Everything so far has been the theory of a machine that billionaires used. Here is the part that matters most to you. You do not have to be one to run a smaller version of it. The plumbing is the same whether the reservoir holds a few hundred thousand dollars or a few hundred million. Only the size of the pipe changes.

The families in the last three chapters can make this sound like a rich person's game. It is not, and it never really was. The Rockefellers did not have a product you are locked out of. They had a habit, applied for a long time, with discipline. Every one of those things is available to a nurse, a plumber, a teacher, or a small business owner who decides to begin.

It is consistency, not size

Here is the catch, and it is the opposite of what the sales pitch usually implies. The number that matters is not how much you put in. It is whether you keep putting it in. A modest amount funded faithfully for twenty years beats a large amount funded for three and then abandoned when money got tight. A policy you overreach on and then let lapse is worse than one you never started, because you paid for the coverage and then walked away before the reservoir ever filled.

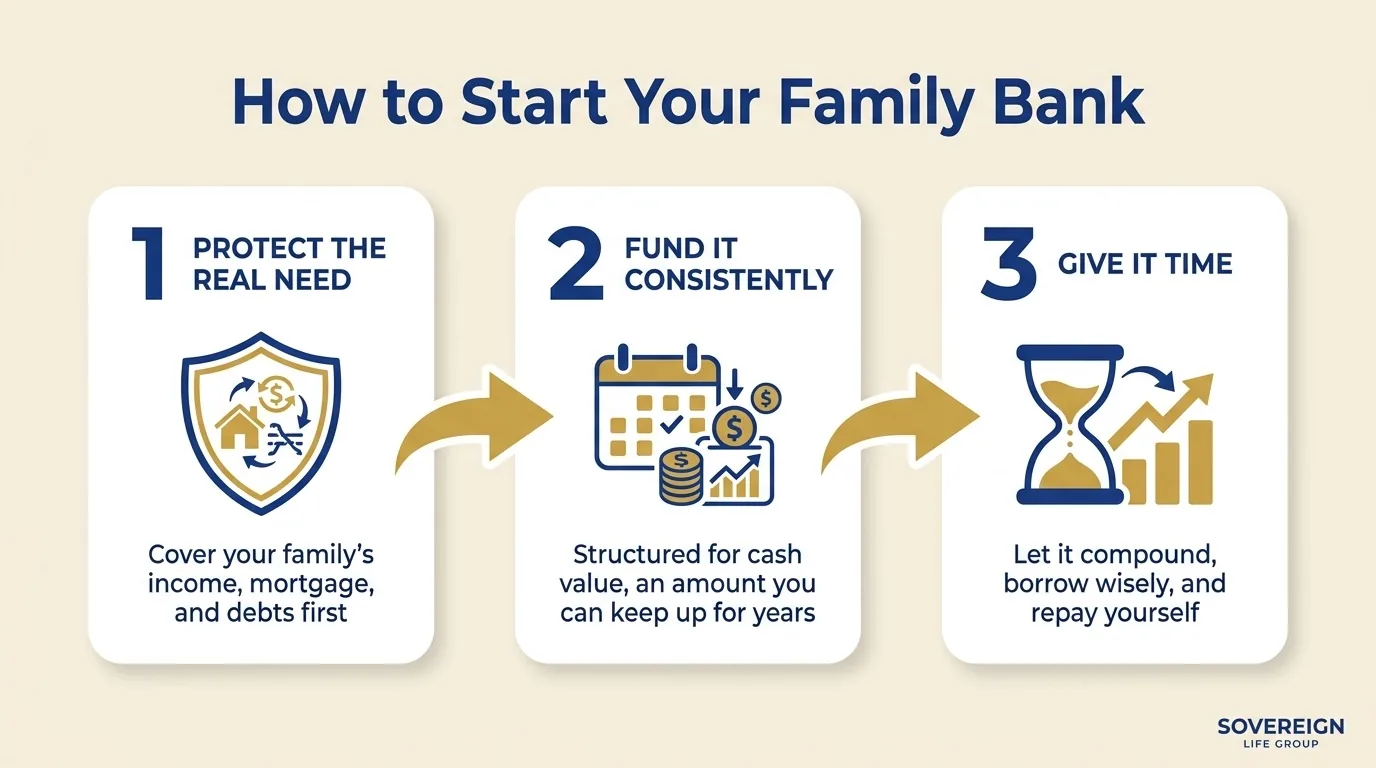

So the first rule of building on a normal income is to choose an amount you can genuinely sustain through a rough patch, not the biggest number a projection makes look exciting. The machine rewards the tortoise. Start where you can stand, then step it up as your income grows. Here is the order that keeps people out of trouble.

None of those three steps requires a windfall. They require a decision, and then repetition, which is honestly the hardest part and also the only part the wealthy never skip. That is the whole secret, if there even is one. The Rockefellers were not doing something you cannot do. They were doing something most people quit. Do not quit, and the machine does the rest.

