By now you might be waiting for the catch. If the engine that refills the reservoir is just life insurance, why doesn't everyone already own it? The answer is that most people have only ever met one kind of life insurance, and it is not the kind that builds a bank.

So let's clear up what a family bank actually is, in plain English, with none of the mystique and none of the sales gloss. It is simpler than it sounds, and the honest version keeps in the parts a good agent should never skip over. None of what follows takes a finance degree. If you understand the difference between renting a home and owning one, you already understand the difference between the two kinds of life insurance, because it is very nearly the same idea.

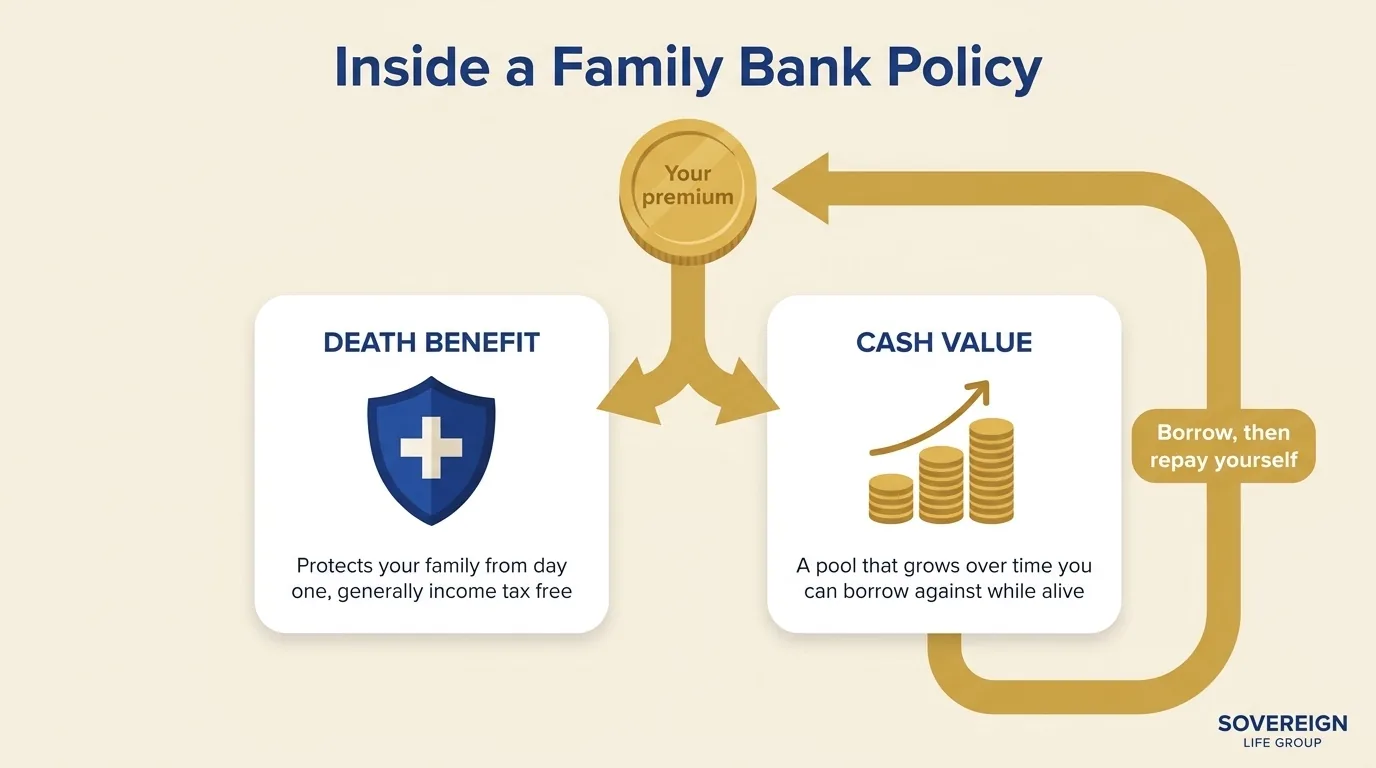

Two policies in one

Most people picture term life insurance. You pay a low premium, and if you die inside a set window, say twenty or thirty years, your family gets a check. Outlive the window and the coverage simply ends, with nothing left over. Term is excellent at one job, covering a big temporary risk cheaply. But it is not an engine. It builds nothing you can touch while you are alive.

