We have talked about the reservoir, the engine, and the two families. Now let's actually turn the machine on and watch the water move. Once you see the cycle run one full turn, the whole strategy stops sounding like a secret and starts sounding like plumbing, which is exactly what it is.

There are five stages, and none of them is complicated on its own. The power is in the loop. Each turn of the cycle leaves the family a little stronger than the turn before, and the loop is built to keep running long after the person who started it is gone.

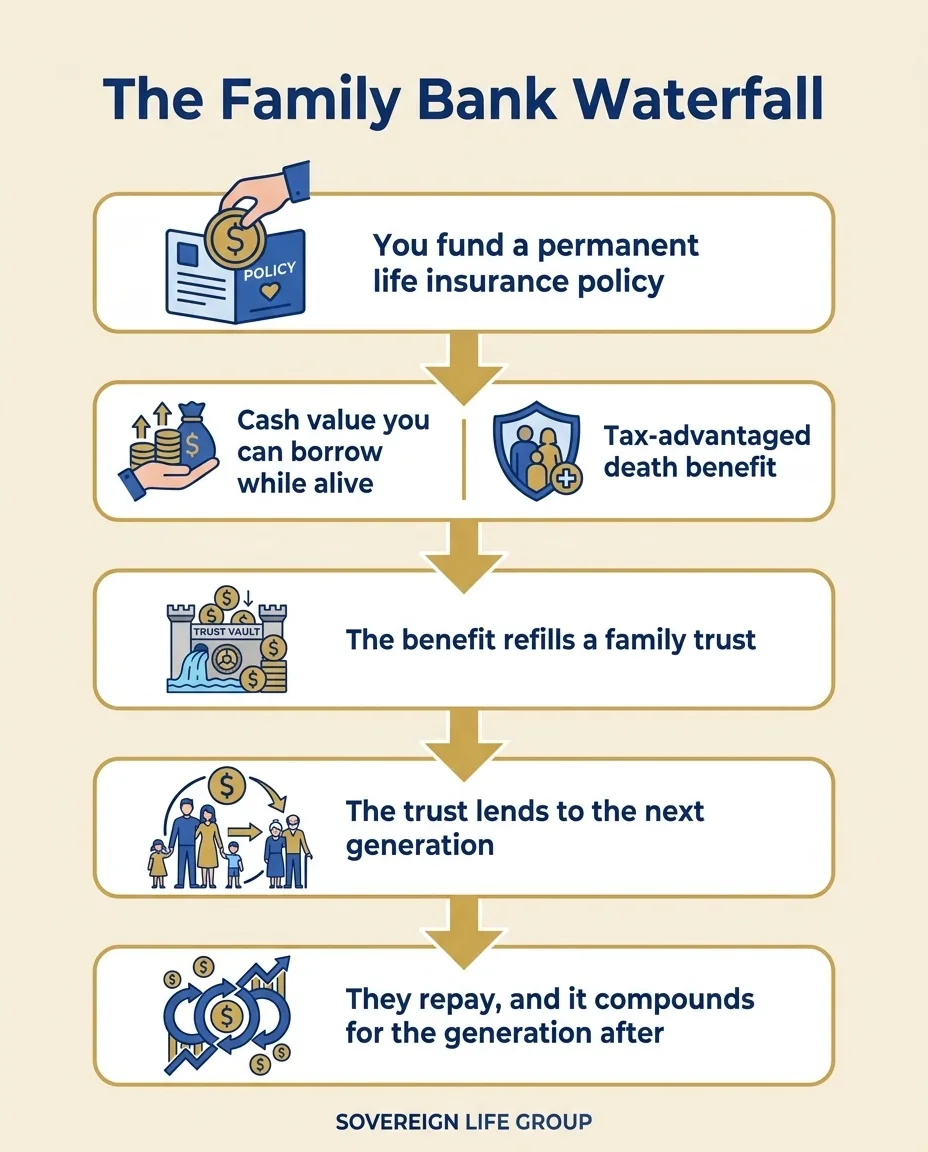

One full turn of the cycle

Stage one, you fund it. You pay premiums into a permanent policy, and part of every payment settles into the cash value. Stage two, it grows. That cash value compounds over the years on a tax-advantaged basis, quietly filling the reservoir whether you are paying attention or not. Stage three, you borrow. Once there is real value inside, you take loans against it for the things life actually costs, a home, a business, a child's education, income in retirement, all while the pool keeps growing behind the loan.

Stage four is the one most people miss, and it is the heart of the whole design. When you pass away, the death benefit, generally income tax free, pours into the reservoir and refills it, ideally inside a trust that holds it for the family. Stage five, the next generation inherits a full pool and the same simple rule: borrow from it, do not drain it. Then the cycle begins again. That is the waterfall.