Start now, not when you can afford more

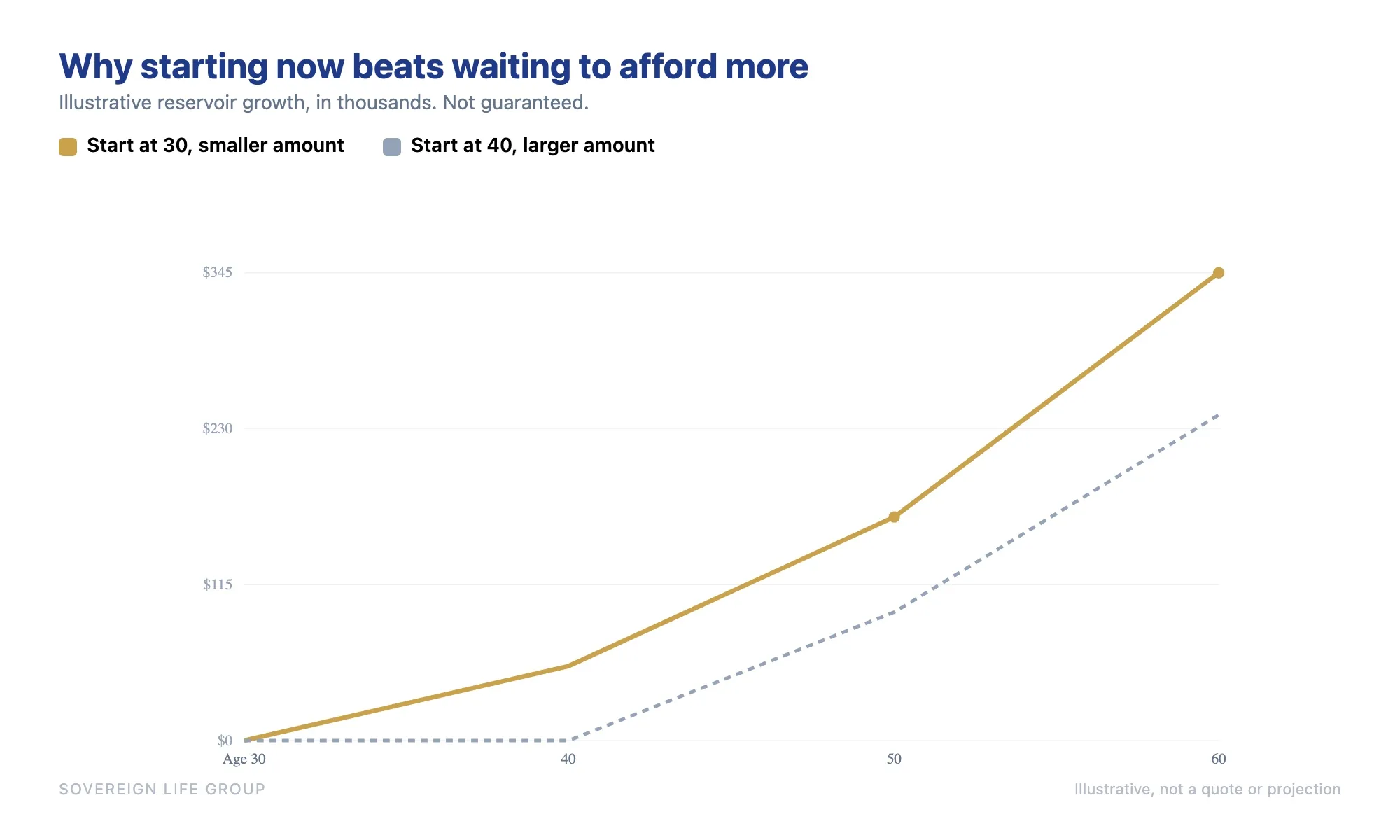

The other rule is simpler. The best day to start was years ago, and the second best day is today. Because the whole engine runs on compounding, time does more of the heavy lifting than the size of your payment ever will. A smaller policy started at thirty routinely outgrows a bigger one started at forty, for the plain reason that the earlier reservoir had ten more years to fill.

Take a healthy couple in their early thirties. They put a few hundred dollars a month into a properly structured policy, sized first to protect their income and mortgage. For the first few years the cash value is modest and the protection is the whole point. By their forties, the reservoir is real enough to borrow against for a car or a business. By retirement, it is a tax-advantaged pool they can draw on for income, with a death benefit still waiting for the next generation. Illustrative only, not a quote or a promise of any result.

Getting the design right

One warning before you shop. Two policies with the same premium can behave very differently depending on how they are built. A policy structured to pay the agent the largest commission is designed differently from one structured to grow your cash value quickly, and that difference shows up in your reservoir for decades. You want an agent who will build it to fund the bank, which sometimes means a smaller commission for them and a fuller pool for you. Ask them directly how the design affects your early cash value. A good one will welcome the question.

Two policies with the same premium can build very different reservoirs. The design is not a detail. It is the whole ballgame.

Two more guardrails, and then you are ready. First, protect before you accumulate. If your family is not yet covered for the real need, the mortgage, the income, the years of raising children, fix that first, because a half-funded bank is no comfort to a family that lost its earner too soon. Second, keep the policy inside the tax rules so it does not tip into a modified endowment contract, which an experienced agent designs around as a matter of course. Get those right and you own a machine that works. Get them wrong and you own an expensive disappointment, which is exactly what the next chapter is here to prevent.

For educational purposes only. Not financial, tax, or legal advice, and not a recommendation of any specific product. Historical accounts are illustrative and not a promise of any result. Life insurance is offered through licensed agents; policies have costs, are not bank accounts, and are not FDIC insured. Joseph McDermott is a licensed life insurance agent (NPN 22121673), brokered through Family First Life. Consult a licensed professional, a tax advisor, and an estate attorney before acting.