A family bank runs on the other kind, permanent life insurance, most often whole life or indexed universal life. A permanent policy is really two things stacked into one. There is a death benefit, the check your family receives, which is generally income tax free and does not expire. And there is a cash value account, a pool of money inside the policy that grows over time on a tax-advantaged basis. That second part is the bank. It is the piece you can borrow against while you are still alive, for a down payment, a business, a college bill, or income in retirement.

That renting-versus-owning comparison holds up well. Term insurance is renting your coverage. You pay for protection during the years you need it most, and when the lease is up you walk away with nothing, which is completely fine if renting was all you needed. Permanent insurance is owning. You pay more, but a portion of every payment builds equity you keep, and one day that equity is yours to borrow against or draw on. Neither choice is wrong. They are answers to two different questions.

How the reservoir fills

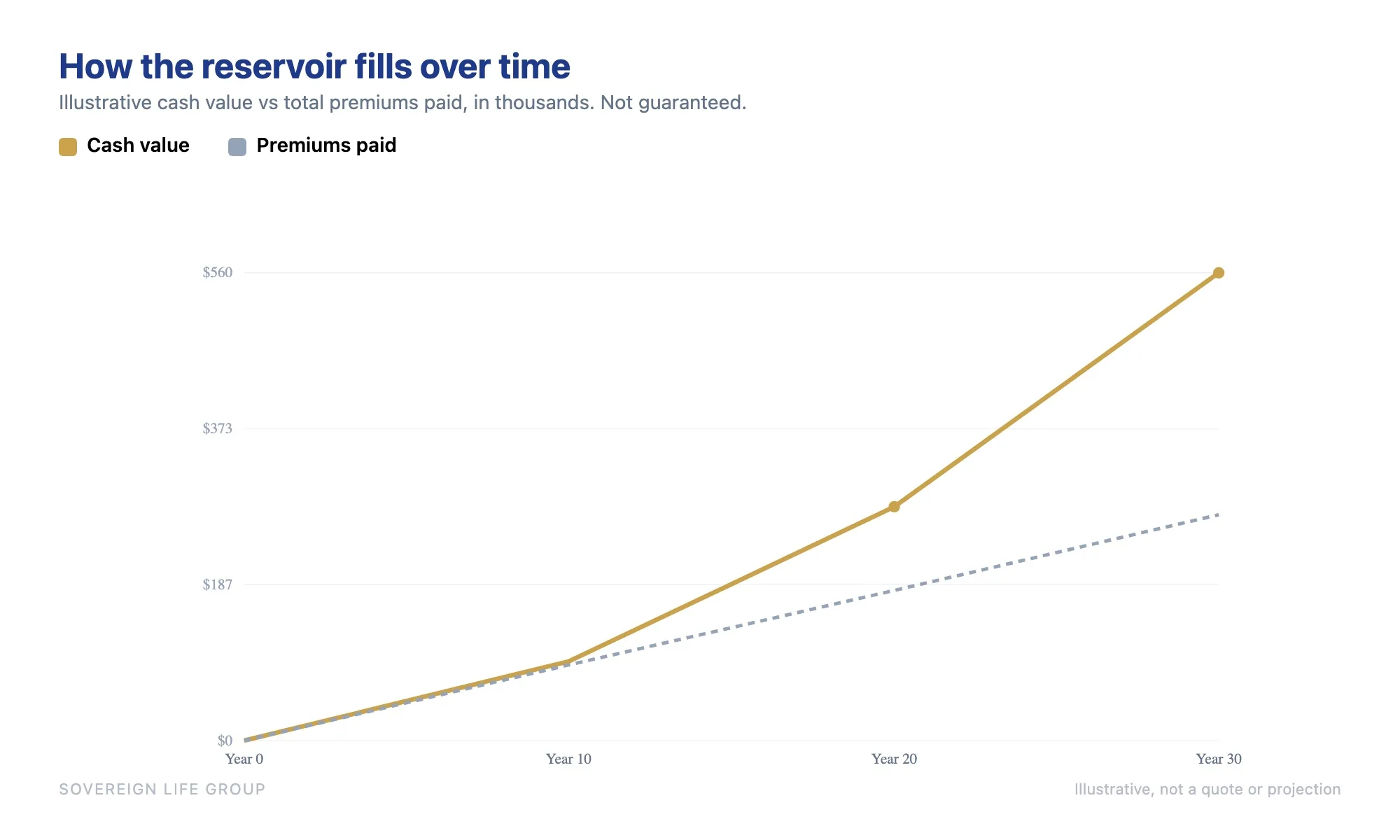

Here is the part people find hard to believe until they see it drawn out. Every time you pay a premium, part of it buys the insurance and part of it goes into your cash value, where it compounds. In the early years most of the money is doing the work of insurance, so the cash value grows slowly. That is the honest truth the glossy ads leave out. A cash value policy is a slow starter. Give it time, though, and the compounding tips in your favor.

You do not have to wait for the reservoir to fill before you can use it. Once there is meaningful value inside, you can take a policy loan against it. The insurer lends you money using your cash value as collateral, so your own pool keeps growing while you put the borrowed cash to work elsewhere. You repay on your own schedule, and the interest travels back toward your policy instead of to an outside bank. That is the whole "be your own bank" idea in one paragraph.

Two honest cautions before we go on. First, those numbers are illustrative, and a real policy depends on the product, the design, and, for indexed policies, how the underlying index performs inside the policy's limits. Anyone who shows you a smooth, guaranteed climb for thirty years is selling, not advising. Second, borrowing is a privilege you can abuse. Loans left unpaid eat into the death benefit, and a policy drained carelessly can even lapse. Treated with respect, the reservoir is a quiet advantage. Treated like a slot machine, it fails like anything else.

