The Vanderbilts left their children a fortune. The Rockefellers left their children a machine. That one word is the whole difference between a family that is still wealthy six generations later and a family that gathered 120 strong in 1973 with not one millionaire in the room.

So let's take the machine apart and see what actually makes it run. It is far simpler than the mystique around it suggests, and every piece of it is within reach of a normal family on a normal income. Forget the oil wells and the railroads for a minute, because the interesting part was never how these families made their money. It was what they did with it once it was made, and that part came down to a structure they built on purpose.

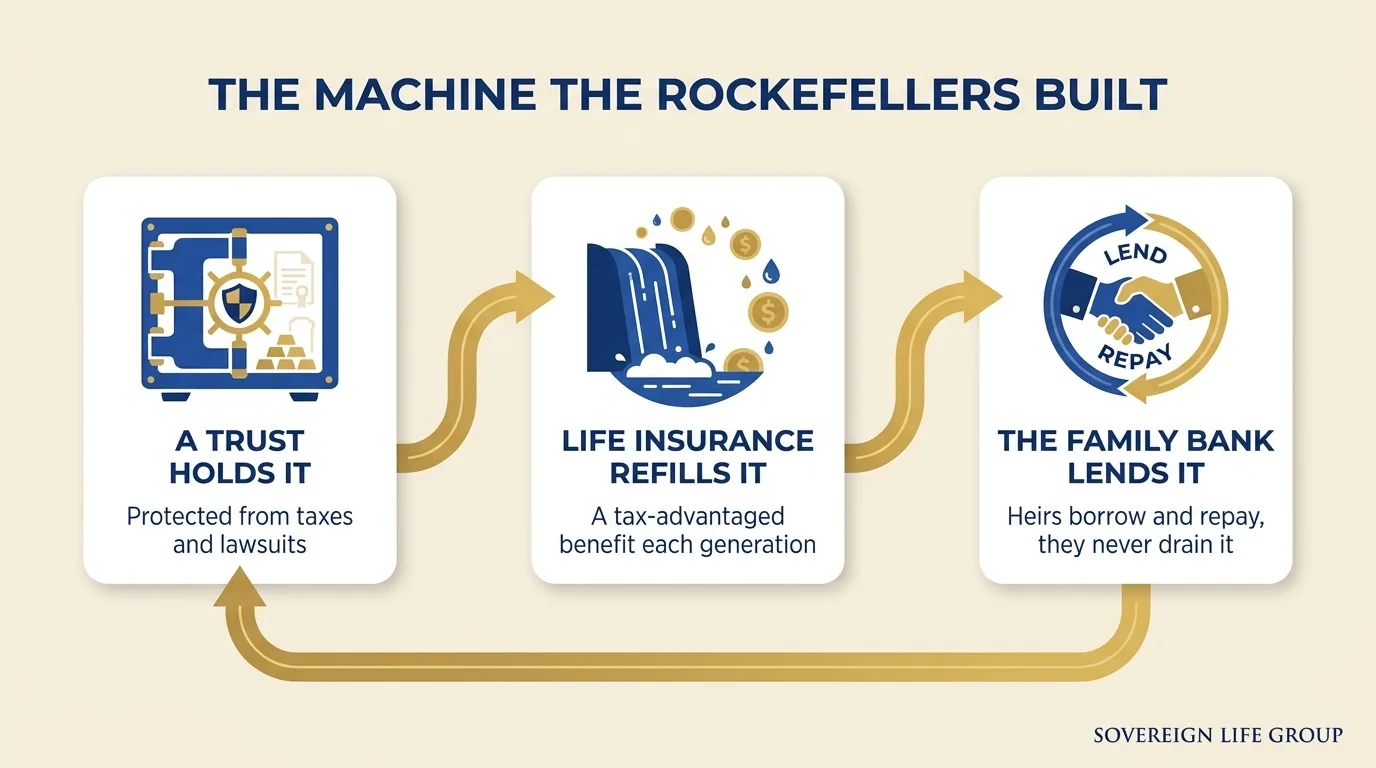

Three parts, working together

Strip away the private banks and the family offices and the Rockefeller machine comes down to three moving parts. Each one covers a weakness in the other two, which is exactly why it holds up over a hundred years instead of falling apart in thirty.

First, a trust holds the money. That keeps it out of reach of unnecessary taxes, of lawsuits, and of the occasional heir who would happily spend the whole thing on a boat. Second, life insurance refills the trust. When a family member dies, a large and generally income-tax-free death benefit flows in and tops the reservoir back up, so the pool the next generation inherits is as full as the one before it. Third, one plain rule governs everything. The family borrows from the pot. It does not empty it. Heirs take loans from their own bank to buy a home or start a business, then pay the money back with interest that stays inside the family instead of going to an outside lender.

Notice that no single part carries the whole load. The trust protects the money but does not grow it. The lending rule keeps the pool intact but does not fill it. Life insurance is the piece that quietly puts water back into the reservoir every time the family loses a member, which is the one event you can count on eventually happening to all of us. Pull that engine out and the machine slowly grinds to a halt. That, in a single sentence, is the Vanderbilt story.

