are purpose built tools, not a first choice for a healthy 35 year old, but a real option when the situation calls for it.

Riders worth knowing about

Riders are add-ons that adjust what a policy does. A few are especially relevant to first responders:

- Living benefits, also called accelerated death benefits. These let you access part of the death benefit early if you are diagnosed with a qualifying terminal, chronic, or critical illness. Given the cancer and cardiac risks tied to the work, this rider matters to a lot of first responders.

- Waiver of premium. If you become disabled and cannot work, this keeps the policy in force without you paying premiums.

- Child or spouse riders. A simple way to add modest coverage for the rest of the household on one policy.

- Accidental death benefit. Pays an additional amount if death is by accident. Useful, but remember it does not pay for illness, so it is a supplement, not a foundation.

See your options in about 2 minutes, no pressure.

What police, fire, corrections, and EMS families each face

The risk picture is not identical across the badge, the helmet, the rig, and the cell block, and carriers see them differently too.

For police officers, some carriers flag law enforcement as hazardous and add a charge, while many do not. Shift work, the physical toll, exposure to the unexpected, and specialty assignments like SWAT or narcotics all factor in. The right carrier underwrites the officer, not the headline. Patrol, detective, and administrative roles are often viewed more favorably than high risk tactical units, so accurate duty descriptions help.

For firefighters, the concerns carriers weigh include smoke and chemical exposure over a career, the cardiac demands of the work, and career versus volunteer status. Municipal structural firefighters are usually underwritten differently than wildland and smokejumper roles, which carry the most scrutiny and are the most likely to draw a flat extra. The spread between carriers is wide, which is exactly why comparison matters.

For EMTs and paramedics, long hours, lifting, road risk, and exposure all come into play, and group coverage through a private ambulance company is often thin or absent. Flight medics and tactical EMS may see additional underwriting questions. A personal policy gives EMS families control that the job does not.

For corrections officers, the work is consistently treated as higher risk by a subset of carriers due to the assault and exposure environment, so this group benefits the most from shopping carriers that do not penalize the role. Dispatchers and 911 telecommunicators, by contrast, usually face little or no occupation rating, though the stress load is real and worth planning around.

Many first responders served in the military before pinning on the badge, and if that is you, the same shop-around logic applies to your life insurance options as a veteran, including the VGLI window after separation. Whatever the role, the core advice is the same. Compare carriers, do not assume your work coverage is enough, and lean on someone who can shop the whole shelf rather than sell you one company's product.

How much life insurance do first responders actually need

This is the question that paralyzes people, so let me make it simple. You are not trying to hit a magic number. You are trying to replace what your family would lose and cover what they would owe. A common starting point is ten to fifteen times your income, but a quick worksheet gets you closer to the truth. Agents call it the DIME method.

- D is for debt. Add up everything that would not disappear: car loans, credit cards, co-signed debt, and any business debt.

- I is for income. Decide how many years your family should be able to replace your income, then multiply. Until the youngest child is grown is a common target.

- M is for mortgage. Add the full payoff of your home loan so your family can stay in the house rather than sell under pressure. This is the heart of mortgage protection coverage.

- E is for education and final expenses. Add the cost of getting the kids through school and the cost of a funeral and final bills, so no one inherits that on top of grief.