Using it while you are alive

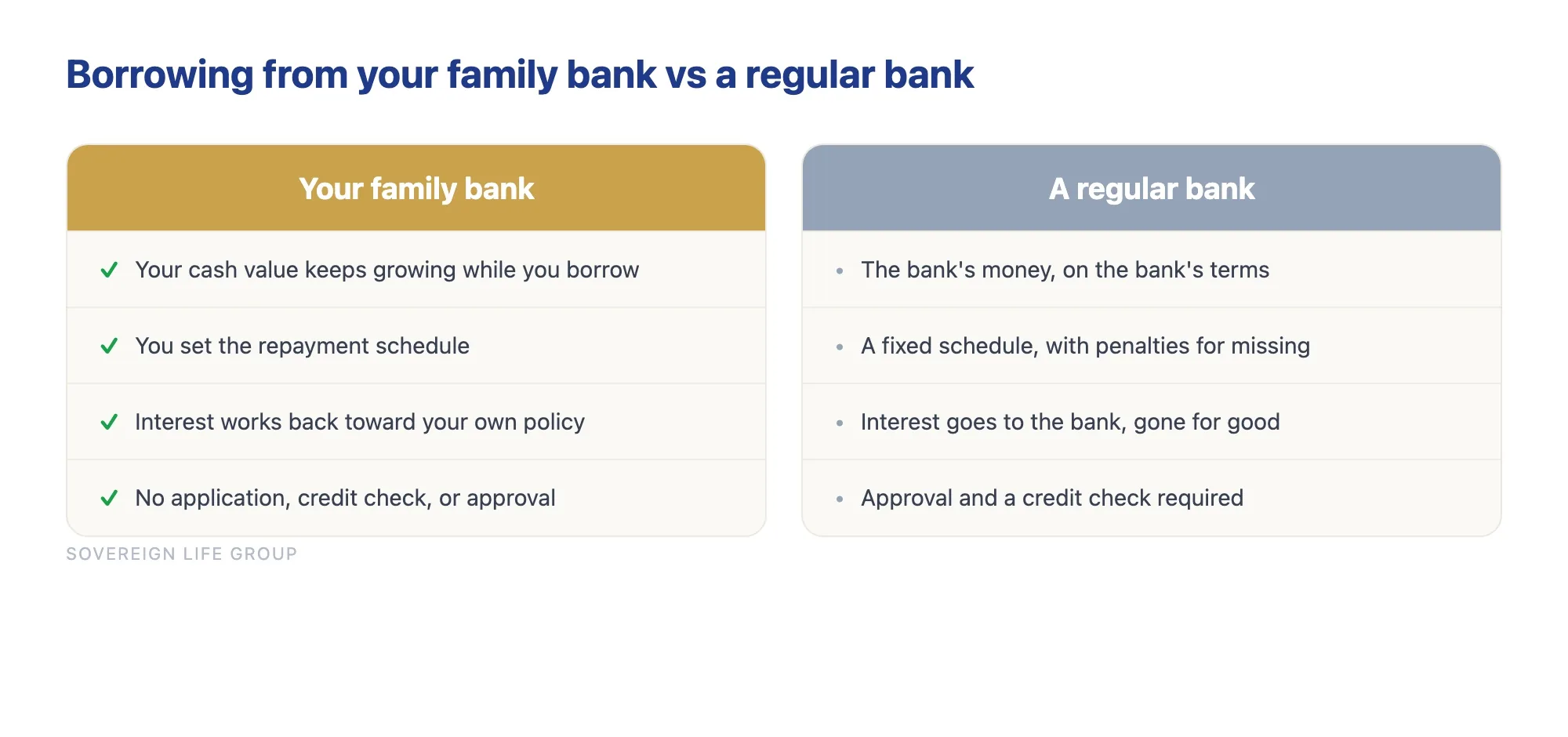

It is tempting to think of life insurance as a bet on dying. A family bank flips that. The busiest years of the machine are the years you are very much alive, borrowing against your own pool to fund the moves that build a life. This is where the "be your own bank" phrase earns its keep, because a loan from your own policy behaves very differently from a loan at a bank.

Say you need thirty thousand dollars for a down payment. Borrow it from your policy and your cash value keeps growing as if the money were still sitting there, because the loan is secured against your value rather than withdrawn from it. You repay on your own timeline, and the interest heads back toward your policy instead of toward a lender who will never think of you again. Put the two side by side and the difference is hard to unsee.

None of this means you should never use a real bank again. It means that for the borrowing you would have done anyway, doing it through your own policy quietly keeps the wealth inside the family instead of leaking a little of it out with every payment. The effect is small on any single loan and large over a lifetime of them. A family that runs its cars, its tuition, and its opportunities through its own pool for thirty years keeps a river of interest inside the household that most families ship off to lenders without a second thought. That recaptured interest is not a magic trick. It is just a leak, closed.

What happens when you are gone

Here is where the trust earns its place. Left on its own, a death benefit is a one-time gift that a grieving family can spend in a year. Held inside a properly drawn trust, that same benefit becomes the refill for the reservoir, released on terms you set while you were alive, lending to your heirs instead of simply handing them a check. This part is estate planning, and it is genuinely a job for an attorney, not a paragraph in a book. But the idea is simple. The trust turns a gift into a system.

The reservoir does not have to be enormous. It has to be consistent, and it has to outlive the person who built it.

Run that loop across three or four generations and the arithmetic starts to feel almost unfair, in your family's favor. Each generation borrows, repays, and adds its own contributions, and each death refills the pool for everyone still living. That is the quiet advantage the Vanderbilts never had and the Rockefellers never let go of. You do not need a dynasty to begin one. You need a single policy, one clear rule, and the patience to let the water rise. The next chapter shows you exactly how to start, on a budget that has nothing to do with oil or railroads.

For educational purposes only. Not financial, tax, or legal advice, and not a recommendation of any specific product. Historical accounts are illustrative and not a promise of any result. Life insurance is offered through licensed agents; policies have costs, are not bank accounts, and are not FDIC insured. Joseph McDermott is a licensed life insurance agent (NPN 22121673), brokered through Family First Life. Consult a licensed professional, a tax advisor, and an estate attorney before acting.