The proof is in the line

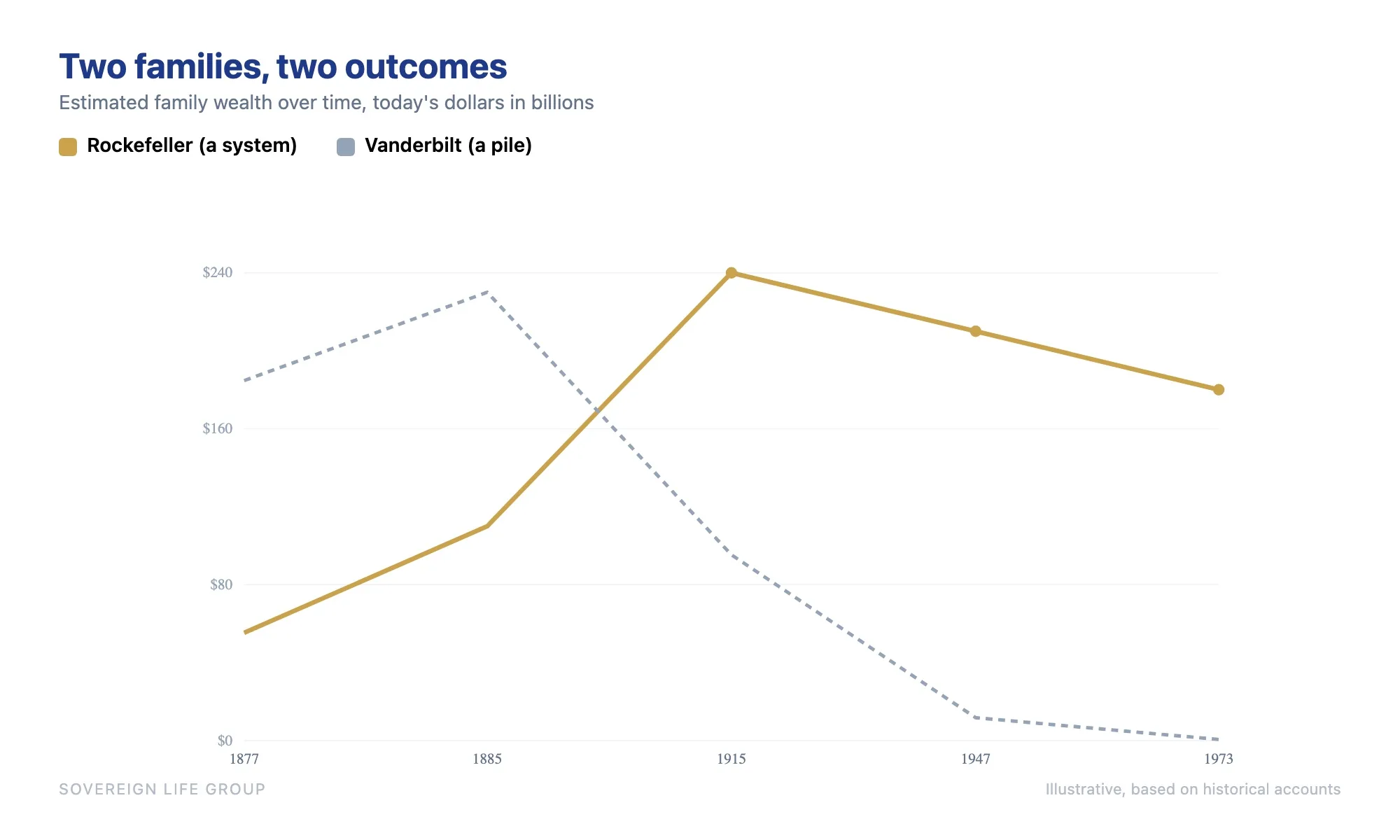

John D. Rockefeller built the first American fortune worth a billion dollars, most of it out of Standard Oil. He could have handed it down as a pile, the way the Commodore did. Instead he and the advisors who followed him built the reservoir, and each generation kept refilling it. More than a century and roughly seven generations later, the family still runs a shared office to manage its money, and the Rockefeller name still means much of what it meant in 1900.

Put the two families on the same chart and you do not need a finance degree to read it.

Same country. Same century. Similar fortunes at the start. One family built a system and watched their line hold its height. The other left a pile and watched it fall off a cliff. Nothing about the Rockefellers was luckier than the Vanderbilts. They were simply more deliberate about what happened to the money after they were gone.

You could point out that the Rockefellers had far more to work with, and they did. But scale is not the lesson. A family with a thousandth of their fortune can run the very same playbook, on the very same principles, and bend their own line in the same direction. The size of the reservoir changes from one family to the next. The plumbing does not.

They were not the only ones

The Rockefellers were not a fluke. Joseph P. Kennedy set up trusts in the 1930s that quietly funded his children's lives and campaigns for decades. The Rothschilds built a banking family that kept its capital inside the bloodline across borders and generations. Different names, same three habits. Hold it, refill it, lend it, and never let the pot run dry.

A trust is discipline you can hire. The engine that refills it is a product you can buy.

Here is the part that should get your attention. None of these families used a secret you cannot get to. A trust is available to anyone who asks an attorney to draw one up. The lending rule is not a product at all, it is just discipline. And the engine that refills the whole thing, the one part doing the quiet heavy lifting, is life insurance. Not a hedge fund. Not a lucky startup. A product you can buy this month, on an ordinary income, from a licensed agent.

That is the good news buried under all the dynasty talk. The Rockefellers did not own a tool you are locked out of. They had a habit and an engine, and both are for sale to any family that decides it wants its money to outlast it. You do not need their fortune to begin. You need their blueprint, scaled to your life. So in the next chapter we start with the engine itself, and the very ordinary product that powers it.

For educational purposes only. Not financial, tax, or legal advice, and not a recommendation of any specific product. Historical accounts are illustrative and not a promise of any result. Life insurance is offered through licensed agents; policies have costs, are not bank accounts, and are not FDIC insured. Joseph McDermott is a licensed life insurance agent (NPN 22121673), brokered through Family First Life. Consult a licensed professional, a tax advisor, and an estate attorney before acting.