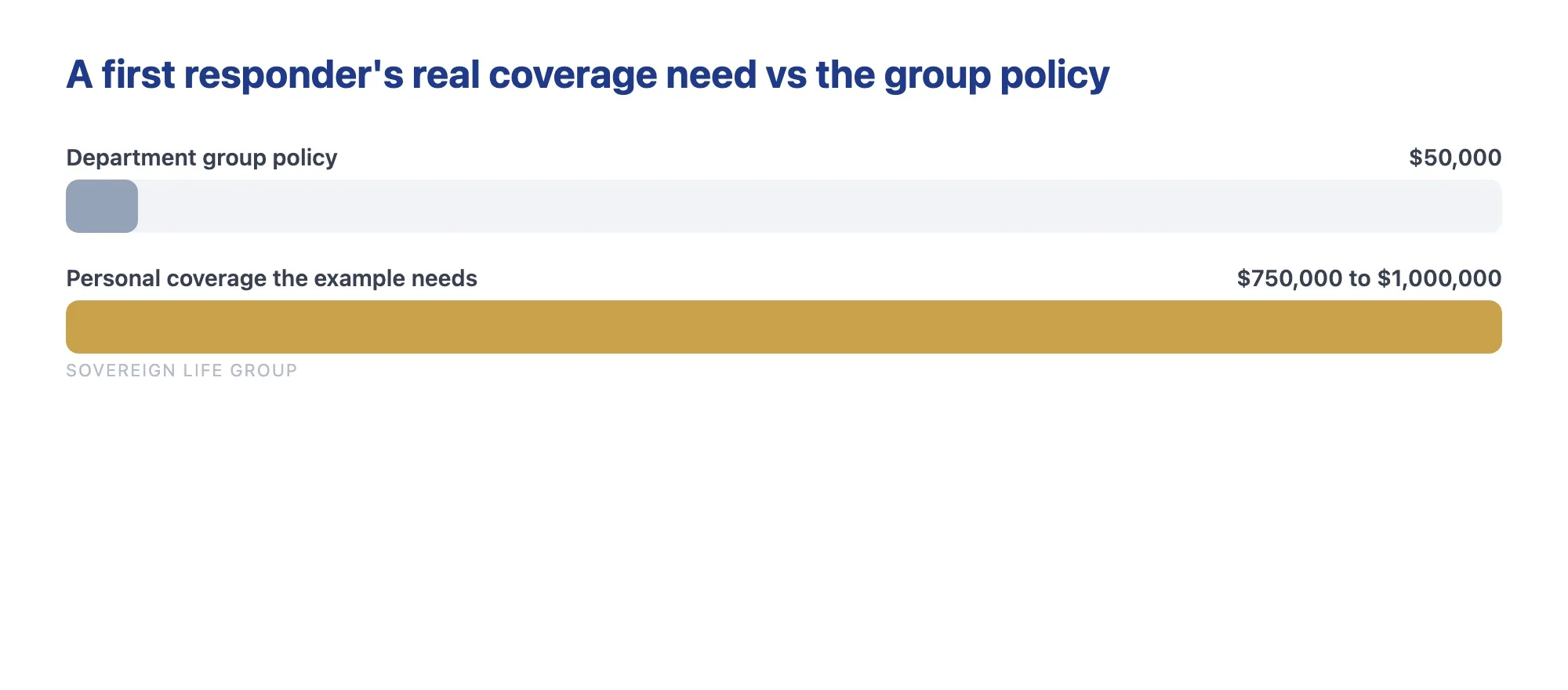

Add those four together, then subtract what you already have, such as a department group policy and any savings. The result is roughly the personal coverage to aim for. A worked example: a 34 year old paramedic earning 70,000 dollars with a 280,000 dollar mortgage, two young kids, and a 50,000 dollar department policy might land around 750,000 dollars to 1,000,000 dollars of personal term coverage once income replacement, the mortgage, and education are stacked up and the small group policy is subtracted. Your numbers will differ, but the method is the point.

Health, tobacco, and mental health on the application

A few honest words about the application itself, because first responders ask about these more than anything else.

Tobacco and nicotine. Smoking or vaping moves you into a tobacco rate class that can cost noticeably more, regardless of your job. Cigars, chew, and nicotine pouches can count too, and rules vary by carrier. If you have quit, the length of time since you stopped matters, so it is worth asking which carriers are most favorable to recent quitters.

Mental health, PTSD, and counseling. This is a real worry in the first responder community, and the fear is bigger than the reality. Seeking counseling or being treated for anxiety, depression, or post-traumatic stress does not automatically raise your rate or get you declined. Carriers look at the specifics: whether it is well managed, whether there has been any hospitalization, and how recent any episodes were. Getting help is the responsible thing to do, and it should not stop you from getting covered. An experienced broker knows which carriers handle these histories most fairly. Please do not skip care to protect an application.

Be accurate, not optimistic. The application asks about your occupation, duties, health, and habits for a reason. Material misstatements can create problems for your family at claim time, during the contestability period in the first two years of a policy. Placing you with a carrier that already treats your job and your health history fairly is far better than hoping something goes unnoticed. Honesty up front is what makes the claim pay later.

How to shop life insurance for first responders the right way

You do not need to become an expert. You need a process and the right person in your corner. Here is the short version.

- Know your numbers first. Run the DIME worksheet above so you walk in with a target rather than a guess.

- Use an independent broker, not a single carrier. Because carriers disagree on how to treat your occupation, the ability to compare many of them is the single biggest lever on your rate. A captive agent can only offer one company's opinion of your job.

