Everything good about a family bank can be undone by a handful of avoidable mistakes. This is the chapter the hype crowd skips, which is exactly why it is in here. Most people who fail with this strategy do not fail because it does not work. They fail because they ran it wrong.

None of these mistakes is exotic. Each one is ordinary, human, and easy to make with a persuasive illustration sitting in front of you. The good news is that once you can name them, you can see them coming from a mile off, and steering around them is far easier than repairing the damage after the fact.

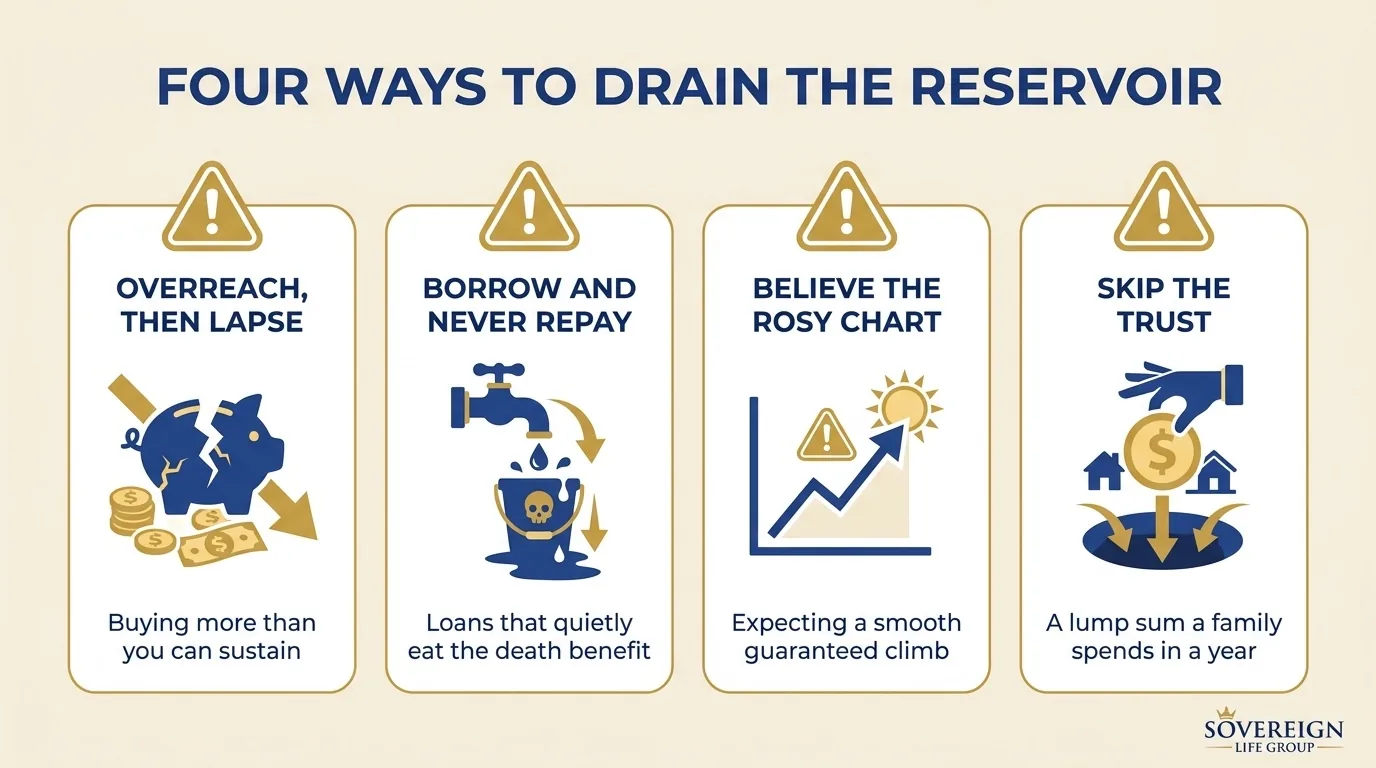

The leaks that start on day one

The first mistake is overreaching. A projection makes a big premium look thrilling, so you commit to more than your budget can survive, and then a job loss or a lean year forces you to stop. A lapsed policy is the worst outcome of all, because you paid for years and then walked away before the reservoir ever filled. Buy the payment you can hold through a storm, not the one that looks best on a sunny day.

The second is the wrong design. Two policies with the same premium can be built to enrich the agent or to grow your cash value, and the gap between them compounds for decades. The third is believing the rosy illustration. An index policy shown climbing in a smooth, guaranteed line every year for thirty years is not a plan, it is a sales tool. Ask to see the guaranteed column and a down year, then watch how the person across the table reacts.

Notice the common thread. Every one of these is a shortcut, a way to reach for the reward without the discipline that earns it. The strategy itself does not fail. The shortcut fails. Respect the machine and it holds up for a hundred years. Try to cheat it and it behaves exactly like everything else you cut corners on.