Look again at that line. The one that starts underwater and then pulls ahead is the entire strategy in a single picture. It rewards patience, and it quietly punishes anyone who expected a quick win. Which brings us to the part the sales pages tend to rush past.

The honest trade-offs

A permanent policy costs more than term for the same death benefit, because you are funding the bank as well as the coverage. The cash value takes years to build into anything meaningful, so this is a long game, not a quick one. A policy loan you never pay back reduces the death benefit your family receives, dollar for dollar. And the policy has to be structured with care to avoid becoming what the tax code calls a modified endowment contract, which would strip away some of the tax advantages. None of this makes it a bad tool. It makes it a tool you have to use on purpose.

There are two common flavors of the engine. Whole life offers steady, guaranteed cash value growth at a modest rate, which suits people who want certainty above all. Indexed universal life ties its growth to a market index, with a floor that limits losses and a cap that limits gains, trading more upside potential for more moving parts. Neither is universally better. The right one depends on your goals, your budget, and how much you value a guarantee over a maybe.

Used well, a family bank is a patient, tax-advantaged way to protect your family today and build a pool you can borrow from for the rest of your life. Used carelessly, or bought on the strength of a rosy illustration, it can disappoint. The entire difference is understanding the machine before you switch it on, which is exactly where we are headed next.

For educational purposes only. Not financial, tax, or legal advice, and not a recommendation of any specific product. Historical accounts are illustrative and not a promise of any result. Life insurance is offered through licensed agents; policies have costs, are not bank accounts, and are not FDIC insured. Joseph McDermott is a licensed life insurance agent (NPN 22121673), brokered through Family First Life. Consult a licensed professional, a tax advisor, and an estate attorney before acting.