- Ask about no exam options. Many carriers offer no exam coverage that approves with a few health questions, sometimes within the week. We compare exam and no exam paths so you see both, because the exam path sometimes wins you a better class.

- Layer it. Keep your group coverage and PSOB eligibility, and build a personal policy underneath as the foundation that follows you for life.

- Add a conversion option and living benefits where it makes sense. These cost little or nothing up front and protect you if your health or your needs change.

- Read the fine print on the job question. Be honest about your occupation and specialty duties on the application. Accuracy is what keeps a claim from being contested.

If you want the deeper, role by role breakdown, our pillar page on life insurance for first responders covers police, fire, EMS, and corrections in one place. If you are simply weighing whether you have enough overall, our overview of life insurance options for families is a good starting point. And when you are ready to talk specifics, the coverage options for families page lays out how the pieces fit together.

Common mistakes first responders make with life insurance

After a lot of these conversations, the same handful of avoidable mistakes come up again and again. Knowing them is half the battle.

- Assuming the department policy is enough. One to two times salary rarely covers a mortgage plus income replacement plus raising kids. It is a start, not a finish.

- Counting on PSOB as life insurance. It pays only for a line of duty event, and most deaths are not line of duty. Plan for the more likely outcome, not just the headline one.

- Applying to one carrier and accepting the first answer. A single rated quote feels like a verdict. It is one opinion. The next carrier may price your job at standard.

- Waiting for a quieter season. Age and health only move one direction. The rate you can lock today is generally the best you will be offered, because tomorrow you are older and your health is less certain.

- Buying only accidental death coverage. It is inexpensive because it pays in narrow circumstances. It is a supplement to real coverage, not a replacement for it.

- Hiding counseling or a manageable condition. It can void a claim later and is usually unnecessary, because the right carrier would have covered you anyway.

Want a straight answer for your situation?

A short, no pressure quote built around your job, your family, and your budget. We will compare the carriers that underwrite first responders fairly so your work is not held against you.

Get a free quote Prefer to talk it through first? Book a 15-minute review and we will look at where you stand before anything else.Frequently asked questions

Does being a first responder raise my life insurance rate?

It can with the wrong carrier, because some treat police, fire, corrections, and EMS work as a hazardous occupation and may add a charge or decline. Many carriers do not penalize the job at all. Because an independent broker can shop the companies that underwrite first responders fairly, your work does not have to inflate your rate.

Is my department or union life insurance enough?

Usually not. Group coverage through your department is typically small, often one or two times salary, and it is not portable, so you lose it when you change jobs or retire. A personal policy is yours to keep for nearly any cause of death and follows you for life.

What does PSOB cover and is it the same as life insurance?

PSOB is a one time federal benefit that pays only for a line of duty death or permanent and total disability of an eligible public safety officer. It is not life insurance, it does not cover an off duty death or an illness, and most first responder deaths are not line of duty. A personal policy covers your family regardless of how you pass.

Do first responders need a medical exam to get covered?

Often no. Many carriers offer no exam coverage that approves with a few health questions, sometimes within the same week. An independent broker can compare exam and no exam options so you see your choices side by side, since the exam path sometimes earns a better health class.

How much life insurance should a first responder have?

A common starting point is ten to fifteen times your income, then refined with the DIME method: add your debt, the income you want to replace, your mortgage payoff, and education plus final expenses, and subtract what you already have. The goal is to keep your family in the home and replace your income for as long as they would feel its loss.

Will counseling or PTSD treatment hurt my application?

Not automatically. Carriers look at whether a mental health condition is well managed and how recent any episodes were, and many cover well managed histories at standard rates. Getting help is the responsible move, and an experienced broker knows which carriers handle these histories most fairly. Do not skip care to protect an application.

Prefer to talk it through first? You can always book a 15 minute review and we will look at where you stand before anything else.

Joseph McDermott is a licensed life insurance agent (NPN 22121673), licensed in 27 states. Brokered through Family First Life, in partnership with Catalyst Life. This article is educational and is not financial, tax, legal, or benefits advice. No rate or approval is guaranteed, and product availability, features, and rates vary by occupation, health, carrier, and state. PSOB is a federal program with its own eligibility rules. Please talk with a licensed professional about your situation before making a decision. Any guarantees are subject to the claims paying ability of the issuing insurance company.