The mistake that hides in plain sight

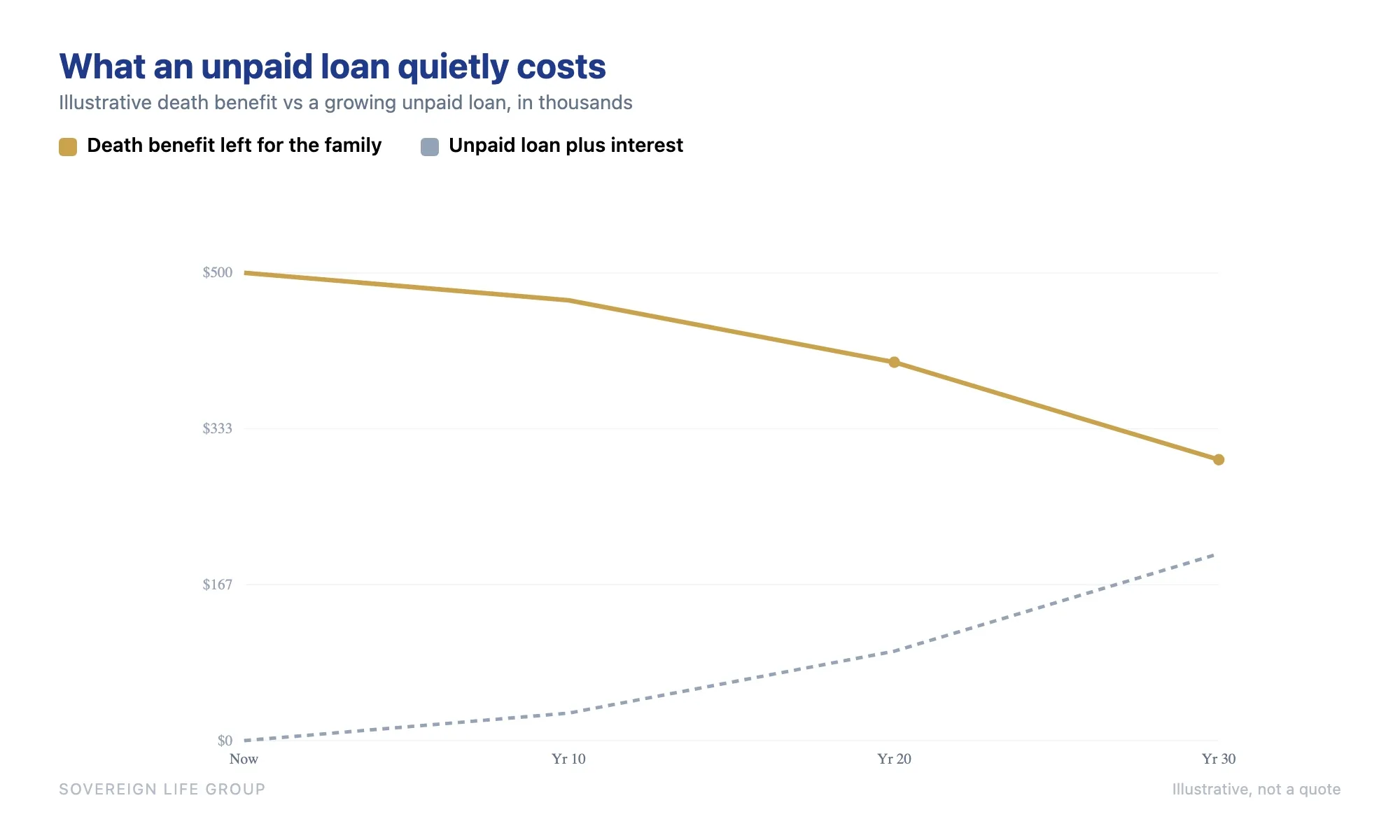

Then there is the one that feels harmless while you are making it. Borrowing from your policy is a feature, not a flaw. But a loan you never repay does not simply sit there quietly. The loan and its interest are subtracted from the death benefit, and if the balance grows large enough, it can eat through the cash value and collapse the whole policy, which can even trigger a tax bill on the way down. The reservoir you built to protect your family can be drained by the very person it was built for.

None of this is an argument against borrowing. It is an argument for treating your family bank like a bank, which means paying yourself back. Look at what an unpaid balance quietly does over time.

Discipline is the whole cost of admission. Borrow for real reasons, pay it back on a real schedule, and this problem never touches you. A policy loan is one of the few loans in your life with no committee to answer to and no due date stamped on it, which is a gift and a trap in the same envelope. The people who win with it simply refuse to treat their own bank any worse than they would treat a stranger's.

The last two, and the biggest

The fifth mistake is skipping the plan for what happens after you are gone. A death benefit with no trust and no strategy behind it is just a lump sum, and a grieving family can spend a lump sum in a year. The structure is what turns a one-time gift into a system, and it is worth a conversation with an estate attorney long before anyone needs it.

There is no version of this strategy that rewards waiting. The machine only works if you turn it on.

And the biggest mistake of all is the quietest one. Waiting. Every year you spend deciding is a year the reservoir does not fill, and a year your age and health quietly make the coverage cost more. Delay is the one mistake that charges you interest whether you notice it or not. So the last chapter is short, and it is about a single thing. How to take the first real step, this week, without overthinking it.

Here is the truth sitting underneath all of these. Every mistake in this chapter is really just a different way of not starting, or not finishing. Avoid them and you are not doing anything clever or complicated. You are doing the boring thing, consistently, which is the only thing that has ever built lasting wealth for anyone.

For educational purposes only. Not financial, tax, or legal advice, and not a recommendation of any specific product. Historical accounts are illustrative and not a promise of any result. Life insurance is offered through licensed agents; policies have costs, are not bank accounts, and are not FDIC insured. Joseph McDermott is a licensed life insurance agent (NPN 22121673), brokered through Family First Life. Consult a licensed professional, a tax advisor, and an estate attorney before acting.